Macy's Boston Consulting Group Matrix

Visual. Strategic. Downloadable.

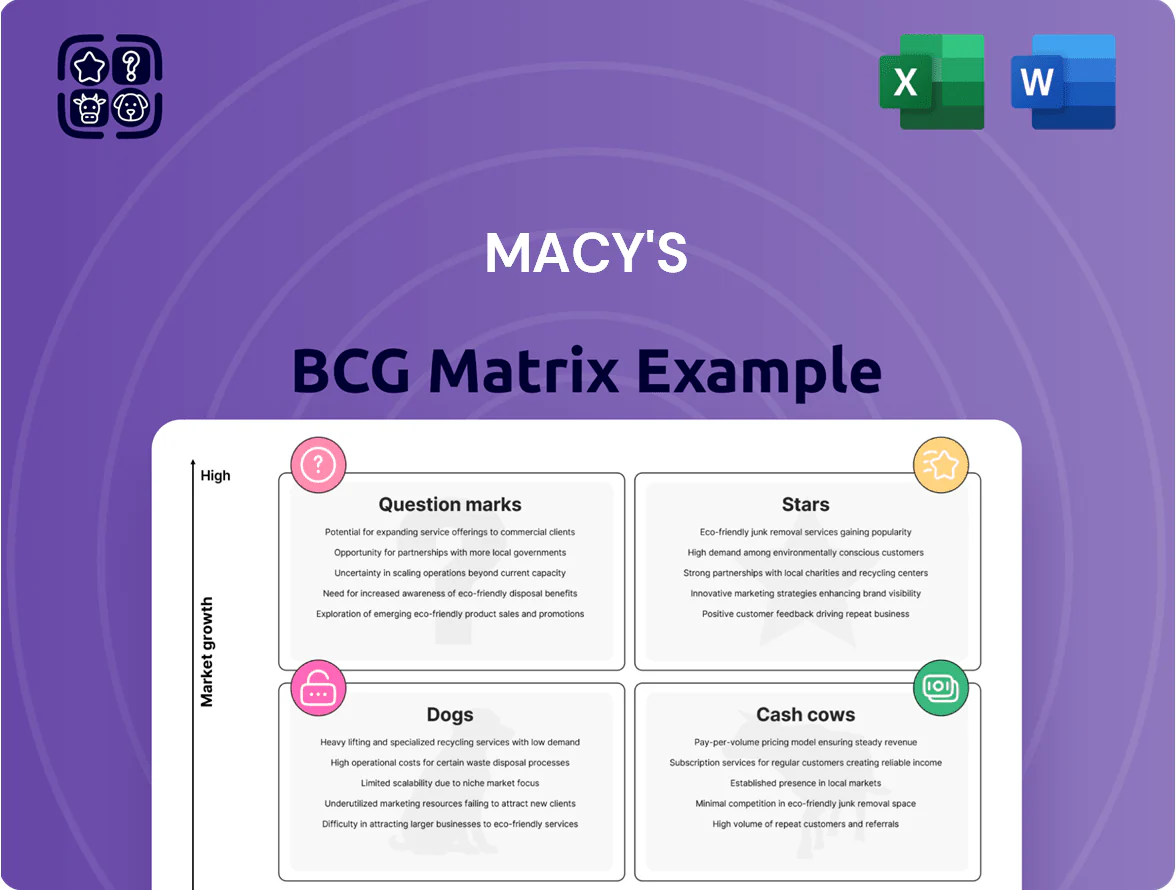

Macy’s BCG Matrix preview highlights how its department-store segments likely split between Cash Cows (established apparel and home goods), Question Marks (digital and off-mall initiatives), and potential Dogs (underperforming specialty lines), signaling where management should milk, invest, or divest. This snapshot teases strategic priorities but leaves out granular quadrant placements, revenue-share data, and tactical moves—purchase the full BCG Matrix for a complete Word report and Excel summary with actionable recommendations to optimize Macy’s portfolio and capital allocation.

Stars

Bloomingdale's Luxury Banner

Bloomingdale's sits in Macy's BCG Matrix as a Star, driving 9.0% comparable sales growth in late 2025 and outpacing the parent chain; nearly 50% of its customers have household incomes above $100,000, concentrating share in premium-to-luxury segments.

Macy's is funding Bloomingdale's expansion with plans for 15 new stores and stepped-up digital investment in 2025–26 to sustain market share gains and conversion among high-value shoppers.

Bluemercury Beauty Retailer

Bluemercury remains a Star in Macy's BCG matrix, posting its 19th straight quarter of comparable sales growth as of Q4 2025 and outpacing Macy's core by ~600 basis points in same-store sales growth.

Macy's is funding a New Blue transformation, modernizing 39 stores and budgeting roughly $60–80 million for upgrades while planning 30 net new Bluemercury openings over 2026–2028 to capture the $50+ billion global prestige beauty market.

The banner burns capital for rapid expansion and store resets but delivers steady market-share gains in luxury skincare and cosmetics, supporting higher average transaction values and gross margins versus department-store apparel.

Reimagine 125 Go-Forward Stores

The Reimagine 125 Go-Forward stores are Stars in Macy's BCG Matrix: they delivered 2.7% comparable sales growth in 2024 vs a -1.2% fleet average, showing clear high-growth potential.

Macy's prioritizes these units with higher staffing, localized events, and premium merchandise, accounting for roughly $1.1B in annual sales and outsized margin contribution.

By focusing capex and marketing on these 125 stores, Macy's aims to convert them into primary cash generators under the Bold New Chapter, targeting mid-single-digit comp growth and margin expansion.

Macy's Marketplace Expansion

The Macy's digital marketplace is a Star in the BCG Matrix, scaling assortment fast and adding third-party SKUs without inventory cost, helping the company regain share in e-commerce.

The platform drove Macy's strongest digital performance in 13 quarters, with marketplace GMV up 28% year-over-year in FY2024 and contribuing to a 14% rise in online sales; AI personalization lifted AOV and repeat rates.

It needs continued tech spend and marketing to sustain growth, but the marketplace enables high-velocity category expansion and is central to Macy's omnichannel push against digital-native rivals.

- Market share gain: marketplace GMV +28% (FY2024)

- Online sales boost: +14% YoY (FY2024)

- Benefit: no inventory overhead, faster SKU growth

- Cost: ongoing tech and promo investment

Small-Format Store Pilots

Macy's small-format stores are Stars: launched in 2023–25 to target suburban neighborhood centers, they are gaining rapid local market share and posting NPS ~10–15 points higher than legacy mall stores as of 2025.

Capital reallocation: Macy's diverted roughly $200–300 million from mall closures into rollout through 2024–25, and same-store sales for small formats rose ~8–12% year-over-year in tested markets.

If scaling continues at current pace—opening ~100 stores by end-2026—these efficient, high-touch formats are likely to become Macy's primary physical footprint.

- Higher NPS: +10–15 points vs malls

- Capex reallocated: $200–300M (2024–25)

- S/S sales growth: +8–12% YoY in pilots

- Target scale: ~100 stores by 2026

Omnichannel surge: Bloomingdale’s, Bluemercury, marketplace & small-format fuel strong growth

Stars: Bloomingdale's, Bluemercury, Reimagine 125 stores, digital marketplace, and small-format units drive high growth and margin; examples—Bloomingdale's comp +9.0% (late 2025), Bluemercury 19th straight quarter growth (Q4 2025), marketplace GMV +28% FY2024, small-format S/S +8–12% pilots.

| Asset | Key metric |

|---|---|

| Bloomingdale's | +9.0% comp (late 2025) |

| Bluemercury | 19 quarters growth (Q4 2025) |

| Marketplace | GMV +28% FY2024 |

| Small-format | S/S +8–12% pilots |

What is included in the product

Comprehensive BCG Matrix of Macy’s: quadrant-by-quadrant analysis with strategic actions, competitive factors, and investment/divestment recommendations.

One-page Macy's BCG Matrix placing each business unit in a quadrant for quick strategic decisions

Cash Cows

Core Macy's Nameplate (Go-Forward)

The 350 go-forward Macy's nameplate stores act as the company's primary Cash Cow, producing the bulk of Macy's $21.4 billion in 2024 net sales and funding operations. With the U.S. department store market largely mature and same-store sales growth low (around 1–2% in 2024), these locations supply steady free cash flow for luxury expansion and interest payments on roughly $2.1 billion in net debt. Macy's is milking these assets by tightening inventory turns to ~4.5x and cutting SG&A to improve adjusted operating margin near 7–8%. As stable market leaders, the nameplate stores underpin capital allocation for new initiatives and omnichannel investments.

Private Label Brands Portfolio

Macy's private-label portfolio, led by I.N.C. and Charter Club, functions as a Cash Cow by delivering higher gross margins than national brands in a mature apparel segment; in 2025 these labels are projected to represent 25% of Macy's $17.3B sales (≈$4.33B), with several individual labels exceeding $1B each.

Credit Card and Financial Services

Macy's credit card operations and proprietary financial services are Cash Cows, with 'other revenue' up 26% year-over-year in Q1 2025, driven by card fees and interest income; this segment produced roughly $350–$450 million in operating profit in 2024–2025, funding dividends and buybacks.

Real Estate Asset Monetization

Macy’s owned real estate, led by Herald Square, acts as a passive Cash Cow via strategic monetization, generating steady cash without operational growth.

In 2025 Macy’s targeted $190 million from asset monetization to boost liquidity and fund investments into Stars like Bluemercury, supporting the Bold New Chapter.

These property proceeds shore up the balance sheet, lower leverage, and provide capital for reinvestment and shareholder returns.

- Owned real estate = recurring cash source

- $190M target in 2025 proceeds

- Funds Bluemercury and Bold New Chapter

- Improves liquidity, reduces leverage

Legacy Giftable Categories

Core giftable categories—sweaters, pajamas, handbags—act as Macy’s Cash Cows, driving high seasonal demand and selling close to full price; in FY2024 Macy’s reported apparel and accessories comps up ~6.2% in holiday months, with Coach accounting for a material share of handbag sales.

These mature categories keep steady market share, cut promotional spend due to ingrained buying habits, and deliver reliable holiday cash inflows—Macy’s holiday gross margin expanded ~130 bps in 2024 versus 2023 thanks partly to lower markdown rates.

- High seasonal demand: sweaters, pajamas, handbags

- Full-price sales: reduced markdowns; +130 bps holiday GM (2024)

- Brand pull: Coach and national brands boost share

- Lower promo spend: steady consumer habits

Macy’s Power Engines: $21.4B stores, $4.3B private labels, $350–450M card profit

Macy’s Cash Cows: 350 nameplate stores drove ~$21.4B sales (2024) and ~7–8% adj. operating margin; private labels ~25% of Macy’s $17.3B core sales (2025 ≈ $4.33B); credit card ops ~$350–450M operating profit (2024–25); targeted $190M asset monetization (2025) to fund Bluemercury.

| Asset | Key 2024–25 |

|---|---|

| Nameplate stores | $21.4B sales; 7–8% op. margin |

| Private labels | 25% core sales ≈ $4.33B (2025) |

| Credit ops | $350–450M op. profit |

| Real estate | $190M monetization target (2025) |

What You See Is What You Get

Macy's BCG Matrix

The file you're previewing is the exact Macy's BCG Matrix report you’ll receive after purchase—fully formatted, market-informed, and free of watermarks or demo content. This final version is ready for immediate download, editing, printing, or presentation to stakeholders. Crafted by strategy professionals for clarity and actionable insight, it requires no revisions or hidden add-ons. Purchase unlocks the same document shown here for use in planning, reporting, or client deliverables.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Visual. Strategic. Downloadable.

Macy’s BCG Matrix preview highlights how its department-store segments likely split between Cash Cows (established apparel and home goods), Question Marks (digital and off-mall initiatives), and potential Dogs (underperforming specialty lines), signaling where management should milk, invest, or divest. This snapshot teases strategic priorities but leaves out granular quadrant placements, revenue-share data, and tactical moves—purchase the full BCG Matrix for a complete Word report and Excel summary with actionable recommendations to optimize Macy’s portfolio and capital allocation.

Stars

Bloomingdale's Luxury Banner

Bloomingdale's sits in Macy's BCG Matrix as a Star, driving 9.0% comparable sales growth in late 2025 and outpacing the parent chain; nearly 50% of its customers have household incomes above $100,000, concentrating share in premium-to-luxury segments.

Macy's is funding Bloomingdale's expansion with plans for 15 new stores and stepped-up digital investment in 2025–26 to sustain market share gains and conversion among high-value shoppers.

Bluemercury Beauty Retailer

Bluemercury remains a Star in Macy's BCG matrix, posting its 19th straight quarter of comparable sales growth as of Q4 2025 and outpacing Macy's core by ~600 basis points in same-store sales growth.

Macy's is funding a New Blue transformation, modernizing 39 stores and budgeting roughly $60–80 million for upgrades while planning 30 net new Bluemercury openings over 2026–2028 to capture the $50+ billion global prestige beauty market.

The banner burns capital for rapid expansion and store resets but delivers steady market-share gains in luxury skincare and cosmetics, supporting higher average transaction values and gross margins versus department-store apparel.

Reimagine 125 Go-Forward Stores

The Reimagine 125 Go-Forward stores are Stars in Macy's BCG Matrix: they delivered 2.7% comparable sales growth in 2024 vs a -1.2% fleet average, showing clear high-growth potential.

Macy's prioritizes these units with higher staffing, localized events, and premium merchandise, accounting for roughly $1.1B in annual sales and outsized margin contribution.

By focusing capex and marketing on these 125 stores, Macy's aims to convert them into primary cash generators under the Bold New Chapter, targeting mid-single-digit comp growth and margin expansion.

Macy's Marketplace Expansion

The Macy's digital marketplace is a Star in the BCG Matrix, scaling assortment fast and adding third-party SKUs without inventory cost, helping the company regain share in e-commerce.

The platform drove Macy's strongest digital performance in 13 quarters, with marketplace GMV up 28% year-over-year in FY2024 and contribuing to a 14% rise in online sales; AI personalization lifted AOV and repeat rates.

It needs continued tech spend and marketing to sustain growth, but the marketplace enables high-velocity category expansion and is central to Macy's omnichannel push against digital-native rivals.

- Market share gain: marketplace GMV +28% (FY2024)

- Online sales boost: +14% YoY (FY2024)

- Benefit: no inventory overhead, faster SKU growth

- Cost: ongoing tech and promo investment

Small-Format Store Pilots

Macy's small-format stores are Stars: launched in 2023–25 to target suburban neighborhood centers, they are gaining rapid local market share and posting NPS ~10–15 points higher than legacy mall stores as of 2025.

Capital reallocation: Macy's diverted roughly $200–300 million from mall closures into rollout through 2024–25, and same-store sales for small formats rose ~8–12% year-over-year in tested markets.

If scaling continues at current pace—opening ~100 stores by end-2026—these efficient, high-touch formats are likely to become Macy's primary physical footprint.

- Higher NPS: +10–15 points vs malls

- Capex reallocated: $200–300M (2024–25)

- S/S sales growth: +8–12% YoY in pilots

- Target scale: ~100 stores by 2026

Omnichannel surge: Bloomingdale’s, Bluemercury, marketplace & small-format fuel strong growth

Stars: Bloomingdale's, Bluemercury, Reimagine 125 stores, digital marketplace, and small-format units drive high growth and margin; examples—Bloomingdale's comp +9.0% (late 2025), Bluemercury 19th straight quarter growth (Q4 2025), marketplace GMV +28% FY2024, small-format S/S +8–12% pilots.

| Asset | Key metric |

|---|---|

| Bloomingdale's | +9.0% comp (late 2025) |

| Bluemercury | 19 quarters growth (Q4 2025) |

| Marketplace | GMV +28% FY2024 |

| Small-format | S/S +8–12% pilots |

What is included in the product

Comprehensive BCG Matrix of Macy’s: quadrant-by-quadrant analysis with strategic actions, competitive factors, and investment/divestment recommendations.

One-page Macy's BCG Matrix placing each business unit in a quadrant for quick strategic decisions

Cash Cows

Core Macy's Nameplate (Go-Forward)

The 350 go-forward Macy's nameplate stores act as the company's primary Cash Cow, producing the bulk of Macy's $21.4 billion in 2024 net sales and funding operations. With the U.S. department store market largely mature and same-store sales growth low (around 1–2% in 2024), these locations supply steady free cash flow for luxury expansion and interest payments on roughly $2.1 billion in net debt. Macy's is milking these assets by tightening inventory turns to ~4.5x and cutting SG&A to improve adjusted operating margin near 7–8%. As stable market leaders, the nameplate stores underpin capital allocation for new initiatives and omnichannel investments.

Private Label Brands Portfolio

Macy's private-label portfolio, led by I.N.C. and Charter Club, functions as a Cash Cow by delivering higher gross margins than national brands in a mature apparel segment; in 2025 these labels are projected to represent 25% of Macy's $17.3B sales (≈$4.33B), with several individual labels exceeding $1B each.

Credit Card and Financial Services

Macy's credit card operations and proprietary financial services are Cash Cows, with 'other revenue' up 26% year-over-year in Q1 2025, driven by card fees and interest income; this segment produced roughly $350–$450 million in operating profit in 2024–2025, funding dividends and buybacks.

Real Estate Asset Monetization

Macy’s owned real estate, led by Herald Square, acts as a passive Cash Cow via strategic monetization, generating steady cash without operational growth.

In 2025 Macy’s targeted $190 million from asset monetization to boost liquidity and fund investments into Stars like Bluemercury, supporting the Bold New Chapter.

These property proceeds shore up the balance sheet, lower leverage, and provide capital for reinvestment and shareholder returns.

- Owned real estate = recurring cash source

- $190M target in 2025 proceeds

- Funds Bluemercury and Bold New Chapter

- Improves liquidity, reduces leverage

Legacy Giftable Categories

Core giftable categories—sweaters, pajamas, handbags—act as Macy’s Cash Cows, driving high seasonal demand and selling close to full price; in FY2024 Macy’s reported apparel and accessories comps up ~6.2% in holiday months, with Coach accounting for a material share of handbag sales.

These mature categories keep steady market share, cut promotional spend due to ingrained buying habits, and deliver reliable holiday cash inflows—Macy’s holiday gross margin expanded ~130 bps in 2024 versus 2023 thanks partly to lower markdown rates.

- High seasonal demand: sweaters, pajamas, handbags

- Full-price sales: reduced markdowns; +130 bps holiday GM (2024)

- Brand pull: Coach and national brands boost share

- Lower promo spend: steady consumer habits

Macy’s Power Engines: $21.4B stores, $4.3B private labels, $350–450M card profit

Macy’s Cash Cows: 350 nameplate stores drove ~$21.4B sales (2024) and ~7–8% adj. operating margin; private labels ~25% of Macy’s $17.3B core sales (2025 ≈ $4.33B); credit card ops ~$350–450M operating profit (2024–25); targeted $190M asset monetization (2025) to fund Bluemercury.

| Asset | Key 2024–25 |

|---|---|

| Nameplate stores | $21.4B sales; 7–8% op. margin |

| Private labels | 25% core sales ≈ $4.33B (2025) |

| Credit ops | $350–450M op. profit |

| Real estate | $190M monetization target (2025) |

What You See Is What You Get

Macy's BCG Matrix

The file you're previewing is the exact Macy's BCG Matrix report you’ll receive after purchase—fully formatted, market-informed, and free of watermarks or demo content. This final version is ready for immediate download, editing, printing, or presentation to stakeholders. Crafted by strategy professionals for clarity and actionable insight, it requires no revisions or hidden add-ons. Purchase unlocks the same document shown here for use in planning, reporting, or client deliverables.