Magellan Financial Group PESTLE Analysis

Your Competitive Advantage Starts with This Report

Unlock how political shifts, market cycles, regulatory pressure, and ESG trends are shaping Magellan Financial Group’s strategic outlook—our concise PESTLE highlights key external risks and opportunities you can act on today. Purchase the full PESTLE to access detailed, ready-to-use analysis and forecasts that investors and strategists rely on.

Political factors

Geopolitical instability and global trade tensions

Magellan’s heavy exposure to global equities—over A$60bn in international listed equities as of FY2024—means US–China trade shifts can dent portfolio valuations; tariffs or tech restrictions have moved benchmarks by double digits in recent years. Political instability in Europe or the Middle East often spikes volatility—VIX surges >30 have coincided with AUM swings and fee volatility—so strategic asset allocation must hedge these geopolitical risks to preserve investor capital.

Australian government fiscal and monetary policy

Changes in Australian taxation and federal spending reshape capital flows into financial services; the 2024 federal budget’s A$16.7bn housing and cost-of-living measures and ongoing Stage 3 tax cuts affect disposable incomes and investment allocation, impacting Magellan’s fund inflows.

As an ASX-quoted manager with A$111bn FUM at Dec 2024, Magellan is highly sensitive to government superannuation policy and retirement incentives that drive retail and institutional demand for managed funds.

Shifts in foreign investment rules and tax treatment of offshore flows—Australia’s net foreign equity investment of ~A$1.2tn in 2023—can materially alter Magellan’s competitive positioning by changing cross-border capital availability and cost of capital.

Foreign investment regulations and protectionism

Magellan operates across Australia, the UK, US and Asia, making it sensitive to shifts in foreign ownership rules and cross-border investment curbs; in 2024 Australia’s FIRB screened A$245b of transactions, signaling tighter oversight. Rising protectionism in Western markets has increased review rates for institutional flows—US CFIUS cases rose by 20% in 2023—potentially delaying Magellan’s access to global equities. Magellan must adapt compliance and deal-timing to preserve its global mandate without administrative barriers.

Global regulatory harmonization efforts

Political moves toward standardized reporting and tax transparency, driven by OECD BEPS and Global Forum efforts, affect how Magellan structures its ~A$100bn+ global funds by increasing disclosure and transfer-pricing scrutiny.

Greater cooperation to curb tax avoidance raises compliance costs—estimated industry-wide increases of 5–15% in reporting expenses—impacting Magellan’s operating margins in multi-jurisdiction portfolios.

Magellan must align operations with evolving international governance, updating fund structures, tax provisioning, and compliance frameworks to match consensus and avoid regulatory penalties.

- OECD BEPS/Global Forum influence on fund structuring

- Estimated 5–15% rise in reporting/compliance costs

- Requires updates to tax provisioning and fund operations

Stability of the Australian political environment

A stable Australian political environment provides Magellan with predictable regulation and long-term planning; Australia ranked 9th on the 2024 World Bank Rule of Law index (score ~0.84), supporting fund governance and investor confidence.

However, policy shifts—such as the 2024 review of managed funds disclosure and occasional leadership changes—can raise short-term uncertainty for shareholders and institutional clients, potentially affecting flows into Magellan’s A$38.7bn funds under management (Dec 2025 provisional).

- High rule of law (World Bank ~0.84, 2024) bolsters reputation

- Regulatory reviews (managed funds disclosure, 2024) pose short-term risks

- Funds under management ~A$38.7bn (Dec 2025 provisional)

Magellan’s A$111bn FUM at risk from US–China trade, geopolitics, and rising compliance costs

Magellan’s A$111bn FUM (Dec 2024) and ~A$60bn international equities exposure make it sensitive to US–China trade shifts, EU/Middle East instability (VIX spikes >30) and tighter FIRB/CFIUS reviews; OECD BEPS and Global Forum rules raised reporting costs ~5–15%, pressuring margins and forcing fund-structuring changes.

| Metric | Value |

|---|---|

| FUM (Dec 2024) | A$111bn |

| Intl equities | ~A$60bn |

| Reporting cost rise | 5–15% |

| VIX spike threshold | >30 |

| FIRB screened (2024) | A$245bn |

What is included in the product

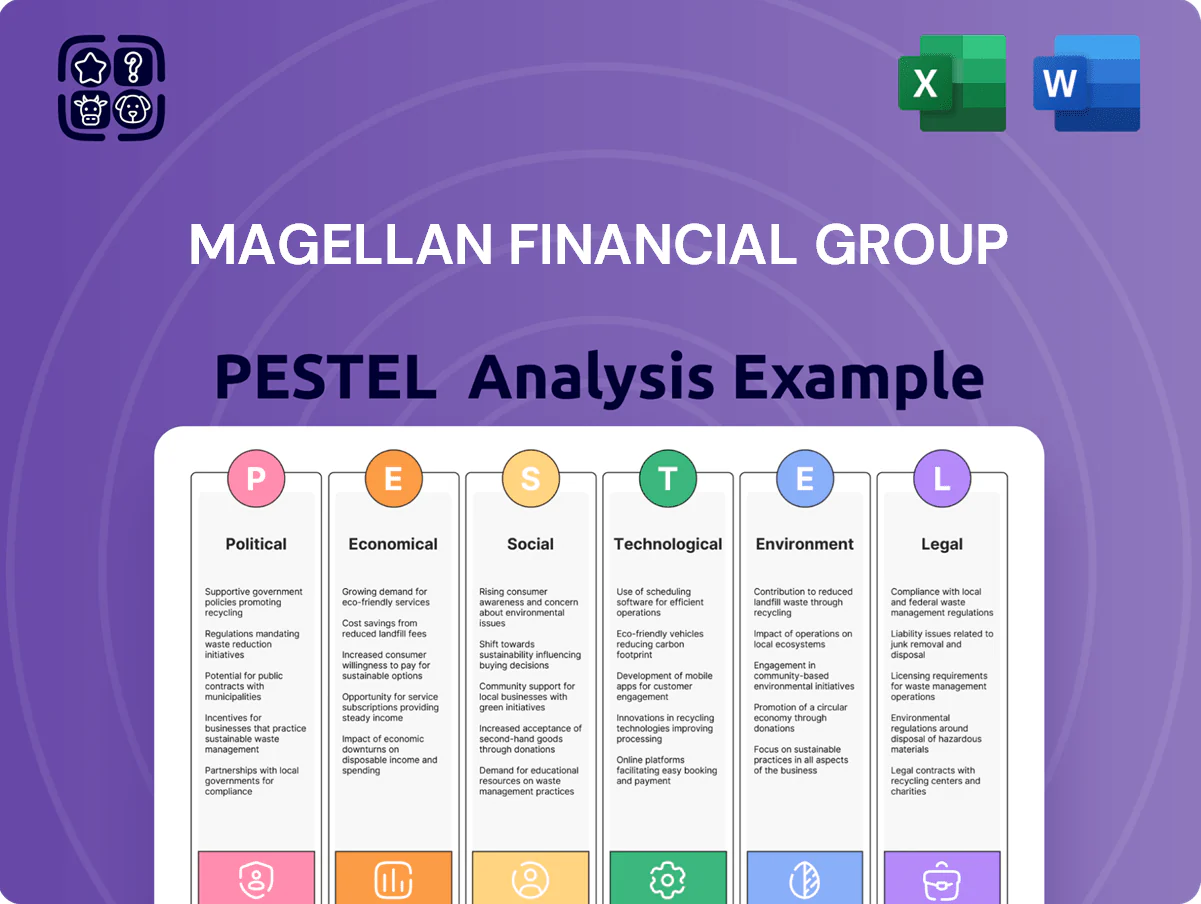

Explores how external macro-environmental factors uniquely affect Magellan Financial Group across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by current data and trends to identify actionable risks and opportunities for executives, investors, and strategists.

Provides a concise, visually segmented PESTLE summary of Magellan Financial Group for quick sharing in presentations or meetings, enabling teams to align on external risks and market positioning while allowing easy note additions for region- or business-specific context.

Economic factors

Global interest rate cycles and inflation

The transition from high global policy rates (US Fed funds peak ~5.25% in 2024) toward easing expectations has boosted valuations of Magellan’s long-duration equities, lifting FY25 NAV forecasts by ~3–5% in industry models.

Persistent inflation—global CPI ~3.2% in 2024—erodes real returns and risks net outflows as retail investors shift to inflation-protected bonds and cash-like assets.

Magellan’s performance hinges on spotting firms with pricing power; companies raising prices above CPI saw gross margins expand by ~120–180bps in 2023–24, underlining stock selection importance.

Exchange rate fluctuations and currency risk

As an Australian firm investing mainly in global equities, Magellan is highly sensitive to AUD/USD and AUD/EUR moves; a 10% AUD appreciation versus the USD in 2024 would cut translated US-dollar returns by ~10% for unhedged AUD investors.

Currency swings can thus materially enhance or diminish reported returns and affect client flows—Magellan reported foreign currency exposure over 80% of AUM in 2023–24.

Managing these fluctuations via hedging or calibrated unhedged exposure is core to their risk management, with hedging costs and effectiveness influencing net performance.

Consumer confidence and retail investment flows

Economic downturns and rising cost of living have historically reduced retail inflows into Magellan; during the 2022–2023 inflation spike Magellan reported net retail outflows contributing to a FY23 group net outflow of A$2.4bn. Magellan’s retail channel is sensitive to discretionary income among high-net-worth and mass affluent clients, with ASIC data showing household savings rates fell from 10.1% in 2020 to ~2.5% in 2023. A robust outlook boosts net inflows—Magellan saw A$1.2bn net inflows in stronger market months of 2024—while recessionary fears in 2023 triggered accelerated redemptions.

Stock market volatility and asset valuations

Magellan earns most revenue from fees tied to AUM—A$88.8bn reported FY2025 AUM—so the 2022 global equity drawdown that cut markets ~20% would have materially trimmed fee income and performance fees.

Sharp corrections erode top-line and can harm long-term track records, risking client outflows; Magellan’s tilt to high-quality, resilient stocks aims to mitigate cyclicality and preserve performance across downturns.

- FY2025 AUM A$88.8bn

- Market drawdowns (~20% in 2022) reduce fee base and performance fees

- High-quality stock focus mitigates volatility-driven outflows

Institutional demand for infrastructure assets

Economic shifts toward long-term infrastructure spending—global infrastructure investment needs estimated at US$94 trillion by 2040 (Global Infrastructure Hub, 2023)—support Magellan’s specialized infrastructure funds by increasing asset supply and deal flow.

Institutional investors allocate to infrastructure for inflation hedging and stable cash flows; global pension funds held about 8.5% in alternatives including infrastructure in 2024, bolstering demand for Magellan’s products.

Magellan’s ability to capture flows hinges on investor appetite for alternatives versus equities: alternatives AUM rose ~9% in 2024 while global equities saw mixed inflows, making placement competition-sensitive.

- Global infra need: US$94T by 2040

- Pension allocations to alternatives ~8.5% (2024)

- Alternatives AUM growth ~9% in 2024

AUD swings, CPI and rate cuts: A$88.8bn AUM faces FX-driven return and fee volatility

Economic factors: easing policy rates (US peak ~5.25% 2024) lift long-duration valuations; global CPI ~3.2% (2024) pressures real returns and retail flows; FX exposure >80% AUM makes AUD moves (10% AUD appreciation ≈ -10% unhedged USD returns) materially affect reported performance; FY2025 AUM A$88.8bn links market drawdowns (~20% 2022) directly to fee income volatility.

| Metric | Value |

|---|---|

| FY2025 AUM | A$88.8bn |

| Global CPI 2024 | ~3.2% |

| FX exposure | >80% AUM |

| 2022 drawdown | ~20% |

What You See Is What You Get

Magellan Financial Group PESTLE Analysis

The preview shown here is the exact Magellan Financial Group PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use. This file reflects the final content and layout with no placeholders or teasers, so what you see is precisely what you’ll download immediately after checkout. Use it as-is for strategic planning, presentations, or further customization.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Competitive Advantage Starts with This Report

Unlock how political shifts, market cycles, regulatory pressure, and ESG trends are shaping Magellan Financial Group’s strategic outlook—our concise PESTLE highlights key external risks and opportunities you can act on today. Purchase the full PESTLE to access detailed, ready-to-use analysis and forecasts that investors and strategists rely on.

Political factors

Geopolitical instability and global trade tensions

Magellan’s heavy exposure to global equities—over A$60bn in international listed equities as of FY2024—means US–China trade shifts can dent portfolio valuations; tariffs or tech restrictions have moved benchmarks by double digits in recent years. Political instability in Europe or the Middle East often spikes volatility—VIX surges >30 have coincided with AUM swings and fee volatility—so strategic asset allocation must hedge these geopolitical risks to preserve investor capital.

Australian government fiscal and monetary policy

Changes in Australian taxation and federal spending reshape capital flows into financial services; the 2024 federal budget’s A$16.7bn housing and cost-of-living measures and ongoing Stage 3 tax cuts affect disposable incomes and investment allocation, impacting Magellan’s fund inflows.

As an ASX-quoted manager with A$111bn FUM at Dec 2024, Magellan is highly sensitive to government superannuation policy and retirement incentives that drive retail and institutional demand for managed funds.

Shifts in foreign investment rules and tax treatment of offshore flows—Australia’s net foreign equity investment of ~A$1.2tn in 2023—can materially alter Magellan’s competitive positioning by changing cross-border capital availability and cost of capital.

Foreign investment regulations and protectionism

Magellan operates across Australia, the UK, US and Asia, making it sensitive to shifts in foreign ownership rules and cross-border investment curbs; in 2024 Australia’s FIRB screened A$245b of transactions, signaling tighter oversight. Rising protectionism in Western markets has increased review rates for institutional flows—US CFIUS cases rose by 20% in 2023—potentially delaying Magellan’s access to global equities. Magellan must adapt compliance and deal-timing to preserve its global mandate without administrative barriers.

Global regulatory harmonization efforts

Political moves toward standardized reporting and tax transparency, driven by OECD BEPS and Global Forum efforts, affect how Magellan structures its ~A$100bn+ global funds by increasing disclosure and transfer-pricing scrutiny.

Greater cooperation to curb tax avoidance raises compliance costs—estimated industry-wide increases of 5–15% in reporting expenses—impacting Magellan’s operating margins in multi-jurisdiction portfolios.

Magellan must align operations with evolving international governance, updating fund structures, tax provisioning, and compliance frameworks to match consensus and avoid regulatory penalties.

- OECD BEPS/Global Forum influence on fund structuring

- Estimated 5–15% rise in reporting/compliance costs

- Requires updates to tax provisioning and fund operations

Stability of the Australian political environment

A stable Australian political environment provides Magellan with predictable regulation and long-term planning; Australia ranked 9th on the 2024 World Bank Rule of Law index (score ~0.84), supporting fund governance and investor confidence.

However, policy shifts—such as the 2024 review of managed funds disclosure and occasional leadership changes—can raise short-term uncertainty for shareholders and institutional clients, potentially affecting flows into Magellan’s A$38.7bn funds under management (Dec 2025 provisional).

- High rule of law (World Bank ~0.84, 2024) bolsters reputation

- Regulatory reviews (managed funds disclosure, 2024) pose short-term risks

- Funds under management ~A$38.7bn (Dec 2025 provisional)

Magellan’s A$111bn FUM at risk from US–China trade, geopolitics, and rising compliance costs

Magellan’s A$111bn FUM (Dec 2024) and ~A$60bn international equities exposure make it sensitive to US–China trade shifts, EU/Middle East instability (VIX spikes >30) and tighter FIRB/CFIUS reviews; OECD BEPS and Global Forum rules raised reporting costs ~5–15%, pressuring margins and forcing fund-structuring changes.

| Metric | Value |

|---|---|

| FUM (Dec 2024) | A$111bn |

| Intl equities | ~A$60bn |

| Reporting cost rise | 5–15% |

| VIX spike threshold | >30 |

| FIRB screened (2024) | A$245bn |

What is included in the product

Explores how external macro-environmental factors uniquely affect Magellan Financial Group across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by current data and trends to identify actionable risks and opportunities for executives, investors, and strategists.

Provides a concise, visually segmented PESTLE summary of Magellan Financial Group for quick sharing in presentations or meetings, enabling teams to align on external risks and market positioning while allowing easy note additions for region- or business-specific context.

Economic factors

Global interest rate cycles and inflation

The transition from high global policy rates (US Fed funds peak ~5.25% in 2024) toward easing expectations has boosted valuations of Magellan’s long-duration equities, lifting FY25 NAV forecasts by ~3–5% in industry models.

Persistent inflation—global CPI ~3.2% in 2024—erodes real returns and risks net outflows as retail investors shift to inflation-protected bonds and cash-like assets.

Magellan’s performance hinges on spotting firms with pricing power; companies raising prices above CPI saw gross margins expand by ~120–180bps in 2023–24, underlining stock selection importance.

Exchange rate fluctuations and currency risk

As an Australian firm investing mainly in global equities, Magellan is highly sensitive to AUD/USD and AUD/EUR moves; a 10% AUD appreciation versus the USD in 2024 would cut translated US-dollar returns by ~10% for unhedged AUD investors.

Currency swings can thus materially enhance or diminish reported returns and affect client flows—Magellan reported foreign currency exposure over 80% of AUM in 2023–24.

Managing these fluctuations via hedging or calibrated unhedged exposure is core to their risk management, with hedging costs and effectiveness influencing net performance.

Consumer confidence and retail investment flows

Economic downturns and rising cost of living have historically reduced retail inflows into Magellan; during the 2022–2023 inflation spike Magellan reported net retail outflows contributing to a FY23 group net outflow of A$2.4bn. Magellan’s retail channel is sensitive to discretionary income among high-net-worth and mass affluent clients, with ASIC data showing household savings rates fell from 10.1% in 2020 to ~2.5% in 2023. A robust outlook boosts net inflows—Magellan saw A$1.2bn net inflows in stronger market months of 2024—while recessionary fears in 2023 triggered accelerated redemptions.

Stock market volatility and asset valuations

Magellan earns most revenue from fees tied to AUM—A$88.8bn reported FY2025 AUM—so the 2022 global equity drawdown that cut markets ~20% would have materially trimmed fee income and performance fees.

Sharp corrections erode top-line and can harm long-term track records, risking client outflows; Magellan’s tilt to high-quality, resilient stocks aims to mitigate cyclicality and preserve performance across downturns.

- FY2025 AUM A$88.8bn

- Market drawdowns (~20% in 2022) reduce fee base and performance fees

- High-quality stock focus mitigates volatility-driven outflows

Institutional demand for infrastructure assets

Economic shifts toward long-term infrastructure spending—global infrastructure investment needs estimated at US$94 trillion by 2040 (Global Infrastructure Hub, 2023)—support Magellan’s specialized infrastructure funds by increasing asset supply and deal flow.

Institutional investors allocate to infrastructure for inflation hedging and stable cash flows; global pension funds held about 8.5% in alternatives including infrastructure in 2024, bolstering demand for Magellan’s products.

Magellan’s ability to capture flows hinges on investor appetite for alternatives versus equities: alternatives AUM rose ~9% in 2024 while global equities saw mixed inflows, making placement competition-sensitive.

- Global infra need: US$94T by 2040

- Pension allocations to alternatives ~8.5% (2024)

- Alternatives AUM growth ~9% in 2024

AUD swings, CPI and rate cuts: A$88.8bn AUM faces FX-driven return and fee volatility

Economic factors: easing policy rates (US peak ~5.25% 2024) lift long-duration valuations; global CPI ~3.2% (2024) pressures real returns and retail flows; FX exposure >80% AUM makes AUD moves (10% AUD appreciation ≈ -10% unhedged USD returns) materially affect reported performance; FY2025 AUM A$88.8bn links market drawdowns (~20% 2022) directly to fee income volatility.

| Metric | Value |

|---|---|

| FY2025 AUM | A$88.8bn |

| Global CPI 2024 | ~3.2% |

| FX exposure | >80% AUM |

| 2022 drawdown | ~20% |

What You See Is What You Get

Magellan Financial Group PESTLE Analysis

The preview shown here is the exact Magellan Financial Group PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use. This file reflects the final content and layout with no placeholders or teasers, so what you see is precisely what you’ll download immediately after checkout. Use it as-is for strategic planning, presentations, or further customization.