Magna International Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

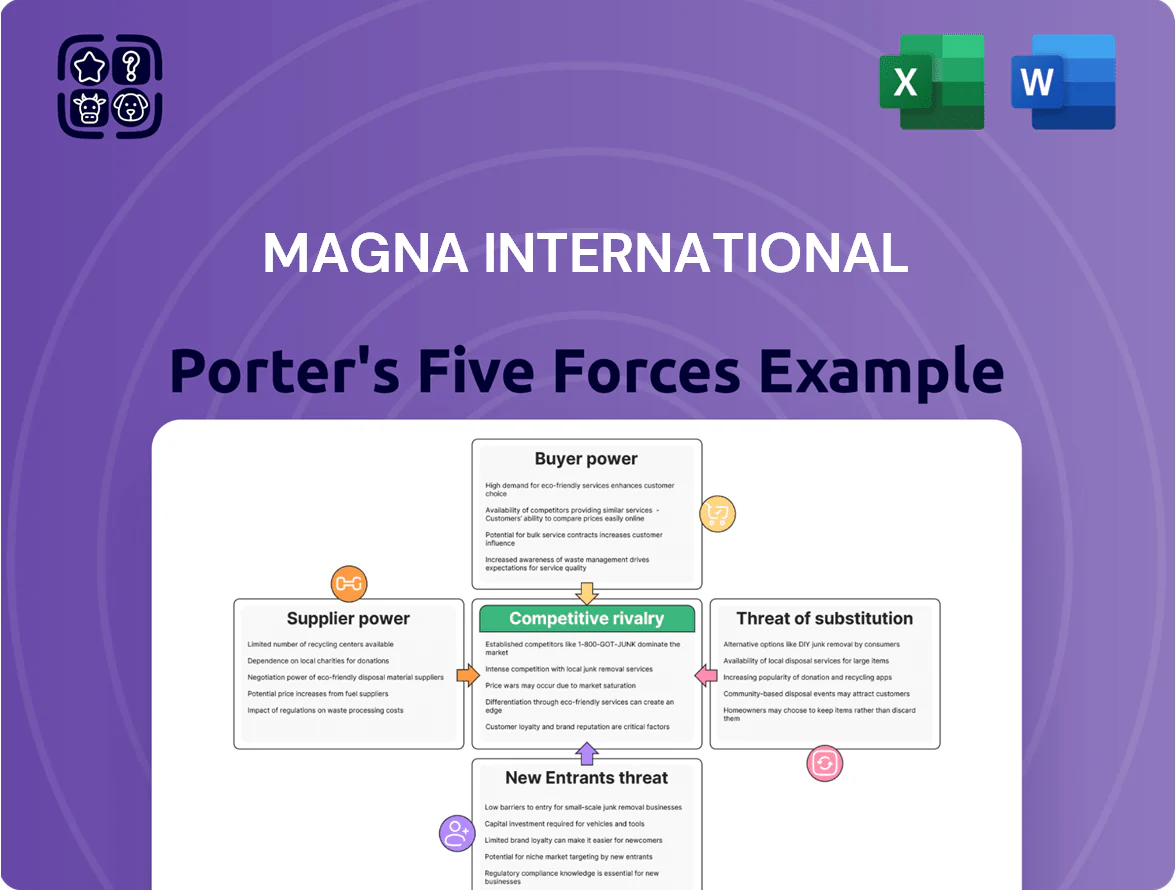

Magna International faces intense buyer pressure, moderate supplier influence, and evolving threats from EV-focused entrants and technological substitutes, while rivalry remains high due to scale-driven OEM relationships and margin compression.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Magna International’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Raw Material Price Volatility

Raw material price volatility remains a key supplier threat to Magna International; steel, aluminum and resins accounted for roughly 28% of COGS in 2024 and steel futures spiked 18% in H2 2025, squeezing margins before index-linked contracts repriced orders.

Magna uses index-based pricing to shift some risk, but typical repricing lags of 60–120 days expose EBITDA to swings — 2025 YTD input cost inflation lifted material spend by ~6–9% versus 2024.

The shift to green steel and certified low-carbon alloys adds premiums of 10–30% from specialized producers, raising procurement complexity and bargaining pressure on Magna’s supplier negotiations.

Semiconductor and Electronic Component Dependency

Despite supply-chain gains, rising ADAS and EV complexity keeps chipmakers' leverage high: high-performance processors and sensors come from a few specialized vendors, so suppliers sustained premium pricing—TSMC and NXP captured ~45% of relevant market segments in 2024, letting them prioritize large-volume buyers across autos and consumer electronics.

Energy Costs and Sustainability Mandates

Suppliers of energy-intensive parts have gained leverage as oil and gas volatility pushed industrial electricity costs up ~12% globally in 2023–24 and carbon pricing spread to 35 jurisdictions by 2025. Magna’s carbon-neutral supply-chain pledge for 2030 narrows eligible vendors, concentrating spend: 20–30% of suppliers must meet green-certification thresholds, so compliant firms can demand long-term contracts and 5–12% premium pricing for verified low‑carbon inputs.

Specialized Labor and Technical Talent

The shift to software-defined vehicles raises supplier power: specialized engineering and software firms command higher rates as Magna embeds digital architectures across modules, increasing spend on external talent from an estimated 12–18% of R&D in 2024 to higher shares in upcoming programs.

High demand for scarce high-tech talent across auto and tech sectors lets suppliers press for favorable contracts, longer minimums, and price premiums, squeezing margins unless Magna vertically integrates or secures long-term partnerships.

- 2024: global automotive software market ≈ $53B, growing ~12% CAGR

- Specialized talent premiums: 20–40% above traditional engineering rates

- Magna R&D outsourcing share: ~12–18% in recent programs

Logistics and Tier 2 Integration

Magna’s global footprint relies on Tier 2/3 suppliers for critical sub-components in just-in-time production; in 2024 roughly 28% of parts spend flowed to these smaller suppliers, raising disruption risk.

Regional logistics hub issues or insolvency among sub-suppliers can create temporary supplier leverage, as a day of assembly-line downtime can cost automakers $20–50m; Magna sometimes provides working capital or engineering support to secure supply.

Magna reported supplier support programs totaling about $350m in 2023–24 to stabilise key Tier 2/3 partners and reduce lead-time volatility.

- 28% of parts spend to Tier 2/3 (2024)

- $20–50m estimated daily assembly-line outage cost

- $350m supplier support (2023–24)

Suppliers Squeeze Margins: Materials, Chips & Talent Concentrate Risk

Suppliers hold moderate-to-high power: raw materials (28% of COGS in 2024) and green-steel premiums (10–30%) squeeze margins; chip and sensor vendors (TSMC, NXP ~45% share in key segments 2024) and scarce software talent (specialist premiums 20–40%) drive pricing leverage; Magna’s $350m supplier support (2023–24) and 28% Tier2/3 spend mitigate but concentrate risk.

| Metric | Value |

|---|---|

| Materials %COGS (2024) | 28% |

| Green-steel premium | 10–30% |

| Chip/vendor share (2024) | ~45% |

| Supplier support (2023–24) | $350m |

| Tier2/3 spend (2024) | 28% |

What is included in the product

Customized Porter’s Five Forces assessment of Magna International that pinpoints competitive intensity, supplier and buyer bargaining power, threat of substitutes and new entrants, and highlights disruptive trends and strategic levers affecting profitability and market positioning.

Concise Porter's Five Forces snapshot for Magna International—quickly gauge supplier, buyer, rivalry, entrant, and substitute pressures to streamline strategic choices and investor briefings.

Customers Bargaining Power

High Concentration of Global OEMs

The automotive market is dominated by a few massive OEMs—Ford Motor Company, General Motors Company, and Volkswagen AG—who together represented roughly 20–30% of Magna International Inc.’s revenue in recent years (Magna reported US$37.7bn revenue in 2024), giving these customers strong negotiating leverage.

Concentration lets OEMs push strict cost-reduction targets and annual productivity give-backs as contract terms, often cutting supplier margins by low-single-digit percentage points each year.

Magna’s dependence on large OEMs raises revenue volatility and forces continuous capital investment to meet OEM efficiency and quality standards.

Shift Toward In-House EV Development

Low Switching Costs for Standard Components

For commodity parts like basic stampings and standard seating frames, OEMs can switch suppliers easily, keeping customer bargaining power high and price sensitivity strong; in 2024, industry data shows multi-sourcing at >60% for such components. Magna must continually innovate and cut costs to retain preferred status, which limits pricing power in legacy segments where margins fell ~120 bps to 7.4% in 2024.

Stringent Quality and ESG Requirements

- 75% of platforms require supplier Scope 3 data

- 60% demand audited labor standards

- Estimated $150–250M/yr Magna compliance spend

- Noncompliance leads to de-sourcing risk

Contract Manufacturing Vulnerability

Magna Steyr depends heavily on contracts with a few OEMs—BMW and Mercedes-Benz account for about 60% of its 2024 assembly revenue—so an OEM shifting production to an underused plant can cut high-margin volume and revenue sharply.

This specialized assembly model gives those OEMs strong leverage in renewals and pricing; Magna reported EBIT margin pressure in 2024 when a single client reduced volumes by ~15%.

- High customer concentration: ~60% revenue from BMW/Mercedes (2024)

- Client volume shift risk: single-client cut ~15% (2024 impact)

- Negotiation leverage: OEMs can demand lower prices/terms

- Margin sensitivity: assembly is higher-margin than commodity parts

OEMs Squeeze Magna: In‑housing, ESG Costs Cut Margins ~5–8% on $37.7B Revenue

Large OEMs (Ford, GM, VW) drive strong buyer power, supplying 20–30% of Magna’s revenue (Magna revenue US$37.7bn in 2024). OEMs press annual cost give-backs, push in-housing (VW 60% vertical integration target 2025; Tesla >50% drivetrain in‑house), and enforce ESG/supply audits, raising compliance costs (~$150–250M/yr) and shortening contracts, which squeezes margins by ~5–8% in competitive e-drive bids.

| Metric | Value (2024–25) |

|---|---|

| Magna revenue | US$37.7bn (2024) |

| OEM share | 20–30% per major OEM |

| Compliance spend | $150–250M/yr |

| In-housing impact | Price pressure 5–8% |

What You See Is What You Get

Magna International Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Magna International you'll receive—no mockups, no placeholders—fully formatted and ready for immediate download upon purchase.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

Magna International faces intense buyer pressure, moderate supplier influence, and evolving threats from EV-focused entrants and technological substitutes, while rivalry remains high due to scale-driven OEM relationships and margin compression.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Magna International’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Raw Material Price Volatility

Raw material price volatility remains a key supplier threat to Magna International; steel, aluminum and resins accounted for roughly 28% of COGS in 2024 and steel futures spiked 18% in H2 2025, squeezing margins before index-linked contracts repriced orders.

Magna uses index-based pricing to shift some risk, but typical repricing lags of 60–120 days expose EBITDA to swings — 2025 YTD input cost inflation lifted material spend by ~6–9% versus 2024.

The shift to green steel and certified low-carbon alloys adds premiums of 10–30% from specialized producers, raising procurement complexity and bargaining pressure on Magna’s supplier negotiations.

Semiconductor and Electronic Component Dependency

Despite supply-chain gains, rising ADAS and EV complexity keeps chipmakers' leverage high: high-performance processors and sensors come from a few specialized vendors, so suppliers sustained premium pricing—TSMC and NXP captured ~45% of relevant market segments in 2024, letting them prioritize large-volume buyers across autos and consumer electronics.

Energy Costs and Sustainability Mandates

Suppliers of energy-intensive parts have gained leverage as oil and gas volatility pushed industrial electricity costs up ~12% globally in 2023–24 and carbon pricing spread to 35 jurisdictions by 2025. Magna’s carbon-neutral supply-chain pledge for 2030 narrows eligible vendors, concentrating spend: 20–30% of suppliers must meet green-certification thresholds, so compliant firms can demand long-term contracts and 5–12% premium pricing for verified low‑carbon inputs.

Specialized Labor and Technical Talent

The shift to software-defined vehicles raises supplier power: specialized engineering and software firms command higher rates as Magna embeds digital architectures across modules, increasing spend on external talent from an estimated 12–18% of R&D in 2024 to higher shares in upcoming programs.

High demand for scarce high-tech talent across auto and tech sectors lets suppliers press for favorable contracts, longer minimums, and price premiums, squeezing margins unless Magna vertically integrates or secures long-term partnerships.

- 2024: global automotive software market ≈ $53B, growing ~12% CAGR

- Specialized talent premiums: 20–40% above traditional engineering rates

- Magna R&D outsourcing share: ~12–18% in recent programs

Logistics and Tier 2 Integration

Magna’s global footprint relies on Tier 2/3 suppliers for critical sub-components in just-in-time production; in 2024 roughly 28% of parts spend flowed to these smaller suppliers, raising disruption risk.

Regional logistics hub issues or insolvency among sub-suppliers can create temporary supplier leverage, as a day of assembly-line downtime can cost automakers $20–50m; Magna sometimes provides working capital or engineering support to secure supply.

Magna reported supplier support programs totaling about $350m in 2023–24 to stabilise key Tier 2/3 partners and reduce lead-time volatility.

- 28% of parts spend to Tier 2/3 (2024)

- $20–50m estimated daily assembly-line outage cost

- $350m supplier support (2023–24)

Suppliers Squeeze Margins: Materials, Chips & Talent Concentrate Risk

Suppliers hold moderate-to-high power: raw materials (28% of COGS in 2024) and green-steel premiums (10–30%) squeeze margins; chip and sensor vendors (TSMC, NXP ~45% share in key segments 2024) and scarce software talent (specialist premiums 20–40%) drive pricing leverage; Magna’s $350m supplier support (2023–24) and 28% Tier2/3 spend mitigate but concentrate risk.

| Metric | Value |

|---|---|

| Materials %COGS (2024) | 28% |

| Green-steel premium | 10–30% |

| Chip/vendor share (2024) | ~45% |

| Supplier support (2023–24) | $350m |

| Tier2/3 spend (2024) | 28% |

What is included in the product

Customized Porter’s Five Forces assessment of Magna International that pinpoints competitive intensity, supplier and buyer bargaining power, threat of substitutes and new entrants, and highlights disruptive trends and strategic levers affecting profitability and market positioning.

Concise Porter's Five Forces snapshot for Magna International—quickly gauge supplier, buyer, rivalry, entrant, and substitute pressures to streamline strategic choices and investor briefings.

Customers Bargaining Power

High Concentration of Global OEMs

The automotive market is dominated by a few massive OEMs—Ford Motor Company, General Motors Company, and Volkswagen AG—who together represented roughly 20–30% of Magna International Inc.’s revenue in recent years (Magna reported US$37.7bn revenue in 2024), giving these customers strong negotiating leverage.

Concentration lets OEMs push strict cost-reduction targets and annual productivity give-backs as contract terms, often cutting supplier margins by low-single-digit percentage points each year.

Magna’s dependence on large OEMs raises revenue volatility and forces continuous capital investment to meet OEM efficiency and quality standards.

Shift Toward In-House EV Development

Low Switching Costs for Standard Components

For commodity parts like basic stampings and standard seating frames, OEMs can switch suppliers easily, keeping customer bargaining power high and price sensitivity strong; in 2024, industry data shows multi-sourcing at >60% for such components. Magna must continually innovate and cut costs to retain preferred status, which limits pricing power in legacy segments where margins fell ~120 bps to 7.4% in 2024.

Stringent Quality and ESG Requirements

- 75% of platforms require supplier Scope 3 data

- 60% demand audited labor standards

- Estimated $150–250M/yr Magna compliance spend

- Noncompliance leads to de-sourcing risk

Contract Manufacturing Vulnerability

Magna Steyr depends heavily on contracts with a few OEMs—BMW and Mercedes-Benz account for about 60% of its 2024 assembly revenue—so an OEM shifting production to an underused plant can cut high-margin volume and revenue sharply.

This specialized assembly model gives those OEMs strong leverage in renewals and pricing; Magna reported EBIT margin pressure in 2024 when a single client reduced volumes by ~15%.

- High customer concentration: ~60% revenue from BMW/Mercedes (2024)

- Client volume shift risk: single-client cut ~15% (2024 impact)

- Negotiation leverage: OEMs can demand lower prices/terms

- Margin sensitivity: assembly is higher-margin than commodity parts

OEMs Squeeze Magna: In‑housing, ESG Costs Cut Margins ~5–8% on $37.7B Revenue

Large OEMs (Ford, GM, VW) drive strong buyer power, supplying 20–30% of Magna’s revenue (Magna revenue US$37.7bn in 2024). OEMs press annual cost give-backs, push in-housing (VW 60% vertical integration target 2025; Tesla >50% drivetrain in‑house), and enforce ESG/supply audits, raising compliance costs (~$150–250M/yr) and shortening contracts, which squeezes margins by ~5–8% in competitive e-drive bids.

| Metric | Value (2024–25) |

|---|---|

| Magna revenue | US$37.7bn (2024) |

| OEM share | 20–30% per major OEM |

| Compliance spend | $150–250M/yr |

| In-housing impact | Price pressure 5–8% |

What You See Is What You Get

Magna International Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Magna International you'll receive—no mockups, no placeholders—fully formatted and ready for immediate download upon purchase.