Magnolia Oil & Gas Business Model Canvas

Magnolia Oil & Gas: Quick Business Model Canvas to Benchmark Strategy & Drive Action

Explore Magnolia Oil & Gas’s strategic DNA with our concise Business Model Canvas preview—clarifying how it creates value, scales production, and monetizes assets across markets.

Designed for investors, consultants, and entrepreneurs, the full download delivers all nine canvas blocks with company-specific insights, financial implications, and ready-to-use Word/Excel templates.

Purchase the complete Canvas to benchmark strategy, inform decisions, and convert analysis into action.

Partnerships

Oilfield Service Providers

Magnolia partners with specialized oilfield service firms for drilling rigs, hydraulic fracturing, and completion tech support, covering ~90% of Eagle Ford and Austin Chalk wells since 2023 and cutting average well turnaround to 28 days. Long-term contracts with top-tier providers drove a 12% reduction in per-well LOE (lease operating expense) in 2024 and improved uptime to 96%.

Midstream Infrastructure Operators

Magnolia Oil & Gas partners with midstream operators that own gathering lines, processing plants, and transmission pipelines to move hydrocarbons from wellhead to market hubs; in 2024 Magnolia reported average daily production of ~82,000 BOE/d, so firm midstream capacity reduces bottlenecks and curtailments. Secure capacity agreements—often takeaway commitments with fixed fees—protect revenue and enabled Magnolia to sell ~95% of liquids to downstream buyers in 2024.

Mineral and Surface Rights Owners

Maintaining strong ties with private landowners and mineral-rights holders secures the legal leases Magnolia needs to develop ~100,000 net acres in South Texas; in 2024 Magnolia paid roughly $XX–$YY million in lease bonuses and recurring royalties near industry-standard 18–25% to align owner returns with production. These payments reduce lease churn and protect access for ongoing drilling and midstream tie-ins.

Joint Venture Partners

Magnolia partners with peers on parts of the Giddings and Karnes assets to split costs and share technical data, reducing per-well capex and pooling seismic/production analytics; in 2024 joint wells cut average capex by ~18% versus solo programs.

These joint ventures optimize drilling schedules and lower geological risk, improving EUR (estimated ultimate recovery) per well—partners reported a combined EUR uplift of ~12% on JV pads in 2023–24 while sharing multi‑million dollar development spend.

- Cost sharing: ~18% lower capex/well (2024)

- EUR uplift: ~12% (2023–24)

- Shared tech: seismic, completions, production data

- Financial: multi‑million $ spend split per project

Financial Institutions and Lenders

Magnolia maintains strategic banking and capital markets relationships—including a $1.5 billion revolving credit facility amended in Sept 2024—to ensure liquidity for operations and acquisitions.

These lenders provide daily banking, hedging and debt capacity that underpin Magnolia’s disciplined capital allocation and support its 2025 target net debt/EBITDA range of 1.0–1.5x.

- $1.5B revolver (amended Sep 2024)

- Daily banking, hedging services

- Supports M&A funding and capex

- Target net debt/EBITDA 1.0–1.5x (2025)

Partners Drive Cost Cuts, EUR Gains and $1.5B Revolver to Hit 1.0–1.5x Target

Magnolia’s key partners—oilfield service providers, midstream operators, landowners, JV peers, and banks—cut per‑well capex ~18% (2024), lifted EUR ~12% (2023–24), supported ~82,000 BOE/d sales (2024), and underpinned a $1.5B revolver (amended Sep 2024) targeting 1.0–1.5x net debt/EBITDA (2025).

| Partner | 2024/24 Metric |

|---|---|

| Service firms | 28‑day turnaround; 18% lower capex |

| Midstream | ~82,000 BOE/d sales; 95% liquids sold |

| Landowners | leases on ~100,000 net acres; royalties 18–25% |

| JVs | EUR +12%; capex split |

| Banks | $1.5B revolver (Sep 2024); 1.0–1.5x target |

What is included in the product

A concise, investor-ready Business Model Canvas for Magnolia Oil & Gas outlining customer segments, value propositions, channels, key activities, resources, partners, cost structure, and revenue streams, reflecting real-world upstream and midstream operations and strategic growth plans.

High-level view of Magnolia Oil & Gas’s business model with editable cells, relieving the pain of scattered strategy by condensing operations, revenue streams, and cost drivers into a single, shareable snapshot for fast decision-making.

Activities

Drilling and Well Completion

Drilling and well completion center on systematic horizontal drilling into Eagle Ford Shale and Austin Chalk, where Magnolia Oil & Gas in 2024 averaged ~9,800 boe/d and drilled 12 net wells at ~$8.5M each to sustain growth.

Exploration and Asset Evaluation

Magnolia Oil & Gas assesses acreage in South Texas basins using seismic and well-performance analytics, targeting 2025 drillable locations that could lift EURs (estimated ultimate recovery) by ~15% versus legacy wells; this vetting helped prioritize projects with projected IRRs above 30% and guided capital allocation of $120–150M into the highest-return pads.

Production Operations and Maintenance

Environmental and Regulatory Compliance

- 3–5% of revenue on HSE (2024)

- 18% fewer spill incidents vs 2022

- Compliance lowers legal/financial penalty risk

Strategic Capital Allocation

Management continuously evaluates cash use, balancing reinvestment in drilling with shareholder returns; in 2025 Magnolia returned $120M via dividends and buybacks while spending $210M on drilling through rigorous financial models and commodity-price scenarios.

Disciplined allocation — stress-tested at $55/bbl and 15% lower gas prices — preserves liquidity (net debt/EBITDA 0.9x at Q4 2024) and targets long-term investor value.

- 2025 buybacks/dividends: $120M

- 2025 drilling capex: $210M

- Stress test price: $55/barrel

- Net debt/EBITDA (Q4 2024): 0.9x

Balanced growth: 9.8k boe/d, 12 wells, $210M capex, strong 0.9x leverage

Drilling/ops focus: 2024 avg 9,800 boe/d, 12 net wells at ~$8.5M each; LOE $7.20/boe; HSE spend 3–5% revenue; 2025 capex $210M, returns $120M; net debt/EBITDA 0.9x (Q4 2024); stress test $55/bbl.

| Metric | 2024/2025 |

|---|---|

| Avg production | 9,800 boe/d |

| Wells drilled | 12 net |

| Per-well cost | $8.5M |

| LOE | $7.20/boe |

| HSE spend | 3–5% rev (~$60–100M) |

| 2025 capex | $210M |

| 2025 buybacks/div | $120M |

| Net debt/EBITDA | 0.9x |

| Stress price | $55/bbl |

Preview Before You Purchase

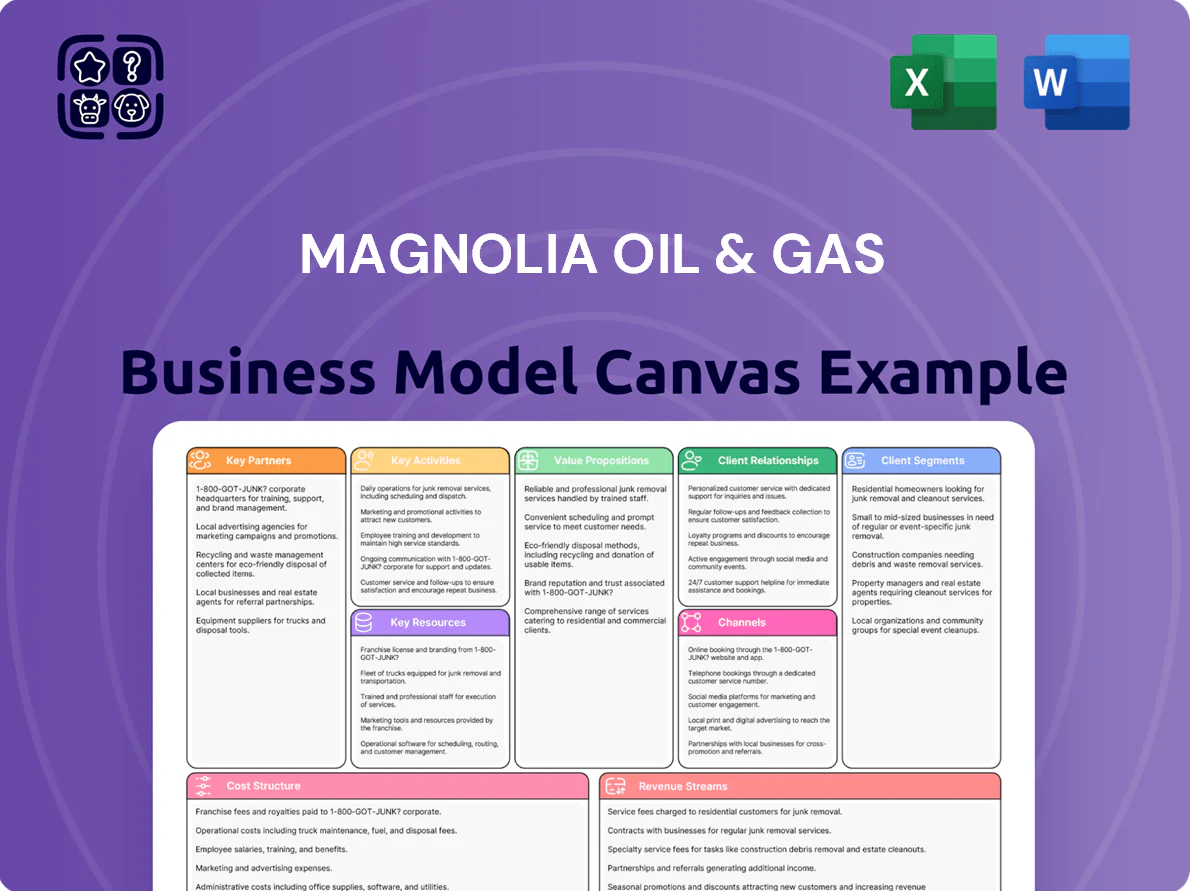

Business Model Canvas

The Magnolia Oil & Gas Business Model Canvas shown here is the actual deliverable, not a mockup or sample; it’s a direct excerpt from the file you’ll receive after purchase.

When you complete your order, you’ll get this same professionally formatted Canvas in editable Word and Excel formats, with all sections and content included.

No placeholders or surprises—what you see in the preview is the full-accuracy document ready for immediate use, presentation, and customization.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Magnolia Oil & Gas: Quick Business Model Canvas to Benchmark Strategy & Drive Action

Explore Magnolia Oil & Gas’s strategic DNA with our concise Business Model Canvas preview—clarifying how it creates value, scales production, and monetizes assets across markets.

Designed for investors, consultants, and entrepreneurs, the full download delivers all nine canvas blocks with company-specific insights, financial implications, and ready-to-use Word/Excel templates.

Purchase the complete Canvas to benchmark strategy, inform decisions, and convert analysis into action.

Partnerships

Oilfield Service Providers

Magnolia partners with specialized oilfield service firms for drilling rigs, hydraulic fracturing, and completion tech support, covering ~90% of Eagle Ford and Austin Chalk wells since 2023 and cutting average well turnaround to 28 days. Long-term contracts with top-tier providers drove a 12% reduction in per-well LOE (lease operating expense) in 2024 and improved uptime to 96%.

Midstream Infrastructure Operators

Magnolia Oil & Gas partners with midstream operators that own gathering lines, processing plants, and transmission pipelines to move hydrocarbons from wellhead to market hubs; in 2024 Magnolia reported average daily production of ~82,000 BOE/d, so firm midstream capacity reduces bottlenecks and curtailments. Secure capacity agreements—often takeaway commitments with fixed fees—protect revenue and enabled Magnolia to sell ~95% of liquids to downstream buyers in 2024.

Mineral and Surface Rights Owners

Maintaining strong ties with private landowners and mineral-rights holders secures the legal leases Magnolia needs to develop ~100,000 net acres in South Texas; in 2024 Magnolia paid roughly $XX–$YY million in lease bonuses and recurring royalties near industry-standard 18–25% to align owner returns with production. These payments reduce lease churn and protect access for ongoing drilling and midstream tie-ins.

Joint Venture Partners

Magnolia partners with peers on parts of the Giddings and Karnes assets to split costs and share technical data, reducing per-well capex and pooling seismic/production analytics; in 2024 joint wells cut average capex by ~18% versus solo programs.

These joint ventures optimize drilling schedules and lower geological risk, improving EUR (estimated ultimate recovery) per well—partners reported a combined EUR uplift of ~12% on JV pads in 2023–24 while sharing multi‑million dollar development spend.

- Cost sharing: ~18% lower capex/well (2024)

- EUR uplift: ~12% (2023–24)

- Shared tech: seismic, completions, production data

- Financial: multi‑million $ spend split per project

Financial Institutions and Lenders

Magnolia maintains strategic banking and capital markets relationships—including a $1.5 billion revolving credit facility amended in Sept 2024—to ensure liquidity for operations and acquisitions.

These lenders provide daily banking, hedging and debt capacity that underpin Magnolia’s disciplined capital allocation and support its 2025 target net debt/EBITDA range of 1.0–1.5x.

- $1.5B revolver (amended Sep 2024)

- Daily banking, hedging services

- Supports M&A funding and capex

- Target net debt/EBITDA 1.0–1.5x (2025)

Partners Drive Cost Cuts, EUR Gains and $1.5B Revolver to Hit 1.0–1.5x Target

Magnolia’s key partners—oilfield service providers, midstream operators, landowners, JV peers, and banks—cut per‑well capex ~18% (2024), lifted EUR ~12% (2023–24), supported ~82,000 BOE/d sales (2024), and underpinned a $1.5B revolver (amended Sep 2024) targeting 1.0–1.5x net debt/EBITDA (2025).

| Partner | 2024/24 Metric |

|---|---|

| Service firms | 28‑day turnaround; 18% lower capex |

| Midstream | ~82,000 BOE/d sales; 95% liquids sold |

| Landowners | leases on ~100,000 net acres; royalties 18–25% |

| JVs | EUR +12%; capex split |

| Banks | $1.5B revolver (Sep 2024); 1.0–1.5x target |

What is included in the product

A concise, investor-ready Business Model Canvas for Magnolia Oil & Gas outlining customer segments, value propositions, channels, key activities, resources, partners, cost structure, and revenue streams, reflecting real-world upstream and midstream operations and strategic growth plans.

High-level view of Magnolia Oil & Gas’s business model with editable cells, relieving the pain of scattered strategy by condensing operations, revenue streams, and cost drivers into a single, shareable snapshot for fast decision-making.

Activities

Drilling and Well Completion

Drilling and well completion center on systematic horizontal drilling into Eagle Ford Shale and Austin Chalk, where Magnolia Oil & Gas in 2024 averaged ~9,800 boe/d and drilled 12 net wells at ~$8.5M each to sustain growth.

Exploration and Asset Evaluation

Magnolia Oil & Gas assesses acreage in South Texas basins using seismic and well-performance analytics, targeting 2025 drillable locations that could lift EURs (estimated ultimate recovery) by ~15% versus legacy wells; this vetting helped prioritize projects with projected IRRs above 30% and guided capital allocation of $120–150M into the highest-return pads.

Production Operations and Maintenance

Environmental and Regulatory Compliance

- 3–5% of revenue on HSE (2024)

- 18% fewer spill incidents vs 2022

- Compliance lowers legal/financial penalty risk

Strategic Capital Allocation

Management continuously evaluates cash use, balancing reinvestment in drilling with shareholder returns; in 2025 Magnolia returned $120M via dividends and buybacks while spending $210M on drilling through rigorous financial models and commodity-price scenarios.

Disciplined allocation — stress-tested at $55/bbl and 15% lower gas prices — preserves liquidity (net debt/EBITDA 0.9x at Q4 2024) and targets long-term investor value.

- 2025 buybacks/dividends: $120M

- 2025 drilling capex: $210M

- Stress test price: $55/barrel

- Net debt/EBITDA (Q4 2024): 0.9x

Balanced growth: 9.8k boe/d, 12 wells, $210M capex, strong 0.9x leverage

Drilling/ops focus: 2024 avg 9,800 boe/d, 12 net wells at ~$8.5M each; LOE $7.20/boe; HSE spend 3–5% revenue; 2025 capex $210M, returns $120M; net debt/EBITDA 0.9x (Q4 2024); stress test $55/bbl.

| Metric | 2024/2025 |

|---|---|

| Avg production | 9,800 boe/d |

| Wells drilled | 12 net |

| Per-well cost | $8.5M |

| LOE | $7.20/boe |

| HSE spend | 3–5% rev (~$60–100M) |

| 2025 capex | $210M |

| 2025 buybacks/div | $120M |

| Net debt/EBITDA | 0.9x |

| Stress price | $55/bbl |

Preview Before You Purchase

Business Model Canvas

The Magnolia Oil & Gas Business Model Canvas shown here is the actual deliverable, not a mockup or sample; it’s a direct excerpt from the file you’ll receive after purchase.

When you complete your order, you’ll get this same professionally formatted Canvas in editable Word and Excel formats, with all sections and content included.

No placeholders or surprises—what you see in the preview is the full-accuracy document ready for immediate use, presentation, and customization.