Magnolia Oil & Gas Marketing Mix

Get Inspired by a Complete Brand Strategy

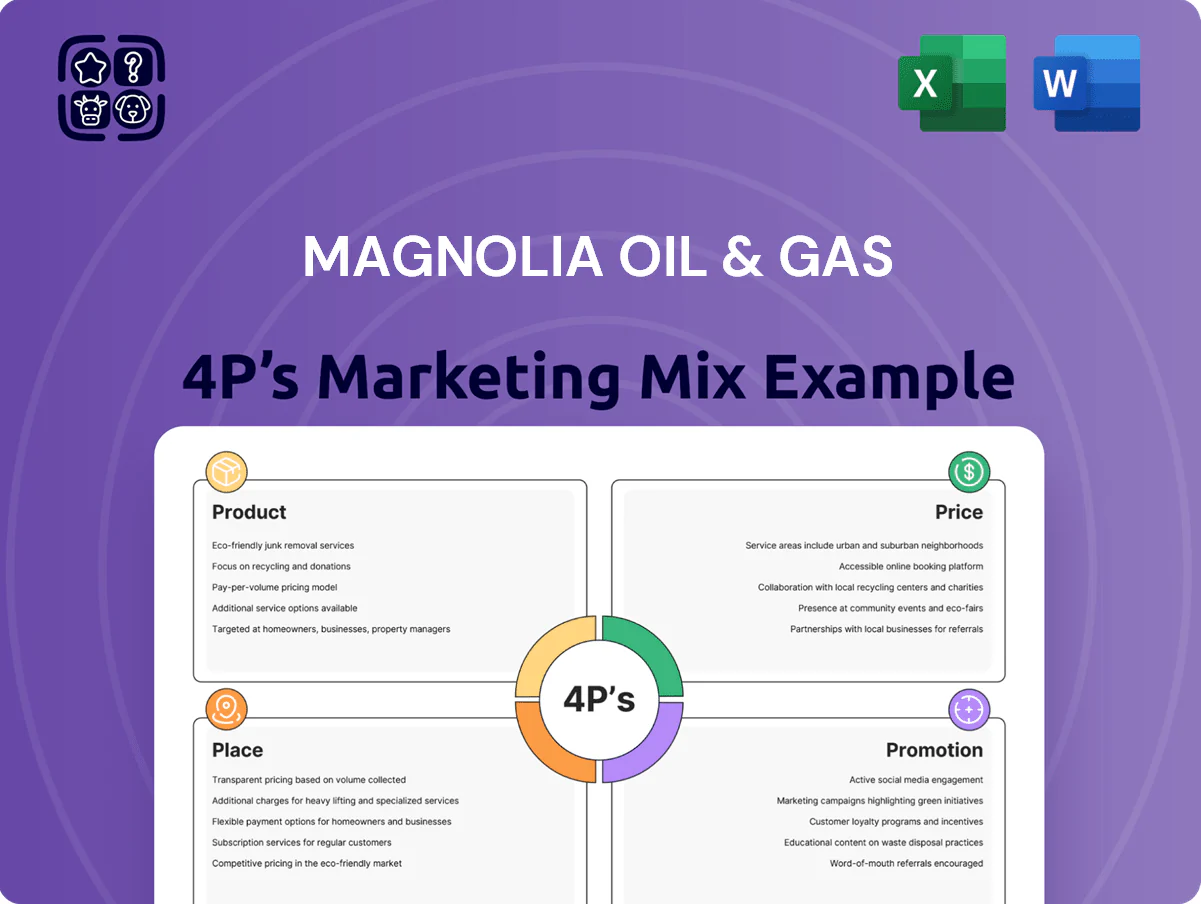

Magnolia Oil & Gas leverages a focused product portfolio, competitive pricing, strategic distribution to key energy hubs, and targeted promotions to strengthen market share; our full 4P’s analysis unpacks these choices and their impact. Purchase the complete, editable report to access data-driven insights, ready-to-use slides, and actionable recommendations for benchmarking or strategy. Save time and apply proven tactics—get the full Magnolia Oil & Gas Marketing Mix now.

Product

Crude Oil Production

Magnolia Oil & Gas produces light sweet crude from Eagle Ford Shale and Austin Chalk, supplying low-sulfur feedstock prized by domestic refineries and export markets; in 2025 the company reports ~55,000 boe/d (barrels oil equivalent per day) from these plays and aims to raise recovery by 8% via advanced horizontal drilling and completion tweaks. The crude’s sub-0.5% sulfur lifts refinery margins and supported $420 million in upstream revenue in FY 2024.

Natural Gas Extraction

Magnolia Oil & Gas produces large volumes of natural gas from South Texas—about 220 MMcf/d in 2025—fueling electricity generation and industrial manufacturing; natural gas demand stayed steady at ~130 Bcf/d U.S. in 2024, supporting midstream sales. Magnolia gathers and processes gas via its integrated midstream network (compression, dehydration, NGL recovery) to meet pipeline and power-plant specs, contributing roughly $240 million in 2025 midstream-adjusted revenue.

Natural Gas Liquids

Magnolia Oil & Gas produces ethane, propane, and butane as natural gas liquids (NGLs), contributing about 18% of 2024 revenue—roughly $145 million of $805 million total—supporting margin diversification.

These NGLs feed the petrochemical sector as primary feedstocks for plastics and chemicals; US ethane demand hit ~3.8 million b/d in 2024, keeping prices firm.

Magnolia uses cryogenic and fractionation separation at wellhead and plants, lifting NGL recovery rates to ~5.2 gallons per Mcf, improving realized NGL value by ~12% in 2024.

Operational Excellence and Technical Expertise

Magnolia Oil & Gas (NYSE: MGY) uses disciplined asset development and reservoir management to boost recovery, applying horizontal drilling and multi-stage hydraulic fracturing across its Eagle Ford and Gulf Coast positions.

In 2024 the company reported total production of ~64,000 boe/d and capex of $290M, with well-level EURs improved ~15% versus 2021 through completion optimization—raising capital efficiency and lowering LOE per boe.

- Production ~64,000 boe/d (2024)

- Capex $290M (2024)

- EUR improvement ~15% vs 2021

- Higher recovery, lower LOE per boe

Low Carbon Intensity Energy

- 0.04% methane intensity vs 0.12% industry avg

- 38% flaring reduction YoY

- 12% of 2024–25 capex for emissions cuts

- Premiums in ESG-linked offtakes reported 3–6% price uplift

Magnolia: 64k boe/d, $420M revenue, $290M capex — emissions cuts and rising EURs

Magnolia (NYSE: MGY) produces ~64,000 boe/d (2024), ~55,000 boe/d light crude from Eagle Ford/Austin Chalk (2025), 220 MMcf/d gas (2025); FY2024 upstream revenue $420M, midstream-adjusted $240M, NGLs $145M (18% of $805M); capex $290M (2024); EUR +15% vs 2021; methane intensity 0.04%; flaring -38% YoY; 12% capex for emissions.

| Metric | 2024/2025 |

|---|---|

| Prod | 64k boe/d |

| Crude | 55k boe/d |

| Gas | 220 MMcf/d |

| Up rev | $420M |

| Capex | $290M |

What is included in the product

Delivers a company-specific deep dive into Magnolia Oil & Gas’s Product, Price, Place, and Promotion strategies, ideal for managers and consultants needing a complete breakdown of the firm’s marketing positioning.

Condenses Magnolia Oil & Gas’s 4P marketing insights into a concise, presentation-ready summary that eases leadership alignment and speeds decision-making by highlighting product, price, place, and promotion strategies at a glance.

Place

Karnes County Core Operations

Magnolia Oil & Gas holds a dominant acreage position in Karnes County, Eagle Ford Shale, where the play produced about 380,000 BPD in 2024; this concentration enables dense pad drilling and higher EURs per well.

Centralized infrastructure in Karnes cuts midstream and transport costs; Magnolia reported ~15% lower LOE (lease operating expense) vs regional peers in FY2024.

Proximity to San Antonio and local service hubs ensures rapid rig mobilization and parts availability, supporting >95% uptime on producing wells during 2024.

Giddings Field Development

Magnolia Oil & Gas has expanded in Giddings Field (Austin Chalk) to secure 1,200+ net drilling locations distinct from Eagle Ford, targeting 20–25% of company-wide production by YE 2025; the asset delivered 15,000 boe/d in H1 2025 and funds reinvestment with projected IRR ~30% on PDP-to-PMN wells, supporting capital allocation that raised 2025 production guidance by 10% versus 2024.

South Texas Midstream Integration

Magnolia Oil & Gas uses a dense South Texas midstream network of pipelines and gathering systems—covering roughly 1,200 miles as of 2025—to move crude and gas from wellhead to regional processors, cutting truck costs and delivery time. These channels handle peak flows up to about 150,000 barrels equivalent per day, crucial for linking production to market. Facilities sit near major intersections like the Agua Dulce and Corpus hubs, letting Magnolia bypass local chokepoints and access diverse delivery points. In 2024 midstream efficiencies helped lower transport per-barrel cost by an estimated 6% versus 2022.

Gulf Coast Market Access

Magnolia Oil & Gas gains strong price and logistics advantages from being near the US Gulf Coast, the world’s top refining and LNG export hub; in 2024 US Gulf Coast refiners processed ~9.5 million barrels/day and LNG exports averaged ~13.2 Bcf/day, cutting Magnolia’s transport costs and time to market.

Proximity to major refinery complexes and LNG terminals boosts Magnolia’s netbacks by lowering midstream fees and export freight, improving realized prices versus inland peers by an estimated $3–6/boe in 2024.

- Gulf Coast refiners ~9.5 MMb/d (2024)

- US LNG exports ~13.2 Bcf/d (2024)

- Estimated netback uplift $3–6/boe (2024)

Global Export Gateways

Through third-party arrangements and Texas Gulf Coast export docks, Magnolia Oil & Gas ships crude and NGLs into international markets, tapping ports like Corpus Christi and Houston that handled ~57% of US crude exports in 2024 (EIA).

Access to global export gateways lets Magnolia capture international price premiums—WTI-Brent spreads averaged +2.1 USD/bbl in 2024—when US supply is heavy, improving realized prices.

By 2025, maintaining export cadence (capacity to move ~50–100 kb/d via contractors) remains core to distribution, cushioning domestic oversupply risks and supporting margin stability.

- Use Gulf export docks via third parties

- 57% US exports via TX ports in 2024 (EIA)

- WTI-Brent +2.1 USD/bbl avg 2024

- Export capacity ~50–100 kb/d via contractors

Magnolia’s 1,200-mile Texas pipeline cuts LOE 15%, boosts netbacks $3–6/boe

Magnolia’s Karnes-centric footprint and 1,200-mile South Texas pipeline network (2025) cut LOE ~15% and transport costs ~6% vs 2022, supporting >95% uptime and 2025 production guidance +10%; Giddings adds 1,200+ locations and 15,000 boe/d H1 2025. Gulf Coast access (refiners 9.5 MMb/d, LNG 13.2 Bcf/d in 2024) and export capacity 50–100 kb/d lift netbacks $3–6/boe (2024).

| Metric | Value |

|---|---|

| Pipelines (2025) | ~1,200 miles |

| LOE vs peers (2024) | ~15% lower |

| Netback uplift (2024) | $3–6/boe |

Full Version Awaits

Magnolia Oil & Gas 4P's Marketing Mix Analysis

The preview shown here is the actual Magnolia Oil & Gas 4P's Marketing Mix Analysis you’ll receive instantly after purchase—fully complete, editable, and ready for immediate use with no surprises.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Get Inspired by a Complete Brand Strategy

Magnolia Oil & Gas leverages a focused product portfolio, competitive pricing, strategic distribution to key energy hubs, and targeted promotions to strengthen market share; our full 4P’s analysis unpacks these choices and their impact. Purchase the complete, editable report to access data-driven insights, ready-to-use slides, and actionable recommendations for benchmarking or strategy. Save time and apply proven tactics—get the full Magnolia Oil & Gas Marketing Mix now.

Product

Crude Oil Production

Magnolia Oil & Gas produces light sweet crude from Eagle Ford Shale and Austin Chalk, supplying low-sulfur feedstock prized by domestic refineries and export markets; in 2025 the company reports ~55,000 boe/d (barrels oil equivalent per day) from these plays and aims to raise recovery by 8% via advanced horizontal drilling and completion tweaks. The crude’s sub-0.5% sulfur lifts refinery margins and supported $420 million in upstream revenue in FY 2024.

Natural Gas Extraction

Magnolia Oil & Gas produces large volumes of natural gas from South Texas—about 220 MMcf/d in 2025—fueling electricity generation and industrial manufacturing; natural gas demand stayed steady at ~130 Bcf/d U.S. in 2024, supporting midstream sales. Magnolia gathers and processes gas via its integrated midstream network (compression, dehydration, NGL recovery) to meet pipeline and power-plant specs, contributing roughly $240 million in 2025 midstream-adjusted revenue.

Natural Gas Liquids

Magnolia Oil & Gas produces ethane, propane, and butane as natural gas liquids (NGLs), contributing about 18% of 2024 revenue—roughly $145 million of $805 million total—supporting margin diversification.

These NGLs feed the petrochemical sector as primary feedstocks for plastics and chemicals; US ethane demand hit ~3.8 million b/d in 2024, keeping prices firm.

Magnolia uses cryogenic and fractionation separation at wellhead and plants, lifting NGL recovery rates to ~5.2 gallons per Mcf, improving realized NGL value by ~12% in 2024.

Operational Excellence and Technical Expertise

Magnolia Oil & Gas (NYSE: MGY) uses disciplined asset development and reservoir management to boost recovery, applying horizontal drilling and multi-stage hydraulic fracturing across its Eagle Ford and Gulf Coast positions.

In 2024 the company reported total production of ~64,000 boe/d and capex of $290M, with well-level EURs improved ~15% versus 2021 through completion optimization—raising capital efficiency and lowering LOE per boe.

- Production ~64,000 boe/d (2024)

- Capex $290M (2024)

- EUR improvement ~15% vs 2021

- Higher recovery, lower LOE per boe

Low Carbon Intensity Energy

- 0.04% methane intensity vs 0.12% industry avg

- 38% flaring reduction YoY

- 12% of 2024–25 capex for emissions cuts

- Premiums in ESG-linked offtakes reported 3–6% price uplift

Magnolia: 64k boe/d, $420M revenue, $290M capex — emissions cuts and rising EURs

Magnolia (NYSE: MGY) produces ~64,000 boe/d (2024), ~55,000 boe/d light crude from Eagle Ford/Austin Chalk (2025), 220 MMcf/d gas (2025); FY2024 upstream revenue $420M, midstream-adjusted $240M, NGLs $145M (18% of $805M); capex $290M (2024); EUR +15% vs 2021; methane intensity 0.04%; flaring -38% YoY; 12% capex for emissions.

| Metric | 2024/2025 |

|---|---|

| Prod | 64k boe/d |

| Crude | 55k boe/d |

| Gas | 220 MMcf/d |

| Up rev | $420M |

| Capex | $290M |

What is included in the product

Delivers a company-specific deep dive into Magnolia Oil & Gas’s Product, Price, Place, and Promotion strategies, ideal for managers and consultants needing a complete breakdown of the firm’s marketing positioning.

Condenses Magnolia Oil & Gas’s 4P marketing insights into a concise, presentation-ready summary that eases leadership alignment and speeds decision-making by highlighting product, price, place, and promotion strategies at a glance.

Place

Karnes County Core Operations

Magnolia Oil & Gas holds a dominant acreage position in Karnes County, Eagle Ford Shale, where the play produced about 380,000 BPD in 2024; this concentration enables dense pad drilling and higher EURs per well.

Centralized infrastructure in Karnes cuts midstream and transport costs; Magnolia reported ~15% lower LOE (lease operating expense) vs regional peers in FY2024.

Proximity to San Antonio and local service hubs ensures rapid rig mobilization and parts availability, supporting >95% uptime on producing wells during 2024.

Giddings Field Development

Magnolia Oil & Gas has expanded in Giddings Field (Austin Chalk) to secure 1,200+ net drilling locations distinct from Eagle Ford, targeting 20–25% of company-wide production by YE 2025; the asset delivered 15,000 boe/d in H1 2025 and funds reinvestment with projected IRR ~30% on PDP-to-PMN wells, supporting capital allocation that raised 2025 production guidance by 10% versus 2024.

South Texas Midstream Integration

Magnolia Oil & Gas uses a dense South Texas midstream network of pipelines and gathering systems—covering roughly 1,200 miles as of 2025—to move crude and gas from wellhead to regional processors, cutting truck costs and delivery time. These channels handle peak flows up to about 150,000 barrels equivalent per day, crucial for linking production to market. Facilities sit near major intersections like the Agua Dulce and Corpus hubs, letting Magnolia bypass local chokepoints and access diverse delivery points. In 2024 midstream efficiencies helped lower transport per-barrel cost by an estimated 6% versus 2022.

Gulf Coast Market Access

Magnolia Oil & Gas gains strong price and logistics advantages from being near the US Gulf Coast, the world’s top refining and LNG export hub; in 2024 US Gulf Coast refiners processed ~9.5 million barrels/day and LNG exports averaged ~13.2 Bcf/day, cutting Magnolia’s transport costs and time to market.

Proximity to major refinery complexes and LNG terminals boosts Magnolia’s netbacks by lowering midstream fees and export freight, improving realized prices versus inland peers by an estimated $3–6/boe in 2024.

- Gulf Coast refiners ~9.5 MMb/d (2024)

- US LNG exports ~13.2 Bcf/d (2024)

- Estimated netback uplift $3–6/boe (2024)

Global Export Gateways

Through third-party arrangements and Texas Gulf Coast export docks, Magnolia Oil & Gas ships crude and NGLs into international markets, tapping ports like Corpus Christi and Houston that handled ~57% of US crude exports in 2024 (EIA).

Access to global export gateways lets Magnolia capture international price premiums—WTI-Brent spreads averaged +2.1 USD/bbl in 2024—when US supply is heavy, improving realized prices.

By 2025, maintaining export cadence (capacity to move ~50–100 kb/d via contractors) remains core to distribution, cushioning domestic oversupply risks and supporting margin stability.

- Use Gulf export docks via third parties

- 57% US exports via TX ports in 2024 (EIA)

- WTI-Brent +2.1 USD/bbl avg 2024

- Export capacity ~50–100 kb/d via contractors

Magnolia’s 1,200-mile Texas pipeline cuts LOE 15%, boosts netbacks $3–6/boe

Magnolia’s Karnes-centric footprint and 1,200-mile South Texas pipeline network (2025) cut LOE ~15% and transport costs ~6% vs 2022, supporting >95% uptime and 2025 production guidance +10%; Giddings adds 1,200+ locations and 15,000 boe/d H1 2025. Gulf Coast access (refiners 9.5 MMb/d, LNG 13.2 Bcf/d in 2024) and export capacity 50–100 kb/d lift netbacks $3–6/boe (2024).

| Metric | Value |

|---|---|

| Pipelines (2025) | ~1,200 miles |

| LOE vs peers (2024) | ~15% lower |

| Netback uplift (2024) | $3–6/boe |

Full Version Awaits

Magnolia Oil & Gas 4P's Marketing Mix Analysis

The preview shown here is the actual Magnolia Oil & Gas 4P's Marketing Mix Analysis you’ll receive instantly after purchase—fully complete, editable, and ready for immediate use with no surprises.