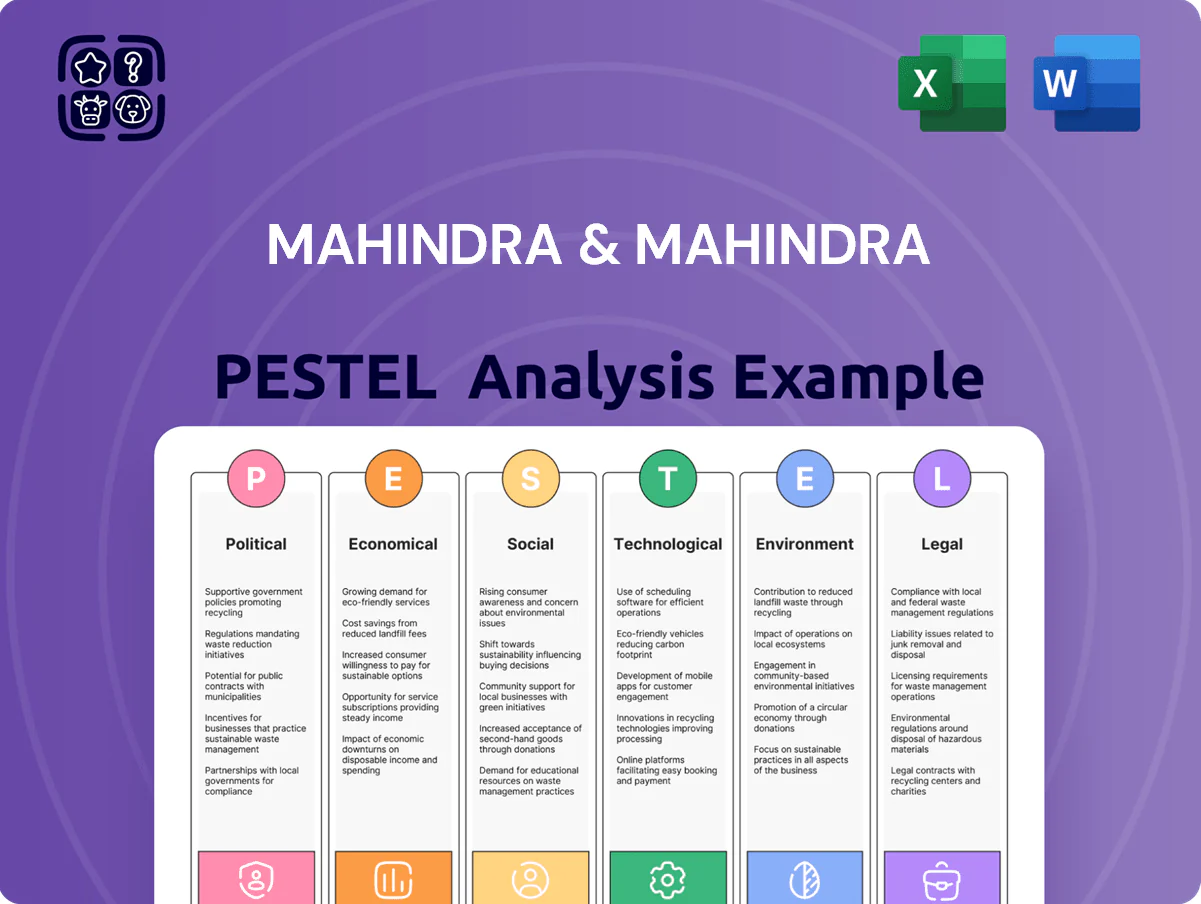

Mahindra & Mahindra PESTLE Analysis

Your Competitive Advantage Starts with This Report

Explore how regulatory shifts, economic cycles, and emerging technologies are reshaping Mahindra & Mahindra’s strategic landscape in our concise PESTLE snapshot—ideal for investors and strategists seeking actionable context. Purchase the full PESTLE to access a comprehensive, editable report with deep-dive insights, risk assessments, and opportunity maps you can apply immediately.

Political factors

Government Electric Vehicle Incentives

The Indian government’s FAME-III and state EV subsidies, totaling an estimated INR 25,000–35,000 crore (2024–25 allocations), lower EV acquisition costs and boost demand for Mahindra’s Born Electric models; e.g., passenger EV sales grew ~45% YoY in FY2024, aiding Mahindra’s urban market push.

Rural Development and Agricultural Subsidies

Government spending on rural infrastructure and direct benefit transfers like PM-Kisan, which paid over 200 billion INR in 2024, directly boosts demand for Mahindra & Mahindra’s tractors and farm equipment by increasing farmer liquidity and purchasing power.

Mahindra’s domestic tractor volumes—about 300,000 units in FY2024—are closely correlated with rural credit flow and subsidy disbursements that enable mechanization upgrades.

A reduction or reallocation of populist/developmental budgets could cause sharp demand swings in the farm equipment segment, affecting Mahindra’s core revenue stream and margins.

Geopolitical Trade Relations

As Mahindra & Mahindra expands in the Americas, Africa and Southeast Asia, FTAs and tariffs materially affect export competitiveness; exports grew 18% YoY in FY2024 for the farm equipment segment, highlighting sensitivity to trade barriers. Geopolitical tensions and rising protectionism—20–35% import duties in some African markets—can disrupt supply chains and raise costs for imported high-tech components. Mahindra must actively manage bilateral trade risks and localize sourcing to preserve its leading global tractor market share of ~17% in FY2024.

Infrastructure Development Initiatives

India’s Gati Shakti and similar infrastructure programs boost demand for Mahindra & Mahindra’s CVs and construction equipment; government capital expenditure rose to 6.1% of GDP in FY2025, supporting higher public works spending.

Improved road connectivity shortens logistics times—road freight share ~60%—encouraging fleet upgrades to heavy-duty solutions, aiding M&M’s CV sales growth (domestic CV industry grew ~12% YoY in 2024).

Political focus on connectivity underpins long-term expansion of domestic logistics and automotive sectors, benefiting M&M’s aftermarket and financing segments.

- Gati Shakti, higher capex (6.1% GDP FY2025) drives CV/CE demand

- Road freight ~60% promotes heavy-duty adoption

- Domestic CV industry ~12% YoY growth in 2024

Regulatory Stability and Tax Policy

Consistency in GST rates (current standard rate 18% for most auto inputs) and a 22% corporate tax baseline aids Mahindra & Mahindra in planning Rs 4,500–5,000 crore annual capex announced for FY2024–25, enabling predictable cash-flow modeling.

Frequent changes in luxury/cess tariffs—e.g., higher cess on large SUVs—would force retail price adjustments that could dent volumes; M&M reported 9% YoY PV growth in FY2024 despite stable levies.

Regulatory stability supports multi-year investments: M&M’s INR 1,000 crore EV R&D commitment through 2025 relies on predictable tax and incentive regimes to justify long-horizon ROI assumptions.

- GST 18% + corporate tax 22% => predictable capex planning

- Luxury/cess changes risk SUV pricing and demand

- Stable policy underpins INR 1,000–5,000 crore multi-year investments

M&M set to gain from EV, tractor & CV demand but faces export/tariff and cess risks

Political support for EVs (FAME-III; INR 25–35k crore 2024–25), rural transfers (PM-Kisan >INR 200bn 2024) and Gati Shakti capex (6.1% GDP FY2025) bolster M&M’s EV, tractor and CV demand; exports +18% YoY (farm equipment FY2024) and ~17% global tractor share expose M&M to trade/tariff risks and luxury cess volatility that could swing volumes and margins.

| Metric | 2024/25 |

|---|---|

| FAME-III budget | INR 25–35k crore |

| PM-Kisan payouts | >INR 200bn |

| Govt capex | 6.1% GDP |

| Tractor global share | ~17% |

| Exports farm eq. | +18% YoY |

What is included in the product

Explores how external macro-environmental factors uniquely affect Mahindra & Mahindra across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and industry-specific examples to identify threats and opportunities for executives, investors, and strategists.

A concise, shareable PESTLE summary of Mahindra & Mahindra that’s visually segmented for quick interpretation, ideal for meetings or presentations and easily dropped into slides or strategy packs.

Economic factors

Interest Rate and Financing Availability

The Reserve Bank of India’s policy rate (repo at 6.50% as of Dec 2025) directly influences vehicle and tractor loan costs, affecting Mahindra & Mahindra’s retail demand, especially among price-sensitive rural buyers; a 100bps rise historically cuts tractor sales by ~4-6%. High rates also raise funding costs for M&M’s capex plans, increasing weighted average cost of capital. Mahindra Finance mitigates this by offering customized EMI structures and risk-priced loans, holding ~18% market share in rural vehicle finance (2024).

Commodity Price Inflation

Fluctuations in steel, aluminium and rare earth prices—steel up ~28% YTD in 2024 and lithium carbonate rising ~40% in 2023—squeeze Mahindra & Mahindra’s manufacturing margins, especially for EVs where battery metals are material.

With global supply-chain volatility causing input-cost swings, M&M must use hedging and value-engineering; M&M reported raw-materials cost inflation of ~6–8% in FY2024 impacting EBITDA.

Sustained raw-material inflation could necessitate vehicle price increases, risking competitiveness in India’s price-sensitive market where M&M holds ~17% share in utility vehicle segment (2024).

Rural Income and Monsoon Performance

Around 40% of Mahindra & Mahindra’s FY2024 automotive and farm revenues are exposed to rural India; with the 2023 monsoon deficit of 8% cutting kharif output and rural income growth slowing to 3.5% in 2023, tractor volumes fell 5% YoY. A normal 2024 monsoon boosted kharif production estimates by 6%, supporting stronger demand for tractors and compact SUVs, while poor or erratic rains force tighter production, inventory and credit risk management.

Currency Exchange Rate Volatility

As a multinational, Mahindra & Mahindra faces INR volatility versus USD and EUR; a 10% INR depreciation in 2023–24 raised import bills for electronics and EV parts by an estimated 8–12%, while boosting tractor export competitiveness—exports grew ~15% YoY in FY2024.

Weaker rupee helps overseas tractor margins but raises costs for imported semiconductors and battery components, squeezing consolidated gross margins; hedging and local sourcing are key to protect profitability of international business units.

- INR depreciation 2023–24: ~10%; import cost impact estimated 8–12%

- Tractor exports FY2024: ~+15% YoY

- Mitigation: hedging, local sourcing, supplier diversification

GDP Growth and Urban Consumption

India's 7.2% GDP growth in FY2023‑24 and projected 6.4% in 2025 by IMF boosts demand for Mahindra's premium SUVs and Tech Mahindra's services as urban consumption rises.

Rising middle‑class incomes and urbanization—urban population ~35% and middle‑class projected >250m households by 2025—shift preferences to feature‑rich vehicles, benefiting Mahindra's higher‑margin models.

Mahindra's market share in PVs and ability to convert rising affluence into sales, plus Tech Mahindra's IT revenue growth (FY2024 revenue ~USD 4.5bn), will determine competitive positioning.

- GDP growth: 7.2% FY2023‑24; IMF 2025 est 6.4%

- Urban population ~35%; middle class >250m households by 2025

- Tech Mahindra FY2024 revenue ~USD 4.5bn

- Success hinges on converting demand into premium SUV sales and IT service contracts

RBI rates, raw‑material spikes and INR swing reshape tractor costs, exports and growth

Economic drivers: RBI repo 6.50% (Dec 2025) affects rural loan costs; 100bps hike cuts tractor sales ~4–6%. FY2024 raw‑material inflation ~6–8%; steel +28% YTD 2024; lithium carbonate +40% (2023). INR depreciation ~10% (2023–24) raised import costs 8–12% but boosted tractor exports +15% FY2024. India GDP 7.2% FY2023‑24; IMF 2025 est 6.4%.

| Metric | Value |

|---|---|

| Repo | 6.50% (Dec 2025) |

| Steel | +28% YTD 2024 |

| Li carbonate | +40% (2023) |

| INR dep. | ~10% (2023–24) |

| Tractor exports | +15% FY2024 |

| GDP | 7.2% FY2023‑24 |

Preview the Actual Deliverable

Mahindra & Mahindra PESTLE Analysis

The preview shown here is the exact Mahindra & Mahindra PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. The layout, content, and structure visible here are exactly what you’ll be able to download immediately after buying. No placeholders, no teasers—this is the real, finished file you’ll own upon checkout.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Competitive Advantage Starts with This Report

Explore how regulatory shifts, economic cycles, and emerging technologies are reshaping Mahindra & Mahindra’s strategic landscape in our concise PESTLE snapshot—ideal for investors and strategists seeking actionable context. Purchase the full PESTLE to access a comprehensive, editable report with deep-dive insights, risk assessments, and opportunity maps you can apply immediately.

Political factors

Government Electric Vehicle Incentives

The Indian government’s FAME-III and state EV subsidies, totaling an estimated INR 25,000–35,000 crore (2024–25 allocations), lower EV acquisition costs and boost demand for Mahindra’s Born Electric models; e.g., passenger EV sales grew ~45% YoY in FY2024, aiding Mahindra’s urban market push.

Rural Development and Agricultural Subsidies

Government spending on rural infrastructure and direct benefit transfers like PM-Kisan, which paid over 200 billion INR in 2024, directly boosts demand for Mahindra & Mahindra’s tractors and farm equipment by increasing farmer liquidity and purchasing power.

Mahindra’s domestic tractor volumes—about 300,000 units in FY2024—are closely correlated with rural credit flow and subsidy disbursements that enable mechanization upgrades.

A reduction or reallocation of populist/developmental budgets could cause sharp demand swings in the farm equipment segment, affecting Mahindra’s core revenue stream and margins.

Geopolitical Trade Relations

As Mahindra & Mahindra expands in the Americas, Africa and Southeast Asia, FTAs and tariffs materially affect export competitiveness; exports grew 18% YoY in FY2024 for the farm equipment segment, highlighting sensitivity to trade barriers. Geopolitical tensions and rising protectionism—20–35% import duties in some African markets—can disrupt supply chains and raise costs for imported high-tech components. Mahindra must actively manage bilateral trade risks and localize sourcing to preserve its leading global tractor market share of ~17% in FY2024.

Infrastructure Development Initiatives

India’s Gati Shakti and similar infrastructure programs boost demand for Mahindra & Mahindra’s CVs and construction equipment; government capital expenditure rose to 6.1% of GDP in FY2025, supporting higher public works spending.

Improved road connectivity shortens logistics times—road freight share ~60%—encouraging fleet upgrades to heavy-duty solutions, aiding M&M’s CV sales growth (domestic CV industry grew ~12% YoY in 2024).

Political focus on connectivity underpins long-term expansion of domestic logistics and automotive sectors, benefiting M&M’s aftermarket and financing segments.

- Gati Shakti, higher capex (6.1% GDP FY2025) drives CV/CE demand

- Road freight ~60% promotes heavy-duty adoption

- Domestic CV industry ~12% YoY growth in 2024

Regulatory Stability and Tax Policy

Consistency in GST rates (current standard rate 18% for most auto inputs) and a 22% corporate tax baseline aids Mahindra & Mahindra in planning Rs 4,500–5,000 crore annual capex announced for FY2024–25, enabling predictable cash-flow modeling.

Frequent changes in luxury/cess tariffs—e.g., higher cess on large SUVs—would force retail price adjustments that could dent volumes; M&M reported 9% YoY PV growth in FY2024 despite stable levies.

Regulatory stability supports multi-year investments: M&M’s INR 1,000 crore EV R&D commitment through 2025 relies on predictable tax and incentive regimes to justify long-horizon ROI assumptions.

- GST 18% + corporate tax 22% => predictable capex planning

- Luxury/cess changes risk SUV pricing and demand

- Stable policy underpins INR 1,000–5,000 crore multi-year investments

M&M set to gain from EV, tractor & CV demand but faces export/tariff and cess risks

Political support for EVs (FAME-III; INR 25–35k crore 2024–25), rural transfers (PM-Kisan >INR 200bn 2024) and Gati Shakti capex (6.1% GDP FY2025) bolster M&M’s EV, tractor and CV demand; exports +18% YoY (farm equipment FY2024) and ~17% global tractor share expose M&M to trade/tariff risks and luxury cess volatility that could swing volumes and margins.

| Metric | 2024/25 |

|---|---|

| FAME-III budget | INR 25–35k crore |

| PM-Kisan payouts | >INR 200bn |

| Govt capex | 6.1% GDP |

| Tractor global share | ~17% |

| Exports farm eq. | +18% YoY |

What is included in the product

Explores how external macro-environmental factors uniquely affect Mahindra & Mahindra across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and industry-specific examples to identify threats and opportunities for executives, investors, and strategists.

A concise, shareable PESTLE summary of Mahindra & Mahindra that’s visually segmented for quick interpretation, ideal for meetings or presentations and easily dropped into slides or strategy packs.

Economic factors

Interest Rate and Financing Availability

The Reserve Bank of India’s policy rate (repo at 6.50% as of Dec 2025) directly influences vehicle and tractor loan costs, affecting Mahindra & Mahindra’s retail demand, especially among price-sensitive rural buyers; a 100bps rise historically cuts tractor sales by ~4-6%. High rates also raise funding costs for M&M’s capex plans, increasing weighted average cost of capital. Mahindra Finance mitigates this by offering customized EMI structures and risk-priced loans, holding ~18% market share in rural vehicle finance (2024).

Commodity Price Inflation

Fluctuations in steel, aluminium and rare earth prices—steel up ~28% YTD in 2024 and lithium carbonate rising ~40% in 2023—squeeze Mahindra & Mahindra’s manufacturing margins, especially for EVs where battery metals are material.

With global supply-chain volatility causing input-cost swings, M&M must use hedging and value-engineering; M&M reported raw-materials cost inflation of ~6–8% in FY2024 impacting EBITDA.

Sustained raw-material inflation could necessitate vehicle price increases, risking competitiveness in India’s price-sensitive market where M&M holds ~17% share in utility vehicle segment (2024).

Rural Income and Monsoon Performance

Around 40% of Mahindra & Mahindra’s FY2024 automotive and farm revenues are exposed to rural India; with the 2023 monsoon deficit of 8% cutting kharif output and rural income growth slowing to 3.5% in 2023, tractor volumes fell 5% YoY. A normal 2024 monsoon boosted kharif production estimates by 6%, supporting stronger demand for tractors and compact SUVs, while poor or erratic rains force tighter production, inventory and credit risk management.

Currency Exchange Rate Volatility

As a multinational, Mahindra & Mahindra faces INR volatility versus USD and EUR; a 10% INR depreciation in 2023–24 raised import bills for electronics and EV parts by an estimated 8–12%, while boosting tractor export competitiveness—exports grew ~15% YoY in FY2024.

Weaker rupee helps overseas tractor margins but raises costs for imported semiconductors and battery components, squeezing consolidated gross margins; hedging and local sourcing are key to protect profitability of international business units.

- INR depreciation 2023–24: ~10%; import cost impact estimated 8–12%

- Tractor exports FY2024: ~+15% YoY

- Mitigation: hedging, local sourcing, supplier diversification

GDP Growth and Urban Consumption

India's 7.2% GDP growth in FY2023‑24 and projected 6.4% in 2025 by IMF boosts demand for Mahindra's premium SUVs and Tech Mahindra's services as urban consumption rises.

Rising middle‑class incomes and urbanization—urban population ~35% and middle‑class projected >250m households by 2025—shift preferences to feature‑rich vehicles, benefiting Mahindra's higher‑margin models.

Mahindra's market share in PVs and ability to convert rising affluence into sales, plus Tech Mahindra's IT revenue growth (FY2024 revenue ~USD 4.5bn), will determine competitive positioning.

- GDP growth: 7.2% FY2023‑24; IMF 2025 est 6.4%

- Urban population ~35%; middle class >250m households by 2025

- Tech Mahindra FY2024 revenue ~USD 4.5bn

- Success hinges on converting demand into premium SUV sales and IT service contracts

RBI rates, raw‑material spikes and INR swing reshape tractor costs, exports and growth

Economic drivers: RBI repo 6.50% (Dec 2025) affects rural loan costs; 100bps hike cuts tractor sales ~4–6%. FY2024 raw‑material inflation ~6–8%; steel +28% YTD 2024; lithium carbonate +40% (2023). INR depreciation ~10% (2023–24) raised import costs 8–12% but boosted tractor exports +15% FY2024. India GDP 7.2% FY2023‑24; IMF 2025 est 6.4%.

| Metric | Value |

|---|---|

| Repo | 6.50% (Dec 2025) |

| Steel | +28% YTD 2024 |

| Li carbonate | +40% (2023) |

| INR dep. | ~10% (2023–24) |

| Tractor exports | +15% FY2024 |

| GDP | 7.2% FY2023‑24 |

Preview the Actual Deliverable

Mahindra & Mahindra PESTLE Analysis

The preview shown here is the exact Mahindra & Mahindra PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. The layout, content, and structure visible here are exactly what you’ll be able to download immediately after buying. No placeholders, no teasers—this is the real, finished file you’ll own upon checkout.