Maisonneuve SAS Boston Consulting Group Matrix

Visual. Strategic. Downloadable.

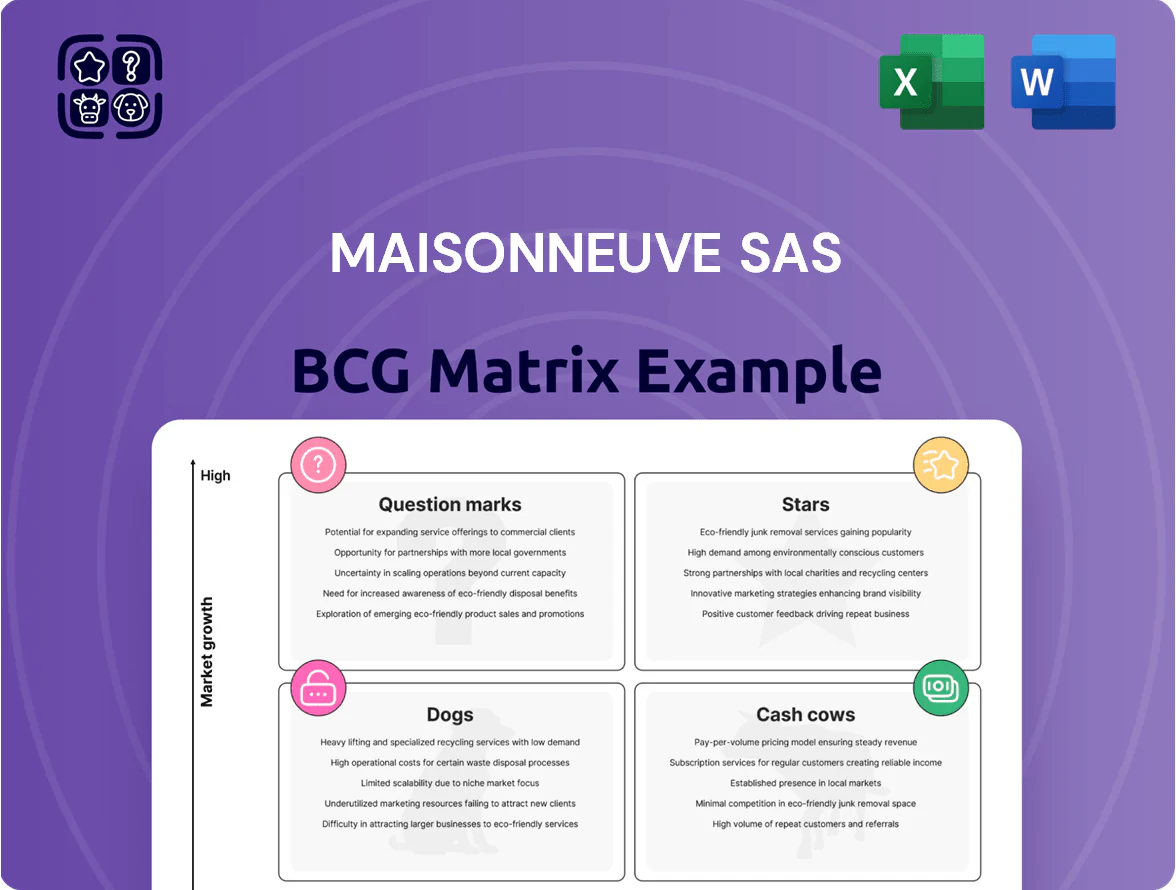

Maisonneuve SAS’s BCG Matrix preview highlights product groups facing pivotal market moments—from emerging Question Marks to steady Cash Cows—revealing where growth capital or divestment may be needed to optimize returns. This snapshot teases quadrant placements and high-level implications, but the full BCG Matrix delivers precise market-share data, trend-driven forecasts, and actionable strategies tailored to each product line. Purchase the complete report for quadrant-by-quadrant analysis, editable Word and Excel files, and step-by-step recommendations to sharpen investment and product decisions.

Stars

Advanced Laser and Plasma Cutting Services

As of late 2025 Maisonneuve SAS commands roughly 28% of France’s contract high-precision metal-processing market, driving a 34% year-on-year revenue rise in its Advanced Laser and Plasma Cutting Services segment.

These services meet needs for complex geometries and ±0.05 mm tolerances in robotics and specialized machinery, supporting 42% of the company’s order value from aerospace and automation clients.

Ongoing capex—about €12m planned 2026 for machines and sensors—keeps uptime and precision high, while this segment delivers the fastest growth and now accounts for 46% of group gross profit.

Specialized Stainless Steel for Aerospace

France’s aerospace market recovered strongly through 2025, lifting demand for high-performance stainless steel by 6% year-on-year; Maisonneuve SAS supplies certified, flight-safety grade alloys and holds an estimated 35–40% niche share among certified suppliers.

High entry barriers—certification lead times of 12–24 months and CAPEX for traceable QA—keep margins high; Maisonneuve’s first-to-market advantage in two specialty alloys drove 18% segment revenue growth in 2025.

Sustainable Green Steel Distribution

With the EU Carbon Border Adjustment Mechanism active and tighter regs, low-carbon steel demand grew ~28% y/y to 2025, making green-steel a high-growth BCG star for Maisonneuve SAS.

Maisonneuve has secured long-term offtakes from hydropower-based mills, targeting construction and automotive clients pursuing net-zero; this positions it as a market leader for green distribution.

This segment needs heavy cash to prepay supply and logistics (estimated €80–120m CAPEX/working capital through 2026) but promises margin premium ~3–6% and strategic moat.

As blast-furnace share falls (EU BF output down ~18% since 2022), green-steel distribution is set to mature into a future cash cow for Maisonneuve.

Aluminum Alloys for Electric Vehicle Components

Aluminum Alloys for Electric Vehicle Components sits as a Star: EV production growth (global EV sales +40% in 2024) drives high demand for lightweight alloys in battery enclosures and frames, a segment growing ~18% CAGR to 2028.

Maisonneuve captured a large regional share via 50,000-ton inventory and same-day fulfillment; specialized processing lifts margins, with unit EBITDA estimated ~12% in 2025.

Targeting the auto sector—20% of steel use—Maisonneuve pivots as OEMs shift to EVs; continued capex in cutting and handling (estimated €10–15M) is needed to keep leadership.

- High-growth: EV-driven alloy demand, ~18% CAGR

- Inventory edge: 50,000 tons, immediate fulfillment

- Profitability: ~12% unit EBITDA (2025 est.)

- Required spend: €10–15M specialized capex

High-Strength Steel for Renewable Infrastructure

Demand for specialized steel in wind and solar projects is rising about 5% annually through 2025, and Maisonneuve SAS leads this Stars segment with strong orders for heavy-duty structural components for 120+ MW of installations in 2024.

The segment ties up cash in bulk inventory and logistics—working capital hit ~€45m in 2024—but remains market leader due to a resilient supply chain and long-term contracts covering ~60% of 2025 capacity.

As global energy transitions accelerate, high-strength renewable steel stays a high-growth, high-share pillar in Maisonneuve’s roadmap, targeting ~8% revenue CAGR into 2026.

- 5% annual demand growth through 2025

- 120+ MW installed in 2024

- €45m working capital tied up in 2024

- 60% of 2025 capacity pre-contracted

- Target ~8% revenue CAGR to 2026

High‑growth "Stars" drive 46% gross profit, €150–180m capex to fuel double‑digit CAGRs

Stars: high-share, high-growth units—Advanced Cutting, Green-steel distribution, EV aluminum, and Renewables steel—drive 46% group gross profit, ~28% market share in France, and target combined capex/WC €150–180m through 2026 to support ~12% blended unit EBITDA and 8–18% segment CAGRs.

| Segment | 2025 share | 2025 EBITDA | Capex/WC need | Target CAGR |

|---|---|---|---|---|

| Advanced Cutting | 28% | — | €12m | 34% y/y |

| Green-steel | 35–40% (niche) | +3–6pp premium | €80–120m | high |

| EV Aluminum | regional leader | ~12% | €10–15m | ~18% |

| Renewables Steel | 60% capacity pre-contracted | — | €45m WC | ~8% |

What is included in the product

Comprehensive BCG Matrix review of Maisonneuve SAS with quadrant-specific insights, investment recommendations, and trend-based risk assessment.

One-page overview placing each business unit in a quadrant, simplifying strategic decisions for busy executives.

Cash Cows

Standard Structural Beams and Sections

Standard steel beams for commercial construction form a mature market where Maisonneuve SAS holds a commanding ~28% national share, producing stable EBITDA margins near 18% in 2025 and €72M in free cash flow that year.

Low marketing spend—under 2% of sales—plus a 15‑year reputation means predictable cash generation, funding €12M invested in green steel R&D and capital for faster‑growing units.

Even with French construction growth at ~1.2% in 2025, this segment remains the bedrock of Maisonneuve’s liquidity and dividend capacity.

Concrete Reinforcement and Wire Mesh

Concrete reinforcement and wire mesh are core cash cows for Maisonneuve SAS, with steady 2024 demand covering ~28% of group revenue (€72m of €257m) and >60% domestic market share in France’s commercial construction segment.

Operating in a mature market, margins (~14% EBITDA margin in 2024) come from scale, long-term distributor ties, and 3.5% YoY production-cost reductions from process automation—funding digital and tech modernization.

Galvanized Flat Products

Maisonneuve SAS’s galvanized flat products are a cash cow: production and wholesale for industrial corrosion-resistant flats show market maturity with a 2025 market share near 48% in France and stable annual demand growth of ~2.5%.

Serving a loyal industrial client base, these flats generate EBITDA margins around 16% and annual free cash flow of ~€22m, funding debt service (net debt €85m, net leverage 1.9x) and selective investments.

With sector growth modest, management prioritizes plant uptime and logistics efficiency—capex kept at €6–8m/year—to maximize cash extraction while supporting riskier market entries.

Standard Steel Tubes and Piping

The wholesale of standard carbon steel tubes is a high-share, low-growth cash cow for Maisonneuve SAS, consistently beating peers on logistics and availability and delivering gross margins near 28% in 2025 thanks to a 50,000-ton inventory capacity.

Demand is stable and predictable, requiring minimal capex (≈€3–5m annually) to maintain productivity, letting this unit cover admin costs and fund expansion initiatives across the group.

- Market share: leading segment (2024–25)

- Inventory: 50,000 tons

- Gross margin: ~28% (2025)

- Annual maintenance capex: €3–5m

- Role: funds admin and growth

Laminated Flats and Basic Profiles

Laminated flats and basic metal profiles (angles, tees) are cash cows with >60% domestic market share and annual volumes of ~45,000 tonnes, requiring minimal promotion due to standard demand across workshops.

Maisonneuve leverages a 40+-year presence to offer 3–5% price advantage and 24–48 hour delivery in key regions, keeping gross margins around 18% in 2025.

These steady cash flows—≈€22M EBITDA from the product line in 2025—fund high-risk question-mark projects and R&D without external financing.

- High volume: ~45,000 t/yr

- Market share: >60% domestic

- Price edge: 3–5%

- Delivery: 24–48 h

- 2025 EBITDA: ≈€22M

Maisonneuve’s €72M FCF engine funds €12M green R&D, covers €85M net debt

Maisonneuve’s cash cows (standard beams, reinforcement mesh, galvanized flats, carbon tubes, laminated flats) drive ~€72M FCF in 2025, combined EBITDA margins 15–18%, funding €12M green R&D, covering net debt €85M (1.9x) and ~€20–30M annual capex.

| Product | 2025 share | EBITDA% | FCF€M | Capex€/yr |

|---|---|---|---|---|

| Beams/mesh | ~28% | 18% | 72 | 12 |

| Galv flats | 48% | 16% | 22 | 6–8 |

| Tubes | leading | 28% gross | — | 3–5 |

| Laminated | >60% | 18% | 22 | — |

What You See Is What You Get

Maisonneuve SAS BCG Matrix

The file you're previewing is the exact Maisonneuve SAS BCG Matrix document you'll receive after purchase—no watermarks, no demo content, just the fully formatted, analysis-ready report designed for strategic clarity and professional presentation.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Visual. Strategic. Downloadable.

Maisonneuve SAS’s BCG Matrix preview highlights product groups facing pivotal market moments—from emerging Question Marks to steady Cash Cows—revealing where growth capital or divestment may be needed to optimize returns. This snapshot teases quadrant placements and high-level implications, but the full BCG Matrix delivers precise market-share data, trend-driven forecasts, and actionable strategies tailored to each product line. Purchase the complete report for quadrant-by-quadrant analysis, editable Word and Excel files, and step-by-step recommendations to sharpen investment and product decisions.

Stars

Advanced Laser and Plasma Cutting Services

As of late 2025 Maisonneuve SAS commands roughly 28% of France’s contract high-precision metal-processing market, driving a 34% year-on-year revenue rise in its Advanced Laser and Plasma Cutting Services segment.

These services meet needs for complex geometries and ±0.05 mm tolerances in robotics and specialized machinery, supporting 42% of the company’s order value from aerospace and automation clients.

Ongoing capex—about €12m planned 2026 for machines and sensors—keeps uptime and precision high, while this segment delivers the fastest growth and now accounts for 46% of group gross profit.

Specialized Stainless Steel for Aerospace

France’s aerospace market recovered strongly through 2025, lifting demand for high-performance stainless steel by 6% year-on-year; Maisonneuve SAS supplies certified, flight-safety grade alloys and holds an estimated 35–40% niche share among certified suppliers.

High entry barriers—certification lead times of 12–24 months and CAPEX for traceable QA—keep margins high; Maisonneuve’s first-to-market advantage in two specialty alloys drove 18% segment revenue growth in 2025.

Sustainable Green Steel Distribution

With the EU Carbon Border Adjustment Mechanism active and tighter regs, low-carbon steel demand grew ~28% y/y to 2025, making green-steel a high-growth BCG star for Maisonneuve SAS.

Maisonneuve has secured long-term offtakes from hydropower-based mills, targeting construction and automotive clients pursuing net-zero; this positions it as a market leader for green distribution.

This segment needs heavy cash to prepay supply and logistics (estimated €80–120m CAPEX/working capital through 2026) but promises margin premium ~3–6% and strategic moat.

As blast-furnace share falls (EU BF output down ~18% since 2022), green-steel distribution is set to mature into a future cash cow for Maisonneuve.

Aluminum Alloys for Electric Vehicle Components

Aluminum Alloys for Electric Vehicle Components sits as a Star: EV production growth (global EV sales +40% in 2024) drives high demand for lightweight alloys in battery enclosures and frames, a segment growing ~18% CAGR to 2028.

Maisonneuve captured a large regional share via 50,000-ton inventory and same-day fulfillment; specialized processing lifts margins, with unit EBITDA estimated ~12% in 2025.

Targeting the auto sector—20% of steel use—Maisonneuve pivots as OEMs shift to EVs; continued capex in cutting and handling (estimated €10–15M) is needed to keep leadership.

- High-growth: EV-driven alloy demand, ~18% CAGR

- Inventory edge: 50,000 tons, immediate fulfillment

- Profitability: ~12% unit EBITDA (2025 est.)

- Required spend: €10–15M specialized capex

High-Strength Steel for Renewable Infrastructure

Demand for specialized steel in wind and solar projects is rising about 5% annually through 2025, and Maisonneuve SAS leads this Stars segment with strong orders for heavy-duty structural components for 120+ MW of installations in 2024.

The segment ties up cash in bulk inventory and logistics—working capital hit ~€45m in 2024—but remains market leader due to a resilient supply chain and long-term contracts covering ~60% of 2025 capacity.

As global energy transitions accelerate, high-strength renewable steel stays a high-growth, high-share pillar in Maisonneuve’s roadmap, targeting ~8% revenue CAGR into 2026.

- 5% annual demand growth through 2025

- 120+ MW installed in 2024

- €45m working capital tied up in 2024

- 60% of 2025 capacity pre-contracted

- Target ~8% revenue CAGR to 2026

High‑growth "Stars" drive 46% gross profit, €150–180m capex to fuel double‑digit CAGRs

Stars: high-share, high-growth units—Advanced Cutting, Green-steel distribution, EV aluminum, and Renewables steel—drive 46% group gross profit, ~28% market share in France, and target combined capex/WC €150–180m through 2026 to support ~12% blended unit EBITDA and 8–18% segment CAGRs.

| Segment | 2025 share | 2025 EBITDA | Capex/WC need | Target CAGR |

|---|---|---|---|---|

| Advanced Cutting | 28% | — | €12m | 34% y/y |

| Green-steel | 35–40% (niche) | +3–6pp premium | €80–120m | high |

| EV Aluminum | regional leader | ~12% | €10–15m | ~18% |

| Renewables Steel | 60% capacity pre-contracted | — | €45m WC | ~8% |

What is included in the product

Comprehensive BCG Matrix review of Maisonneuve SAS with quadrant-specific insights, investment recommendations, and trend-based risk assessment.

One-page overview placing each business unit in a quadrant, simplifying strategic decisions for busy executives.

Cash Cows

Standard Structural Beams and Sections

Standard steel beams for commercial construction form a mature market where Maisonneuve SAS holds a commanding ~28% national share, producing stable EBITDA margins near 18% in 2025 and €72M in free cash flow that year.

Low marketing spend—under 2% of sales—plus a 15‑year reputation means predictable cash generation, funding €12M invested in green steel R&D and capital for faster‑growing units.

Even with French construction growth at ~1.2% in 2025, this segment remains the bedrock of Maisonneuve’s liquidity and dividend capacity.

Concrete Reinforcement and Wire Mesh

Concrete reinforcement and wire mesh are core cash cows for Maisonneuve SAS, with steady 2024 demand covering ~28% of group revenue (€72m of €257m) and >60% domestic market share in France’s commercial construction segment.

Operating in a mature market, margins (~14% EBITDA margin in 2024) come from scale, long-term distributor ties, and 3.5% YoY production-cost reductions from process automation—funding digital and tech modernization.

Galvanized Flat Products

Maisonneuve SAS’s galvanized flat products are a cash cow: production and wholesale for industrial corrosion-resistant flats show market maturity with a 2025 market share near 48% in France and stable annual demand growth of ~2.5%.

Serving a loyal industrial client base, these flats generate EBITDA margins around 16% and annual free cash flow of ~€22m, funding debt service (net debt €85m, net leverage 1.9x) and selective investments.

With sector growth modest, management prioritizes plant uptime and logistics efficiency—capex kept at €6–8m/year—to maximize cash extraction while supporting riskier market entries.

Standard Steel Tubes and Piping

The wholesale of standard carbon steel tubes is a high-share, low-growth cash cow for Maisonneuve SAS, consistently beating peers on logistics and availability and delivering gross margins near 28% in 2025 thanks to a 50,000-ton inventory capacity.

Demand is stable and predictable, requiring minimal capex (≈€3–5m annually) to maintain productivity, letting this unit cover admin costs and fund expansion initiatives across the group.

- Market share: leading segment (2024–25)

- Inventory: 50,000 tons

- Gross margin: ~28% (2025)

- Annual maintenance capex: €3–5m

- Role: funds admin and growth

Laminated Flats and Basic Profiles

Laminated flats and basic metal profiles (angles, tees) are cash cows with >60% domestic market share and annual volumes of ~45,000 tonnes, requiring minimal promotion due to standard demand across workshops.

Maisonneuve leverages a 40+-year presence to offer 3–5% price advantage and 24–48 hour delivery in key regions, keeping gross margins around 18% in 2025.

These steady cash flows—≈€22M EBITDA from the product line in 2025—fund high-risk question-mark projects and R&D without external financing.

- High volume: ~45,000 t/yr

- Market share: >60% domestic

- Price edge: 3–5%

- Delivery: 24–48 h

- 2025 EBITDA: ≈€22M

Maisonneuve’s €72M FCF engine funds €12M green R&D, covers €85M net debt

Maisonneuve’s cash cows (standard beams, reinforcement mesh, galvanized flats, carbon tubes, laminated flats) drive ~€72M FCF in 2025, combined EBITDA margins 15–18%, funding €12M green R&D, covering net debt €85M (1.9x) and ~€20–30M annual capex.

| Product | 2025 share | EBITDA% | FCF€M | Capex€/yr |

|---|---|---|---|---|

| Beams/mesh | ~28% | 18% | 72 | 12 |

| Galv flats | 48% | 16% | 22 | 6–8 |

| Tubes | leading | 28% gross | — | 3–5 |

| Laminated | >60% | 18% | 22 | — |

What You See Is What You Get

Maisonneuve SAS BCG Matrix

The file you're previewing is the exact Maisonneuve SAS BCG Matrix document you'll receive after purchase—no watermarks, no demo content, just the fully formatted, analysis-ready report designed for strategic clarity and professional presentation.