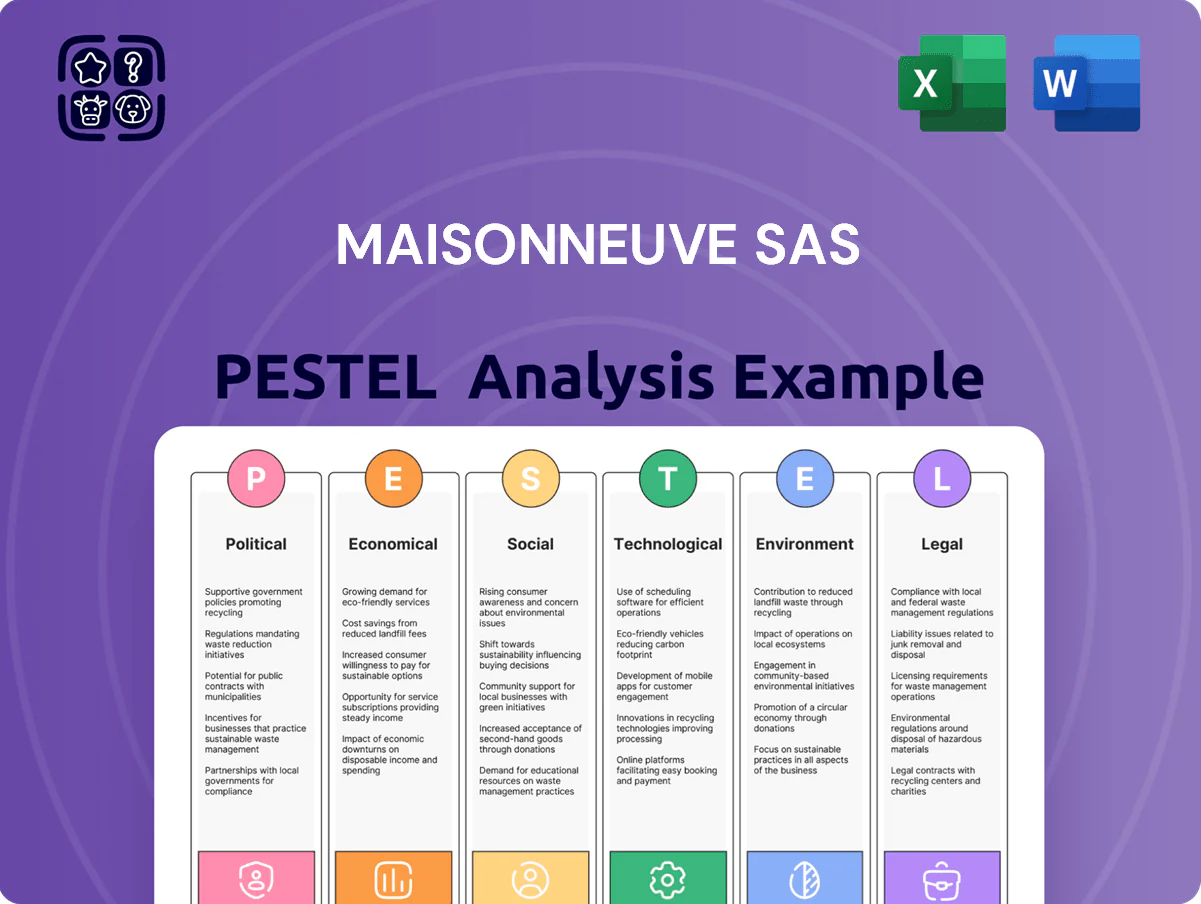

Maisonneuve SAS PESTLE Analysis

Skip the Research. Get the Strategy.

Uncover how political shifts, economic trends, and technological disruption are shaping Maisonneuve SAS’s strategic outlook with our concise PESTLE snapshot—then dive deeper with the full report for actionable insights, charts, and risk scores tailored for investors and strategists; purchase now to get the complete, ready-to-use analysis instantly.

Political factors

EU Trade Protectionism and Quotas

The EU enforces safeguard measures and quotas on steel imports, limiting non-EU volumes by roughly 3–6% annually and contributing to a 2024 intra-EU price premium of about 8–12% versus global benchmarks; Maisonneuve SAS must manage constrained external supply and higher input costs as these barriers shape raw material availability and procurement pricing.

French Infrastructure Stimulus Packages

Government-led renovation and transport expansion programs drive steady demand for structural steel and beams; France's 2025 infrastructure budget allocated €30.7bn to transport and renovation, supporting Maisonneuve SAS order visibility.

Political stances on national debt and spending directly affect long-term contract pipelines; 2024–25 public investment pledges reduced fiscal uncertainty, with public investment at 3.2% of GDP aiding project financing.

As of late 2025, France's nuclear commitment (€50bn over 2021–2030 for nuclear overhaul) and rail expansion (planned 2,000 km of upgrades by 2030) remain primary drivers of heavy metal consumption for Maisonneuve SAS.

Geopolitical Supply Chain Stability

Ongoing geopolitical tensions in Eastern Europe and the Middle East have pushed global freight rates up 28% since 2022 and raised spot prices for key alloying metals—nickel up 42% and chrome up 18% in 2023–2024—impacting Maisonneuve SAS’s import costs and lead times for special steels. Political instability increases logistics premiums and insurance, raising landed costs by an estimated 6–10% for affected shipments. Maisonneuve must keep flexible procurement, diversify suppliers, and hold strategic buffer inventories to mitigate supply shocks and currency-linked price volatility.

Energy Sovereignty and Subsidies

The French policy on industrial energy pricing, including regulated tariffs and the ARENH mechanism, directly affects Maisonneuve SAS’s plasma and laser cutting costs; industrial electricity prices averaged circa €0.12–0.15/kWh in 2024 for large users, influencing margin pressure.

State support—subsidies, price caps introduced during the 2022–24 energy crisis—improves competitiveness of local processing versus lower-cost international centers by reducing effective energy costs up to 20% for beneficiaries.

Ongoing moves toward energy sovereignty and investments in renewables and nuclear capacity aim to stabilize industrial tariffs long-term, potentially lowering volatility in utility expenses for heavy machinery.

- 2024 industrial electricity ~€0.12–0.15/kWh

- Subsidies/price caps reduced costs up to ~20% (2022–24)

- Energy independence policies target tariff stability and lower long-term volatility

Regional Industrial Development Policies

Regional political support for industrial hubs in France affects zoning and expansion for Maisonneuve SAS wholesale warehouses, with Île-de-France and Auvergne-Rhône-Alpes allocating over 1.2 billion euros in 2024–2025 industrial revitalization funds that ease permitting.

Regional incentives for metallurgical job creation, such as Hauts-de-France grants covering up to 30% of CAPEX or tax credits worth €50–€200k per new skilled job in 2024, can reduce facility upgrade costs.

Maintaining strong relationships with local elected officials and prefectures is essential to navigate administrative hurdles, shorten permit timelines (average reduced from 14 to 6 months with active engagement) and secure site-level approvals.

- Regional funds €1.2bn (2024–25) support industrial hubs

- Grants/tax credits up to 30% CAPEX or €50–€200k per job

- Active stakeholder engagement can cut permit timelines from 14 to 6 months

EU quotas and France capex lift steel prices 6–12% amid higher power and freight costs

EU import quotas raise intra-EU steel prices ~8–12% (2024); France 2025 infra budget €30.7bn and nuclear/rail capex (€50bn nuclear 2021–30; 2,000 km rail upgrades by 2030) boost demand; 2024 industrial power €0.12–0.15/kWh (subsidies cut costs up to 20%); freight and alloy shocks raised landed costs ~6–10% (2022–24).

| Metric | Value |

|---|---|

| EU price premium | 8–12% |

| France infra budget | €30.7bn (2025) |

| Industrial power | €0.12–0.15/kWh (2024) |

| Nuclear capex | €50bn (2021–30) |

| Landed cost rise | 6–10% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Maisonneuve SAS across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven, region- and industry-specific insights to identify threats and opportunities, support scenario planning, and inform investor-ready strategy and funding materials.

A concise, visually segmented PESTLE summary of Maisonneuve SAS that’s easy to drop into presentations or planning sessions, helping teams quickly align on external risks and market positioning.

Economic factors

Steel Price Volatility in Global Markets

The wholesale trade of metallurgical products is highly sensitive to iron ore and scrap prices, with benchmark iron ore futures swinging ~30% in 2024 and average EU scrap prices up ~18% year-on-year, directly pressuring Maisonneuve SAS’s procurement costs.

Demand shifts in China, which consumed ~55% of seaborne iron ore in 2024, materially alter Maisonneuve’s cost basis and resale margins.

By end-2025, hedging and strategic stockpiling to manage a realized price volatility range of ±25–35% will be critical to protect EBITDA margins.

Interest Rate Impact on Construction

High ECB rates raised the euro area benchmark to 3.75%–4.00% in 2024–25, lifting corporate borrowing costs and pushing average Eurozone construction loan rates above 5%, which dampens large project financing for tubes, beams and concrete buyers.

Inflationary Pressures on Operational Costs

Persistent inflation—France's CPI rose 4.2% in 2024—pushes Maisonneuve SAS higher labor, logistics and specialty gas costs (acetylene/oxygen prices up ~12% YoY), squeezing margins on oxy-cutting and laser services.

Passing costs risks losing price-sensitive clients to leaner rivals; 2024 industrial price index gains of 6% highlight margin pressure across metal processing.

Stable French wage growth (average manufacturing pay +3.5% in 2024) is critical to control overhead tied to skilled operators.

Currency Exchange Rate Fluctuations

As a wholesaler sourcing specialized products outside the Eurozone, Maisonneuve SAS sees procurement costs sensitive to EUR/USD moves; each 5% euro depreciation vs the dollar can raise import costs by about 4–6% for high-grade special steels.

Late-2025 data showed EUR/USD averaging ~1.08 with daily volatility around 0.8%, keeping pricing uncertainty for specialty-steel imports.

Strategic financial planning—currency hedging, invoice currency clauses, and supplier renegotiation—helps protect margins against exchange-rate shocks.

- 5% euro depreciation ≈ 4–6% import cost rise

- Late-2025 EUR/USD ~1.08, daily vol ~0.8%

- Use hedging, invoicing terms, supplier renegotiation

Growth in Renewable Energy Infrastructure

The global renewable energy market reached an estimated 1.5 trillion USD in 2024, with wind and solar investments up 8% year-on-year, creating strong demand for structural steel used in turbine foundations and panel frames.

For Maisonneuve SAS this shift offers a high-growth opportunity to diversify from residential construction, targeting projects that grew 12% in Europe in 2024.

Allocating capex and inventory toward certified structural steel for renewables is a key economic strategy for the 2026 fiscal year to capture projected sector growth.

- 2024 renewables market ~1.5T USD; wind/solar investments +8% YoY

- European renewables projects +12% in 2024

- 2026 focus: capex + inventory for structural steel in renewables

Commodity swings, tighter ECB rates and rising costs squeeze margins as renewables surge

Iron ore futures swung ~30% in 2024 and EU scrap +18% YoY, pressuring procurement; China bought ~55% of seaborne ore in 2024, impacting margins. ECB rates 3.75–4.00% (2024–25) and France CPI +4.2% (2024) raised borrowing, labor (+3.5%) and gas costs (+12%), squeezing EBITDA; EUR/USD ~1.08 late-2025, 0.8% daily vol; renewables market ~$1.5T (2024), EU projects +12%.

| Metric | Value |

|---|---|

| Iron ore vol | ~30% |

| EU scrap YoY | +18% |

| ECB rate | 3.75–4.00% |

| France CPI 2024 | +4.2% |

| EUR/USD late-2025 | ~1.08 |

| Renewables 2024 | ~$1.5T |

Same Document Delivered

Maisonneuve SAS PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use; it contains the complete Maisonneuve SAS PESTLE analysis with the same layout, insights, and structure you’ll download immediately after payment.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Skip the Research. Get the Strategy.

Uncover how political shifts, economic trends, and technological disruption are shaping Maisonneuve SAS’s strategic outlook with our concise PESTLE snapshot—then dive deeper with the full report for actionable insights, charts, and risk scores tailored for investors and strategists; purchase now to get the complete, ready-to-use analysis instantly.

Political factors

EU Trade Protectionism and Quotas

The EU enforces safeguard measures and quotas on steel imports, limiting non-EU volumes by roughly 3–6% annually and contributing to a 2024 intra-EU price premium of about 8–12% versus global benchmarks; Maisonneuve SAS must manage constrained external supply and higher input costs as these barriers shape raw material availability and procurement pricing.

French Infrastructure Stimulus Packages

Government-led renovation and transport expansion programs drive steady demand for structural steel and beams; France's 2025 infrastructure budget allocated €30.7bn to transport and renovation, supporting Maisonneuve SAS order visibility.

Political stances on national debt and spending directly affect long-term contract pipelines; 2024–25 public investment pledges reduced fiscal uncertainty, with public investment at 3.2% of GDP aiding project financing.

As of late 2025, France's nuclear commitment (€50bn over 2021–2030 for nuclear overhaul) and rail expansion (planned 2,000 km of upgrades by 2030) remain primary drivers of heavy metal consumption for Maisonneuve SAS.

Geopolitical Supply Chain Stability

Ongoing geopolitical tensions in Eastern Europe and the Middle East have pushed global freight rates up 28% since 2022 and raised spot prices for key alloying metals—nickel up 42% and chrome up 18% in 2023–2024—impacting Maisonneuve SAS’s import costs and lead times for special steels. Political instability increases logistics premiums and insurance, raising landed costs by an estimated 6–10% for affected shipments. Maisonneuve must keep flexible procurement, diversify suppliers, and hold strategic buffer inventories to mitigate supply shocks and currency-linked price volatility.

Energy Sovereignty and Subsidies

The French policy on industrial energy pricing, including regulated tariffs and the ARENH mechanism, directly affects Maisonneuve SAS’s plasma and laser cutting costs; industrial electricity prices averaged circa €0.12–0.15/kWh in 2024 for large users, influencing margin pressure.

State support—subsidies, price caps introduced during the 2022–24 energy crisis—improves competitiveness of local processing versus lower-cost international centers by reducing effective energy costs up to 20% for beneficiaries.

Ongoing moves toward energy sovereignty and investments in renewables and nuclear capacity aim to stabilize industrial tariffs long-term, potentially lowering volatility in utility expenses for heavy machinery.

- 2024 industrial electricity ~€0.12–0.15/kWh

- Subsidies/price caps reduced costs up to ~20% (2022–24)

- Energy independence policies target tariff stability and lower long-term volatility

Regional Industrial Development Policies

Regional political support for industrial hubs in France affects zoning and expansion for Maisonneuve SAS wholesale warehouses, with Île-de-France and Auvergne-Rhône-Alpes allocating over 1.2 billion euros in 2024–2025 industrial revitalization funds that ease permitting.

Regional incentives for metallurgical job creation, such as Hauts-de-France grants covering up to 30% of CAPEX or tax credits worth €50–€200k per new skilled job in 2024, can reduce facility upgrade costs.

Maintaining strong relationships with local elected officials and prefectures is essential to navigate administrative hurdles, shorten permit timelines (average reduced from 14 to 6 months with active engagement) and secure site-level approvals.

- Regional funds €1.2bn (2024–25) support industrial hubs

- Grants/tax credits up to 30% CAPEX or €50–€200k per job

- Active stakeholder engagement can cut permit timelines from 14 to 6 months

EU quotas and France capex lift steel prices 6–12% amid higher power and freight costs

EU import quotas raise intra-EU steel prices ~8–12% (2024); France 2025 infra budget €30.7bn and nuclear/rail capex (€50bn nuclear 2021–30; 2,000 km rail upgrades by 2030) boost demand; 2024 industrial power €0.12–0.15/kWh (subsidies cut costs up to 20%); freight and alloy shocks raised landed costs ~6–10% (2022–24).

| Metric | Value |

|---|---|

| EU price premium | 8–12% |

| France infra budget | €30.7bn (2025) |

| Industrial power | €0.12–0.15/kWh (2024) |

| Nuclear capex | €50bn (2021–30) |

| Landed cost rise | 6–10% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Maisonneuve SAS across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven, region- and industry-specific insights to identify threats and opportunities, support scenario planning, and inform investor-ready strategy and funding materials.

A concise, visually segmented PESTLE summary of Maisonneuve SAS that’s easy to drop into presentations or planning sessions, helping teams quickly align on external risks and market positioning.

Economic factors

Steel Price Volatility in Global Markets

The wholesale trade of metallurgical products is highly sensitive to iron ore and scrap prices, with benchmark iron ore futures swinging ~30% in 2024 and average EU scrap prices up ~18% year-on-year, directly pressuring Maisonneuve SAS’s procurement costs.

Demand shifts in China, which consumed ~55% of seaborne iron ore in 2024, materially alter Maisonneuve’s cost basis and resale margins.

By end-2025, hedging and strategic stockpiling to manage a realized price volatility range of ±25–35% will be critical to protect EBITDA margins.

Interest Rate Impact on Construction

High ECB rates raised the euro area benchmark to 3.75%–4.00% in 2024–25, lifting corporate borrowing costs and pushing average Eurozone construction loan rates above 5%, which dampens large project financing for tubes, beams and concrete buyers.

Inflationary Pressures on Operational Costs

Persistent inflation—France's CPI rose 4.2% in 2024—pushes Maisonneuve SAS higher labor, logistics and specialty gas costs (acetylene/oxygen prices up ~12% YoY), squeezing margins on oxy-cutting and laser services.

Passing costs risks losing price-sensitive clients to leaner rivals; 2024 industrial price index gains of 6% highlight margin pressure across metal processing.

Stable French wage growth (average manufacturing pay +3.5% in 2024) is critical to control overhead tied to skilled operators.

Currency Exchange Rate Fluctuations

As a wholesaler sourcing specialized products outside the Eurozone, Maisonneuve SAS sees procurement costs sensitive to EUR/USD moves; each 5% euro depreciation vs the dollar can raise import costs by about 4–6% for high-grade special steels.

Late-2025 data showed EUR/USD averaging ~1.08 with daily volatility around 0.8%, keeping pricing uncertainty for specialty-steel imports.

Strategic financial planning—currency hedging, invoice currency clauses, and supplier renegotiation—helps protect margins against exchange-rate shocks.

- 5% euro depreciation ≈ 4–6% import cost rise

- Late-2025 EUR/USD ~1.08, daily vol ~0.8%

- Use hedging, invoicing terms, supplier renegotiation

Growth in Renewable Energy Infrastructure

The global renewable energy market reached an estimated 1.5 trillion USD in 2024, with wind and solar investments up 8% year-on-year, creating strong demand for structural steel used in turbine foundations and panel frames.

For Maisonneuve SAS this shift offers a high-growth opportunity to diversify from residential construction, targeting projects that grew 12% in Europe in 2024.

Allocating capex and inventory toward certified structural steel for renewables is a key economic strategy for the 2026 fiscal year to capture projected sector growth.

- 2024 renewables market ~1.5T USD; wind/solar investments +8% YoY

- European renewables projects +12% in 2024

- 2026 focus: capex + inventory for structural steel in renewables

Commodity swings, tighter ECB rates and rising costs squeeze margins as renewables surge

Iron ore futures swung ~30% in 2024 and EU scrap +18% YoY, pressuring procurement; China bought ~55% of seaborne ore in 2024, impacting margins. ECB rates 3.75–4.00% (2024–25) and France CPI +4.2% (2024) raised borrowing, labor (+3.5%) and gas costs (+12%), squeezing EBITDA; EUR/USD ~1.08 late-2025, 0.8% daily vol; renewables market ~$1.5T (2024), EU projects +12%.

| Metric | Value |

|---|---|

| Iron ore vol | ~30% |

| EU scrap YoY | +18% |

| ECB rate | 3.75–4.00% |

| France CPI 2024 | +4.2% |

| EUR/USD late-2025 | ~1.08 |

| Renewables 2024 | ~$1.5T |

Same Document Delivered

Maisonneuve SAS PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use; it contains the complete Maisonneuve SAS PESTLE analysis with the same layout, insights, and structure you’ll download immediately after payment.