Major Cineplex Group Porter's Five Forces Analysis

From Overview to Strategy Blueprint

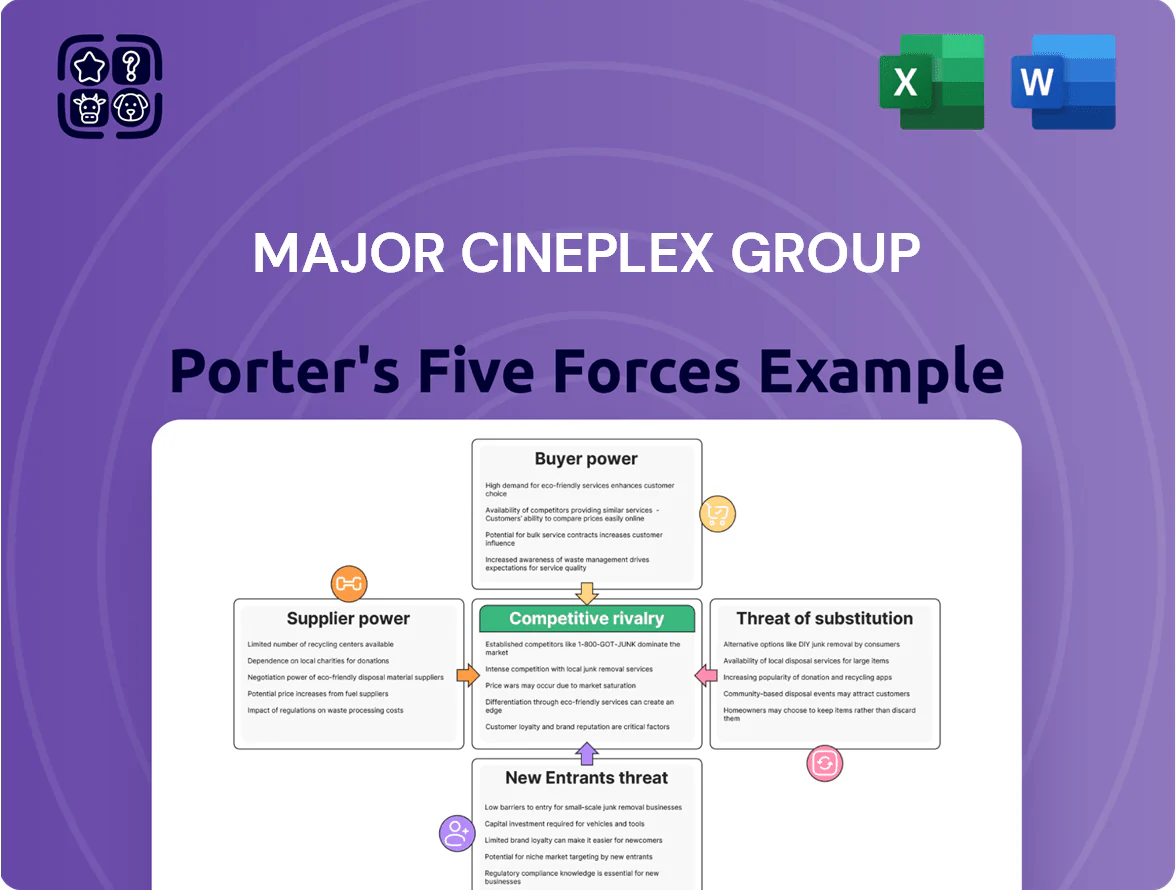

Major Cineplex faces moderate buyer power, high substitute threats from streaming and home entertainment, concentrated supplier leverage for premium content, and barriers to entry softened by digital channels.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Major Cineplex Group’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Film Studio Dominance

Major Hollywood studios and local distributors control the primary content pipeline for Major Cineplex Group, limiting access to high-budget blockbusters that drive box office—top 10 studios supplied about 78% of global box-office revenue in 2024 (MPAA/Comscore data).

With few alternatives, suppliers set revenue-share and release windows; typical distributor splits for tentpoles ran 40–55% of gross in Southeast Asia in 2024, pressuring exhibitor margins.

Media consolidation by end-2025—Disney, Warner Bros. Discovery, Universal/NBCUniversal and Paramount—left four firms accounting for over 65% of global studio output, concentrating negotiation power and scheduling leverage.

Technology Licensing Costs

Specialized projection and sound systems such as IMAX, ScreenX, and Dolby Atmos are licensed by a few global vendors, giving suppliers strong bargaining power over Major Cineplex Group; maintaining these partnerships is costly—IMAX licensing can exceed $1m per theatre retrofit and Dolby Atmos upgrades often run $100k–$300k—yet necessary to command 20–40% premium ticket pricing in the luxury segment.

Concession Product Monopolies

High-margin snacks and drinks at Major Cineplex are mostly supplied by multinationals like PepsiCo and Nestlé, which held global snack market shares of ~20–25% in 2024; their brand equity lets them demand long-term exclusive deals that limit switchability.

Concession sales made up ~35% of Major Cineplex’s 2024 ancillary revenue, so dependency on these stable suppliers raises supplier bargaining power and risks margin pressure if contract terms tighten.

Real Estate Developer Influence

Content Production Integration

Major Cineplex reduces supplier power by investing in its own production and distribution—Saham Film and M Pictures output helped the group capture ~12% of Thai box office revenue in 2024, downing external content spend by an estimated THB 450m that year.

Still, global blockbusters (Disney, Warner) drove ~58% of Thailand’s 2024 box office, so in-house titles only partially offset studios’ leverage over first-run screens and pricing.

- In-house share ~12% of box office (2024)

- Estimated external-content cost cut THB 450m (2024)

- International blockbusters ~58% box office (2024)

Studio dominance, squeezed exhibitors: rents/rights cut EBITDA as tech & snacks drive margins

Suppliers hold strong leverage: top studios supplied ~78% global box office (2024) and four majors produced >65% output (end-2025), distributor splits of 40–55% in SEA squeezed exhibitor margins, IMAX/Dolby licenses cost $100k–$1m+ per retrofit yet enable 20–40% ticket premiums, concessions (35% ancillary revenue) rely on PepsiCo/Nestlé (20–25% snack share), and mall landlords with <3% vacancy pushed rents +5–8% (2024), where a 10% rent rise ≈ −2–3ppt EBITDA.

| Metric | 2024–25 |

|---|---|

| Top studios share | ~78% |

| Four majors output | >65% (end‑2025) |

| Distributor split (tentpoles) | 40–55% |

| IMAX/Dolby retrofit | $100k–$1m+ |

| Concessions share | ~35% ancillary rev |

| Snack suppliers market | 20–25% |

| Bangkok vacancy | <3% (2024) |

| Rents YoY | +5–8% (2024) |

| 10% rent impact | ≈ −2–3ppt EBITDA |

What is included in the product

Tailored Porter's Five Forces analysis for Major Cineplex Group, uncovering competitive intensity, buyer/supplier power, threat of new entrants and substitutes, and highlighting disruptive trends and strategic levers that affect pricing, profitability, and market share.

A concise Porter's Five Forces snapshot for Major Cineplex Group—quickly highlights bargaining, rivalry, entry threats, supplier power, and substitutes to streamline strategic decisions and investor pitches.

Customers Bargaining Power

Low Switching Costs

Moviegoers in Thailand face low switching costs and can move between Major Cineplex, SF Cinema (SF Corporation), and boutique chains or OTT platforms like Netflix with no financial penalty, so Major Cineplex must constantly run promotions—its 2024 loyalty program reported 2.1 million members, a defensive play against churn. This ease of changing weekend plans puts steady pressure on pricing, service quality, and new formats (IMAX, VIP); box office share slipped 2.4% in 2023, showing migration risk. Constant innovation in F&B, app UX, and targeted discounts is required to retain market share and protect average ticket revenue, which fell 1.8% year-over-year in 2024.

Price Sensitivity in Local Markets

A large share of Thai moviegoers—survey data from 2024 shows about 62%—report being price-sensitive to ticket and concession hikes, rising further during economic slowdowns and when inflation exceeded 3.5% in 2023–24. If Major Cineplex raises prices above a perceived value point, many patrons delay visits or switch to streaming; Thailand’s SVOD subscriptions grew 18% in 2024, signaling substitution risk. This sensitivity constrains Major Cineplex’s ability to pass on higher operating costs without hurting attendance and ancillary sales.

Information Transparency

Digital platforms and social media let Thai consumers compare showtimes, ticket prices, and reviews across Major Cineplex and rivals in seconds; 72% of Thai moviegoers used apps or social media for planning in 2024, per Nielsen Thailand. This transparency pushes customers to choose convenience and price—weekday occupancy fell to 28% in 2023—so data-driven choices now dominate. Major Cineplex must run aggressive digital marketing, dynamic pricing, and real-time inventory updates to win bookings; its Q4 2024 digital sales rose 18% after targeted campaigns. Real-time price management and loyalty personalization are now table stakes.

Demand for Premium Experiences

Customers now demand luxury amenities—reclining seats, gourmet food, and premium AV—and Major Cineplex Group (MCG) sees premium ticket share rise: in 2024 premium screens accounted for ~42% of box office revenue, up from 31% in 2019.

The willingness to pay hinges on exclusivity and quality, so customers gain bargaining power by favoring theaters with top-tier experiences; MCG’s D-Box and IMAX adoption lifted average ticket price by ~28% in 2023.

- Premium screens = 42% box office (2024)

- Avg ticket price +28% from IMAX/D-Box (2023)

- Upgrades driven by customer choice

Impact of Loyalty Programs

The M Pass and membership schemes give customers predictable costs but raise expectations for ongoing value; Major Cineplex reported 2.4 million active members in 2024, who contributed about 28% of ticket revenue.

If perceived benefits fall, the company risks rapid churn among frequent visitors—losing recurring revenue and first-party data that underpins pricing and personalization.

- 2.4M active members (2024)

- 28% of ticket revenue from members

- High churn risk if benefits shrink

- Loyalists drive data-driven pricing

Price-savvy customers force Major Cineplex to discount, personalize & premium-upgrade

Customers hold strong bargaining power: low switching costs, high price sensitivity (62% in 2024), and transparency (72% use apps) force Major Cineplex to discount, personalize, and upgrade experiences; premium screens drove ~42% of box office in 2024, members (2.4M) provided 28% of ticket revenue.

| Metric | Value (2024) |

|---|---|

| Price-sensitive users | 62% |

| App/social planners | 72% |

| Premium box office | 42% |

| Active members | 2.4M |

| Member ticket rev | 28% |

Same Document Delivered

Major Cineplex Group Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Major Cineplex Group you'll receive immediately after purchase—no placeholders or samples.

The document displayed is the full, professionally formatted analysis ready for download and use the moment you buy, covering industry rivalry, buyer and supplier power, threats of entry and substitutes.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

Major Cineplex faces moderate buyer power, high substitute threats from streaming and home entertainment, concentrated supplier leverage for premium content, and barriers to entry softened by digital channels.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Major Cineplex Group’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Film Studio Dominance

Major Hollywood studios and local distributors control the primary content pipeline for Major Cineplex Group, limiting access to high-budget blockbusters that drive box office—top 10 studios supplied about 78% of global box-office revenue in 2024 (MPAA/Comscore data).

With few alternatives, suppliers set revenue-share and release windows; typical distributor splits for tentpoles ran 40–55% of gross in Southeast Asia in 2024, pressuring exhibitor margins.

Media consolidation by end-2025—Disney, Warner Bros. Discovery, Universal/NBCUniversal and Paramount—left four firms accounting for over 65% of global studio output, concentrating negotiation power and scheduling leverage.

Technology Licensing Costs

Specialized projection and sound systems such as IMAX, ScreenX, and Dolby Atmos are licensed by a few global vendors, giving suppliers strong bargaining power over Major Cineplex Group; maintaining these partnerships is costly—IMAX licensing can exceed $1m per theatre retrofit and Dolby Atmos upgrades often run $100k–$300k—yet necessary to command 20–40% premium ticket pricing in the luxury segment.

Concession Product Monopolies

High-margin snacks and drinks at Major Cineplex are mostly supplied by multinationals like PepsiCo and Nestlé, which held global snack market shares of ~20–25% in 2024; their brand equity lets them demand long-term exclusive deals that limit switchability.

Concession sales made up ~35% of Major Cineplex’s 2024 ancillary revenue, so dependency on these stable suppliers raises supplier bargaining power and risks margin pressure if contract terms tighten.

Real Estate Developer Influence

Content Production Integration

Major Cineplex reduces supplier power by investing in its own production and distribution—Saham Film and M Pictures output helped the group capture ~12% of Thai box office revenue in 2024, downing external content spend by an estimated THB 450m that year.

Still, global blockbusters (Disney, Warner) drove ~58% of Thailand’s 2024 box office, so in-house titles only partially offset studios’ leverage over first-run screens and pricing.

- In-house share ~12% of box office (2024)

- Estimated external-content cost cut THB 450m (2024)

- International blockbusters ~58% box office (2024)

Studio dominance, squeezed exhibitors: rents/rights cut EBITDA as tech & snacks drive margins

Suppliers hold strong leverage: top studios supplied ~78% global box office (2024) and four majors produced >65% output (end-2025), distributor splits of 40–55% in SEA squeezed exhibitor margins, IMAX/Dolby licenses cost $100k–$1m+ per retrofit yet enable 20–40% ticket premiums, concessions (35% ancillary revenue) rely on PepsiCo/Nestlé (20–25% snack share), and mall landlords with <3% vacancy pushed rents +5–8% (2024), where a 10% rent rise ≈ −2–3ppt EBITDA.

| Metric | 2024–25 |

|---|---|

| Top studios share | ~78% |

| Four majors output | >65% (end‑2025) |

| Distributor split (tentpoles) | 40–55% |

| IMAX/Dolby retrofit | $100k–$1m+ |

| Concessions share | ~35% ancillary rev |

| Snack suppliers market | 20–25% |

| Bangkok vacancy | <3% (2024) |

| Rents YoY | +5–8% (2024) |

| 10% rent impact | ≈ −2–3ppt EBITDA |

What is included in the product

Tailored Porter's Five Forces analysis for Major Cineplex Group, uncovering competitive intensity, buyer/supplier power, threat of new entrants and substitutes, and highlighting disruptive trends and strategic levers that affect pricing, profitability, and market share.

A concise Porter's Five Forces snapshot for Major Cineplex Group—quickly highlights bargaining, rivalry, entry threats, supplier power, and substitutes to streamline strategic decisions and investor pitches.

Customers Bargaining Power

Low Switching Costs

Moviegoers in Thailand face low switching costs and can move between Major Cineplex, SF Cinema (SF Corporation), and boutique chains or OTT platforms like Netflix with no financial penalty, so Major Cineplex must constantly run promotions—its 2024 loyalty program reported 2.1 million members, a defensive play against churn. This ease of changing weekend plans puts steady pressure on pricing, service quality, and new formats (IMAX, VIP); box office share slipped 2.4% in 2023, showing migration risk. Constant innovation in F&B, app UX, and targeted discounts is required to retain market share and protect average ticket revenue, which fell 1.8% year-over-year in 2024.

Price Sensitivity in Local Markets

A large share of Thai moviegoers—survey data from 2024 shows about 62%—report being price-sensitive to ticket and concession hikes, rising further during economic slowdowns and when inflation exceeded 3.5% in 2023–24. If Major Cineplex raises prices above a perceived value point, many patrons delay visits or switch to streaming; Thailand’s SVOD subscriptions grew 18% in 2024, signaling substitution risk. This sensitivity constrains Major Cineplex’s ability to pass on higher operating costs without hurting attendance and ancillary sales.

Information Transparency

Digital platforms and social media let Thai consumers compare showtimes, ticket prices, and reviews across Major Cineplex and rivals in seconds; 72% of Thai moviegoers used apps or social media for planning in 2024, per Nielsen Thailand. This transparency pushes customers to choose convenience and price—weekday occupancy fell to 28% in 2023—so data-driven choices now dominate. Major Cineplex must run aggressive digital marketing, dynamic pricing, and real-time inventory updates to win bookings; its Q4 2024 digital sales rose 18% after targeted campaigns. Real-time price management and loyalty personalization are now table stakes.

Demand for Premium Experiences

Customers now demand luxury amenities—reclining seats, gourmet food, and premium AV—and Major Cineplex Group (MCG) sees premium ticket share rise: in 2024 premium screens accounted for ~42% of box office revenue, up from 31% in 2019.

The willingness to pay hinges on exclusivity and quality, so customers gain bargaining power by favoring theaters with top-tier experiences; MCG’s D-Box and IMAX adoption lifted average ticket price by ~28% in 2023.

- Premium screens = 42% box office (2024)

- Avg ticket price +28% from IMAX/D-Box (2023)

- Upgrades driven by customer choice

Impact of Loyalty Programs

The M Pass and membership schemes give customers predictable costs but raise expectations for ongoing value; Major Cineplex reported 2.4 million active members in 2024, who contributed about 28% of ticket revenue.

If perceived benefits fall, the company risks rapid churn among frequent visitors—losing recurring revenue and first-party data that underpins pricing and personalization.

- 2.4M active members (2024)

- 28% of ticket revenue from members

- High churn risk if benefits shrink

- Loyalists drive data-driven pricing

Price-savvy customers force Major Cineplex to discount, personalize & premium-upgrade

Customers hold strong bargaining power: low switching costs, high price sensitivity (62% in 2024), and transparency (72% use apps) force Major Cineplex to discount, personalize, and upgrade experiences; premium screens drove ~42% of box office in 2024, members (2.4M) provided 28% of ticket revenue.

| Metric | Value (2024) |

|---|---|

| Price-sensitive users | 62% |

| App/social planners | 72% |

| Premium box office | 42% |

| Active members | 2.4M |

| Member ticket rev | 28% |

Same Document Delivered

Major Cineplex Group Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Major Cineplex Group you'll receive immediately after purchase—no placeholders or samples.

The document displayed is the full, professionally formatted analysis ready for download and use the moment you buy, covering industry rivalry, buyer and supplier power, threats of entry and substitutes.