M&G PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Discover how political shifts, economic cycles, and technological innovation are shaping M&G’s strategic outlook in our concise PESTLE snapshot—perfect for investors and strategists who need fast, actionable context; purchase the full PESTLE to access the detailed findings, data-backed implications, and ready-to-use slides and templates for immediate decision-making.

Political factors

UK Post-Brexit Regulatory Alignment

The UK in late 2025 continues streamlining financial rules post-Brexit, targeting a 10–15% reduction in capital charges under planned Solvency II reforms versus EU levels to boost competitiveness; M&G must adjust asset allocations to capture projected £200–300bn inflows into UK funds if reforms attract global insurers.

Geopolitical Volatility and Global Trade

Ongoing tensions in Eastern Europe and the Middle East have raised market volatility—MSCI World implied volatility spiked ~28% in 2024—dampening investor sentiment across M&G’s international exposures and pressuring fund flows.

Political instability drives flight-to-quality: global bond inflows rose to $120bn in 2024 Q3 while equity mutual fund flows turned negative, reducing asset management inflows and risk appetite for M&G.

Management must track trade-policy shifts: consolidated capital controls and proposed tariffs in 2024 threatened cross-border investment, risking reduced flows between Western markets and emerging economies where M&G has significant allocations.

Government Pension Reform Initiatives

The UK government’s Mansion House reforms push for pension consolidation and a shift toward private market allocations, with DB/DC schemes targeting higher illiquid exposure—UK pension schemes held £1.9tn in private markets by 2023, favoring managers like M&G with deep private-asset capabilities and £341bn AUM (2024). Potential tax-incentive changes for ISAs and pensions remain a key political lever that could materially affect M&G’s retail savings flows.

International Market Access and Licensing

UK ties with Singapore and Hong Kong shape M&G's market access; UK-Singapore trade saw bilateral investment of £45bn in 2023 and HK remains a major conduit for Asian assets, supporting M&G's expansion plans.

Local licenses and JV approvals hinge on bilateral agreements and regulatory cooperation—e.g., UK-Singapore FinTech Bridge and Memoranda of Understanding that speed authorisations.

Rising regional protectionism—ASEAN tariff adjustments and 2024/25 localization rules—could limit cross-border asset flows and slow M&G's AUM growth.

- UK–Singapore £45bn bilateral investment (2023)

- Reliance on MoUs/FinTech Bridge for licensing

- 2024/25 localization rules risk constraining AUM expansion

Public Policy on Sustainable Finance

Political pressure to meet Net Zero by 2050 has led to new reporting mandates and EU/UK green taxonomies; in 2024 the UK’s Sustainability Disclosure Requirements and EU CSRD expanded coverage to ~50,000 firms, increasing demand for compliant funds.

M&G must align strategy with government sustainability goals to remain eligible for state-linked mandates and avoid backlash; sovereign and public-sector allocations to green bonds exceeded $1.2tn globally in 2024.

Ongoing political debates over ESG priorities continue to shape M&G’s product roadmap, influencing allocation to transition finance, green bonds, and climate-aligned strategies that grew 18% year-on-year in 2024.

- Net Zero 2050 mandates driving reporting rules (SDR/CSRD)

- State-linked mandates favor compliance — public green bond market >$1.2tn (2024)

- ESG political debate directs product focus; climate-aligned assets +18% y/y (2024)

Regulatory shifts, geo-volatility and pension flows reshape M&G allocations and demand

Political shifts (UK Solvency II reform targeting 10–15% lower capital charges; £200–300bn potential UK fund inflows), geopolitical-driven volatility (MSCI World IV +28% in 2024), pension private-market demand (UK pensions £1.9tn private by 2023), and sustainability rules (SDR/CSRD covering ~50,000 firms) materially affect M&G’s allocation, product demand and cross-border licensing.

| Metric | Value |

|---|---|

| Solvency II cut | 10–15% |

| UK fund inflows (proj) | £200–300bn |

| MSCI World IV (2024) | +28% |

| UK pensions private | £1.9tn (2023) |

| SDR/CSRD coverage | ~50,000 firms |

What is included in the product

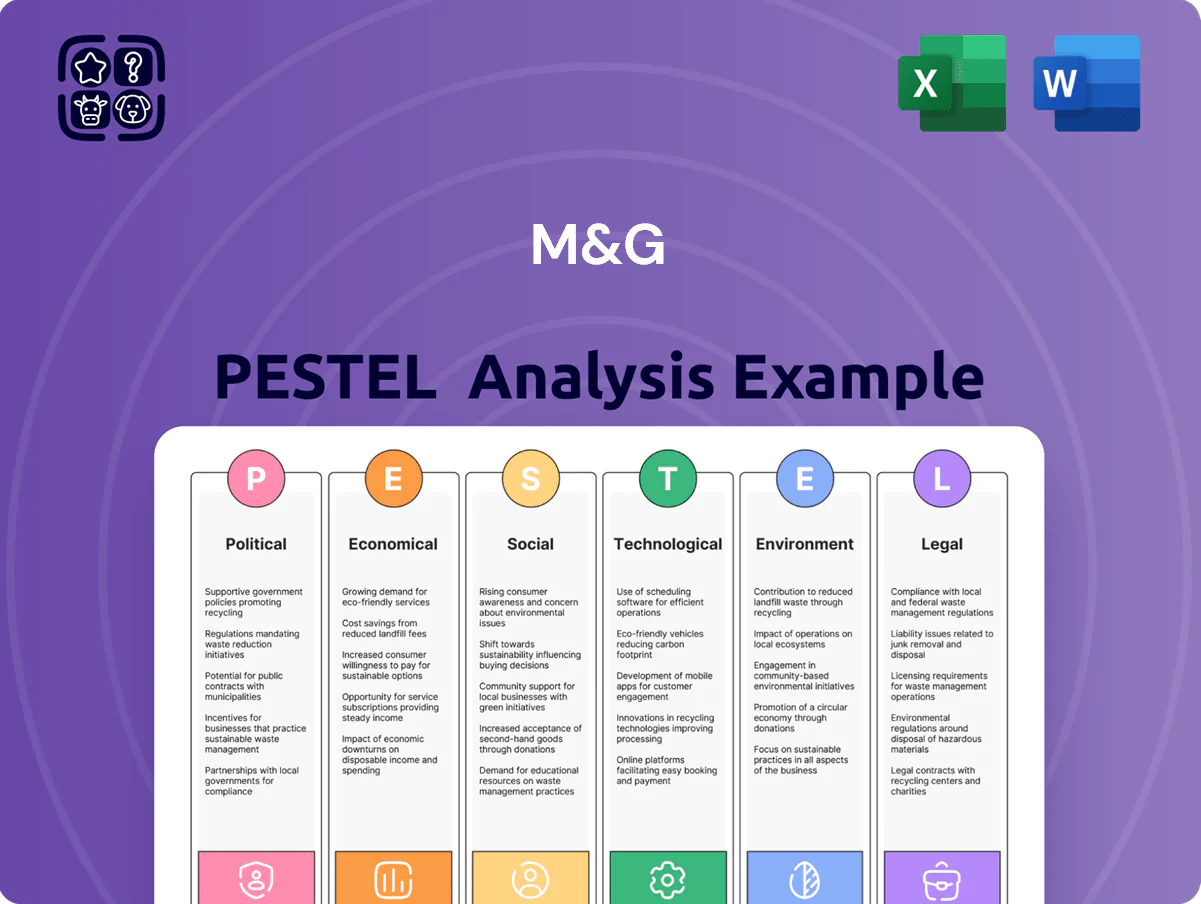

Explores how external macro-environmental factors uniquely affect M&G across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify risks and opportunities.

Provides a clean, summarized M&G PESTLE that’s visually segmented by category for quick interpretation and easily dropped into presentations or shared across teams to align on external risks and market positioning.

Economic factors

Interest Rate Environment and Monetary Policy

As of late 2025, the shift from peak policy rates (UK Bank Rate peaked at 5.25% in 2023) toward cuts—markets priced ~125 bps of BoE easing in 2025–26—raises bond prices, boosting M&G’s fixed-income asset valuations while increasing present value of life insurance liabilities; a 100 bps decline can raise duration-weighted liabilities materially. BoE and ECB moves remain primary drivers of volatility and portfolio performance.

Inflationary Pressures on Operational Costs

Persistent wage inflation and premium pay for specialized asset-management talent pushed M&G’s cost-to-income to about 62% in FY2024, up from 58% in 2022; despite UK CPI cooling to ~2.3% in 2025, staff and contractor costs remain elevated. Technology, compliance and data infrastructure spending—estimated at ~£250–300m annually—keeps overhead high. Controlling these expenses is crucial to sustain M&G’s 2024 dividend yield near 5%.

Equity Market Performance and AUM

M&Gs AUM, £337bn at H1 2025, is highly sensitive to global equity and bond market moves; a 10% MSCI World drop in 2022 cut asset values and client wealth, pressuring AUM and revenues. UK and Euro area GDP growth — 0.4% and 0.7% y/y in 2024 — constrain disposable income for retail savings, limiting net inflows. Bullish markets bolster fee-based income, while recessions prompt outflows and de-risking.

Currency Exchange Rate Fluctuations

As a global asset manager, M&G faces GBP volatility versus USD and EUR—GBP moved ~5.6% vs USD and ~3.2% vs EUR in 2024, affecting international asset valuations and translating into swings in reported AUM in sterling terms.

Currency swings can materially alter reported earnings when non-UK profits are repatriated; M&G reported 2024 non-UK revenue ~48% of group income, increasing FX sensitivity.

Hedging strategies (forward contracts, cross-currency swaps) are essential; M&G’s treasury guidance shows active FX hedges covering a meaningful portion of foreign cash flows to reduce GBP-driven earnings volatility.

- GBP volatility 2024: ~5.6% vs USD, ~3.2% vs EUR

- Non-UK revenue ~48% of group income (2024)

- Use of forwards and swaps to hedge repatriation risk

Credit Market Spreads and Default Risks

Economic health directly drives credit spreads and default risks across M&G’s corporate bond and private credit books; UK investment-grade spreads tightened to ~80bps in Jan 2025 from 140bps in Oct 2023, signaling improved confidence but recession risks persist.

Narrowing spreads imply lower impairment probability, while widening—seen in stressed Q4 2023—raises loss expectations; M&G’s tilt to high-quality credit (majority investment grade) reduces downside exposure.

- IG spreads ~80bps (Jan 2025)

- High-yield spreads >300bps during stress

- Portfolio skewed to investment-grade, lowering expected loss

BoE easing lifts bond values but spikes insurance liabilities, FX and spread risks rise

Monetary easing priced for 2025–26 (BoE cuts ~125bps) lifts bond valuations but increases PV of insurance liabilities; 100bps rate fall materially raises duration-weighted liabilities. AUM £337bn (H1 2025) and fee income are market-sensitive; 2024 non-UK revenue ~48% increases FX exposure—GBP vol 2024: ~5.6% vs USD, ~3.2% vs EUR. IG spreads ~80bps (Jan 2025), HY >300bps under stress.

| Metric | Value |

|---|---|

| AUM (H1 2025) | £337bn |

| Non-UK revenue (2024) | 48% |

| GBP vol 2024 | 5.6% vs USD / 3.2% vs EUR |

| IG spreads (Jan 2025) | ~80bps |

Preview Before You Purchase

M&G PESTLE Analysis

The preview shown here is the exact M&G PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Discover how political shifts, economic cycles, and technological innovation are shaping M&G’s strategic outlook in our concise PESTLE snapshot—perfect for investors and strategists who need fast, actionable context; purchase the full PESTLE to access the detailed findings, data-backed implications, and ready-to-use slides and templates for immediate decision-making.

Political factors

UK Post-Brexit Regulatory Alignment

The UK in late 2025 continues streamlining financial rules post-Brexit, targeting a 10–15% reduction in capital charges under planned Solvency II reforms versus EU levels to boost competitiveness; M&G must adjust asset allocations to capture projected £200–300bn inflows into UK funds if reforms attract global insurers.

Geopolitical Volatility and Global Trade

Ongoing tensions in Eastern Europe and the Middle East have raised market volatility—MSCI World implied volatility spiked ~28% in 2024—dampening investor sentiment across M&G’s international exposures and pressuring fund flows.

Political instability drives flight-to-quality: global bond inflows rose to $120bn in 2024 Q3 while equity mutual fund flows turned negative, reducing asset management inflows and risk appetite for M&G.

Management must track trade-policy shifts: consolidated capital controls and proposed tariffs in 2024 threatened cross-border investment, risking reduced flows between Western markets and emerging economies where M&G has significant allocations.

Government Pension Reform Initiatives

The UK government’s Mansion House reforms push for pension consolidation and a shift toward private market allocations, with DB/DC schemes targeting higher illiquid exposure—UK pension schemes held £1.9tn in private markets by 2023, favoring managers like M&G with deep private-asset capabilities and £341bn AUM (2024). Potential tax-incentive changes for ISAs and pensions remain a key political lever that could materially affect M&G’s retail savings flows.

International Market Access and Licensing

UK ties with Singapore and Hong Kong shape M&G's market access; UK-Singapore trade saw bilateral investment of £45bn in 2023 and HK remains a major conduit for Asian assets, supporting M&G's expansion plans.

Local licenses and JV approvals hinge on bilateral agreements and regulatory cooperation—e.g., UK-Singapore FinTech Bridge and Memoranda of Understanding that speed authorisations.

Rising regional protectionism—ASEAN tariff adjustments and 2024/25 localization rules—could limit cross-border asset flows and slow M&G's AUM growth.

- UK–Singapore £45bn bilateral investment (2023)

- Reliance on MoUs/FinTech Bridge for licensing

- 2024/25 localization rules risk constraining AUM expansion

Public Policy on Sustainable Finance

Political pressure to meet Net Zero by 2050 has led to new reporting mandates and EU/UK green taxonomies; in 2024 the UK’s Sustainability Disclosure Requirements and EU CSRD expanded coverage to ~50,000 firms, increasing demand for compliant funds.

M&G must align strategy with government sustainability goals to remain eligible for state-linked mandates and avoid backlash; sovereign and public-sector allocations to green bonds exceeded $1.2tn globally in 2024.

Ongoing political debates over ESG priorities continue to shape M&G’s product roadmap, influencing allocation to transition finance, green bonds, and climate-aligned strategies that grew 18% year-on-year in 2024.

- Net Zero 2050 mandates driving reporting rules (SDR/CSRD)

- State-linked mandates favor compliance — public green bond market >$1.2tn (2024)

- ESG political debate directs product focus; climate-aligned assets +18% y/y (2024)

Regulatory shifts, geo-volatility and pension flows reshape M&G allocations and demand

Political shifts (UK Solvency II reform targeting 10–15% lower capital charges; £200–300bn potential UK fund inflows), geopolitical-driven volatility (MSCI World IV +28% in 2024), pension private-market demand (UK pensions £1.9tn private by 2023), and sustainability rules (SDR/CSRD covering ~50,000 firms) materially affect M&G’s allocation, product demand and cross-border licensing.

| Metric | Value |

|---|---|

| Solvency II cut | 10–15% |

| UK fund inflows (proj) | £200–300bn |

| MSCI World IV (2024) | +28% |

| UK pensions private | £1.9tn (2023) |

| SDR/CSRD coverage | ~50,000 firms |

What is included in the product

Explores how external macro-environmental factors uniquely affect M&G across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify risks and opportunities.

Provides a clean, summarized M&G PESTLE that’s visually segmented by category for quick interpretation and easily dropped into presentations or shared across teams to align on external risks and market positioning.

Economic factors

Interest Rate Environment and Monetary Policy

As of late 2025, the shift from peak policy rates (UK Bank Rate peaked at 5.25% in 2023) toward cuts—markets priced ~125 bps of BoE easing in 2025–26—raises bond prices, boosting M&G’s fixed-income asset valuations while increasing present value of life insurance liabilities; a 100 bps decline can raise duration-weighted liabilities materially. BoE and ECB moves remain primary drivers of volatility and portfolio performance.

Inflationary Pressures on Operational Costs

Persistent wage inflation and premium pay for specialized asset-management talent pushed M&G’s cost-to-income to about 62% in FY2024, up from 58% in 2022; despite UK CPI cooling to ~2.3% in 2025, staff and contractor costs remain elevated. Technology, compliance and data infrastructure spending—estimated at ~£250–300m annually—keeps overhead high. Controlling these expenses is crucial to sustain M&G’s 2024 dividend yield near 5%.

Equity Market Performance and AUM

M&Gs AUM, £337bn at H1 2025, is highly sensitive to global equity and bond market moves; a 10% MSCI World drop in 2022 cut asset values and client wealth, pressuring AUM and revenues. UK and Euro area GDP growth — 0.4% and 0.7% y/y in 2024 — constrain disposable income for retail savings, limiting net inflows. Bullish markets bolster fee-based income, while recessions prompt outflows and de-risking.

Currency Exchange Rate Fluctuations

As a global asset manager, M&G faces GBP volatility versus USD and EUR—GBP moved ~5.6% vs USD and ~3.2% vs EUR in 2024, affecting international asset valuations and translating into swings in reported AUM in sterling terms.

Currency swings can materially alter reported earnings when non-UK profits are repatriated; M&G reported 2024 non-UK revenue ~48% of group income, increasing FX sensitivity.

Hedging strategies (forward contracts, cross-currency swaps) are essential; M&G’s treasury guidance shows active FX hedges covering a meaningful portion of foreign cash flows to reduce GBP-driven earnings volatility.

- GBP volatility 2024: ~5.6% vs USD, ~3.2% vs EUR

- Non-UK revenue ~48% of group income (2024)

- Use of forwards and swaps to hedge repatriation risk

Credit Market Spreads and Default Risks

Economic health directly drives credit spreads and default risks across M&G’s corporate bond and private credit books; UK investment-grade spreads tightened to ~80bps in Jan 2025 from 140bps in Oct 2023, signaling improved confidence but recession risks persist.

Narrowing spreads imply lower impairment probability, while widening—seen in stressed Q4 2023—raises loss expectations; M&G’s tilt to high-quality credit (majority investment grade) reduces downside exposure.

- IG spreads ~80bps (Jan 2025)

- High-yield spreads >300bps during stress

- Portfolio skewed to investment-grade, lowering expected loss

BoE easing lifts bond values but spikes insurance liabilities, FX and spread risks rise

Monetary easing priced for 2025–26 (BoE cuts ~125bps) lifts bond valuations but increases PV of insurance liabilities; 100bps rate fall materially raises duration-weighted liabilities. AUM £337bn (H1 2025) and fee income are market-sensitive; 2024 non-UK revenue ~48% increases FX exposure—GBP vol 2024: ~5.6% vs USD, ~3.2% vs EUR. IG spreads ~80bps (Jan 2025), HY >300bps under stress.

| Metric | Value |

|---|---|

| AUM (H1 2025) | £337bn |

| Non-UK revenue (2024) | 48% |

| GBP vol 2024 | 5.6% vs USD / 3.2% vs EUR |

| IG spreads (Jan 2025) | ~80bps |

Preview Before You Purchase

M&G PESTLE Analysis

The preview shown here is the exact M&G PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.