Manitowoc Boston Consulting Group Matrix

See the Bigger Picture

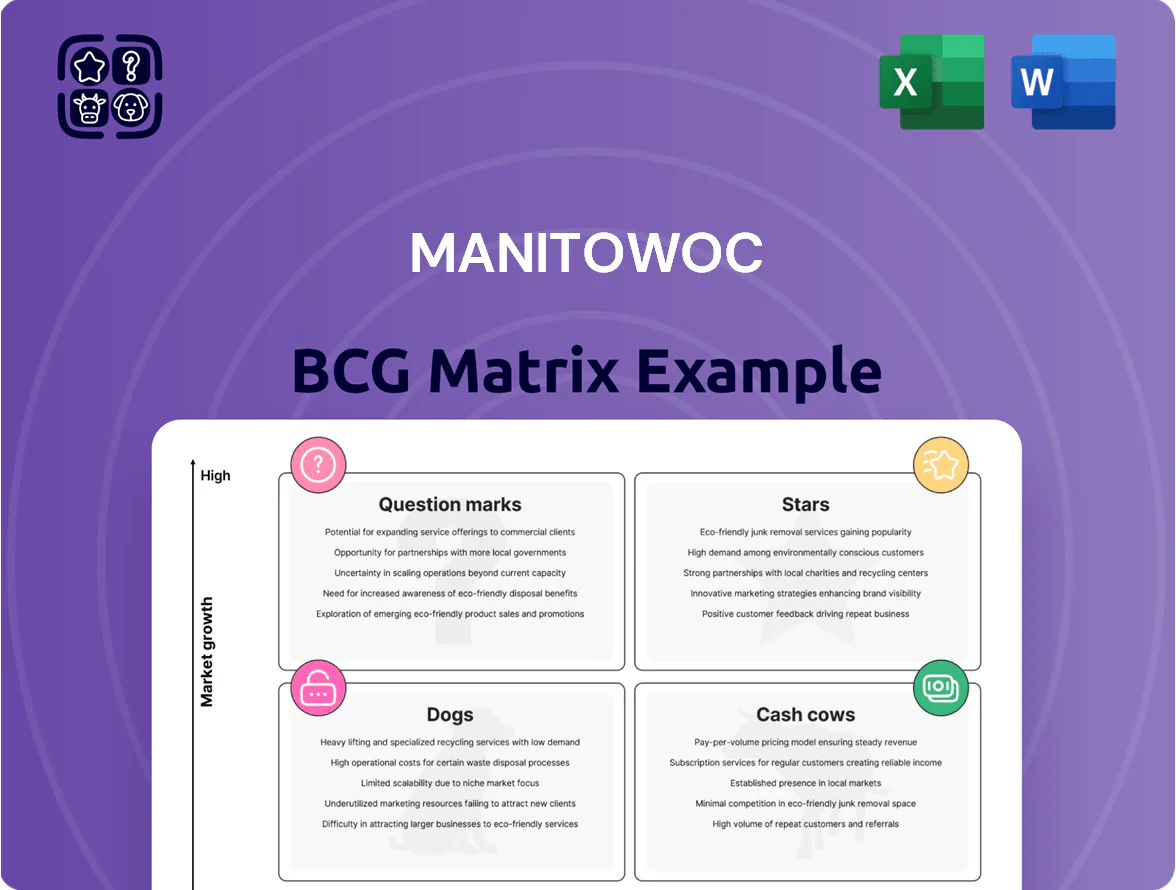

Manitowoc’s BCG Matrix preview highlights where key product lines—cranes, marine systems, and service offerings—sit across growth and market-share axes, signaling which are Stars, Cash Cows, Dogs, or Question Marks and what that means for capital allocation. This snapshot points to high-growth crane segments and mature service revenues needing different strategies. Dive deeper into this company’s BCG Matrix and gain a clear view of where its products stand—Stars, Cash Cows, Dogs, or Question Marks. Purchase the full version for a complete breakdown and strategic insights you can act on.

Stars

Aftermarket Services and CRANES+50

Aftermarket, central to CRANES+50, hit a record $690.5 million in non-new machine sales by end-2025, with parts, maintenance and field service up 10% year-over-year.

These recurring, higher-margin revenues moved Manitowoc toward a steadier cash profile; aftermarket contributed roughly 28% of 2025 service-segment revenue and improved gross margins by about 150 basis points.

Manitowoc is scaling global service footprints—adding 35 service centers in 2024–25 and boosting field-tech headcount 18%—to cement aftermarket as a stable cash generator.

Potain Tower Cranes in Europe

Potain tower cranes in Europe are a Star: the EU tower crane market grew for the fifth straight quarter in Q4 2025 with orders up ~9% YoY, and Potain holds about 28–32% market share, driven by €8–12bn public construction stimulus and rising urban prefabrication demand.

High order backlog—estimated at €1.1–1.4bn entering 2026—requires continued capex to fend off Liebherr and XCMG, but positions Potain as Manitowoc’s primary growth engine for 2026.

Mobile Hydraulic Cranes (Grove Brand)

Grove mobile hydraulic cranes are a Star in Manitowoc’s BCG matrix, leading the 51–150 ton segment which is over 33% of the global crane market (2025 IHS Markit).

Despite a soft North American macro, 2025 shipments rose 12% Y/Y and Q4 order book jumped 38%, signalling strong demand for versatile lifting solutions.

Ongoing R&D in All-Terrain and Rough-Terrain models (R&D spend ~2.8% of revenue in 2025) keeps Grove competitive as the global market recovers.

Direct-to-Customer Distribution (MGX)

Direct-to-Customer Distribution (MGX) is a high-growth move: MGX Equipment Services shifted Manitowoc toward rentals and direct sales, targeting higher lifecycle margins and growing U.S. Southeast share after acquiring Ring Power’s crane assets in Jan 2025, adding ~120 machines and boosting regional fleet by ~18%.

The unit consumes cash for fleet expansion and new branches—Manitowoc allocated $85m capex to MGX in FY2025 YTD—but offers higher returns via rental utilization rates (projected 62% vs 45% company average) and service revenue growth.

- Acquisition: Ring Power crane assets, Jan 2025, ~120 units

- Fleet boost: +18% Southeast presence

- FY2025 MGX capex: $85m YTD

- Projected utilization: 62% vs 45% company avg

High-Capacity Lattice Boom Crawlers

Manitowoc ranks top-three globally in crawler cranes, leading in high-capacity models (300+t) used for infrastructure and energy; these units drove 2024 revenue of about $1.1bn in the crane division, per company filings.

Segment for >300-ton crawlers is forecast at ~7.8% CAGR to 2026, powered by global wind and renewable projects requiring heavy lifts.

High engineering R&D and capital tooling sustain market position; unit ASPs often exceed $5M, keeping margins sensitive to commodity costs.

- Top-three market share in crawlers

- >300t segment CAGR ~7.8% to 2026

- 2024 crane revenue ~ $1.1bn

- Typical ASPs > $5M; high R&D capex

Aftermarket drives margins; Potain strong in EU—Grove shipments +12%, MGX rental rising

Aftermarket and Potain tower cranes are Stars: aftermarket hit $690.5M non-new sales in 2025 (~28% of service revenue), boosting gross margin +150bps; Potain holds ~30% EU share with €1.1–1.4bn backlog entering 2026. Grove mobile cranes led 51–150t with 12% shipment growth in 2025; MGX rental push got $85M capex YTD and projected 62% utilization.

| Metric | 2025 / Note |

|---|---|

| Aftermarket sales | $690.5M |

| Aftermarket share (service) | ~28% |

| Potain EU share | 28–32% |

| Potain backlog | €1.1–1.4B |

| Grove shipment growth | +12% Y/Y |

| MGX capex FY2025 YTD | $85M |

| MGX projected utilization | 62% |

What is included in the product

Comprehensive BCG review of Manitowoc’s units with strategic guidance on Stars, Cash Cows, Question Marks, and Dogs.

One-page Manitowoc BCG Matrix placing each segment in a quadrant for quick strategic decisions and executive review.

Cash Cows

North American Mobile Crane Fleet

The North American mobile crane fleet is Manitowoc’s largest revenue engine, accounting for about 40% of 2024 consolidated sales (roughly $900m of $2.25bn), driven by steady replacement cycles in a mature market.

Despite muted 2024 sentiment from trade and infrastructure uncertainty, the installed base yields high-margin parts and service—service margins near 30%—providing recurring cash flow.

That cash generation funds R&D and capex for digital telematics and electric crane pilots, with Manitowoc allocating ~ $75m to these initiatives in 2024.

National Crane Boom Trucks

National Crane boom trucks hold roughly a 40–50% share of the North American boom truck market (2024 industry estimates), in a mature segment with ~2% annual growth; margins run high—EBIT margins around 12–15% for Manitowoc’s mobile crane segment in FY2024—driven by manufacturing scale and repeat utility/construction orders.

Low promo spend and stable aftersales lift operating cash flow, letting Manitowoc reinvest minimal capex and channel excess cash to service corporate debt; here’s the quick math: steady unit volumes plus 12–15% EBIT convert to free cash flow that materially reduces leverage.

Potain Self-Erecting Cranes

The Potain self-erecting crane line dominates the mature European residential market with estimated 35–40% market share in 2024, delivering stable annual aftermarket & unit-margin cash flows; Manitowoc reported Crane segment margins ~9.8% in FY2024, and these units require low CAPEX—capex per unit ~€15–25k vs €200k+ for larger tower cranes.

Legacy Crane Care Support

Legacy Crane Care Support: Manitowoc’s established Crane Care maintains thousands of aging cranes globally, generating high-margin aftermarket revenue—service margins often exceed 30% and contributed roughly $180–200M in annual EBITDA-equivalent cash flow in 2024.

Because the service network and parts logistics already exist, growth costs are low, making it a classic cash cow that funds R&D for next-gen lifting tech, fueling about 25–30% of the company’s annual R&D spend.

- Thousands of cranes maintained worldwide

- Service margins ~30%+

- $180–200M cash flow (2024 est.)

- Funds ~25–30% of Manitowoc R&D

Shuttlelift Industrial Cranes

Shuttlelift carry-deck cranes dominate niche industrial and shipyard markets where Manitowoc holds above 60% market share and demand grows roughly 1–2% annually, making this a slow-growth, high-share segment.

These specialized cranes face limited competitors, have product lifecycles exceeding 15 years, and generate stable EBITDA margins near 18–22%, classifying them as classic cash cows.

Earnings fund higher-growth bets such as the mobile-crane electrification program, which targets a 2026 rollout and R&D spend of ~$45–55m over 2024–2026.

- High share: >60%

- Growth: 1–2% CAGR

- Lifecycle: >15 years

- EBITDA: ~18–22%

- Funding: $45–55m R&D to 2026

Manitowoc's mobile, Potain & Shuttlelift: $900M cash cows fueling 30% margins

Manitowoc’s North American mobile and Potain self-erecting lines plus Crane Care and Shuttlelift are cash cows: ~40% of 2024 sales (~$900m of $2.25bn), service margins ~30%, Crane segment EBIT ~9.8% (FY2024), Shuttlelift EBITDA ~18–22%, cash flow ~$180–200m (2024 est.) funding ~$75m capex and ~25–30% of R&D.

| Item | 2024 |

|---|---|

| Revenue share | ~40% ($900m) |

| Service margin | ~30% |

| Crane EBIT | ~9.8% |

| Shuttlelift EBITDA | 18–22% |

| Cash flow | $180–200m |

| R&D funded | 25–30% |

Delivered as Shown

Manitowoc BCG Matrix

The file you're previewing is the exact Manitowoc BCG Matrix report you'll receive after purchase—fully formatted, analysis-ready, and free of watermarks or demo content for immediate use in presentations or planning.

This preview mirrors the final deliverable: a professionally crafted BCG Matrix with market-informed positioning and clear visuals, sent directly to your inbox with no further edits required.

What you see here is the actual editable file available upon purchase—ready to download, print, or incorporate into client decks and internal strategy sessions.

You're viewing the genuine Manitowoc BCG Matrix document that becomes yours after a one-time purchase, designed by strategy experts for instant application in competitive and portfolio analysis.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

See the Bigger Picture

Manitowoc’s BCG Matrix preview highlights where key product lines—cranes, marine systems, and service offerings—sit across growth and market-share axes, signaling which are Stars, Cash Cows, Dogs, or Question Marks and what that means for capital allocation. This snapshot points to high-growth crane segments and mature service revenues needing different strategies. Dive deeper into this company’s BCG Matrix and gain a clear view of where its products stand—Stars, Cash Cows, Dogs, or Question Marks. Purchase the full version for a complete breakdown and strategic insights you can act on.

Stars

Aftermarket Services and CRANES+50

Aftermarket, central to CRANES+50, hit a record $690.5 million in non-new machine sales by end-2025, with parts, maintenance and field service up 10% year-over-year.

These recurring, higher-margin revenues moved Manitowoc toward a steadier cash profile; aftermarket contributed roughly 28% of 2025 service-segment revenue and improved gross margins by about 150 basis points.

Manitowoc is scaling global service footprints—adding 35 service centers in 2024–25 and boosting field-tech headcount 18%—to cement aftermarket as a stable cash generator.

Potain Tower Cranes in Europe

Potain tower cranes in Europe are a Star: the EU tower crane market grew for the fifth straight quarter in Q4 2025 with orders up ~9% YoY, and Potain holds about 28–32% market share, driven by €8–12bn public construction stimulus and rising urban prefabrication demand.

High order backlog—estimated at €1.1–1.4bn entering 2026—requires continued capex to fend off Liebherr and XCMG, but positions Potain as Manitowoc’s primary growth engine for 2026.

Mobile Hydraulic Cranes (Grove Brand)

Grove mobile hydraulic cranes are a Star in Manitowoc’s BCG matrix, leading the 51–150 ton segment which is over 33% of the global crane market (2025 IHS Markit).

Despite a soft North American macro, 2025 shipments rose 12% Y/Y and Q4 order book jumped 38%, signalling strong demand for versatile lifting solutions.

Ongoing R&D in All-Terrain and Rough-Terrain models (R&D spend ~2.8% of revenue in 2025) keeps Grove competitive as the global market recovers.

Direct-to-Customer Distribution (MGX)

Direct-to-Customer Distribution (MGX) is a high-growth move: MGX Equipment Services shifted Manitowoc toward rentals and direct sales, targeting higher lifecycle margins and growing U.S. Southeast share after acquiring Ring Power’s crane assets in Jan 2025, adding ~120 machines and boosting regional fleet by ~18%.

The unit consumes cash for fleet expansion and new branches—Manitowoc allocated $85m capex to MGX in FY2025 YTD—but offers higher returns via rental utilization rates (projected 62% vs 45% company average) and service revenue growth.

- Acquisition: Ring Power crane assets, Jan 2025, ~120 units

- Fleet boost: +18% Southeast presence

- FY2025 MGX capex: $85m YTD

- Projected utilization: 62% vs 45% company avg

High-Capacity Lattice Boom Crawlers

Manitowoc ranks top-three globally in crawler cranes, leading in high-capacity models (300+t) used for infrastructure and energy; these units drove 2024 revenue of about $1.1bn in the crane division, per company filings.

Segment for >300-ton crawlers is forecast at ~7.8% CAGR to 2026, powered by global wind and renewable projects requiring heavy lifts.

High engineering R&D and capital tooling sustain market position; unit ASPs often exceed $5M, keeping margins sensitive to commodity costs.

- Top-three market share in crawlers

- >300t segment CAGR ~7.8% to 2026

- 2024 crane revenue ~ $1.1bn

- Typical ASPs > $5M; high R&D capex

Aftermarket drives margins; Potain strong in EU—Grove shipments +12%, MGX rental rising

Aftermarket and Potain tower cranes are Stars: aftermarket hit $690.5M non-new sales in 2025 (~28% of service revenue), boosting gross margin +150bps; Potain holds ~30% EU share with €1.1–1.4bn backlog entering 2026. Grove mobile cranes led 51–150t with 12% shipment growth in 2025; MGX rental push got $85M capex YTD and projected 62% utilization.

| Metric | 2025 / Note |

|---|---|

| Aftermarket sales | $690.5M |

| Aftermarket share (service) | ~28% |

| Potain EU share | 28–32% |

| Potain backlog | €1.1–1.4B |

| Grove shipment growth | +12% Y/Y |

| MGX capex FY2025 YTD | $85M |

| MGX projected utilization | 62% |

What is included in the product

Comprehensive BCG review of Manitowoc’s units with strategic guidance on Stars, Cash Cows, Question Marks, and Dogs.

One-page Manitowoc BCG Matrix placing each segment in a quadrant for quick strategic decisions and executive review.

Cash Cows

North American Mobile Crane Fleet

The North American mobile crane fleet is Manitowoc’s largest revenue engine, accounting for about 40% of 2024 consolidated sales (roughly $900m of $2.25bn), driven by steady replacement cycles in a mature market.

Despite muted 2024 sentiment from trade and infrastructure uncertainty, the installed base yields high-margin parts and service—service margins near 30%—providing recurring cash flow.

That cash generation funds R&D and capex for digital telematics and electric crane pilots, with Manitowoc allocating ~ $75m to these initiatives in 2024.

National Crane Boom Trucks

National Crane boom trucks hold roughly a 40–50% share of the North American boom truck market (2024 industry estimates), in a mature segment with ~2% annual growth; margins run high—EBIT margins around 12–15% for Manitowoc’s mobile crane segment in FY2024—driven by manufacturing scale and repeat utility/construction orders.

Low promo spend and stable aftersales lift operating cash flow, letting Manitowoc reinvest minimal capex and channel excess cash to service corporate debt; here’s the quick math: steady unit volumes plus 12–15% EBIT convert to free cash flow that materially reduces leverage.

Potain Self-Erecting Cranes

The Potain self-erecting crane line dominates the mature European residential market with estimated 35–40% market share in 2024, delivering stable annual aftermarket & unit-margin cash flows; Manitowoc reported Crane segment margins ~9.8% in FY2024, and these units require low CAPEX—capex per unit ~€15–25k vs €200k+ for larger tower cranes.

Legacy Crane Care Support

Legacy Crane Care Support: Manitowoc’s established Crane Care maintains thousands of aging cranes globally, generating high-margin aftermarket revenue—service margins often exceed 30% and contributed roughly $180–200M in annual EBITDA-equivalent cash flow in 2024.

Because the service network and parts logistics already exist, growth costs are low, making it a classic cash cow that funds R&D for next-gen lifting tech, fueling about 25–30% of the company’s annual R&D spend.

- Thousands of cranes maintained worldwide

- Service margins ~30%+

- $180–200M cash flow (2024 est.)

- Funds ~25–30% of Manitowoc R&D

Shuttlelift Industrial Cranes

Shuttlelift carry-deck cranes dominate niche industrial and shipyard markets where Manitowoc holds above 60% market share and demand grows roughly 1–2% annually, making this a slow-growth, high-share segment.

These specialized cranes face limited competitors, have product lifecycles exceeding 15 years, and generate stable EBITDA margins near 18–22%, classifying them as classic cash cows.

Earnings fund higher-growth bets such as the mobile-crane electrification program, which targets a 2026 rollout and R&D spend of ~$45–55m over 2024–2026.

- High share: >60%

- Growth: 1–2% CAGR

- Lifecycle: >15 years

- EBITDA: ~18–22%

- Funding: $45–55m R&D to 2026

Manitowoc's mobile, Potain & Shuttlelift: $900M cash cows fueling 30% margins

Manitowoc’s North American mobile and Potain self-erecting lines plus Crane Care and Shuttlelift are cash cows: ~40% of 2024 sales (~$900m of $2.25bn), service margins ~30%, Crane segment EBIT ~9.8% (FY2024), Shuttlelift EBITDA ~18–22%, cash flow ~$180–200m (2024 est.) funding ~$75m capex and ~25–30% of R&D.

| Item | 2024 |

|---|---|

| Revenue share | ~40% ($900m) |

| Service margin | ~30% |

| Crane EBIT | ~9.8% |

| Shuttlelift EBITDA | 18–22% |

| Cash flow | $180–200m |

| R&D funded | 25–30% |

Delivered as Shown

Manitowoc BCG Matrix

The file you're previewing is the exact Manitowoc BCG Matrix report you'll receive after purchase—fully formatted, analysis-ready, and free of watermarks or demo content for immediate use in presentations or planning.

This preview mirrors the final deliverable: a professionally crafted BCG Matrix with market-informed positioning and clear visuals, sent directly to your inbox with no further edits required.

What you see here is the actual editable file available upon purchase—ready to download, print, or incorporate into client decks and internal strategy sessions.

You're viewing the genuine Manitowoc BCG Matrix document that becomes yours after a one-time purchase, designed by strategy experts for instant application in competitive and portfolio analysis.