Manitowoc Porter's Five Forces Analysis

From Overview to Strategy Blueprint

Manitowoc operates in a capital-intensive, cyclical market where supplier concentration, buyer bargaining power, and the threat of substitutes critically shape margins and growth prospects; our snapshot highlights key pressures but omits detailed force ratings and sector benchmarks.

This brief only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Manitowoc’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Specialized Component Providers

Manitowoc depends on a small group of specialized suppliers for high-performance engines, hydraulics, and transmissions, which gives those vendors strong price and lead-time leverage.

These components are safety-critical, so switching costs are high and supplier bargaining power rises, reflected in supplier-related input cost inflation of about 6–8% for heavy machinery in 2024.

By end-2025, electrified component adoption cut qualified vendors by roughly 30%, further concentrating supply and boosting supplier power in procurements.

Volatility in Raw Material Procurement

Steel is a key input for Manitowoc cranes; global HRC (hot‑rolled coil) prices swung 18% in 2024–2025, driven by tariffs and Chinese output cuts, squeezing margins when contracts lack pass‑through clauses.

Long‑term OEM contracts delay price recovery, so a $100/ton HRC rise can cut gross margin by ~120–160 bps on Manitowoc’s 2024 revenue base ($1.9B); suppliers gain leverage if geopolitical risk in Russia/Ukraine or China persists.

Technical Complexity and Switching Costs

Integration of proprietary software and telematics into Manitowoc cranes raises switching costs: replacing an electronics supplier often needs R&D runs of 6–18 months and lab certification costing $0.5–2.0M per product line, per internal industry benchmarks in 2024.

Impact of Global Logistics and Freight

Suppliers of bulky sub-assemblies wield bargaining power via control of local manufacturing hubs and logistics; in 2025 port congestion and modal limits raised landed costs by ~6–9% industry-wide, favoring suppliers near Manitowoc plants.

Fuel surcharges averaged $0.12–0.18 per ton-mile in 2025, so suppliers with integrated logistics or proximate sites capture margin and timing advantages; Manitowoc often concedes terms to keep global assembly lines on schedule.

- Port congestion +6–9% landed cost (2025)

- Fuel surcharge $0.12–0.18/ton-mile (2025)

- Proximity reduces lead time, raises supplier leverage

- Manitowoc accepts logistics terms to avoid line stoppages

Supplier Forward Integration Threats

Supplier forward integration is uncommon in heavy machinery, but some large wear-part makers began selling direct aftermarket services in 2024–25, pressuring OEMs like Manitowoc (MTW) by threatening higher input costs and cannibalized service margins.

If key suppliers of pins, bushings, hydraulics or wear liners bypass OEM channels, Manitowoc could lose service revenue that made up about 18% of Crane segment sales in 2023, while sourcing costs could rise 5–10% per supplier reports.

This risk is strongest where suppliers hold patents or exclusive alloys; their IP gives them leverage to sell directly to fleet owners and tilt bargaining power toward suppliers.

- 2024–25 trend: select wear-part firms offering direct aftermarket sales

- Impact: potential 5–10% input-cost increase; service revenue at 18% of Crane sales (2023)

- Key driver: supplier IP on high-wear components

Supplier squeeze, electrification cuts vendors 30%—input inflation & HRC swings dent margins

Manitowoc faces high supplier power from a few specialized engine, hydraulic and electrified-component vendors, raising switching costs and input inflation (6–8% in 2024). Electrification cut qualified vendors ~30% by end‑2025, concentrating supply; HRC swings of 18% (2024–25) and $100/ton HRC shock ≈120–160bps gross margin hit. Aftermarket direct sales risk could raise input costs 5–10%.

| Metric | 2024–25 |

|---|---|

| Input inflation | 6–8% |

| Qualified vendors (electrified) | -30% |

| HRC price swing | 18% |

| HRC $100/ton impact | 120–160bps GM |

| Aftermarket cost risk | +5–10% |

What is included in the product

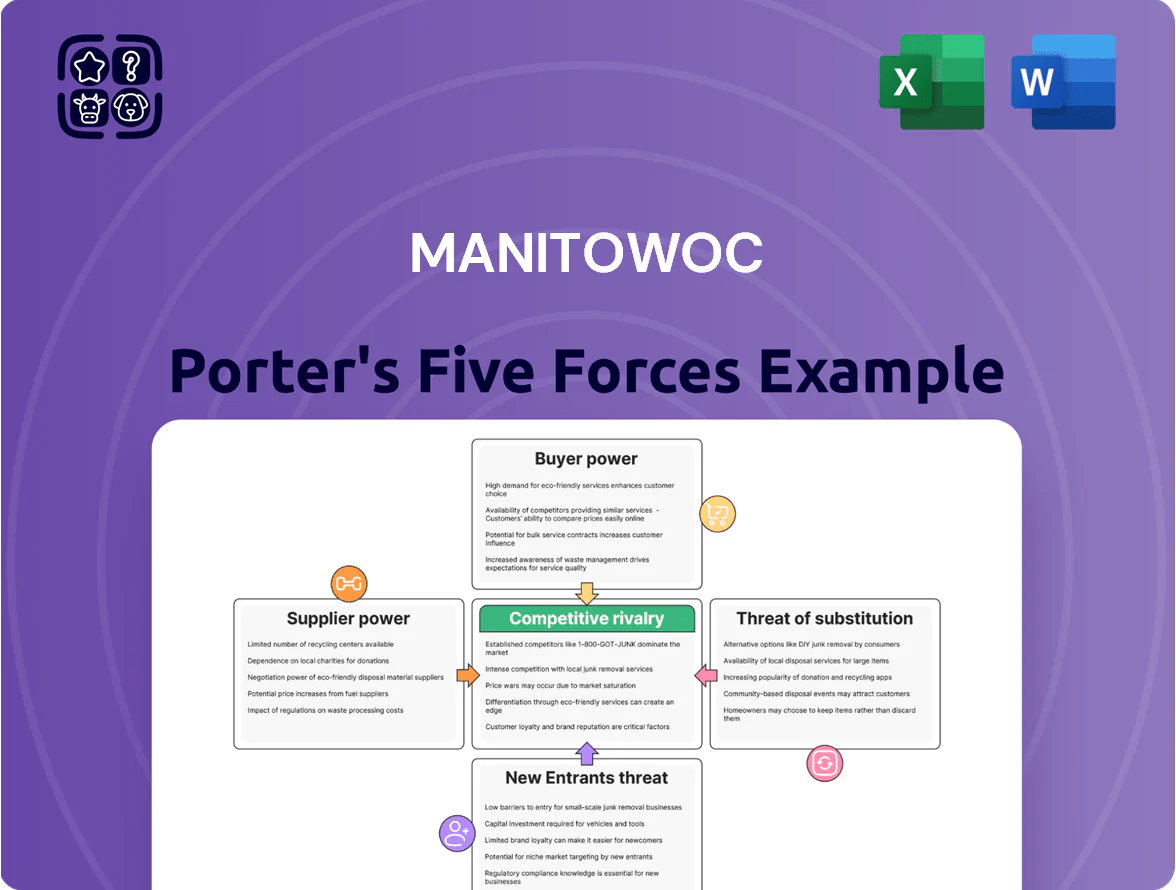

Examines competitive intensity, supplier and buyer power, threat of substitutes and new entrants specific to Manitowoc, highlighting pricing pressures, supplier dependencies, substitute technologies, and barriers that protect its market position.

A concise Porter’s Five Forces snapshot for Manitowoc—highlighting competitive threats, supplier/customer leverage, and substitution risks to speed strategic decisions.

Customers Bargaining Power

Consolidation of Major Equipment Rental Firms

By 2025, three rental giants account for roughly 40% of global crane rental spend, buying fleets in batches that push Manitowoc to grant volume discounts of 8–12% and bespoke service SLAs, squeezing reported gross margins by ~150–250 basis points versus 2020 levels.

Low Switching Costs Between Major Brands

For many standard lifting tasks, customers can switch among Manitowoc, Liebherr, and Tadano with minimal disruption, since mobile and tower cranes share core functionality and attachment compatibility; operator retraining typically takes days, not months.

This low switching cost pushed Manitowoc to match competitors on price and financing; in 2024 global crane OEM margins tightened—average gross margin fell to ~18%—forcing more aggressive TCO (total cost of ownership) offers.

High Sensitivity to Economic and Construction Cycles

Demand for cranes is highly cyclical and tied to infrastructure spending, energy projects, and commercial real estate; global crane sales fell about 12% in 2023 after reduced U.S. infrastructure starts, and industry forecasts in late 2025 point to muted orders as capex slows. During high interest rates and economic cooling in late 2025, buyers become very price-sensitive and often delay fleet renewals, cutting order volumes by double digits in some segments. This shift gives customers bargaining power to push for price concessions, longer payment terms, and extended warranties. Manufacturers like Manitowoc face pressure to protect factory utilization, so they accept weaker pricing or add-ons to keep plants running.

Information Symmetry and Digital Transparency

- Telematics + market data = better price & service comparisons

- Used-crane price index +18% (Ritchie Bros. 2024)

- TCO models spotlight maintenance, uptime, residual value

Demand for Comprehensive Aftermarket Support

Customers now demand equipment with guaranteed uptime and service-level agreements, shifting purchase decisions toward solution-based deals; 2025 market data shows aftermarket services grew 7.8% YoY and represent ~18% of global crane OEM revenue, concentrating leverage with buyers.

This trend lets buyers set long-term support terms and transfer maintenance risk to manufacturers, pressuring Manitowoc to offer uptime guarantees and predictive maintenance or lose share to rivals offering aggressive SLA bundles.

- Aftermarket = ~18% OEM revenue (2025)

- Service market +7.8% YoY (2025)

- Uptime SLAs raise switching risk

- Predictive maintenance critical to retain customers

Renters’ 40% Clout Squeezes OEMs—Margins Slashed, Used Prices Up 18%

Buyers hold strong leverage: three renters ~40% market share (2025), forcing 8–12% volume discounts and SLAs that shave 150–250 bps off gross margin; OEM gross margins fell to ~18% in 2024. Low switching costs and TCO models—plus used-crane prices +18% (Ritchie Bros. 2024)—empower negotiations; aftermarket (18% of OEM revenue, +7.8% YoY in 2025) shifts leverage to buyers.

| Metric | Value |

|---|---|

| Top renters share | ~40% (2025) |

| Volume discounts | 8–12% |

| Gross margin OEMs | ~18% (2024) |

| Used price change | +18% (Ritchie Bros. 2024) |

| Aftermarket share | ~18% revenue, +7.8% YoY (2025) |

Same Document Delivered

Manitowoc Porter's Five Forces Analysis

This preview shows the exact Manitowoc Porter’s Five Forces analysis you’ll receive after purchase—fully formatted, professionally written, and ready for immediate download and use with no placeholders or mockups.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

Manitowoc operates in a capital-intensive, cyclical market where supplier concentration, buyer bargaining power, and the threat of substitutes critically shape margins and growth prospects; our snapshot highlights key pressures but omits detailed force ratings and sector benchmarks.

This brief only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Manitowoc’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Specialized Component Providers

Manitowoc depends on a small group of specialized suppliers for high-performance engines, hydraulics, and transmissions, which gives those vendors strong price and lead-time leverage.

These components are safety-critical, so switching costs are high and supplier bargaining power rises, reflected in supplier-related input cost inflation of about 6–8% for heavy machinery in 2024.

By end-2025, electrified component adoption cut qualified vendors by roughly 30%, further concentrating supply and boosting supplier power in procurements.

Volatility in Raw Material Procurement

Steel is a key input for Manitowoc cranes; global HRC (hot‑rolled coil) prices swung 18% in 2024–2025, driven by tariffs and Chinese output cuts, squeezing margins when contracts lack pass‑through clauses.

Long‑term OEM contracts delay price recovery, so a $100/ton HRC rise can cut gross margin by ~120–160 bps on Manitowoc’s 2024 revenue base ($1.9B); suppliers gain leverage if geopolitical risk in Russia/Ukraine or China persists.

Technical Complexity and Switching Costs

Integration of proprietary software and telematics into Manitowoc cranes raises switching costs: replacing an electronics supplier often needs R&D runs of 6–18 months and lab certification costing $0.5–2.0M per product line, per internal industry benchmarks in 2024.

Impact of Global Logistics and Freight

Suppliers of bulky sub-assemblies wield bargaining power via control of local manufacturing hubs and logistics; in 2025 port congestion and modal limits raised landed costs by ~6–9% industry-wide, favoring suppliers near Manitowoc plants.

Fuel surcharges averaged $0.12–0.18 per ton-mile in 2025, so suppliers with integrated logistics or proximate sites capture margin and timing advantages; Manitowoc often concedes terms to keep global assembly lines on schedule.

- Port congestion +6–9% landed cost (2025)

- Fuel surcharge $0.12–0.18/ton-mile (2025)

- Proximity reduces lead time, raises supplier leverage

- Manitowoc accepts logistics terms to avoid line stoppages

Supplier Forward Integration Threats

Supplier forward integration is uncommon in heavy machinery, but some large wear-part makers began selling direct aftermarket services in 2024–25, pressuring OEMs like Manitowoc (MTW) by threatening higher input costs and cannibalized service margins.

If key suppliers of pins, bushings, hydraulics or wear liners bypass OEM channels, Manitowoc could lose service revenue that made up about 18% of Crane segment sales in 2023, while sourcing costs could rise 5–10% per supplier reports.

This risk is strongest where suppliers hold patents or exclusive alloys; their IP gives them leverage to sell directly to fleet owners and tilt bargaining power toward suppliers.

- 2024–25 trend: select wear-part firms offering direct aftermarket sales

- Impact: potential 5–10% input-cost increase; service revenue at 18% of Crane sales (2023)

- Key driver: supplier IP on high-wear components

Supplier squeeze, electrification cuts vendors 30%—input inflation & HRC swings dent margins

Manitowoc faces high supplier power from a few specialized engine, hydraulic and electrified-component vendors, raising switching costs and input inflation (6–8% in 2024). Electrification cut qualified vendors ~30% by end‑2025, concentrating supply; HRC swings of 18% (2024–25) and $100/ton HRC shock ≈120–160bps gross margin hit. Aftermarket direct sales risk could raise input costs 5–10%.

| Metric | 2024–25 |

|---|---|

| Input inflation | 6–8% |

| Qualified vendors (electrified) | -30% |

| HRC price swing | 18% |

| HRC $100/ton impact | 120–160bps GM |

| Aftermarket cost risk | +5–10% |

What is included in the product

Examines competitive intensity, supplier and buyer power, threat of substitutes and new entrants specific to Manitowoc, highlighting pricing pressures, supplier dependencies, substitute technologies, and barriers that protect its market position.

A concise Porter’s Five Forces snapshot for Manitowoc—highlighting competitive threats, supplier/customer leverage, and substitution risks to speed strategic decisions.

Customers Bargaining Power

Consolidation of Major Equipment Rental Firms

By 2025, three rental giants account for roughly 40% of global crane rental spend, buying fleets in batches that push Manitowoc to grant volume discounts of 8–12% and bespoke service SLAs, squeezing reported gross margins by ~150–250 basis points versus 2020 levels.

Low Switching Costs Between Major Brands

For many standard lifting tasks, customers can switch among Manitowoc, Liebherr, and Tadano with minimal disruption, since mobile and tower cranes share core functionality and attachment compatibility; operator retraining typically takes days, not months.

This low switching cost pushed Manitowoc to match competitors on price and financing; in 2024 global crane OEM margins tightened—average gross margin fell to ~18%—forcing more aggressive TCO (total cost of ownership) offers.

High Sensitivity to Economic and Construction Cycles

Demand for cranes is highly cyclical and tied to infrastructure spending, energy projects, and commercial real estate; global crane sales fell about 12% in 2023 after reduced U.S. infrastructure starts, and industry forecasts in late 2025 point to muted orders as capex slows. During high interest rates and economic cooling in late 2025, buyers become very price-sensitive and often delay fleet renewals, cutting order volumes by double digits in some segments. This shift gives customers bargaining power to push for price concessions, longer payment terms, and extended warranties. Manufacturers like Manitowoc face pressure to protect factory utilization, so they accept weaker pricing or add-ons to keep plants running.

Information Symmetry and Digital Transparency

- Telematics + market data = better price & service comparisons

- Used-crane price index +18% (Ritchie Bros. 2024)

- TCO models spotlight maintenance, uptime, residual value

Demand for Comprehensive Aftermarket Support

Customers now demand equipment with guaranteed uptime and service-level agreements, shifting purchase decisions toward solution-based deals; 2025 market data shows aftermarket services grew 7.8% YoY and represent ~18% of global crane OEM revenue, concentrating leverage with buyers.

This trend lets buyers set long-term support terms and transfer maintenance risk to manufacturers, pressuring Manitowoc to offer uptime guarantees and predictive maintenance or lose share to rivals offering aggressive SLA bundles.

- Aftermarket = ~18% OEM revenue (2025)

- Service market +7.8% YoY (2025)

- Uptime SLAs raise switching risk

- Predictive maintenance critical to retain customers

Renters’ 40% Clout Squeezes OEMs—Margins Slashed, Used Prices Up 18%

Buyers hold strong leverage: three renters ~40% market share (2025), forcing 8–12% volume discounts and SLAs that shave 150–250 bps off gross margin; OEM gross margins fell to ~18% in 2024. Low switching costs and TCO models—plus used-crane prices +18% (Ritchie Bros. 2024)—empower negotiations; aftermarket (18% of OEM revenue, +7.8% YoY in 2025) shifts leverage to buyers.

| Metric | Value |

|---|---|

| Top renters share | ~40% (2025) |

| Volume discounts | 8–12% |

| Gross margin OEMs | ~18% (2024) |

| Used price change | +18% (Ritchie Bros. 2024) |

| Aftermarket share | ~18% revenue, +7.8% YoY (2025) |

Same Document Delivered

Manitowoc Porter's Five Forces Analysis

This preview shows the exact Manitowoc Porter’s Five Forces analysis you’ll receive after purchase—fully formatted, professionally written, and ready for immediate download and use with no placeholders or mockups.