Manpower PESTLE Analysis

Skip the Research. Get the Strategy.

Discover how political shifts, economic cycles, and tech disruption are reshaping Manpower’s competitive landscape—our concise PESTLE highlights the risks and opportunities driving strategic choices. Ready-made for investors and strategists, the full report delivers granular insights and actionable recommendations. Purchase the complete PESTLE now to access the data-backed analysis you need to outmaneuver rivals.

Political factors

Geopolitical instability and trade policies

Ongoing regional conflicts and shifting trade alliances as of late 2025 disrupted supply chains and reduced labor mobility, with UNCTAD reporting global trade growth down to 0.7% in 2024–25 and cross-border talent flows falling 12% year-over-year; ManpowerGroup faces higher redeployment costs and placement delays. Political shifts in major economies prompted stricter visa regimes—OECD data shows work permit approvals declined 9% in 2024—affecting ManpowerGroup’s ability to move talent and maintain operations in volatile regions.

Government labor market interventions

Governments are boosting labor interventions: 2024 OECD data shows over 60% of member states use hiring subsidies or wage top-ups, pushing firms toward temporary staffing—beneficial for ManpowerGroup, which reported 2024 global staffing revenue of $21.0bn, with flexible work demand up 8% YoY.

Changes in taxation and corporate policy

Public sector infrastructure and job creation

Large-scale government spending—USD 1.2 trillion global infrastructure pipeline and US Inflation Reduction Act investments exceeding USD 391 billion through 2024—drives strong demand for construction and engineering staffing, benefiting ManpowerGroup’s Experis and Manpower brands.

Public commitments to green energy and infrastructure translate into multi-year hiring for skilled trades and engineers, while digital transformation initiatives (e.g., EU digital decade targets, US federal IT modernization budgets >USD 30 billion in 2024) expand IT staffing and consulting opportunities.

- USD 1.2T global infrastructure pipeline

- USD 391B IRA investments through 2024

- US federal IT modernization >USD 30B (2024)

- ManpowerGroup positioned in construction, engineering, IT staffing

Regulatory focus on the gig economy

- 30+ US states with gig-related bills in 2025

- Projected 5–8% payroll cost increase if benefits mandated

- Estimated 10–15% rise in lobbying/compliance spend vs 2024

Global trade drag and policy shifts boost temp staffing as payroll costs rise

Regional conflicts, trade slowdowns (UNCTAD trade growth 0.7% 2024–25) and stricter visas (OECD work permits −9% 2024) raise redeployment costs; govts favor hiring subsidies (>60% OECD) boosting temp staffing demand—ManpowerGroup 2024 staffing revenue $21.0bn. BEPS 2.0 (15%) and gig-worker laws (30+ US states 2025) could add 5–8% payroll costs; infrastructure/IRA/IT budgets (USD 1.2T/391B/30B) drive demand.

| Metric | Value |

|---|---|

| Staffing revenue 2024 | $21.0bn |

| Trade growth 2024–25 | 0.7% |

| Work permits 2024 | −9% |

| BEPS 2.0 rate | 15% |

| IRA thru 2024 | $391B |

What is included in the product

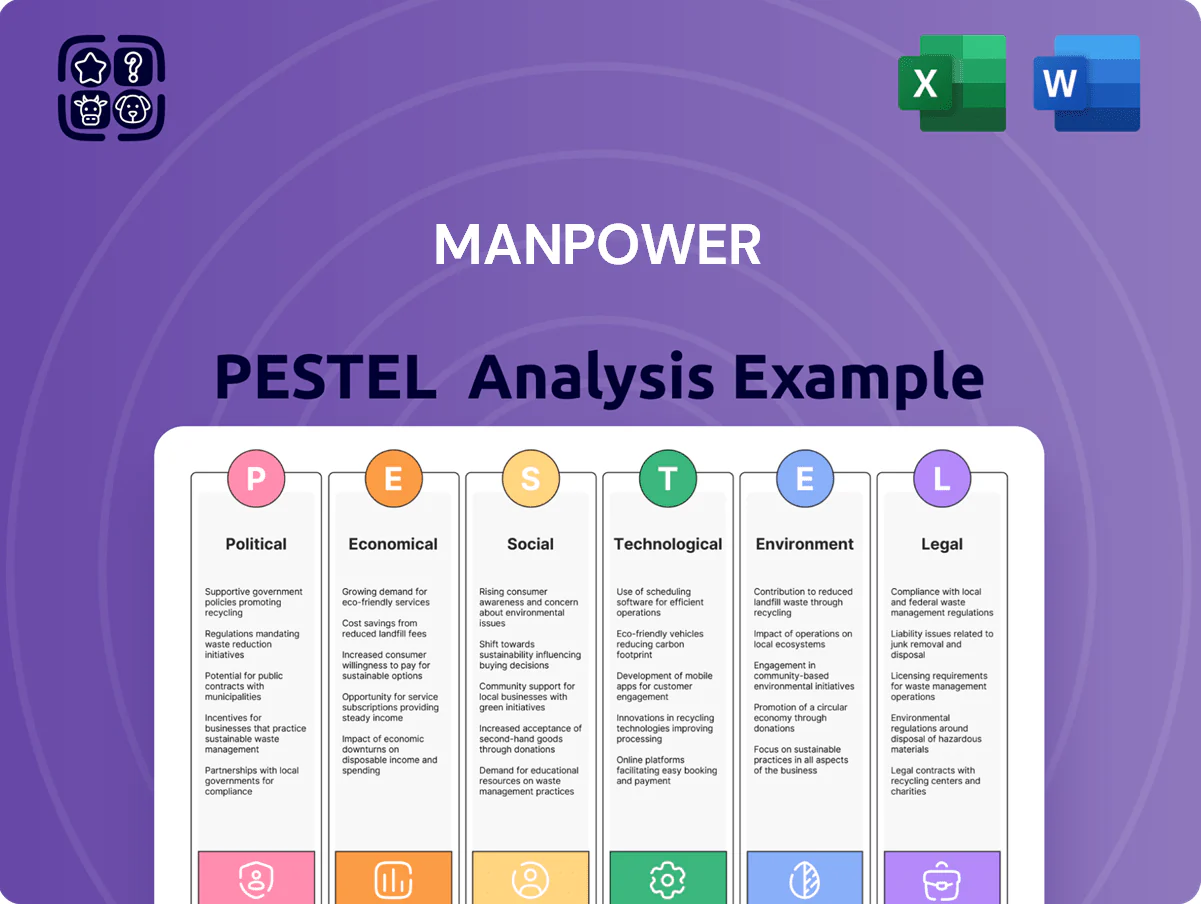

Explores how external macro-environmental factors uniquely affect Manpower across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify threats and opportunities for executives, consultants, and entrepreneurs.

A concise Manpower PESTLE summary that distills regulatory, economic, social, technological, environmental and legal drivers into an easily shareable slide-ready format to streamline planning and stakeholder alignment.

Economic factors

Global inflationary pressures and wage growth

Persistent inflation through 2025—global CPI averaging about 4.5% in 2024–25 vs pre‑pandemic ~2%—has driven nominal wage increases of roughly 5–7% in key markets, complicating ManpowerGroup’s recruitment pricing models.

Manpower must balance rising internal labor costs (2024 SG&A wage pressure up ~6%) with client fee sensitivity as clients face margin compression from higher input costs.

High wage volatility has led to more frequent contract renegotiations and a need for granular market pricing data; Manpower’s pricing teams report renegotiation cycles shortening to 6–9 months in volatile regions.

Currency exchange rate fluctuations

As a global staffing firm in 70+ countries, ManpowerGroup reported 2024 revenue of $20.9B, making USD/EUR moves material; a 10% USD strengthening vs EUR could swing reported operating income by hundreds of millions due to translation effects.

In 2024 ManpowerGroup recorded FX losses of $145M; therefore hedging and natural hedges are essential to stabilize cash flows and investor expectations across its multinational operations.

Interest rate cycles and corporate CAPEX

As of late 2025, global policy rates remain elevated—US Fed funds ~5.25–5.50% and ECB depo ~3.75%—pressuring corporate CAPEX and prompting clients to curb permanent hires; ManpowerGroup sees higher demand for temporary staffing, with US temp placements up ~6% YoY in H1 2025. If rates ease, firms historically increase CAPEX and professional recruitment needs rise, boosting Manpower’s high-end placement revenue share.

Cyclical nature of the staffing industry

The demand for ManpowerGroup's services tracks global GDP and industrial production; IMF projected 2025 global GDP growth at ~3.0% in 2024–25, and Manpower reported revenue sensitivity with Q3 2024 temporary staffing volumes down ~4% y/y in softer markets.

Economic slowdowns compress placement volumes, while recoveries unlock rapid growth in just-in-time staffing—Manpower saw 2H 2023–2024 upticks in North America temp hours returning to pre‑pandemic levels.

Diversification across sectors (IT, healthcare, manufacturing) reduced region-specific downside: in 2024 non-industrial segments contributed >60% of gross margin, mitigating cyclical risk.

- Revenue correlated with GDP cycles; temp volumes fell ~4% y/y in Q3 2024

- Recovery phases drive faster growth in just-in-time staffing

- Non-industrial segments >60% of gross margin in 2024, aiding diversification

Emergence of high-growth developing markets

Economic expansion in Southeast Asia and parts of Latin America — GDP growth of 4.5–5.5% in ASEAN (2024 IMF) and ~3.0–4.0% in major Latin American economies — opens new revenue streams as mature markets plateau.

ManpowerGroup needs targeted investment to capture share as local firms professionalize HR; staffing demand in APAC rose ~6% YoY in 2024 (Manpower internal regional reports).

These regions carry higher volatility, currency risk, and varied consumer purchasing power, with unemployment rates ranging from 3% to 10% across key markets.

- GDP growth: ASEAN ~4.5–5.5% (2024 IMF)

- Latin America growth: ~3–4% (2024)

- APAC staffing demand: ~6% YoY (2024 Manpower data)

- Unemployment variance: 3–10% across markets

- Risks: currency volatility, differing purchasing power

Manpower: $20.9B revenue, inflation fuels temp staffing surge; FX bites $145M

Inflation-driven wage growth (~5–7% 2024–25) and elevated rates (Fed ~5.25–5.50% 2025) shift demand toward temp staffing (US temp +6% H1 2025); FX weakness cost Manpower $145M in 2024; global revenue $20.9B (2024); ASEAN GDP ~4.5–5.5% (2024), LatAm ~3–4% (2024), APAC staffing +6% YoY (2024).

| Metric | Value |

|---|---|

| Revenue 2024 | $20.9B |

| FX loss 2024 | $145M |

| Wage growth | 5–7% |

| US temp H1 2025 | +6% YoY |

Preview the Actual Deliverable

Manpower PESTLE Analysis

The preview shown here is the exact Manpower PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use; no placeholders or teasers. The content, layout, and insights visible in this preview match the downloadable file you’ll get immediately after checkout. Use it for strategic planning, market assessment, and stakeholder presentations without further edits.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Skip the Research. Get the Strategy.

Discover how political shifts, economic cycles, and tech disruption are reshaping Manpower’s competitive landscape—our concise PESTLE highlights the risks and opportunities driving strategic choices. Ready-made for investors and strategists, the full report delivers granular insights and actionable recommendations. Purchase the complete PESTLE now to access the data-backed analysis you need to outmaneuver rivals.

Political factors

Geopolitical instability and trade policies

Ongoing regional conflicts and shifting trade alliances as of late 2025 disrupted supply chains and reduced labor mobility, with UNCTAD reporting global trade growth down to 0.7% in 2024–25 and cross-border talent flows falling 12% year-over-year; ManpowerGroup faces higher redeployment costs and placement delays. Political shifts in major economies prompted stricter visa regimes—OECD data shows work permit approvals declined 9% in 2024—affecting ManpowerGroup’s ability to move talent and maintain operations in volatile regions.

Government labor market interventions

Governments are boosting labor interventions: 2024 OECD data shows over 60% of member states use hiring subsidies or wage top-ups, pushing firms toward temporary staffing—beneficial for ManpowerGroup, which reported 2024 global staffing revenue of $21.0bn, with flexible work demand up 8% YoY.

Changes in taxation and corporate policy

Public sector infrastructure and job creation

Large-scale government spending—USD 1.2 trillion global infrastructure pipeline and US Inflation Reduction Act investments exceeding USD 391 billion through 2024—drives strong demand for construction and engineering staffing, benefiting ManpowerGroup’s Experis and Manpower brands.

Public commitments to green energy and infrastructure translate into multi-year hiring for skilled trades and engineers, while digital transformation initiatives (e.g., EU digital decade targets, US federal IT modernization budgets >USD 30 billion in 2024) expand IT staffing and consulting opportunities.

- USD 1.2T global infrastructure pipeline

- USD 391B IRA investments through 2024

- US federal IT modernization >USD 30B (2024)

- ManpowerGroup positioned in construction, engineering, IT staffing

Regulatory focus on the gig economy

- 30+ US states with gig-related bills in 2025

- Projected 5–8% payroll cost increase if benefits mandated

- Estimated 10–15% rise in lobbying/compliance spend vs 2024

Global trade drag and policy shifts boost temp staffing as payroll costs rise

Regional conflicts, trade slowdowns (UNCTAD trade growth 0.7% 2024–25) and stricter visas (OECD work permits −9% 2024) raise redeployment costs; govts favor hiring subsidies (>60% OECD) boosting temp staffing demand—ManpowerGroup 2024 staffing revenue $21.0bn. BEPS 2.0 (15%) and gig-worker laws (30+ US states 2025) could add 5–8% payroll costs; infrastructure/IRA/IT budgets (USD 1.2T/391B/30B) drive demand.

| Metric | Value |

|---|---|

| Staffing revenue 2024 | $21.0bn |

| Trade growth 2024–25 | 0.7% |

| Work permits 2024 | −9% |

| BEPS 2.0 rate | 15% |

| IRA thru 2024 | $391B |

What is included in the product

Explores how external macro-environmental factors uniquely affect Manpower across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify threats and opportunities for executives, consultants, and entrepreneurs.

A concise Manpower PESTLE summary that distills regulatory, economic, social, technological, environmental and legal drivers into an easily shareable slide-ready format to streamline planning and stakeholder alignment.

Economic factors

Global inflationary pressures and wage growth

Persistent inflation through 2025—global CPI averaging about 4.5% in 2024–25 vs pre‑pandemic ~2%—has driven nominal wage increases of roughly 5–7% in key markets, complicating ManpowerGroup’s recruitment pricing models.

Manpower must balance rising internal labor costs (2024 SG&A wage pressure up ~6%) with client fee sensitivity as clients face margin compression from higher input costs.

High wage volatility has led to more frequent contract renegotiations and a need for granular market pricing data; Manpower’s pricing teams report renegotiation cycles shortening to 6–9 months in volatile regions.

Currency exchange rate fluctuations

As a global staffing firm in 70+ countries, ManpowerGroup reported 2024 revenue of $20.9B, making USD/EUR moves material; a 10% USD strengthening vs EUR could swing reported operating income by hundreds of millions due to translation effects.

In 2024 ManpowerGroup recorded FX losses of $145M; therefore hedging and natural hedges are essential to stabilize cash flows and investor expectations across its multinational operations.

Interest rate cycles and corporate CAPEX

As of late 2025, global policy rates remain elevated—US Fed funds ~5.25–5.50% and ECB depo ~3.75%—pressuring corporate CAPEX and prompting clients to curb permanent hires; ManpowerGroup sees higher demand for temporary staffing, with US temp placements up ~6% YoY in H1 2025. If rates ease, firms historically increase CAPEX and professional recruitment needs rise, boosting Manpower’s high-end placement revenue share.

Cyclical nature of the staffing industry

The demand for ManpowerGroup's services tracks global GDP and industrial production; IMF projected 2025 global GDP growth at ~3.0% in 2024–25, and Manpower reported revenue sensitivity with Q3 2024 temporary staffing volumes down ~4% y/y in softer markets.

Economic slowdowns compress placement volumes, while recoveries unlock rapid growth in just-in-time staffing—Manpower saw 2H 2023–2024 upticks in North America temp hours returning to pre‑pandemic levels.

Diversification across sectors (IT, healthcare, manufacturing) reduced region-specific downside: in 2024 non-industrial segments contributed >60% of gross margin, mitigating cyclical risk.

- Revenue correlated with GDP cycles; temp volumes fell ~4% y/y in Q3 2024

- Recovery phases drive faster growth in just-in-time staffing

- Non-industrial segments >60% of gross margin in 2024, aiding diversification

Emergence of high-growth developing markets

Economic expansion in Southeast Asia and parts of Latin America — GDP growth of 4.5–5.5% in ASEAN (2024 IMF) and ~3.0–4.0% in major Latin American economies — opens new revenue streams as mature markets plateau.

ManpowerGroup needs targeted investment to capture share as local firms professionalize HR; staffing demand in APAC rose ~6% YoY in 2024 (Manpower internal regional reports).

These regions carry higher volatility, currency risk, and varied consumer purchasing power, with unemployment rates ranging from 3% to 10% across key markets.

- GDP growth: ASEAN ~4.5–5.5% (2024 IMF)

- Latin America growth: ~3–4% (2024)

- APAC staffing demand: ~6% YoY (2024 Manpower data)

- Unemployment variance: 3–10% across markets

- Risks: currency volatility, differing purchasing power

Manpower: $20.9B revenue, inflation fuels temp staffing surge; FX bites $145M

Inflation-driven wage growth (~5–7% 2024–25) and elevated rates (Fed ~5.25–5.50% 2025) shift demand toward temp staffing (US temp +6% H1 2025); FX weakness cost Manpower $145M in 2024; global revenue $20.9B (2024); ASEAN GDP ~4.5–5.5% (2024), LatAm ~3–4% (2024), APAC staffing +6% YoY (2024).

| Metric | Value |

|---|---|

| Revenue 2024 | $20.9B |

| FX loss 2024 | $145M |

| Wage growth | 5–7% |

| US temp H1 2025 | +6% YoY |

Preview the Actual Deliverable

Manpower PESTLE Analysis

The preview shown here is the exact Manpower PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use; no placeholders or teasers. The content, layout, and insights visible in this preview match the downloadable file you’ll get immediately after checkout. Use it for strategic planning, market assessment, and stakeholder presentations without further edits.