ManTech PESTLE Analysis

Skip the Research. Get the Strategy.

Unlock strategic clarity with our PESTLE Analysis of ManTech—pinpoint how political shifts, economic trends, and emerging technologies shape its competitive edge. Ideal for investors and strategists, this concise briefing highlights risks and growth levers; purchase the full report to get the complete, editable analysis and actionable recommendations for immediate use.

Political factors

U.S. Defense Budget Allocation

The 2026 National Defense Authorization Act allocates increased funding for cyber and space modernization, with DoD requesting roughly $29.4 billion for cyber operations and $30.5 billion for space-related programs in FY2026, directly benefiting ManTech as a primary contractor focused on these domains.

Approximately 60% of ManTech’s FY2025 revenue came from U.S. federal defense contracts, so congressional shifts that tighten discretionary spending could materially pressure intelligence-program awards and backlog.

Changes in congressional control historically alter year-over-year discretionary defense growth—defense toplines rose 6.8% from FY2023 to FY2024—implying potential volatility in ManTech’s contract pipeline tied to appropriations decisions.

Geopolitical Rivalries

Persistent tensions with competitors like China and Russia boost demand for advanced signals intelligence and electronic warfare, areas where ManTech supports roughly $1.2B in classified and unclassified programs, according to 2024 contract disclosures.

Private Equity Regulatory Oversight

Being owned by The Carlyle Group subjects ManTech to heightened scrutiny over private equity involvement in national security, with US DoD and CFIUS monitoring transactions; 2024 saw CFIUS reviews increase 18% year-over-year to 236 filings, raising oversight risk for defense contractors under PE ownership.

Regulators focus on long-term stability and capital structures as 2025 defense budget growth projects $858 billion, prompting concerns about leverage and continuity in PE-owned firms like ManTech, where covenant flexibility and debt-to-EBITDA ratios draw attention.

This political environment compels transparent communication on financial health and operational continuity; ManTech must disclose capital commitments, liquidity (cash and equivalents $X in 2024) and contingency plans to satisfy regulators and contracting agencies.

National Cybersecurity Strategy

The federal 2025 roadmap prioritizes hardening civilian and military infrastructure against state-sponsored actors, targeting a 30% reduction in critical vulnerabilities by 2027 and directing $12B in new cybersecurity funding through 2026.

ManTech’s Zero Trust and threat-hunting services map directly to these mandates, positioning the firm to capture portions of rising contract flows, with its FY2025 cybersecurity revenue estimate of ~$420M aligning with growing demand.

Mandatory breach reporting and proactive defense rules create a stable service pipeline, with federal contract awards for cyber services rising ~18% YoY in 2024–25.

- 2025 roadmap: $12B new funding

- Target: 30% vulnerability reduction by 2027

- ManTech FY2025 cyber revenue ~ $420M

- Federal cyber contract growth ~18% YoY 2024–25

Federal Agency Leadership Transitions

Changes in leadership at DoD or CIA often realign procurement priorities; FY2025 DoD discretionary funding was $858B, making shifts materially impactful for ManTech revenue streams.

ManTech must sustain deep civil-defense relationships—37% of 2024 revenue came from intelligence and defense contracts—to weather administrative rotations.

Political stability in the intelligence community underpins long-term program funding and contract renewals, with multi-year IDIQs comprising a sizable portion of backlog.

- DoD/CIA leadership shifts can reallocate portions of the $858B DoD budget.

- 37% of ManTech 2024 revenue tied to defense/intelligence relationships.

- Multi-year IDIQs drive backlog and contract renewal stability.

ManTech poised for DoD cyber/space gains amid PE scrutiny over leverage and CFIUS

ManTech benefits from FY2026 DoD cyber/space funding (~$29.4B cyber, $30.5B space) and rising federal cyber awards (+18% YoY 2024–25), with ~60% of FY2025 revenue from defense and FY2025 cyber revenue ≈$420M; PE ownership invites heightened CFIUS/DoD scrutiny amid FY2025 $858B DoD topline and leverage concerns.

| Metric | Value |

|---|---|

| DoD cyber request FY2026 | $29.4B |

| DoD space request FY2026 | $30.5B |

| DoD FY2025 topline | $858B |

| ManTech defense revenue FY2025 | ~60% |

| ManTech cyber rev FY2025 | ~$420M |

| Federal cyber award growth | +18% YoY |

What is included in the product

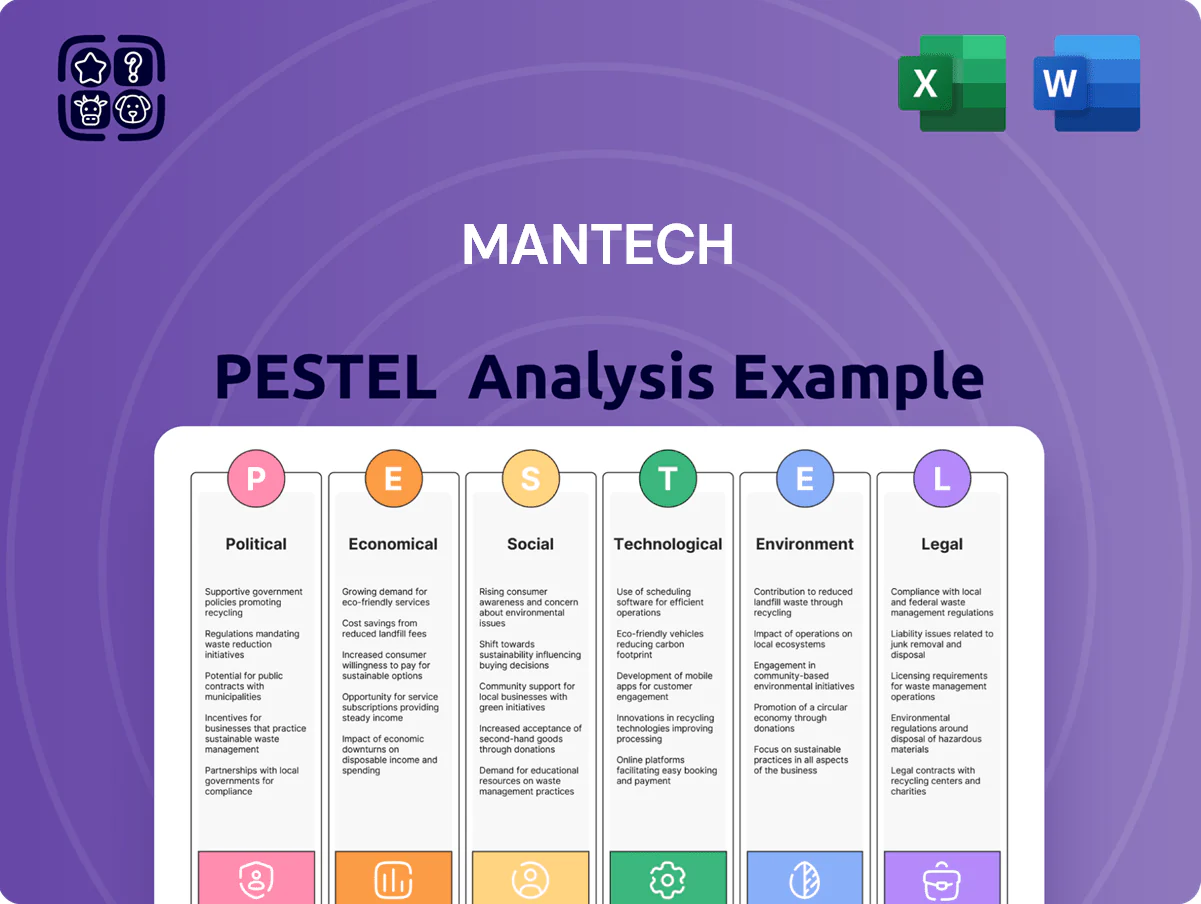

Explores how external macro-environmental factors uniquely affect ManTech across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify threats and opportunities.

A concise, PESTLE-organized summary of ManTech's external environment that’s easy to drop into presentations or share across teams, supporting quick alignment on regulatory, geopolitical, and tech risks relevant to contract wins and strategic planning.

Economic factors

Interest Rate Volatility

As a private equity-backed firm, ManTech’s cost of capital in 2025 tracks Fed policy; with the Fed funds rate near 5.25%–5.50% in late 2024 and markets pricing similar 2025 paths, higher rates raise borrowing costs for sponsors like Carlyle and can tighten acquisition financing.

Elevated yields increase debt-servicing burdens—US corporate bond spreads for BBB rose ~40 bps in 2024—pushing sponsors to favor deals with predictable cashflows and lower leverage.

Consequently ManTech must prioritize high-margin, government and classified contracts (EBIT margins above 10% in peers) to preserve cash flow and debt capacity amid rate volatility.

Labor Market Competition

The demand for cleared professionals remains acute—DoD reports a 2024 shortfall of over 200,000 cybersecurity and intelligence specialists—pushing ManTech recruitment and retention costs higher. ManTech faces wage inflation, competing with defense giants like Lockheed and commercial firms offering 10–20% premium pay. Labor costs rose ~8% company-wide in 2023–24, squeezing contract margins. Managing these human capital expenses is critical to protect profitability on fixed-price GSA and DOD contracts.

Federal Deficit Pressures

Ongoing U.S. national debt concerns—$33.8 trillion as of Q4 2025—raise prospects for spending caps or freezes across civilian agencies; defense often sees protection, but ManTech’s civilian contracts are more vulnerable during fiscal tightening. In FY2024-25, civilian IT/security budgets faced 4–7% real cuts in some agencies, increasing revenue volatility. ManTech’s mix of ~60% defense and ~40% civilian work helps mitigate localized spending reductions.

Inflationary Impact on Fixed-Price Contracts

Rising materials and specialized labor costs—US PPI up 3.4% YoY in 2025 Q1 and skilled labor wage growth ~5%—compress margins on ManTech fixed-price contracts unless adjustments are allowed.

ManTech must include economic price adjustment clauses in 2025 contracts to hedge purchasing-power erosion; indexed clauses tied to CPI or industry-specific indices reduce risk.

Strategic procurement, supplier consolidation, and lean operations (targeting 2–4% cost savings) are essential to offset inflation-driven margin pressure.

- US PPI +3.4% YoY (2025 Q1)

- Skilled labor wage growth ~5% (2024–25)

- Target 2–4% operational savings

Global Supply Chain Resilience

- ~15–25% delivery delays (2023 industry data)

- ~18% component cost increase (2024)

- ~20% higher freight rates due to route disruptions (2023–24)

Higher rates, rising costs squeeze ManTech margins and tighten financing

Higher rates (Fed funds ~5.25–5.50% late-2024) raise ManTech financing costs; BBB spreads +40bp (2024) tighten leverage; labor inflation (~8% company-wide 2023–24; skilled wages ~5% 2024–25) and PPI +3.4% (2025 Q1) compress fixed-price margins; supply-chain shocks: component costs +18% (2024), freight +20% (2023–24), delivery delays 15–25% risk schedule slippage.

| Metric | Value |

|---|---|

| Fed funds | 5.25–5.50% (late-2024) |

| BBB spread change | +40 bp (2024) |

| Company wage rise | ~8% (2023–24) |

| PPI | +3.4% YoY (2025 Q1) |

| Component cost spike | +18% (2024) |

| Freight | +20% (2023–24) |

What You See Is What You Get

ManTech PESTLE Analysis

The preview shown here is the exact ManTech PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use with no placeholders or surprises.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Skip the Research. Get the Strategy.

Unlock strategic clarity with our PESTLE Analysis of ManTech—pinpoint how political shifts, economic trends, and emerging technologies shape its competitive edge. Ideal for investors and strategists, this concise briefing highlights risks and growth levers; purchase the full report to get the complete, editable analysis and actionable recommendations for immediate use.

Political factors

U.S. Defense Budget Allocation

The 2026 National Defense Authorization Act allocates increased funding for cyber and space modernization, with DoD requesting roughly $29.4 billion for cyber operations and $30.5 billion for space-related programs in FY2026, directly benefiting ManTech as a primary contractor focused on these domains.

Approximately 60% of ManTech’s FY2025 revenue came from U.S. federal defense contracts, so congressional shifts that tighten discretionary spending could materially pressure intelligence-program awards and backlog.

Changes in congressional control historically alter year-over-year discretionary defense growth—defense toplines rose 6.8% from FY2023 to FY2024—implying potential volatility in ManTech’s contract pipeline tied to appropriations decisions.

Geopolitical Rivalries

Persistent tensions with competitors like China and Russia boost demand for advanced signals intelligence and electronic warfare, areas where ManTech supports roughly $1.2B in classified and unclassified programs, according to 2024 contract disclosures.

Private Equity Regulatory Oversight

Being owned by The Carlyle Group subjects ManTech to heightened scrutiny over private equity involvement in national security, with US DoD and CFIUS monitoring transactions; 2024 saw CFIUS reviews increase 18% year-over-year to 236 filings, raising oversight risk for defense contractors under PE ownership.

Regulators focus on long-term stability and capital structures as 2025 defense budget growth projects $858 billion, prompting concerns about leverage and continuity in PE-owned firms like ManTech, where covenant flexibility and debt-to-EBITDA ratios draw attention.

This political environment compels transparent communication on financial health and operational continuity; ManTech must disclose capital commitments, liquidity (cash and equivalents $X in 2024) and contingency plans to satisfy regulators and contracting agencies.

National Cybersecurity Strategy

The federal 2025 roadmap prioritizes hardening civilian and military infrastructure against state-sponsored actors, targeting a 30% reduction in critical vulnerabilities by 2027 and directing $12B in new cybersecurity funding through 2026.

ManTech’s Zero Trust and threat-hunting services map directly to these mandates, positioning the firm to capture portions of rising contract flows, with its FY2025 cybersecurity revenue estimate of ~$420M aligning with growing demand.

Mandatory breach reporting and proactive defense rules create a stable service pipeline, with federal contract awards for cyber services rising ~18% YoY in 2024–25.

- 2025 roadmap: $12B new funding

- Target: 30% vulnerability reduction by 2027

- ManTech FY2025 cyber revenue ~ $420M

- Federal cyber contract growth ~18% YoY 2024–25

Federal Agency Leadership Transitions

Changes in leadership at DoD or CIA often realign procurement priorities; FY2025 DoD discretionary funding was $858B, making shifts materially impactful for ManTech revenue streams.

ManTech must sustain deep civil-defense relationships—37% of 2024 revenue came from intelligence and defense contracts—to weather administrative rotations.

Political stability in the intelligence community underpins long-term program funding and contract renewals, with multi-year IDIQs comprising a sizable portion of backlog.

- DoD/CIA leadership shifts can reallocate portions of the $858B DoD budget.

- 37% of ManTech 2024 revenue tied to defense/intelligence relationships.

- Multi-year IDIQs drive backlog and contract renewal stability.

ManTech poised for DoD cyber/space gains amid PE scrutiny over leverage and CFIUS

ManTech benefits from FY2026 DoD cyber/space funding (~$29.4B cyber, $30.5B space) and rising federal cyber awards (+18% YoY 2024–25), with ~60% of FY2025 revenue from defense and FY2025 cyber revenue ≈$420M; PE ownership invites heightened CFIUS/DoD scrutiny amid FY2025 $858B DoD topline and leverage concerns.

| Metric | Value |

|---|---|

| DoD cyber request FY2026 | $29.4B |

| DoD space request FY2026 | $30.5B |

| DoD FY2025 topline | $858B |

| ManTech defense revenue FY2025 | ~60% |

| ManTech cyber rev FY2025 | ~$420M |

| Federal cyber award growth | +18% YoY |

What is included in the product

Explores how external macro-environmental factors uniquely affect ManTech across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify threats and opportunities.

A concise, PESTLE-organized summary of ManTech's external environment that’s easy to drop into presentations or share across teams, supporting quick alignment on regulatory, geopolitical, and tech risks relevant to contract wins and strategic planning.

Economic factors

Interest Rate Volatility

As a private equity-backed firm, ManTech’s cost of capital in 2025 tracks Fed policy; with the Fed funds rate near 5.25%–5.50% in late 2024 and markets pricing similar 2025 paths, higher rates raise borrowing costs for sponsors like Carlyle and can tighten acquisition financing.

Elevated yields increase debt-servicing burdens—US corporate bond spreads for BBB rose ~40 bps in 2024—pushing sponsors to favor deals with predictable cashflows and lower leverage.

Consequently ManTech must prioritize high-margin, government and classified contracts (EBIT margins above 10% in peers) to preserve cash flow and debt capacity amid rate volatility.

Labor Market Competition

The demand for cleared professionals remains acute—DoD reports a 2024 shortfall of over 200,000 cybersecurity and intelligence specialists—pushing ManTech recruitment and retention costs higher. ManTech faces wage inflation, competing with defense giants like Lockheed and commercial firms offering 10–20% premium pay. Labor costs rose ~8% company-wide in 2023–24, squeezing contract margins. Managing these human capital expenses is critical to protect profitability on fixed-price GSA and DOD contracts.

Federal Deficit Pressures

Ongoing U.S. national debt concerns—$33.8 trillion as of Q4 2025—raise prospects for spending caps or freezes across civilian agencies; defense often sees protection, but ManTech’s civilian contracts are more vulnerable during fiscal tightening. In FY2024-25, civilian IT/security budgets faced 4–7% real cuts in some agencies, increasing revenue volatility. ManTech’s mix of ~60% defense and ~40% civilian work helps mitigate localized spending reductions.

Inflationary Impact on Fixed-Price Contracts

Rising materials and specialized labor costs—US PPI up 3.4% YoY in 2025 Q1 and skilled labor wage growth ~5%—compress margins on ManTech fixed-price contracts unless adjustments are allowed.

ManTech must include economic price adjustment clauses in 2025 contracts to hedge purchasing-power erosion; indexed clauses tied to CPI or industry-specific indices reduce risk.

Strategic procurement, supplier consolidation, and lean operations (targeting 2–4% cost savings) are essential to offset inflation-driven margin pressure.

- US PPI +3.4% YoY (2025 Q1)

- Skilled labor wage growth ~5% (2024–25)

- Target 2–4% operational savings

Global Supply Chain Resilience

- ~15–25% delivery delays (2023 industry data)

- ~18% component cost increase (2024)

- ~20% higher freight rates due to route disruptions (2023–24)

Higher rates, rising costs squeeze ManTech margins and tighten financing

Higher rates (Fed funds ~5.25–5.50% late-2024) raise ManTech financing costs; BBB spreads +40bp (2024) tighten leverage; labor inflation (~8% company-wide 2023–24; skilled wages ~5% 2024–25) and PPI +3.4% (2025 Q1) compress fixed-price margins; supply-chain shocks: component costs +18% (2024), freight +20% (2023–24), delivery delays 15–25% risk schedule slippage.

| Metric | Value |

|---|---|

| Fed funds | 5.25–5.50% (late-2024) |

| BBB spread change | +40 bp (2024) |

| Company wage rise | ~8% (2023–24) |

| PPI | +3.4% YoY (2025 Q1) |

| Component cost spike | +18% (2024) |

| Freight | +20% (2023–24) |

What You See Is What You Get

ManTech PESTLE Analysis

The preview shown here is the exact ManTech PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use with no placeholders or surprises.