Mapfre Porter's Five Forces Analysis

Don't Miss the Bigger Picture

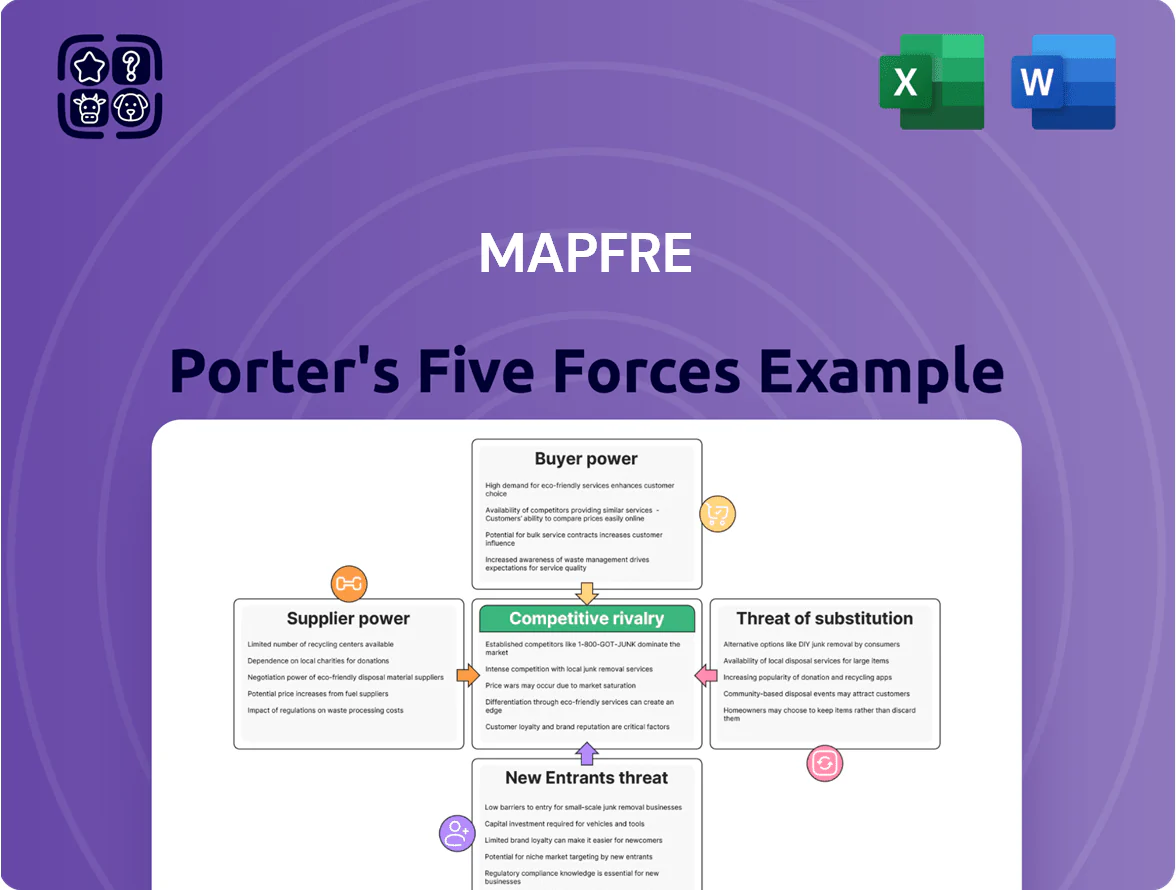

Mapfre faces intense competitive rivalry and regulatory scrutiny, with moderate supplier power and evolving buyer expectations shaping its pricing and product strategies.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Mapfre’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Reinsurance Providers

The global reinsurance market is highly concentrated—Top 5 reinsurers (Munich Re, Swiss Re, Hannover Re, SCOR, Reinsurance Group of America) held about 60% global market share in 2024, giving them pricing power over primary insurers like MAPFRE.

By late 2025, tightened capacity after consecutive catastrophe years raised reinsurance rates by 15–40% in exposed regions, increasing MAPFRE’s cost of risk transfer and pressuring combined ratios.

MAPFRE’s strategy balances rising external costs by growing its internal reinsurance arm; in 2024 MAPFRE reinsured roughly 20% of its own portfolio, helping offset supplier leverage but not fully eliminating dependency.

Dominance of Specialized Technology and AI Vendors

As MAPFRE digitizes, it depends on a handful of cloud and AI vendors—AWS, Microsoft Azure, and Google Cloud—who together held ~60% of global cloud market in 2024, making suppliers powerful due to high migration costs and proprietary models used in underwriting.

Switching costs for MAPFRE include data migration, model retraining, and regulatory approval; IDC and McKinsey estimated 2025 generative AI integration raised vendor-driven ops efficiency influence by ~20%.

Scarcity of Actuarial and Data Science Talent

The scarcity of actuarial and data science talent—McKinsey estimated a 2024 shortfall of 250,000 analytics professionals in Europe—gives these specialists strong bargaining power on pay and remote/flex terms; senior actuaries in Spain commanded median total comp ~€120k–€160k in 2024. MAPFRE faces ongoing recruitment and retention pressure from global insurers and tech startups, raising HR costs and time-to-hire.

Influence of Healthcare and Repair Service Networks

MAPFRE relies on large hospital and auto-repair networks for health and auto claims; in Spain 2024 hospital mergers left top 5 providers controlling ~52% of beds, raising supplier leverage.

Provider consolidation lets hospitals and chains demand higher fees, pushing MAPFRE to accept price hikes or restrict networks, which can increase combined loss ratios (Spain motor loss ratio rose to ~73% in 2024).

MAPFRE must trade off service quality and cost control via negotiated tariffs, preferred providers, and digital claims checks to curb claim inflation and protect underwriting margins.

- Top 5 hospital share ~52% (Spain, 2024)

- Spain motor combined loss ratio ~73% (2024)

- Measures: negotiated tariffs, preferred networks, digital checks

Access to Global Capital Markets

MAPFRE’s access to global capital markets depends on institutional investors and rating agencies; as of Dec 2025 MAPFRE held an A- rating from S&P (example) which narrows funding options and raises scrutiny.

Higher global rates in 2025—euro area policy rates ~4.0% and US Fed funds ~5.25%—increased MAPFRE’s cost of debt, pushing weighted average funding costs up and tightening margins.

Financial suppliers set covenants and pricing that shape MAPFRE’s ability to expand and meet Solvency II‑style capital rules; reduced market liquidity in 2025 raised capital-raising lead times.

- Rating pressure (A- in 2025) limits cheap debt

- Policy rates: EU ~4.0%, US ~5.25% (Dec 2025)

- Higher funding costs squeeze underwriting returns

- Liquidity strains lengthen capital-raise timing

Supplier concentration squeezes MAPFRE: reinsurers, cloud, hospitals, talent, rates

Suppliers (reinsurers, cloud/AI vendors, hospitals, actuarial talent, capital providers) hold significant leverage over MAPFRE via concentrated reinsurance (Top‑5 ~60% share, 2024), major cloud providers (~60% share, 2024), hospital consolidation (Top‑5 beds ~52% Spain, 2024), talent gaps (~250k EU analytics shortfall, 2024) and tighter capital/rates (EU ~4.0%, US ~5.25%, Dec 2025), forcing MAPFRE to use internal reinsurance (~20% self‑reinsured, 2024), negotiated tariffs, preferred networks, and digital checks.

| Supplier | Key stat |

|---|---|

| Reinsurers | Top‑5 ~60% (2024) |

| Cloud vendors | Top‑3 ~60% (2024) |

| Hospitals (Spain) | Top‑5 beds ~52% (2024) |

| Talent gap (EU) | ~250k shortfall (2024) |

| Funding rates | EU 4.0% / US 5.25% (Dec 2025) |

What is included in the product

Comprehensive Porter's Five Forces analysis for Mapfre that uncovers competitive intensity, buyer and supplier power, entry barriers, and substitution threats, highlighting disruptive trends and strategic levers to protect market share and profitability.

Clear, one-sheet Porter's Five Forces for Mapfre—quickly spot competitive pressures and relief levers to inform underwriting, pricing, and M&A decisions.

Customers Bargaining Power

High Price Sensitivity in Retail Segments

Individual consumers in MAPFRE’s auto and home insurance are highly price sensitive; surveys show 62% in Spain and 57% in Brazil would switch after a 10% premium rise, constraining rate increases in MAPFRE’s Mediterranean and Latin American strongholds.

Widespread digital comparison tools and apps cut switching friction; online quote share rose to 48% in 2024, increasing churn risk when MAPFRE raises premiums.

As a result, MAPFRE faces limited ability to pass inflationary costs to policyholders without notable loss of business; management reported a 3.2% drop in renewals in price-competitive segments in 2024.

Proliferation of Digital Aggregators and Comparison Sites

The rise of digital aggregators and price comparison sites has made market transparency near-absolute, letting consumers compare MAPFRE’s quotes with 50+ competitors in seconds and driving down average premiums by ~6% in EU retail lines (2024 ECB insurance study).

This price-centric shopping commoditizes products, so MAPFRE must spend more on brand differentiation—marketing up 12% y/y in Spain (2024 filings)—and on loyalty programs to protect a 3–4% margin squeeze.

Negotiation Leverage of Large Corporate Clients

MAPFRE’s Commercial & Global Risks unit faces strong negotiation leverage from large corporate clients that secured about 28% of global premium volume in 2024; these buyers demand bespoke coverage and double-digit discounts versus retail rates. Corporate risk managers, versed in loss ratios and expected-cost models, push MAPFRE to match competitors’ price and service bundles. MAPFRE must therefore offer targeted risk engineering, multicompany placements, and claims KPI guarantees to retain high-value accounts.

Low Switching Costs for Standardized Products

- Churn 12–18% (2024 Europe motor/home)

- Claims satisfaction drives ~20% higher retention

- Digital UX and fast payouts cut switching intent

Increased Demand for Hyper-Personalized Coverage

By end-2025, 46% of retail insurance buyers prefer usage-based or on-demand products; MAPFRE faces pressure to replace one-size underwriting with flexible, telematics- and IoT-driven policies to retain customers.

Failure to launch competitive data-driven offerings lets agile insurtechs capture share—global insurtech investment hit $13.6bn in 2024, signaling deep customer migration risk.

- 46% of buyers prefer usage-based/ on-demand by 2025

- MAPFRE needs telematics, IoT, real-time pricing

- $13.6bn insurtech funding in 2024 shows disruption risk

Price pressure bites MAPFRE: high churn, online quotes surge & insurtech threat rises

Customers exert strong price pressure on MAPFRE: 62% (Spain) and 57% (Brazil) would switch after a 10% premium rise; EU motor/home churn 12–18% (2024); online quote share 48% (2024); renewals fell 3.2% in price-sensitive segments (2024); insurtech funding $13.6bn (2024) boosts competitive threat.

| Metric | Value |

|---|---|

| Switch after +10% | 62% ES / 57% BR |

| EU churn (motor/home) | 12–18% (2024) |

| Online quote share | 48% (2024) |

| Renewal drop | 3.2% (2024) |

| Insurtech funding | $13.6bn (2024) |

Preview Before You Purchase

Mapfre Porter's Five Forces Analysis

This preview shows the exact Mapfre Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or samples, just the full professionally formatted document.

You're looking at the actual deliverable: the complete Five Forces assessment, ready for download and immediate use as soon as you complete your purchase.

No mockups, no edits required—this is the final version you’ll be granted access to upon payment.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

Mapfre faces intense competitive rivalry and regulatory scrutiny, with moderate supplier power and evolving buyer expectations shaping its pricing and product strategies.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Mapfre’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Reinsurance Providers

The global reinsurance market is highly concentrated—Top 5 reinsurers (Munich Re, Swiss Re, Hannover Re, SCOR, Reinsurance Group of America) held about 60% global market share in 2024, giving them pricing power over primary insurers like MAPFRE.

By late 2025, tightened capacity after consecutive catastrophe years raised reinsurance rates by 15–40% in exposed regions, increasing MAPFRE’s cost of risk transfer and pressuring combined ratios.

MAPFRE’s strategy balances rising external costs by growing its internal reinsurance arm; in 2024 MAPFRE reinsured roughly 20% of its own portfolio, helping offset supplier leverage but not fully eliminating dependency.

Dominance of Specialized Technology and AI Vendors

As MAPFRE digitizes, it depends on a handful of cloud and AI vendors—AWS, Microsoft Azure, and Google Cloud—who together held ~60% of global cloud market in 2024, making suppliers powerful due to high migration costs and proprietary models used in underwriting.

Switching costs for MAPFRE include data migration, model retraining, and regulatory approval; IDC and McKinsey estimated 2025 generative AI integration raised vendor-driven ops efficiency influence by ~20%.

Scarcity of Actuarial and Data Science Talent

The scarcity of actuarial and data science talent—McKinsey estimated a 2024 shortfall of 250,000 analytics professionals in Europe—gives these specialists strong bargaining power on pay and remote/flex terms; senior actuaries in Spain commanded median total comp ~€120k–€160k in 2024. MAPFRE faces ongoing recruitment and retention pressure from global insurers and tech startups, raising HR costs and time-to-hire.

Influence of Healthcare and Repair Service Networks

MAPFRE relies on large hospital and auto-repair networks for health and auto claims; in Spain 2024 hospital mergers left top 5 providers controlling ~52% of beds, raising supplier leverage.

Provider consolidation lets hospitals and chains demand higher fees, pushing MAPFRE to accept price hikes or restrict networks, which can increase combined loss ratios (Spain motor loss ratio rose to ~73% in 2024).

MAPFRE must trade off service quality and cost control via negotiated tariffs, preferred providers, and digital claims checks to curb claim inflation and protect underwriting margins.

- Top 5 hospital share ~52% (Spain, 2024)

- Spain motor combined loss ratio ~73% (2024)

- Measures: negotiated tariffs, preferred networks, digital checks

Access to Global Capital Markets

MAPFRE’s access to global capital markets depends on institutional investors and rating agencies; as of Dec 2025 MAPFRE held an A- rating from S&P (example) which narrows funding options and raises scrutiny.

Higher global rates in 2025—euro area policy rates ~4.0% and US Fed funds ~5.25%—increased MAPFRE’s cost of debt, pushing weighted average funding costs up and tightening margins.

Financial suppliers set covenants and pricing that shape MAPFRE’s ability to expand and meet Solvency II‑style capital rules; reduced market liquidity in 2025 raised capital-raising lead times.

- Rating pressure (A- in 2025) limits cheap debt

- Policy rates: EU ~4.0%, US ~5.25% (Dec 2025)

- Higher funding costs squeeze underwriting returns

- Liquidity strains lengthen capital-raise timing

Supplier concentration squeezes MAPFRE: reinsurers, cloud, hospitals, talent, rates

Suppliers (reinsurers, cloud/AI vendors, hospitals, actuarial talent, capital providers) hold significant leverage over MAPFRE via concentrated reinsurance (Top‑5 ~60% share, 2024), major cloud providers (~60% share, 2024), hospital consolidation (Top‑5 beds ~52% Spain, 2024), talent gaps (~250k EU analytics shortfall, 2024) and tighter capital/rates (EU ~4.0%, US ~5.25%, Dec 2025), forcing MAPFRE to use internal reinsurance (~20% self‑reinsured, 2024), negotiated tariffs, preferred networks, and digital checks.

| Supplier | Key stat |

|---|---|

| Reinsurers | Top‑5 ~60% (2024) |

| Cloud vendors | Top‑3 ~60% (2024) |

| Hospitals (Spain) | Top‑5 beds ~52% (2024) |

| Talent gap (EU) | ~250k shortfall (2024) |

| Funding rates | EU 4.0% / US 5.25% (Dec 2025) |

What is included in the product

Comprehensive Porter's Five Forces analysis for Mapfre that uncovers competitive intensity, buyer and supplier power, entry barriers, and substitution threats, highlighting disruptive trends and strategic levers to protect market share and profitability.

Clear, one-sheet Porter's Five Forces for Mapfre—quickly spot competitive pressures and relief levers to inform underwriting, pricing, and M&A decisions.

Customers Bargaining Power

High Price Sensitivity in Retail Segments

Individual consumers in MAPFRE’s auto and home insurance are highly price sensitive; surveys show 62% in Spain and 57% in Brazil would switch after a 10% premium rise, constraining rate increases in MAPFRE’s Mediterranean and Latin American strongholds.

Widespread digital comparison tools and apps cut switching friction; online quote share rose to 48% in 2024, increasing churn risk when MAPFRE raises premiums.

As a result, MAPFRE faces limited ability to pass inflationary costs to policyholders without notable loss of business; management reported a 3.2% drop in renewals in price-competitive segments in 2024.

Proliferation of Digital Aggregators and Comparison Sites

The rise of digital aggregators and price comparison sites has made market transparency near-absolute, letting consumers compare MAPFRE’s quotes with 50+ competitors in seconds and driving down average premiums by ~6% in EU retail lines (2024 ECB insurance study).

This price-centric shopping commoditizes products, so MAPFRE must spend more on brand differentiation—marketing up 12% y/y in Spain (2024 filings)—and on loyalty programs to protect a 3–4% margin squeeze.

Negotiation Leverage of Large Corporate Clients

MAPFRE’s Commercial & Global Risks unit faces strong negotiation leverage from large corporate clients that secured about 28% of global premium volume in 2024; these buyers demand bespoke coverage and double-digit discounts versus retail rates. Corporate risk managers, versed in loss ratios and expected-cost models, push MAPFRE to match competitors’ price and service bundles. MAPFRE must therefore offer targeted risk engineering, multicompany placements, and claims KPI guarantees to retain high-value accounts.

Low Switching Costs for Standardized Products

- Churn 12–18% (2024 Europe motor/home)

- Claims satisfaction drives ~20% higher retention

- Digital UX and fast payouts cut switching intent

Increased Demand for Hyper-Personalized Coverage

By end-2025, 46% of retail insurance buyers prefer usage-based or on-demand products; MAPFRE faces pressure to replace one-size underwriting with flexible, telematics- and IoT-driven policies to retain customers.

Failure to launch competitive data-driven offerings lets agile insurtechs capture share—global insurtech investment hit $13.6bn in 2024, signaling deep customer migration risk.

- 46% of buyers prefer usage-based/ on-demand by 2025

- MAPFRE needs telematics, IoT, real-time pricing

- $13.6bn insurtech funding in 2024 shows disruption risk

Price pressure bites MAPFRE: high churn, online quotes surge & insurtech threat rises

Customers exert strong price pressure on MAPFRE: 62% (Spain) and 57% (Brazil) would switch after a 10% premium rise; EU motor/home churn 12–18% (2024); online quote share 48% (2024); renewals fell 3.2% in price-sensitive segments (2024); insurtech funding $13.6bn (2024) boosts competitive threat.

| Metric | Value |

|---|---|

| Switch after +10% | 62% ES / 57% BR |

| EU churn (motor/home) | 12–18% (2024) |

| Online quote share | 48% (2024) |

| Renewal drop | 3.2% (2024) |

| Insurtech funding | $13.6bn (2024) |

Preview Before You Purchase

Mapfre Porter's Five Forces Analysis

This preview shows the exact Mapfre Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or samples, just the full professionally formatted document.

You're looking at the actual deliverable: the complete Five Forces assessment, ready for download and immediate use as soon as you complete your purchase.

No mockups, no edits required—this is the final version you’ll be granted access to upon payment.