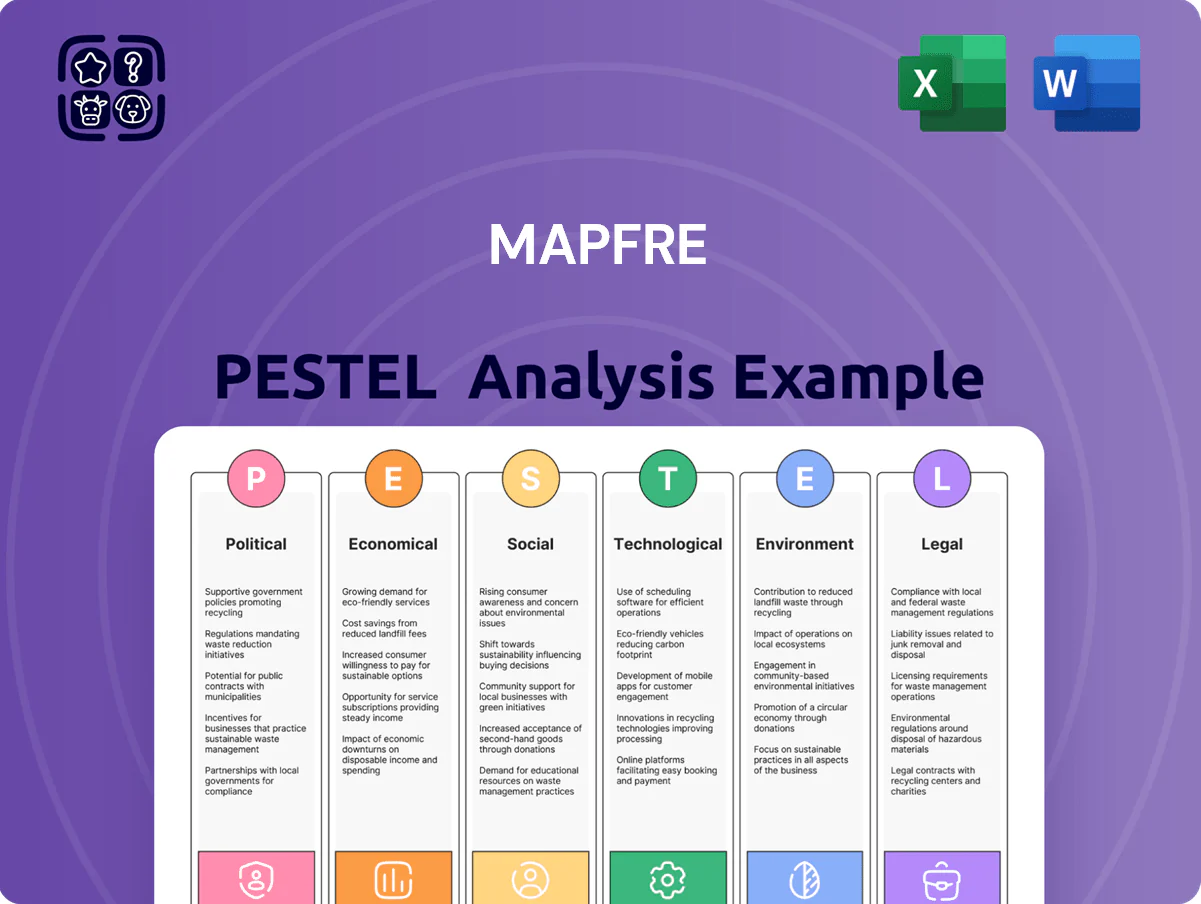

Mapfre PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Gain a competitive edge with our PESTLE analysis of Mapfre—concise, current, and focused on the political, economic, social, technological, legal, and environmental forces shaping its prospects; buy the full report to access actionable insights, scenarios, and strategic recommendations you can use immediately.

Political factors

Regulatory stability in core Iberian and Latin American markets

Regulatory stability in Spain and Brazil is critical for MAPFRE, as Spain and Brazil together accounted for about 54% of MAPFRE Grupo revenues in 2024 (≈€21.6bn of €40.0bn), so reforms to social security and private pension rules materially affect demand for life and savings products.

Recent proposals in Spain to adjust pension replacement rates and Brazil's 2024 pension rule changes could shift premium flows and reserves assumptions, altering product mix and solvency needs.

MAPFRE must also manage political volatility across Latin America—countries with higher risk can affect licenses and capital repatriation, influencing the group’s capital allocation and regulatory capital buffers.

Geopolitical tensions and global reinsurance stability

Ongoing geopolitical conflicts and trade disputes at end-2025 have tightened global reinsurance capacity, pushing average treaty rates up about 12% year-on-year and raising political risk insurance premia by ~18%, per market reports. These shifts strain availability for international commercial clients, with some markets limiting aggregate limits. MAPFRE’s presence in 50+ countries necessitates advanced cross-border risk models and robust sanctions compliance to avoid regulatory fines and coverage gaps.

Government mandates on mandatory insurance coverage

Political mandates on mandatory health, auto or catastrophe insurance directly affect MAPFRE’s market share and product design, with Spain’s compulsory motor third-party liability sustaining roughly 40% of its Iberian motor book in 2024.

Expansion or contraction of government-subsidized programs—for example Latin American social insurance growth of 6% GDP in 2023—can open distribution channels or raise competition from public insurers.

MAPFRE monitors policy shifts closely and adjusted its 2024 portfolio, reallocating €350m of capital to align products with national safety nets and social welfare objectives.

Taxation policies and corporate fiscal responsibility

Changes in corporate tax rates and the OECD/GloBE global minimum tax (15%) affect MAPFRE’s net margins across Spain, Latin America and US operations; in 2024 MAPFRE reported a consolidated tax expense of €338m, reflecting geographic tax mix pressures.

Governments increasingly offer tax credits for green investments; MAPFRE’s 2023 sustainable investments amounted to €2.1bn, leveraged for tax incentives in several jurisdictions.

MAPFRE aligns financial planning to optimize tax efficiency while publishing transparent fiscal governance—effective tax rate 2023: 17.8%—to maintain stakeholder trust.

- Global minimum tax (15%) impacts profit allocation

- €338m tax expense (2024), 17.8% effective tax rate (2023)

- €2.1bn sustainable investments (2023) used for tax incentives

Public-private partnerships in healthcare and infrastructure

Governments increasingly turn to private insurers like MAPFRE to ease public healthcare burdens; MAPFRE reported €1.1bn in global health premiums in 2024, highlighting expansion opportunities through public-private contracts.

These partnerships enable MAPFRE to scale health coverage and deliver essential services to wider populations, aligning with its 2024 strategy to grow health GWP by ~8% year-on-year.

Navigating political requirements and procurement rules is critical to secure long-term growth in health and infrastructure sectors amid rising public contract scrutiny.

- MAPFRE 2024 health premiums: €1.1bn

- Target health GWP growth ~8% YoY (2024 strategy)

- Requires compliance with procurement and political risk frameworks

MAPFRE faces tax, reinsurance and political shocks in Spain/Brazil, pressuring margins

Political/regulatory shifts in Spain and Brazil (≈54% of 2024 revenues, €21.6bn) materially affect MAPFRE’s life/savings demand, solvency and capital allocation; OECD/GloBE 15% tax and 2024 tax expense €338m reshape net margins. Reinsurance tightening (+12% treaty rates) and higher political risk premia (~+18%) increase costs; public-private health contracts (health premiums €1.1bn in 2024) offer growth but require strict procurement compliance.

| Metric | Value |

|---|---|

| 2024 revenues (Spain+Brazil) | €21.6bn (≈54%) |

| 2024 tax expense | €338m |

| Effective tax rate 2023 | 17.8% |

| Sustainable investments 2023 | €2.1bn |

| Health premiums 2024 | €1.1bn |

| Reinsurance rate change | +12% YoY |

| Political risk premia change | +18% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Mapfre across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—using current data and regional regulatory context.

Clean, concise Mapfre PESTLE summary that’s visually segmented for quick interpretation, easily dropped into presentations, annotated for local context, and shareable across teams to streamline risk discussions and strategic planning.

Economic factors

Interest rate environment and investment portfolio yields

At end-2025, ECB rates around 3.25% and US 10y at ~4.2% materially lift MAPFRE’s investment income given ~70% fixed-income allocation, improving life-margin prospects; however a 2025 yield spike caused unrealized bond MTM losses of several hundred million euros on longer-duration holdings. MAPFRE actively adjusts duration and ALM to capture higher yields while limiting interest-rate sensitivity.

Inflationary pressure on claims and operational costs

Persistent inflation in labor, medical services and auto parts has pushed MAPFRE’s combined ratio higher, with Spain’s motor repair costs up ~8% YoY and global medical inflation near 6% in 2024, directly raising claims expenses and loss ratios.

To protect profitability MAPFRE must apply disciplined pricing and more frequent premium adjustments across P&C lines; the group raised tariffs by c.4–7% in 2024 in key markets.

Managing the lag between cost inflation and premium increases remains critical, as delayed repricing can erode underwriting margins and drive higher reserve strain.

Currency fluctuations in emerging markets

As a multinational operating extensively in Latin America, MAPFRE faces volatility from currencies such as the Brazilian Real and Mexican Peso versus the Euro; the Real fell about 9% against the Euro in 2024, amplifying translation risk for 2024 earnings. Significant depreciations erode the value of international revenues and equity when reported in euros, with MAPFRE reporting Latin America contributed ~28% of gross written premiums in 2024. The group uses hedging strategies—forwards, options and natural hedges—to mitigate FX impact and stated in its 2024 annual report that hedges reduced net exposure by an estimated 60% during major swings.

Global economic growth and insurance demand

The pace of GDP growth in MAPFRE’s core markets—Spain, Brazil, Mexico and the US—directly shapes demand for commercial and personal insurance; IMF 2025 forecasts showed 1.2% for Spain and 2.4% for Latin America, constraining premium growth in 2024–25.

Economic slowdowns cut discretionary insurance spending and depress car sales (global auto sales fell ~2.5% in 2024) and property development activity, reducing new business volumes.

MAPFRE has increased diversification—non-life vs life mix and international expansion—helping sustain operating revenue (2024 revenue €22.1bn) amid stagnant GDP phases.

- GDP sensitivity: key markets growth ~1–2.5% (2024–25)

- Auto sales decline ~2.5% (2024) reduces motor premiums

- 2024 revenue €22.1bn; diversification cushions downturns

Consumer purchasing power and premium sensitivity

The OECD reported real household disposable income rose 1.2% in 2025 Q4, moderating lapses in MAPFRE life policies but urban Spanish households saw 0.5–1.5 pp higher lapse rates in lower-income brackets; comprehensive auto uptake remained 3% below 2019 levels in price-sensitive markets.

MAPFRE faces competition from low-cost insurers and insurtechs with 10–18% pricing discounts; it offsets pressure by leveraging brand trust, 82% satisfaction scores in Spain (2024), and flexible monthly payment plans to preserve retention.

- 2025 disposable income +1.2% OECD; lapses higher in low-income segments

- Auto comprehensive uptake −3% vs 2019 in price-sensitive markets

- Competitors offer 10–18% lower pricing

- MAPFRE satisfaction 82% (Spain 2024); flexible payments boost retention

Higher yields lift MAPFRE income but FX, inflation and GDP slow premium growth

Higher yields (ECB ~3.25%, US 10y ~4.2% end-2025) boost MAPFRE investment income but caused several hundred million euros MTM losses in 2025; inflation (Spain motor repair +8% YoY, global medical ~6% in 2024) raised combined ratio; FX (BRL −9% vs EUR in 2024) and GDP headwinds (Spain ~1.2%, LatAm ~2.4% IMF 2025) constrain premium growth; 2024 revenue €22.1bn; hedges cut FX exposure ~60%.

| Metric | Value |

|---|---|

| 2024 Revenue | €22.1bn |

| ECB rate | ~3.25% |

| US 10y | ~4.2% |

| BRL vs EUR 2024 | −9% |

| Spain motor repair inflation | +8% YoY |

Same Document Delivered

Mapfre PESTLE Analysis

The preview shown here is the exact Mapfre PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic analysis and decision-making.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Gain a competitive edge with our PESTLE analysis of Mapfre—concise, current, and focused on the political, economic, social, technological, legal, and environmental forces shaping its prospects; buy the full report to access actionable insights, scenarios, and strategic recommendations you can use immediately.

Political factors

Regulatory stability in core Iberian and Latin American markets

Regulatory stability in Spain and Brazil is critical for MAPFRE, as Spain and Brazil together accounted for about 54% of MAPFRE Grupo revenues in 2024 (≈€21.6bn of €40.0bn), so reforms to social security and private pension rules materially affect demand for life and savings products.

Recent proposals in Spain to adjust pension replacement rates and Brazil's 2024 pension rule changes could shift premium flows and reserves assumptions, altering product mix and solvency needs.

MAPFRE must also manage political volatility across Latin America—countries with higher risk can affect licenses and capital repatriation, influencing the group’s capital allocation and regulatory capital buffers.

Geopolitical tensions and global reinsurance stability

Ongoing geopolitical conflicts and trade disputes at end-2025 have tightened global reinsurance capacity, pushing average treaty rates up about 12% year-on-year and raising political risk insurance premia by ~18%, per market reports. These shifts strain availability for international commercial clients, with some markets limiting aggregate limits. MAPFRE’s presence in 50+ countries necessitates advanced cross-border risk models and robust sanctions compliance to avoid regulatory fines and coverage gaps.

Government mandates on mandatory insurance coverage

Political mandates on mandatory health, auto or catastrophe insurance directly affect MAPFRE’s market share and product design, with Spain’s compulsory motor third-party liability sustaining roughly 40% of its Iberian motor book in 2024.

Expansion or contraction of government-subsidized programs—for example Latin American social insurance growth of 6% GDP in 2023—can open distribution channels or raise competition from public insurers.

MAPFRE monitors policy shifts closely and adjusted its 2024 portfolio, reallocating €350m of capital to align products with national safety nets and social welfare objectives.

Taxation policies and corporate fiscal responsibility

Changes in corporate tax rates and the OECD/GloBE global minimum tax (15%) affect MAPFRE’s net margins across Spain, Latin America and US operations; in 2024 MAPFRE reported a consolidated tax expense of €338m, reflecting geographic tax mix pressures.

Governments increasingly offer tax credits for green investments; MAPFRE’s 2023 sustainable investments amounted to €2.1bn, leveraged for tax incentives in several jurisdictions.

MAPFRE aligns financial planning to optimize tax efficiency while publishing transparent fiscal governance—effective tax rate 2023: 17.8%—to maintain stakeholder trust.

- Global minimum tax (15%) impacts profit allocation

- €338m tax expense (2024), 17.8% effective tax rate (2023)

- €2.1bn sustainable investments (2023) used for tax incentives

Public-private partnerships in healthcare and infrastructure

Governments increasingly turn to private insurers like MAPFRE to ease public healthcare burdens; MAPFRE reported €1.1bn in global health premiums in 2024, highlighting expansion opportunities through public-private contracts.

These partnerships enable MAPFRE to scale health coverage and deliver essential services to wider populations, aligning with its 2024 strategy to grow health GWP by ~8% year-on-year.

Navigating political requirements and procurement rules is critical to secure long-term growth in health and infrastructure sectors amid rising public contract scrutiny.

- MAPFRE 2024 health premiums: €1.1bn

- Target health GWP growth ~8% YoY (2024 strategy)

- Requires compliance with procurement and political risk frameworks

MAPFRE faces tax, reinsurance and political shocks in Spain/Brazil, pressuring margins

Political/regulatory shifts in Spain and Brazil (≈54% of 2024 revenues, €21.6bn) materially affect MAPFRE’s life/savings demand, solvency and capital allocation; OECD/GloBE 15% tax and 2024 tax expense €338m reshape net margins. Reinsurance tightening (+12% treaty rates) and higher political risk premia (~+18%) increase costs; public-private health contracts (health premiums €1.1bn in 2024) offer growth but require strict procurement compliance.

| Metric | Value |

|---|---|

| 2024 revenues (Spain+Brazil) | €21.6bn (≈54%) |

| 2024 tax expense | €338m |

| Effective tax rate 2023 | 17.8% |

| Sustainable investments 2023 | €2.1bn |

| Health premiums 2024 | €1.1bn |

| Reinsurance rate change | +12% YoY |

| Political risk premia change | +18% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Mapfre across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—using current data and regional regulatory context.

Clean, concise Mapfre PESTLE summary that’s visually segmented for quick interpretation, easily dropped into presentations, annotated for local context, and shareable across teams to streamline risk discussions and strategic planning.

Economic factors

Interest rate environment and investment portfolio yields

At end-2025, ECB rates around 3.25% and US 10y at ~4.2% materially lift MAPFRE’s investment income given ~70% fixed-income allocation, improving life-margin prospects; however a 2025 yield spike caused unrealized bond MTM losses of several hundred million euros on longer-duration holdings. MAPFRE actively adjusts duration and ALM to capture higher yields while limiting interest-rate sensitivity.

Inflationary pressure on claims and operational costs

Persistent inflation in labor, medical services and auto parts has pushed MAPFRE’s combined ratio higher, with Spain’s motor repair costs up ~8% YoY and global medical inflation near 6% in 2024, directly raising claims expenses and loss ratios.

To protect profitability MAPFRE must apply disciplined pricing and more frequent premium adjustments across P&C lines; the group raised tariffs by c.4–7% in 2024 in key markets.

Managing the lag between cost inflation and premium increases remains critical, as delayed repricing can erode underwriting margins and drive higher reserve strain.

Currency fluctuations in emerging markets

As a multinational operating extensively in Latin America, MAPFRE faces volatility from currencies such as the Brazilian Real and Mexican Peso versus the Euro; the Real fell about 9% against the Euro in 2024, amplifying translation risk for 2024 earnings. Significant depreciations erode the value of international revenues and equity when reported in euros, with MAPFRE reporting Latin America contributed ~28% of gross written premiums in 2024. The group uses hedging strategies—forwards, options and natural hedges—to mitigate FX impact and stated in its 2024 annual report that hedges reduced net exposure by an estimated 60% during major swings.

Global economic growth and insurance demand

The pace of GDP growth in MAPFRE’s core markets—Spain, Brazil, Mexico and the US—directly shapes demand for commercial and personal insurance; IMF 2025 forecasts showed 1.2% for Spain and 2.4% for Latin America, constraining premium growth in 2024–25.

Economic slowdowns cut discretionary insurance spending and depress car sales (global auto sales fell ~2.5% in 2024) and property development activity, reducing new business volumes.

MAPFRE has increased diversification—non-life vs life mix and international expansion—helping sustain operating revenue (2024 revenue €22.1bn) amid stagnant GDP phases.

- GDP sensitivity: key markets growth ~1–2.5% (2024–25)

- Auto sales decline ~2.5% (2024) reduces motor premiums

- 2024 revenue €22.1bn; diversification cushions downturns

Consumer purchasing power and premium sensitivity

The OECD reported real household disposable income rose 1.2% in 2025 Q4, moderating lapses in MAPFRE life policies but urban Spanish households saw 0.5–1.5 pp higher lapse rates in lower-income brackets; comprehensive auto uptake remained 3% below 2019 levels in price-sensitive markets.

MAPFRE faces competition from low-cost insurers and insurtechs with 10–18% pricing discounts; it offsets pressure by leveraging brand trust, 82% satisfaction scores in Spain (2024), and flexible monthly payment plans to preserve retention.

- 2025 disposable income +1.2% OECD; lapses higher in low-income segments

- Auto comprehensive uptake −3% vs 2019 in price-sensitive markets

- Competitors offer 10–18% lower pricing

- MAPFRE satisfaction 82% (Spain 2024); flexible payments boost retention

Higher yields lift MAPFRE income but FX, inflation and GDP slow premium growth

Higher yields (ECB ~3.25%, US 10y ~4.2% end-2025) boost MAPFRE investment income but caused several hundred million euros MTM losses in 2025; inflation (Spain motor repair +8% YoY, global medical ~6% in 2024) raised combined ratio; FX (BRL −9% vs EUR in 2024) and GDP headwinds (Spain ~1.2%, LatAm ~2.4% IMF 2025) constrain premium growth; 2024 revenue €22.1bn; hedges cut FX exposure ~60%.

| Metric | Value |

|---|---|

| 2024 Revenue | €22.1bn |

| ECB rate | ~3.25% |

| US 10y | ~4.2% |

| BRL vs EUR 2024 | −9% |

| Spain motor repair inflation | +8% YoY |

Same Document Delivered

Mapfre PESTLE Analysis

The preview shown here is the exact Mapfre PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic analysis and decision-making.