Maple Leaf Boston Consulting Group Matrix

Unlock Strategic Clarity

The Maple Leaf BCG Matrix preview highlights where key product lines currently sit—showing growth potential, cash generation, and where resources may be leaking—but it’s only a snapshot of strategic opportunity. Purchase the full BCG Matrix for detailed quadrant assignments, underlying market data, and actionable recommendations tailored to each business unit. Get instant access to a ready-to-use Word report plus an Excel summary that speeds decision-making and clarifies where to invest, divest, or defend next.

Stars

Fresh Poultry Segment

Fresh Poultry is a Star: Q3 2025 sales jumped 15.7%, driven by a shift to value‑added retail and foodservice and full output from the London, Ontario plant, lifting segment EBITDA margin to an estimated 9.8% in FY2025.

Sustainable Meats Portfolio

Maple Leaf Foods has branded its Sustainable Meats portfolio—carbon-neutral and RWA (raised without antibiotics)—as a primary growth engine in North America, targeting double-digit CAGR versus ~3–4% CPG growth; management cites 2026 guidance where Sustainable Meats is expected to outpace the broader market.

U.S. Market Expansion

Maple Leaf is rapidly expanding in the U.S.; brand Just Bare surpassed $1 billion in retail sales by Q1 2025, signaling strong product-market fit and pricing power.

This move targets high-growth share gains versus U.S. incumbents, driven by clearer sustainability claims and premium branding, with U.S. revenue up ~35% YoY in 2024.

Ongoing investment in distribution and marketing—targeting a 20% increase in U.S. SKU distribution and +15% ad spend in 2025—is required to convert current momentum into long-term leadership.

Bacon Center of Excellence

Bacon Center of Excellence, Maple Leaf’s Winnipeg facility, hit full business-case benefits in late 2024 and drove double-digit category growth through 2025, with premium bacon volumes up 18% and segment revenue rising 22% year-over-year.

By prioritizing high-margin breakfast and snacking SKUs, the unit lifted Prepared Foods’ margin by 150 basis points and returned payback on the capital investment within 30 months, making it a BCG Matrix star with high market growth and leading share.

- 18% volume growth 2025

- 22% revenue increase 2025

- +150 bps margin impact

- 30-month capital payback

Innovation Pipeline and New SKUs

With over 50 new consumer-relevant innovations launched in 2025, Maple Leaf’s rapid product development is capturing trends in convenience and frozen breakfast, driving mid-single-digit top-line growth forecast of ~4–6% for 2026.

High adoption rates are securing shelf space in high-growth channels; convenience and frozen breakfast now represent an estimated 12% of revenue, up 3 points year-over-year, boosting market relevance and retailer support.

- 50+ new SKUs launched in 2025

- 2026 revenue growth projection: ~4–6%

- Convenience/frozen breakfast ≈12% of revenue (+3 ppt YoY)

- Faster shelf gains in high-growth retail channels

High-Growth Proteins: Fresh Poultry +15.7%, Just Bare $1B+, Bacon +18%—50+ SKUs

Stars: Fresh Poultry, Sustainable Meats, Just Bare and Bacon CoE drive high growth—Fresh Poultry +15.7% Q3 2025, Just Bare $1B+ retail by Q1 2025, Bacon volumes +18% 2025; Sustainable Meats targets double‑digit CAGR vs 3–4% CPG; 50+ SKUs 2025, convenience/frozen breakfast 12% revenue (+3 ppt).

| Metric | 2025 |

|---|---|

| Fresh Poultry sales | +15.7% |

| Just Bare retail | $1.0B+ |

| Bacon vol. | +18% |

| New SKUs | 50+ |

What is included in the product

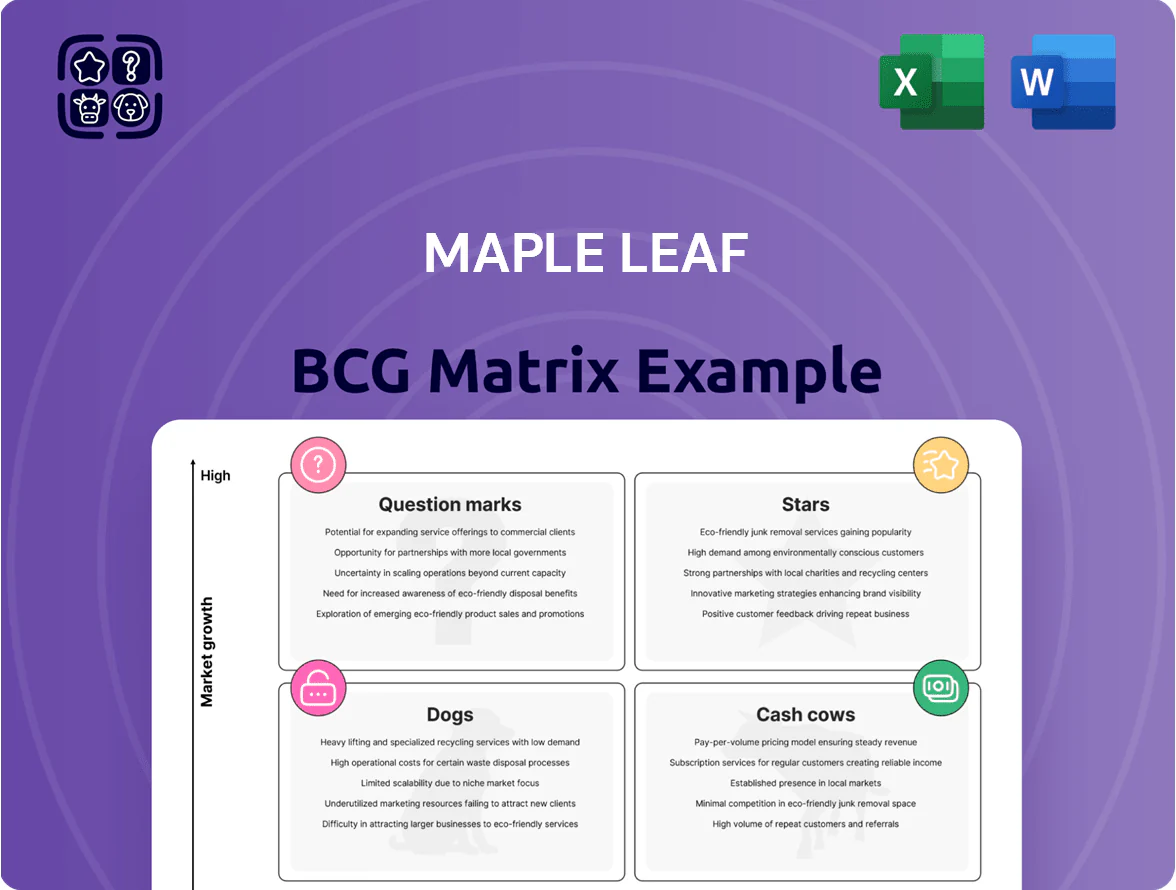

Comprehensive BCG Matrix review of Maple Leaf’s portfolio with strategic moves for Stars, Cash Cows, Question Marks, and Dogs.

One-page BCG matrix placing each Maple Leaf business unit in a clear quadrant for instant portfolio clarity.

Cash Cows

Prepared Meats Core Brands

The flagship Maple Leaf and Schneiders brands hold ~45–55% combined share of Canada’s deli and prepared meats market (2024 Nielsen data), producing steady EBITDA margins near 12% and roughly CAD 350–400m annual free cash flow in 2024.

With major capital projects finished by end-2024, incremental capex needs are low (projected CAD 50–70m annually 2025–27), so this cash funds dividend increases and services CAD 1.2bn net debt as Maple Leaf shifts to a brand-led CPG model.

Canadian Retail Operations

Maple Leaf Foods holds ~18% share of the Canadian retail CPG meat and prepared foods market (2024), serving major chains like Loblaw, Sobeys and Metro and generating stable EBITDA margins near 12% in 2024.

Canada’s CPG growth averages ~2% annually (2020–24), yet Maple Leaf’s scale and long-term supply contracts drive cash conversion that funds ~CAD 120–150m/year in R&D and supports international Star-category expansion.

Foodservice Distribution Network

Maple Leaf’s Foodservice Distribution Network holds long-term contracts with major Canadian chains, generating high-volume revenue—about CAD 2.1 billion sales in 2024 and ~9% adjusted operating margin—making it a classic Cash Cow in the BCG matrix.

Market is mature, so promotional spend is low (<1.5% of segment sales), keeping margins steady and funding capital needs without equity raises.

These steady margins underpin Maple Leaf’s investment-grade balance sheet through 2026, supporting net debt/EBITDA near 1.8x in 2025.

International Pork Sales (Post-Spin-off)

Post-spin-off (Canada Packers, Dec 2025), Maple Leaf keeps strategic stakes and evergreen supply contracts that deliver steady international pork revenue—about CAD 220m in 2025 export-linked receipts, smoothing exposure to hog-price swings.

These predictable cash flows fund high-margin prepared-food R&D and shareholder returns; management redirected ~CAD 150m in 2025 to innovation and CAD 70m to buybacks/dividends.

- Evergreen supply secures volumes, cuts production volatility

- ~CAD 220m export-linked revenue (2025)

- ~CAD 150m to prepared-food innovation (2025)

- ~CAD 70m returned to shareholders (2025)

Legacy Processing Facilities

Legacy Processing Facilities have been optimized by closing 6 older plants and consolidating production into 4 modern hubs, raising factory utilization to 92% and boosting EBITDA margins on mature lines from 12% (2019) to 21% (2024) under the Fuel for Growth cost cuts.

These lines deliver ~1.2 million tonnes of staple products annually, require <3% capex-to-sales, and contribute ~38% of Maple Leaf’s operating cash flow in FY2024.

- Closed 6 plants, 4 hubs remain

- Utilization 92%

- EBITDA margin up 9 pts to 21%

- ~1.2M tonnes/year output

- Capex-to-sales <3%

- 38% of FY2024 operating cash flow

Maple Leaf: Strong FCF, 1.8x Net Debt, CAD 150m R&D & CAD 70m Returns in 2025

Maple Leaf’s Cash Cows: flagship deli/prepared brands (45–55% category share) and Foodservice network (CAD 2.1bn sales, ~9% adj. op margin) generated CAD 350–400m free cash flow in 2024; capex 2025–27 ~CAD 50–70m supports CAD 1.2bn net debt (net debt/EBITDA ~1.8x) while funding CAD 150m R&D and CAD 70m returns in 2025.

| Metric | 2024/25 |

|---|---|

| Free cash flow | CAD 350–400m (2024) |

| Foodservice sales | CAD 2.1bn (2024) |

| Capex | CAD 50–70m (2025–27) |

| R&D | CAD 150m (2025) |

| Share returns | CAD 70m (2025) |

Preview = Final Product

Maple Leaf BCG Matrix

The file you're previewing is the exact Maple Leaf BCG Matrix report you'll receive after purchase—no watermarks, no placeholders—just a fully formatted, analysis-ready document designed for strategic clarity and professional presentation.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Unlock Strategic Clarity

The Maple Leaf BCG Matrix preview highlights where key product lines currently sit—showing growth potential, cash generation, and where resources may be leaking—but it’s only a snapshot of strategic opportunity. Purchase the full BCG Matrix for detailed quadrant assignments, underlying market data, and actionable recommendations tailored to each business unit. Get instant access to a ready-to-use Word report plus an Excel summary that speeds decision-making and clarifies where to invest, divest, or defend next.

Stars

Fresh Poultry Segment

Fresh Poultry is a Star: Q3 2025 sales jumped 15.7%, driven by a shift to value‑added retail and foodservice and full output from the London, Ontario plant, lifting segment EBITDA margin to an estimated 9.8% in FY2025.

Sustainable Meats Portfolio

Maple Leaf Foods has branded its Sustainable Meats portfolio—carbon-neutral and RWA (raised without antibiotics)—as a primary growth engine in North America, targeting double-digit CAGR versus ~3–4% CPG growth; management cites 2026 guidance where Sustainable Meats is expected to outpace the broader market.

U.S. Market Expansion

Maple Leaf is rapidly expanding in the U.S.; brand Just Bare surpassed $1 billion in retail sales by Q1 2025, signaling strong product-market fit and pricing power.

This move targets high-growth share gains versus U.S. incumbents, driven by clearer sustainability claims and premium branding, with U.S. revenue up ~35% YoY in 2024.

Ongoing investment in distribution and marketing—targeting a 20% increase in U.S. SKU distribution and +15% ad spend in 2025—is required to convert current momentum into long-term leadership.

Bacon Center of Excellence

Bacon Center of Excellence, Maple Leaf’s Winnipeg facility, hit full business-case benefits in late 2024 and drove double-digit category growth through 2025, with premium bacon volumes up 18% and segment revenue rising 22% year-over-year.

By prioritizing high-margin breakfast and snacking SKUs, the unit lifted Prepared Foods’ margin by 150 basis points and returned payback on the capital investment within 30 months, making it a BCG Matrix star with high market growth and leading share.

- 18% volume growth 2025

- 22% revenue increase 2025

- +150 bps margin impact

- 30-month capital payback

Innovation Pipeline and New SKUs

With over 50 new consumer-relevant innovations launched in 2025, Maple Leaf’s rapid product development is capturing trends in convenience and frozen breakfast, driving mid-single-digit top-line growth forecast of ~4–6% for 2026.

High adoption rates are securing shelf space in high-growth channels; convenience and frozen breakfast now represent an estimated 12% of revenue, up 3 points year-over-year, boosting market relevance and retailer support.

- 50+ new SKUs launched in 2025

- 2026 revenue growth projection: ~4–6%

- Convenience/frozen breakfast ≈12% of revenue (+3 ppt YoY)

- Faster shelf gains in high-growth retail channels

High-Growth Proteins: Fresh Poultry +15.7%, Just Bare $1B+, Bacon +18%—50+ SKUs

Stars: Fresh Poultry, Sustainable Meats, Just Bare and Bacon CoE drive high growth—Fresh Poultry +15.7% Q3 2025, Just Bare $1B+ retail by Q1 2025, Bacon volumes +18% 2025; Sustainable Meats targets double‑digit CAGR vs 3–4% CPG; 50+ SKUs 2025, convenience/frozen breakfast 12% revenue (+3 ppt).

| Metric | 2025 |

|---|---|

| Fresh Poultry sales | +15.7% |

| Just Bare retail | $1.0B+ |

| Bacon vol. | +18% |

| New SKUs | 50+ |

What is included in the product

Comprehensive BCG Matrix review of Maple Leaf’s portfolio with strategic moves for Stars, Cash Cows, Question Marks, and Dogs.

One-page BCG matrix placing each Maple Leaf business unit in a clear quadrant for instant portfolio clarity.

Cash Cows

Prepared Meats Core Brands

The flagship Maple Leaf and Schneiders brands hold ~45–55% combined share of Canada’s deli and prepared meats market (2024 Nielsen data), producing steady EBITDA margins near 12% and roughly CAD 350–400m annual free cash flow in 2024.

With major capital projects finished by end-2024, incremental capex needs are low (projected CAD 50–70m annually 2025–27), so this cash funds dividend increases and services CAD 1.2bn net debt as Maple Leaf shifts to a brand-led CPG model.

Canadian Retail Operations

Maple Leaf Foods holds ~18% share of the Canadian retail CPG meat and prepared foods market (2024), serving major chains like Loblaw, Sobeys and Metro and generating stable EBITDA margins near 12% in 2024.

Canada’s CPG growth averages ~2% annually (2020–24), yet Maple Leaf’s scale and long-term supply contracts drive cash conversion that funds ~CAD 120–150m/year in R&D and supports international Star-category expansion.

Foodservice Distribution Network

Maple Leaf’s Foodservice Distribution Network holds long-term contracts with major Canadian chains, generating high-volume revenue—about CAD 2.1 billion sales in 2024 and ~9% adjusted operating margin—making it a classic Cash Cow in the BCG matrix.

Market is mature, so promotional spend is low (<1.5% of segment sales), keeping margins steady and funding capital needs without equity raises.

These steady margins underpin Maple Leaf’s investment-grade balance sheet through 2026, supporting net debt/EBITDA near 1.8x in 2025.

International Pork Sales (Post-Spin-off)

Post-spin-off (Canada Packers, Dec 2025), Maple Leaf keeps strategic stakes and evergreen supply contracts that deliver steady international pork revenue—about CAD 220m in 2025 export-linked receipts, smoothing exposure to hog-price swings.

These predictable cash flows fund high-margin prepared-food R&D and shareholder returns; management redirected ~CAD 150m in 2025 to innovation and CAD 70m to buybacks/dividends.

- Evergreen supply secures volumes, cuts production volatility

- ~CAD 220m export-linked revenue (2025)

- ~CAD 150m to prepared-food innovation (2025)

- ~CAD 70m returned to shareholders (2025)

Legacy Processing Facilities

Legacy Processing Facilities have been optimized by closing 6 older plants and consolidating production into 4 modern hubs, raising factory utilization to 92% and boosting EBITDA margins on mature lines from 12% (2019) to 21% (2024) under the Fuel for Growth cost cuts.

These lines deliver ~1.2 million tonnes of staple products annually, require <3% capex-to-sales, and contribute ~38% of Maple Leaf’s operating cash flow in FY2024.

- Closed 6 plants, 4 hubs remain

- Utilization 92%

- EBITDA margin up 9 pts to 21%

- ~1.2M tonnes/year output

- Capex-to-sales <3%

- 38% of FY2024 operating cash flow

Maple Leaf: Strong FCF, 1.8x Net Debt, CAD 150m R&D & CAD 70m Returns in 2025

Maple Leaf’s Cash Cows: flagship deli/prepared brands (45–55% category share) and Foodservice network (CAD 2.1bn sales, ~9% adj. op margin) generated CAD 350–400m free cash flow in 2024; capex 2025–27 ~CAD 50–70m supports CAD 1.2bn net debt (net debt/EBITDA ~1.8x) while funding CAD 150m R&D and CAD 70m returns in 2025.

| Metric | 2024/25 |

|---|---|

| Free cash flow | CAD 350–400m (2024) |

| Foodservice sales | CAD 2.1bn (2024) |

| Capex | CAD 50–70m (2025–27) |

| R&D | CAD 150m (2025) |

| Share returns | CAD 70m (2025) |

Preview = Final Product

Maple Leaf BCG Matrix

The file you're previewing is the exact Maple Leaf BCG Matrix report you'll receive after purchase—no watermarks, no placeholders—just a fully formatted, analysis-ready document designed for strategic clarity and professional presentation.