Maple Leaf Porter's Five Forces Analysis

From Overview to Strategy Blueprint

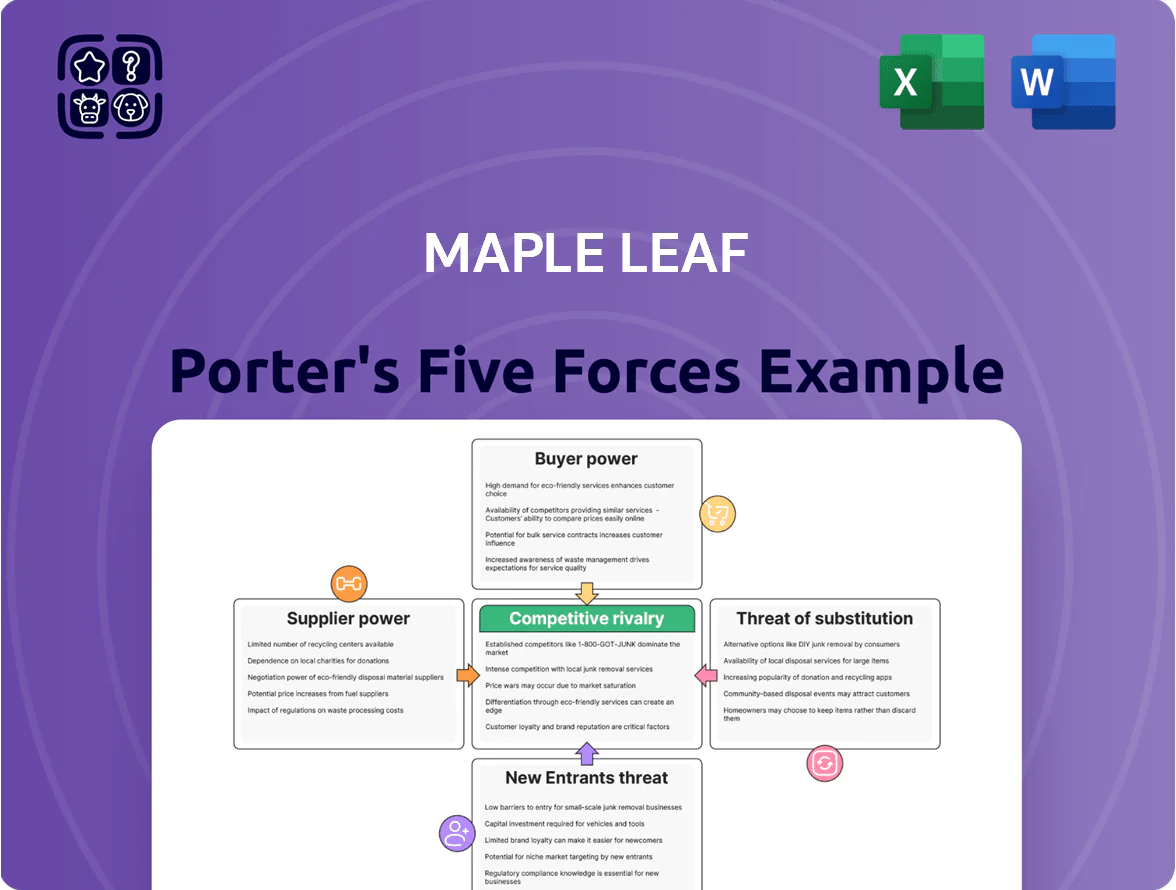

Maple Leaf faces moderate buyer power, margin pressure from large retailers, and steady rivalry among branded and private-label competitors, while supplier leverage and new entrants remain manageable due to scale and distribution advantages.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Maple Leaf’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Commodity Price Volatility

Maple Leaf Foods depends on feed grains and livestock; corn and soybean prices rose ~28% and 22% respectively in 2023, pressuring COGS and margins. Weather, disease outbreaks, and tariffs drive supply shifts the company cannot control, and suppliers can pass through costs during shortages. In 2024 Q3 Maple Leaf reported a 6% YoY increase in input costs, highlighting volatility risk. If commodity-driven inflation persists, gross margin compression will continue.

Livestock Producer Fragmentation

Energy and Utility Costs

Processing plants need heavy energy for refrigeration, cooking and sanitation, so utility firms are key suppliers; Maple Leaf Foods reported energy costs ~4–6% of COGS in 2024.

Canada’s carbon pricing rose to CAD 80/tCO2e by 2025, plus provincial rules, raising energy suppliers’ leverage over margins.

Limited ability to switch providers or self-generate increases supplier power in overheads, pressuring operating margins unless capex for onsite renewables is deployed.

Specialized Packaging Materials

Specialized sustainable packaging suppliers wield strong bargaining power: only about 12 global vendors can meet high-volume, plastic-free specs, and their proprietary tech is key for Maple Leaf to hit its 2030 ESG targets (30% packaging carbon reduction).

Switching suppliers risks six-figure transition costs per line and 2–4 week production downtime, plus retooling CAPEX; that raises supplier leverage over price and contract terms.

- ~12 qualified suppliers worldwide

- 2030 ESG: 30% packaging carbon cut target

- Switch cost: six-figure per line; 2–4 week downtime

- Proprietary tech => limited substitutes, higher prices

Labor Market Dynamics

Moderate supplier power: rising grain, input & labour costs, high packaging switching barriers

Suppliers exert moderate power: commodity grain shocks lifted corn +28% and soy +22% in 2023, Maple Leaf input costs +6% YoY in 2024, energy ~4–6% of COGS, carbon price CAD80/tCO2e by 2025, 12 global packaging suppliers, switching costs six-figure per line and 2–4 week downtime, labour costs +6% FY2024, Canada unemployment 5.7% in 2024.

| Metric | Value |

|---|---|

| Corn change 2023 | +28% |

| Soy change 2023 | +22% |

| Input costs 2024 | +6% YoY |

| Energy % of COGS | 4–6% |

| Carbon price 2025 | CAD80/tCO2e |

| Qualified packaging suppliers | ~12 |

| Switching cost per line | Six-figure; 2–4 wk downtime |

| Labour cost change FY2024 | +6% |

| Canada unemployment 2024 | 5.7% |

What is included in the product

Tailored exclusively for Maple Leaf, this Porter's Five Forces analysis uncovers competitive drivers, supplier and buyer power, entry barriers, substitutes, and emerging threats, with strategic commentary to assess pricing influence and market protection.

A one-sheet Maple Leaf Porter’s Five Forces summary that instantly maps competitive pressure and relieves decision-making friction for fast, board-ready insights.

Customers Bargaining Power

Retail Concentration in Canada

Canada’s grocery market is highly concentrated: Loblaws, Sobeys (Empire), and Metro held about 75% of national market share in 2024, giving them strong leverage over suppliers.

These chains press for lower wholesale prices and better promotional funding; in 2023 retailers captured roughly 60–70% of category margins on private-label growth.

Maple Leaf Foods must sustain favoured listings and promotional support with these buyers to keep shelf space and reach most Canadian shoppers.

Private Label Competition

Retailers like Walmart and Loblaw have expanded private-label meat and plant-based lines, growing private-label share in Canadian protein aisles to ~18% by 2024, squeezing Maple Leaf Foods’ margin recovery and forcing continuous product and cost innovation.

If Maple Leaf’s premium price gap exceeds ~10–15%, procurement teams and value-conscious shoppers shift to cheaper store brands, cutting Maple Leaf volume and pricing power—Maple Leaf saw a 2.3% volume drop in select categories in 2023 when undercut by private labels.

Consumer Price Sensitivity

Consumers’ price sensitivity rose sharply with 2022–24 food inflation; 2024 Statistics Canada data show grocery prices up ~20% vs 2019, prompting trade-downs to cheaper cuts and plant proteins—Maple Leaf Foods (TSX: MFI) faces retailers who refuse input-price pass-throughs.

This forces Maple Leaf to protect margins while keeping shelf prices competitive; NielsenIQ reported 12–18% volume shifts to private labels in 2024, so consumers will defect if price > perceived value.

Foodservice Volume Requirements

- High-volume contracts with price caps

- Switching risk to global suppliers (6% export growth 2024)

- Hospitality margins ~3% in 2024, pushing cost focus

Low Switching Costs for Buyers

Retailers and foodservice buyers face low switching costs for bacon and plant-based burgers, so Maple Leaf must spend more on brand loyalty and differentiation to hold share; in 2024 Canada retail bacon private-label share reached ~40%, raising pricing pressure.

Without clear unique value props, Maple Leaf is exposed to large buyers—Grocery chains like Loblaw and Sobeys accounted for over 60% of Canadian grocery sales in 2024, giving them strong leverage.

- Low switching costs — easy SKU swaps

- Private-label bacon ~40% retail share (2024)

- Top grocers >60% market control (2024)

- Need higher marketing R&D spend to defend share

Grocers’ 75% grip and rising private‑label (18–40%) squeeze Maple Leaf margins

Retailers (Loblaw, Sobeys, Metro) held ~75% Canada grocery share in 2024, pressuring Maple Leaf on price and promotions; private-label protein rose to ~18% (retail) and bacon private-label ~40% (2024), causing category volume shifts of 12–18% to store brands; foodservice contracts cap margins ~<8% and restaurant net margin ~3% (2024), raising buyer leverage.

| Metric | 2024 |

|---|---|

| Top grocers share | ~75% |

| Private-label protein | ~18% |

| Bacon private-label | ~40% |

| Volume shift to PL | 12–18% |

| Foodservice margin cap | <8% |

Same Document Delivered

Maple Leaf Porter's Five Forces Analysis

This preview shows the exact Maple Leaf Porter’s Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups; fully formatted, professionally written, and ready for download and use the moment you buy.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

Maple Leaf faces moderate buyer power, margin pressure from large retailers, and steady rivalry among branded and private-label competitors, while supplier leverage and new entrants remain manageable due to scale and distribution advantages.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Maple Leaf’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Commodity Price Volatility

Maple Leaf Foods depends on feed grains and livestock; corn and soybean prices rose ~28% and 22% respectively in 2023, pressuring COGS and margins. Weather, disease outbreaks, and tariffs drive supply shifts the company cannot control, and suppliers can pass through costs during shortages. In 2024 Q3 Maple Leaf reported a 6% YoY increase in input costs, highlighting volatility risk. If commodity-driven inflation persists, gross margin compression will continue.

Livestock Producer Fragmentation

Energy and Utility Costs

Processing plants need heavy energy for refrigeration, cooking and sanitation, so utility firms are key suppliers; Maple Leaf Foods reported energy costs ~4–6% of COGS in 2024.

Canada’s carbon pricing rose to CAD 80/tCO2e by 2025, plus provincial rules, raising energy suppliers’ leverage over margins.

Limited ability to switch providers or self-generate increases supplier power in overheads, pressuring operating margins unless capex for onsite renewables is deployed.

Specialized Packaging Materials

Specialized sustainable packaging suppliers wield strong bargaining power: only about 12 global vendors can meet high-volume, plastic-free specs, and their proprietary tech is key for Maple Leaf to hit its 2030 ESG targets (30% packaging carbon reduction).

Switching suppliers risks six-figure transition costs per line and 2–4 week production downtime, plus retooling CAPEX; that raises supplier leverage over price and contract terms.

- ~12 qualified suppliers worldwide

- 2030 ESG: 30% packaging carbon cut target

- Switch cost: six-figure per line; 2–4 week downtime

- Proprietary tech => limited substitutes, higher prices

Labor Market Dynamics

Moderate supplier power: rising grain, input & labour costs, high packaging switching barriers

Suppliers exert moderate power: commodity grain shocks lifted corn +28% and soy +22% in 2023, Maple Leaf input costs +6% YoY in 2024, energy ~4–6% of COGS, carbon price CAD80/tCO2e by 2025, 12 global packaging suppliers, switching costs six-figure per line and 2–4 week downtime, labour costs +6% FY2024, Canada unemployment 5.7% in 2024.

| Metric | Value |

|---|---|

| Corn change 2023 | +28% |

| Soy change 2023 | +22% |

| Input costs 2024 | +6% YoY |

| Energy % of COGS | 4–6% |

| Carbon price 2025 | CAD80/tCO2e |

| Qualified packaging suppliers | ~12 |

| Switching cost per line | Six-figure; 2–4 wk downtime |

| Labour cost change FY2024 | +6% |

| Canada unemployment 2024 | 5.7% |

What is included in the product

Tailored exclusively for Maple Leaf, this Porter's Five Forces analysis uncovers competitive drivers, supplier and buyer power, entry barriers, substitutes, and emerging threats, with strategic commentary to assess pricing influence and market protection.

A one-sheet Maple Leaf Porter’s Five Forces summary that instantly maps competitive pressure and relieves decision-making friction for fast, board-ready insights.

Customers Bargaining Power

Retail Concentration in Canada

Canada’s grocery market is highly concentrated: Loblaws, Sobeys (Empire), and Metro held about 75% of national market share in 2024, giving them strong leverage over suppliers.

These chains press for lower wholesale prices and better promotional funding; in 2023 retailers captured roughly 60–70% of category margins on private-label growth.

Maple Leaf Foods must sustain favoured listings and promotional support with these buyers to keep shelf space and reach most Canadian shoppers.

Private Label Competition

Retailers like Walmart and Loblaw have expanded private-label meat and plant-based lines, growing private-label share in Canadian protein aisles to ~18% by 2024, squeezing Maple Leaf Foods’ margin recovery and forcing continuous product and cost innovation.

If Maple Leaf’s premium price gap exceeds ~10–15%, procurement teams and value-conscious shoppers shift to cheaper store brands, cutting Maple Leaf volume and pricing power—Maple Leaf saw a 2.3% volume drop in select categories in 2023 when undercut by private labels.

Consumer Price Sensitivity

Consumers’ price sensitivity rose sharply with 2022–24 food inflation; 2024 Statistics Canada data show grocery prices up ~20% vs 2019, prompting trade-downs to cheaper cuts and plant proteins—Maple Leaf Foods (TSX: MFI) faces retailers who refuse input-price pass-throughs.

This forces Maple Leaf to protect margins while keeping shelf prices competitive; NielsenIQ reported 12–18% volume shifts to private labels in 2024, so consumers will defect if price > perceived value.

Foodservice Volume Requirements

- High-volume contracts with price caps

- Switching risk to global suppliers (6% export growth 2024)

- Hospitality margins ~3% in 2024, pushing cost focus

Low Switching Costs for Buyers

Retailers and foodservice buyers face low switching costs for bacon and plant-based burgers, so Maple Leaf must spend more on brand loyalty and differentiation to hold share; in 2024 Canada retail bacon private-label share reached ~40%, raising pricing pressure.

Without clear unique value props, Maple Leaf is exposed to large buyers—Grocery chains like Loblaw and Sobeys accounted for over 60% of Canadian grocery sales in 2024, giving them strong leverage.

- Low switching costs — easy SKU swaps

- Private-label bacon ~40% retail share (2024)

- Top grocers >60% market control (2024)

- Need higher marketing R&D spend to defend share

Grocers’ 75% grip and rising private‑label (18–40%) squeeze Maple Leaf margins

Retailers (Loblaw, Sobeys, Metro) held ~75% Canada grocery share in 2024, pressuring Maple Leaf on price and promotions; private-label protein rose to ~18% (retail) and bacon private-label ~40% (2024), causing category volume shifts of 12–18% to store brands; foodservice contracts cap margins ~<8% and restaurant net margin ~3% (2024), raising buyer leverage.

| Metric | 2024 |

|---|---|

| Top grocers share | ~75% |

| Private-label protein | ~18% |

| Bacon private-label | ~40% |

| Volume shift to PL | 12–18% |

| Foodservice margin cap | <8% |

Same Document Delivered

Maple Leaf Porter's Five Forces Analysis

This preview shows the exact Maple Leaf Porter’s Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups; fully formatted, professionally written, and ready for download and use the moment you buy.