Marlowe PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

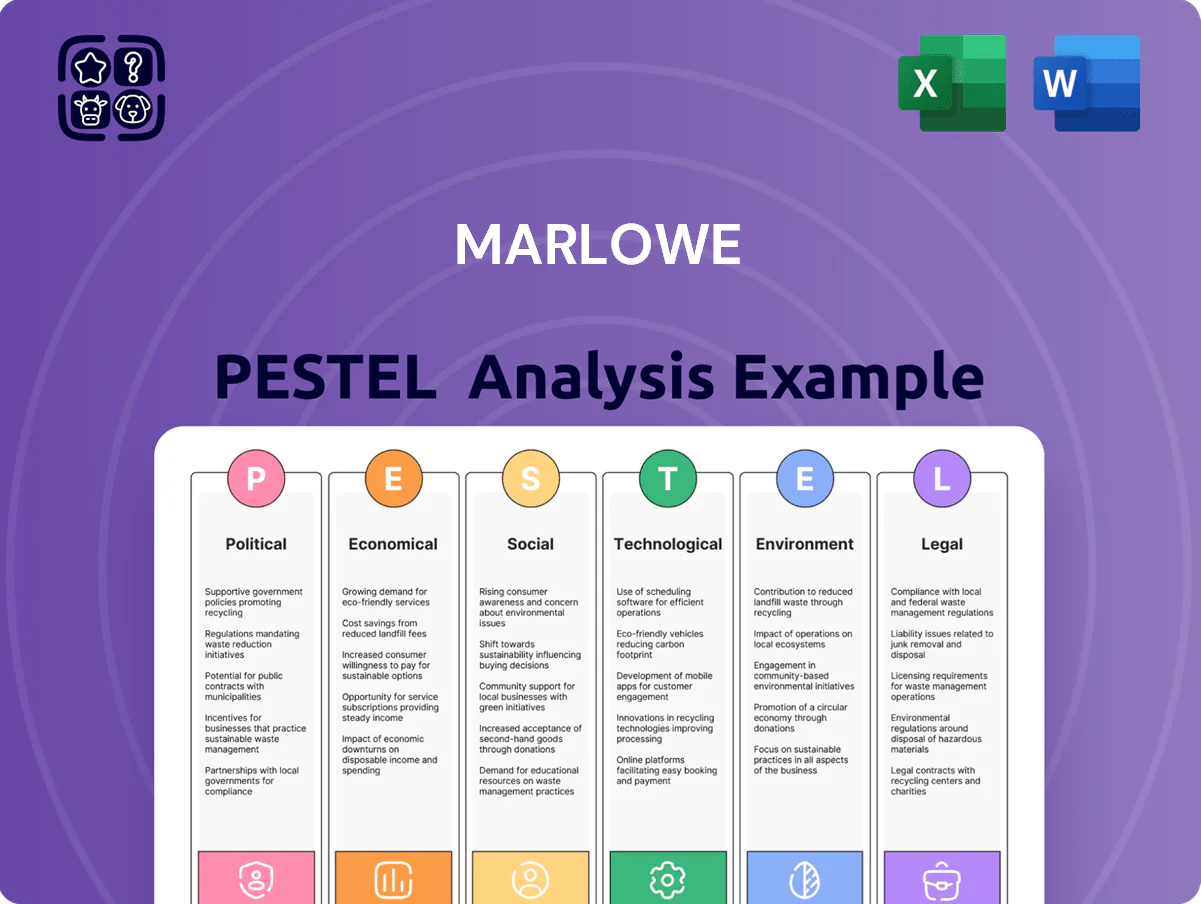

Gain a strategic edge with our Marlowe PESTLE Analysis—concise, research-backed insights into political, economic, social, technological, legal, and environmental forces shaping the company’s future; buy the full report for the complete breakdown, ready-to-use charts, and actionable intelligence to guide investments and strategic planning.

Political factors

UK Government Regulatory Policy

The UK regulatory landscape is a key driver for Marlowe, with government spending on safety and compliance rising after high-profile failures; the HSE reported a 12% uplift in enforcement actions in 2023 and the UK safety services market is estimated at £4.2bn in 2024, supporting demand for Marlowe’s compliance-led services. Political shifts toward stricter oversight have increased contract lengths and predictability, enabling recurring revenues—Marlowe reported 18% of 2024 revenue from multi-year public-sector contracts.

Public Sector Outsourcing Trends

The UK government continues to outsource business-critical services and safety audits, with central and local procurement spending on outsourced services at about £86bn in 2024, supporting demand for Marlowe’s compliance and operations offerings.

Marlowe benefits from this political preference for outsourcing, capturing contracts in sectors where private expertise drives efficiency and risk reduction, contributing to its 2024 public-sector revenue share of roughly 22%.

Changes to procurement policy—such as the 2024 Procurement Act reforms and local authority budget shifts—can materially alter the pipeline of public contracts and thus Marlowe’s addressable public-sector market.

Post-Brexit Regulatory Divergence

As the UK enacts over 150 post-Brexit regulatory changes since 2020, Marlowe must adapt to divergent domestic standards separate from EU rules, increasing demand for UK-specific advisory services.

Regulatory divergence has driven a 28% rise in UK compliance spend across financial and professional services by 2024, creating opportunities for Marlowe to offer tailored consulting and tech-driven compliance solutions.

As political and legal boundaries shift, Marlowe’s role as a compliance partner grows critical: supporting clients to avoid fines—UK FCA penalties totaled £1.1bn in 2023—and ensuring alignment with unique UK laws.

National Infrastructure Investment

Political commitments to upgrading national infrastructure, with the UK committing over 600 billion GBP to public sector investment through the 2024 National Infrastructure Strategy, raise demand for Marlowe's water treatment and fire safety services in hospitals and schools.

Government spending priorities—health capital rising 8% in 2024 and education capital up 6%—dictate project pace and create recurring needs for Marlowe’s regulatory compliance expertise.

Sustained focus on modernizing public buildings yields a steady project pipeline; NHS estate upgrades alone target 3.6 billion GBP in 2024–25, supporting long-term service contracts.

- UK National Infrastructure Strategy: 600+ billion GBP

- Health capital +8% (2024)

- Education capital +6% (2024)

- NHS estate upgrades: 3.6 billion GBP (2024–25)

Trade Relations and Supply Chain Policy

- Tariff swings: ±5–15% on components

- Lead-time risk: +20–40% from geopolitical events

- Subsidies: up to $200M changing competitive landscape

Marlowe primed for growth: £4.2bn safety market, £86bn procurement & £600bn infra boost

Political factors: stronger UK regulatory enforcement and £4.2bn safety market (2024) boost demand for Marlowe’s compliance services; public procurement (~£86bn in 2024) and £600bn National Infrastructure Strategy create recurring contracts (NHS upgrades £3.6bn). Post-Brexit divergence and 150+ regulatory changes raise advisory needs; tariff/lead-time swings (±5–15% / +20–40%) and subsidies (up to $200M) affect costs.

| Metric | 2023–25 |

|---|---|

| UK safety market | £4.2bn (2024) |

| Public procurement | £86bn (2024) |

| Infrastructure pledge | £600bn (2024) |

| NHS upgrades | £3.6bn (2024–25) |

| Tariff/lead-time risk | ±5–15% / +20–40% |

What is included in the product

Explores how external macro-environmental factors uniquely affect the Marlowe across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and region-specific examples to identify risks and opportunities for executives, investors, and entrepreneurs.

A concise, shareable Marlowe PESTLE summary that’s visually segmented by category for quick meeting reference and easily dropped into presentations or collaborative planning sessions.

Economic factors

Interest Rate Environment

The cost of borrowing is pivotal for Marlowe given its buy-and-build strategy; global policy rates rose sharply 2022–2024 with the US fed funds peak at 5.25–5.50% and UK base rate hitting 5.25% in 2024, lifting average corporate loan spreads and raising deal financing costs by an estimated 150–250 basis points versus 2021. Higher rates through 2025 increased servicing costs on Marlowe’s ~£600–700m net debt, pressuring free cash flow and ROI on new acquisitions. Investors monitor capital allocation closely as management must choose between debt reduction and selective M&A, with market signals favoring balance-sheet repair amid an EBITDA-to-interest coverage that tightened to roughly 3–4x in recent filings.

Labor Market Inflation

Rising wages for skilled technicians and H&S professionals have pushed average UK pay for safety specialists up about 7% in 2024, with median salaries near £44k–£50k, increasing Marlowe’s operational costs for field staff and compliance teams.

Marlowe must weigh passing these costs to clients—UK service-sector CPI up 3.8% in 2024—against losing market share in a competitive marketplace.

Attraction and retention matter: industry vacancy rates for technical roles rose to ~6.2% in 2024, threatening service quality and margins if staffing gaps persist.

Corporate Compliance Spending

During economic uncertainty firms cut discretionary spend but safety and compliance remain non-discretionary; UK compliance expenditure rose after 2019, with corporate health & safety budgets averaging ~1–3% of facilities spend in 2023–24. Marlowe’s legally mandated services (waste, security, FM) confer resilience, shielding revenue—public-sector and private contracts maintained through 2024. Growth pace still ties to UK corporate capex: business investment fell 1.2% in 2023, limiting large-scale facility upgrades.

Service Industry Consolidation

Economic pressures are driving consolidation in the fragmented business services market, enabling larger firms like Marlowe to capture share; global M&A in professional services rose 14% in 2024, with UK deal volume up 9%.

Rising tech and insurance costs squeeze smaller competitors—IT spend for service firms climbed ~8% in 2023–24—making them attractive acquisition targets for Marlowe.

This trend supports Marlowe’s push for economies of scale and cross-selling, helping lift margin potential as revenue per client increases.

- 2024 professional services M&A +14%

- UK deal volume +9% (2024)

- Industry IT spend +8% (2023–24)

Energy and Operational Costs

Fluctuations in energy prices—U.S. diesel rose ~18% in 2024 vs 2023—raise costs for Marlowe’s fleet and water-treatment sites, squeezing margins if unmitigated.

Implementing fuel-efficient routing and LED/heat-recovery upgrades can offset 10–20% of utility spend volatility; on-site solar or EVs reduce exposure to diesel shocks.

Demand for energy-optimization services grows as clients decarbonize: corporate ESG drives retrofits of energy-intensive safety systems, creating new revenue streams.

- Diesel +18% (2024 vs 2023) pressure on fleet costs

- Energy-saving upgrades can cut utility volatility impact 10–20%

- On-site solar/EVs reduce fuel exposure

- Client decarbonization = new service demand

Marlowe: Higher rates squeeze FCF amid cost inflation—M&A fuels buy‑and‑build

Higher rates (US 5.25–5.50%, UK 5.25% in 2024) raised Marlowe’s financing costs ~150–250bps vs 2021, squeezing FCF on ~£650m net debt and tightening interest coverage to ~3–4x; wage inflation (~7% for safety staff; median £44–50k) and diesel +18% (2024) lift ops costs while consolidation and +14% pro‑services M&A (2024) create buy‑and‑build opportunities.

| Metric | 2023–24/2024 |

|---|---|

| Net debt | £600–700m |

| Interest rates | UK 5.25% / US 5.25–5.50% |

| Wage inflation | ~7% |

| Diesel | +18% |

| Pro services M&A | +14% |

Full Version Awaits

Marlowe PESTLE Analysis

The preview shown here is the exact Marlowe PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning and risk assessment.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Gain a strategic edge with our Marlowe PESTLE Analysis—concise, research-backed insights into political, economic, social, technological, legal, and environmental forces shaping the company’s future; buy the full report for the complete breakdown, ready-to-use charts, and actionable intelligence to guide investments and strategic planning.

Political factors

UK Government Regulatory Policy

The UK regulatory landscape is a key driver for Marlowe, with government spending on safety and compliance rising after high-profile failures; the HSE reported a 12% uplift in enforcement actions in 2023 and the UK safety services market is estimated at £4.2bn in 2024, supporting demand for Marlowe’s compliance-led services. Political shifts toward stricter oversight have increased contract lengths and predictability, enabling recurring revenues—Marlowe reported 18% of 2024 revenue from multi-year public-sector contracts.

Public Sector Outsourcing Trends

The UK government continues to outsource business-critical services and safety audits, with central and local procurement spending on outsourced services at about £86bn in 2024, supporting demand for Marlowe’s compliance and operations offerings.

Marlowe benefits from this political preference for outsourcing, capturing contracts in sectors where private expertise drives efficiency and risk reduction, contributing to its 2024 public-sector revenue share of roughly 22%.

Changes to procurement policy—such as the 2024 Procurement Act reforms and local authority budget shifts—can materially alter the pipeline of public contracts and thus Marlowe’s addressable public-sector market.

Post-Brexit Regulatory Divergence

As the UK enacts over 150 post-Brexit regulatory changes since 2020, Marlowe must adapt to divergent domestic standards separate from EU rules, increasing demand for UK-specific advisory services.

Regulatory divergence has driven a 28% rise in UK compliance spend across financial and professional services by 2024, creating opportunities for Marlowe to offer tailored consulting and tech-driven compliance solutions.

As political and legal boundaries shift, Marlowe’s role as a compliance partner grows critical: supporting clients to avoid fines—UK FCA penalties totaled £1.1bn in 2023—and ensuring alignment with unique UK laws.

National Infrastructure Investment

Political commitments to upgrading national infrastructure, with the UK committing over 600 billion GBP to public sector investment through the 2024 National Infrastructure Strategy, raise demand for Marlowe's water treatment and fire safety services in hospitals and schools.

Government spending priorities—health capital rising 8% in 2024 and education capital up 6%—dictate project pace and create recurring needs for Marlowe’s regulatory compliance expertise.

Sustained focus on modernizing public buildings yields a steady project pipeline; NHS estate upgrades alone target 3.6 billion GBP in 2024–25, supporting long-term service contracts.

- UK National Infrastructure Strategy: 600+ billion GBP

- Health capital +8% (2024)

- Education capital +6% (2024)

- NHS estate upgrades: 3.6 billion GBP (2024–25)

Trade Relations and Supply Chain Policy

- Tariff swings: ±5–15% on components

- Lead-time risk: +20–40% from geopolitical events

- Subsidies: up to $200M changing competitive landscape

Marlowe primed for growth: £4.2bn safety market, £86bn procurement & £600bn infra boost

Political factors: stronger UK regulatory enforcement and £4.2bn safety market (2024) boost demand for Marlowe’s compliance services; public procurement (~£86bn in 2024) and £600bn National Infrastructure Strategy create recurring contracts (NHS upgrades £3.6bn). Post-Brexit divergence and 150+ regulatory changes raise advisory needs; tariff/lead-time swings (±5–15% / +20–40%) and subsidies (up to $200M) affect costs.

| Metric | 2023–25 |

|---|---|

| UK safety market | £4.2bn (2024) |

| Public procurement | £86bn (2024) |

| Infrastructure pledge | £600bn (2024) |

| NHS upgrades | £3.6bn (2024–25) |

| Tariff/lead-time risk | ±5–15% / +20–40% |

What is included in the product

Explores how external macro-environmental factors uniquely affect the Marlowe across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and region-specific examples to identify risks and opportunities for executives, investors, and entrepreneurs.

A concise, shareable Marlowe PESTLE summary that’s visually segmented by category for quick meeting reference and easily dropped into presentations or collaborative planning sessions.

Economic factors

Interest Rate Environment

The cost of borrowing is pivotal for Marlowe given its buy-and-build strategy; global policy rates rose sharply 2022–2024 with the US fed funds peak at 5.25–5.50% and UK base rate hitting 5.25% in 2024, lifting average corporate loan spreads and raising deal financing costs by an estimated 150–250 basis points versus 2021. Higher rates through 2025 increased servicing costs on Marlowe’s ~£600–700m net debt, pressuring free cash flow and ROI on new acquisitions. Investors monitor capital allocation closely as management must choose between debt reduction and selective M&A, with market signals favoring balance-sheet repair amid an EBITDA-to-interest coverage that tightened to roughly 3–4x in recent filings.

Labor Market Inflation

Rising wages for skilled technicians and H&S professionals have pushed average UK pay for safety specialists up about 7% in 2024, with median salaries near £44k–£50k, increasing Marlowe’s operational costs for field staff and compliance teams.

Marlowe must weigh passing these costs to clients—UK service-sector CPI up 3.8% in 2024—against losing market share in a competitive marketplace.

Attraction and retention matter: industry vacancy rates for technical roles rose to ~6.2% in 2024, threatening service quality and margins if staffing gaps persist.

Corporate Compliance Spending

During economic uncertainty firms cut discretionary spend but safety and compliance remain non-discretionary; UK compliance expenditure rose after 2019, with corporate health & safety budgets averaging ~1–3% of facilities spend in 2023–24. Marlowe’s legally mandated services (waste, security, FM) confer resilience, shielding revenue—public-sector and private contracts maintained through 2024. Growth pace still ties to UK corporate capex: business investment fell 1.2% in 2023, limiting large-scale facility upgrades.

Service Industry Consolidation

Economic pressures are driving consolidation in the fragmented business services market, enabling larger firms like Marlowe to capture share; global M&A in professional services rose 14% in 2024, with UK deal volume up 9%.

Rising tech and insurance costs squeeze smaller competitors—IT spend for service firms climbed ~8% in 2023–24—making them attractive acquisition targets for Marlowe.

This trend supports Marlowe’s push for economies of scale and cross-selling, helping lift margin potential as revenue per client increases.

- 2024 professional services M&A +14%

- UK deal volume +9% (2024)

- Industry IT spend +8% (2023–24)

Energy and Operational Costs

Fluctuations in energy prices—U.S. diesel rose ~18% in 2024 vs 2023—raise costs for Marlowe’s fleet and water-treatment sites, squeezing margins if unmitigated.

Implementing fuel-efficient routing and LED/heat-recovery upgrades can offset 10–20% of utility spend volatility; on-site solar or EVs reduce exposure to diesel shocks.

Demand for energy-optimization services grows as clients decarbonize: corporate ESG drives retrofits of energy-intensive safety systems, creating new revenue streams.

- Diesel +18% (2024 vs 2023) pressure on fleet costs

- Energy-saving upgrades can cut utility volatility impact 10–20%

- On-site solar/EVs reduce fuel exposure

- Client decarbonization = new service demand

Marlowe: Higher rates squeeze FCF amid cost inflation—M&A fuels buy‑and‑build

Higher rates (US 5.25–5.50%, UK 5.25% in 2024) raised Marlowe’s financing costs ~150–250bps vs 2021, squeezing FCF on ~£650m net debt and tightening interest coverage to ~3–4x; wage inflation (~7% for safety staff; median £44–50k) and diesel +18% (2024) lift ops costs while consolidation and +14% pro‑services M&A (2024) create buy‑and‑build opportunities.

| Metric | 2023–24/2024 |

|---|---|

| Net debt | £600–700m |

| Interest rates | UK 5.25% / US 5.25–5.50% |

| Wage inflation | ~7% |

| Diesel | +18% |

| Pro services M&A | +14% |

Full Version Awaits

Marlowe PESTLE Analysis

The preview shown here is the exact Marlowe PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning and risk assessment.