Martinrea Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

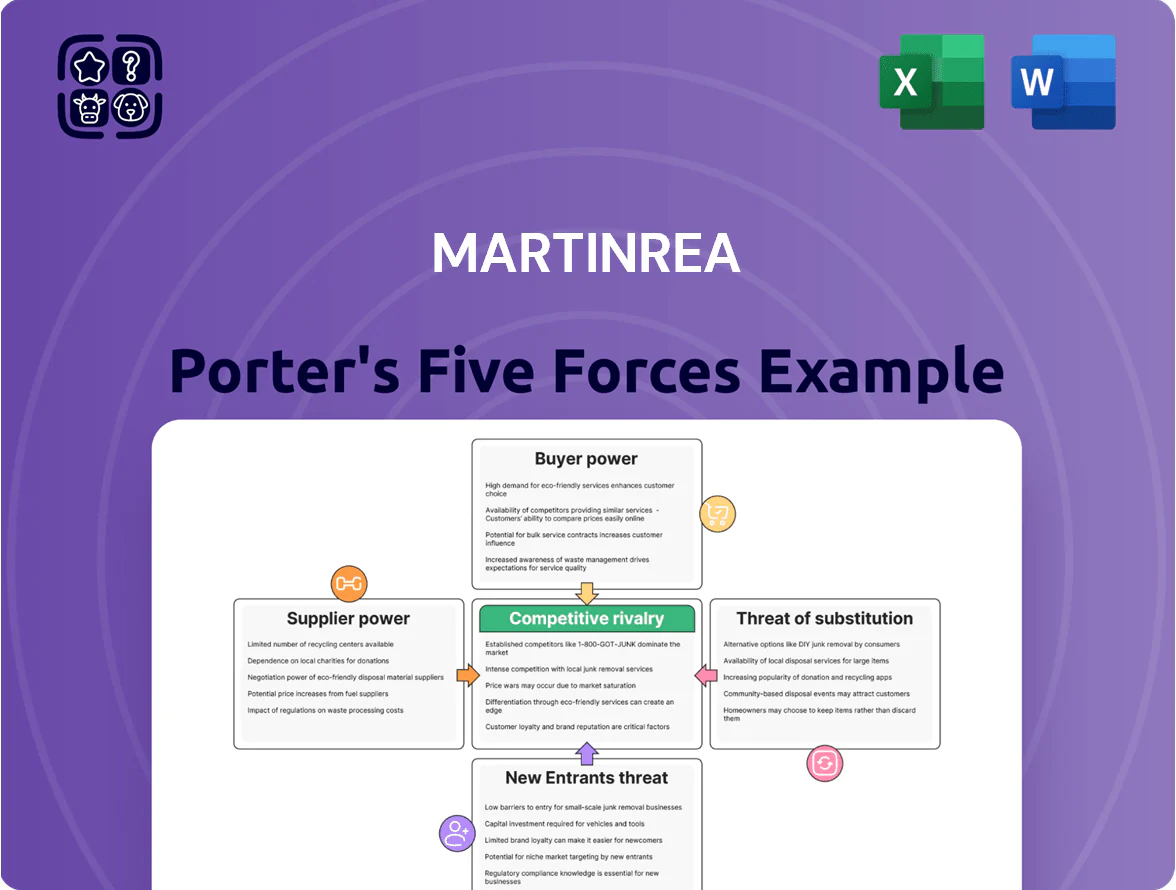

Martinrea faces moderate supplier power and intense buyer pressure amid cyclical auto demand, with technology shifts raising substitute and entrant risks; competitive rivalry remains high across components and geographies.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Martinrea’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Raw Material Commodity Price Sensitivity

Martinrea depends heavily on steel and aluminum, which saw LME aluminum rise ~12% and hot-rolled coil steel up ~9% in 2024, so raw-material swings hit margins directly.

Index-based pricing and OEM pass-throughs cushion long-term exposure, but 30–90 day lag in adjustments can cut quarterly gross margin by 1–3 percentage points.

Primary-metal suppliers hold leverage because their materials are critical for automotive lightweighting and limited by concentrated global smelting capacity.

Energy and Utility Cost Fluctuations

The energy-intensive aluminum casting and metal forming at Martinrea makes the firm highly sensitive to electricity and natural gas price swings; for example, industrial electricity rates in Ontario rose ~8% in 2023–2024 and U.S. industrial natural gas averages moved between $3.50–$6.00/MMBtu in 2024, directly impacting COGS. Suppliers in the energy sector hold moderate bargaining power since industrial rates are often regulated or limited by regional grid capacity, reducing pure market leverage. By late 2025, contracts and cost models grew more complex as Martinrea negotiates green-energy premiums and renewable energy credits—corporate PPAs now cover ~12–20% of industrial demand in North America, raising short-term costs but lowering long-term price volatility.

Specialized Tooling and Equipment Providers

Suppliers of specialized tooling and high-tech machine tools exert strong leverage over Martinrea because their equipment is is critical to meet OEM specs for advanced manufacturing and fluid management systems.

The global market for precision machine tools is concentrated: the top 10 suppliers held about 62% of revenues in 2024, raising Martinrea’s dependency and bargaining costs.

This concentration can push CAPEX higher—Martinrea reported capital expenditures of US$172m in 2024—making supplier pricing and lead times key to margins.

Tier 2 and Tier 3 Component Dependencies

Martinrea relies on many Tier 2/3 suppliers for sub-components and specialized chemical coatings; in 2024 about 18% of its parts spend was with suppliers below Tier 1, raising concentration risk.

Disruptions in these tiers can halt assembly lines, giving niche suppliers tactical bargaining power during shortages—Martinrea reported a 7% production hit from supplier delays in 2023.

Active supplier monitoring, dual-sourcing and inventory buffers are required to protect delivery schedules to OEMs and avoid penalties.

- 18% parts spend with Tier 2/3 (2024)

- 7% production impact from delays (2023)

- Mitigations: dual-sourcing, buffers, supplier audits

Labor Market Dynamics and Skilled Trades

The scarcity of skilled labor for specialized manufacturing roles is a binding constraint for Martinrea; as EV architectures rise, demand for battery, powertrain and software-tuned technicians and engineers grew ~22% industry-wide in 2023–2024, pushing wage premiums 8–15% and raising production costs; specialized recruiters and unions thus hold greater pricing power, increasing OEM supplier margins and capitalizing hiring bottlenecks.

- Skilled labor shortage binds capacity

- EV-related roles up ~22% (2023–24)

- Wage premiums rose 8–15%

- Recruiters/unions gain negotiation leverage

Rising metal, tool and labor costs squeeze Martinrea margins and boost supplier power

Suppliers hold moderate-to-high bargaining power for Martinrea: raw metals (aluminum up ~12% in 2024) and concentrated precision-tool markets (top 10 = 62% revenues in 2024) lift input and CAPEX costs; Tier‑2/3 concentration (18% spend) and a 7% 2023 production hit amplify tactical power; skilled‑labor shortages (EV roles +22% in 2023–24) raise wages 8–15%, further pressuring margins.

| Metric | Value |

|---|---|

| Aluminum price move (2024) | +12% |

| Top10 machine‑tool share (2024) | 62% |

| Tier2/3 spend (2024) | 18% |

| Production hit (2023) | 7% |

| EV role demand (2023–24) | +22% |

| Wage premium | 8–15% |

What is included in the product

Tailored Porter's Five Forces analysis for Martinrea that uncovers competitive drivers, supplier and buyer power, entry barriers, substitutes, and disruptive threats, with actionable strategic insights to inform investor and management decisions.

A concise Porter's Five Forces snapshot for Martinrea—clarifies competitive pressures at a glance to speed strategic decisions.

Customers Bargaining Power

Concentration of Major Global OEMs

Strenuous Annual Price Reduction Demands

Automotive OEMs demand annual productivity gains and price cuts—often 1–3% yearly—pressuring Martinrea's margins and forcing continuous innovation and cost-savings; this contributed to the industry average supplier margin compression to roughly 6–8% in 2024. OEMs' audit rights and cost-transparency demands amplify customer power, enabling them to verify supplier cost models and extract further concessions, so Martinrea must prioritize automation and lean projects to protect EBIT.

Rigorous Quality and Safety Certifications

Customers set technical benchmarks that give them strong leverage over Martinrea; global OEMs demand IATF 16949 automotive quality certification and strict PPAP (production part approval process) compliance, and noncompliance can drop a supplier from approved lists within months.

Failing standards risks costly recalls—automotive recalls cost OEMs and suppliers an average $2,000–$10,000 per vehicle in direct charges in recent large recalls—and can exclude Martinrea from contracts worth millions.

This buyer-driven dynamic makes excellence the baseline: OEMs can demand defect rates under 50 PPM (parts per million) and warranty exposure limits, keeping bargaining power firmly with customers.

Switching Costs and Long-Term Program Ties

OEMs hold strong bargaining power, but high mid-program switching costs give Martinrea defensive stability; re-tooling a platform often costs tens to hundreds of millions and validation can add months and >$10m per component, so OEMs avoid changes mid-cycle.

This integration creates mutual dependency that tempers customer leverage across a model lifecycle, reducing effective price pressure and securing recurring volume for Martinrea.

- Re-tooling: $10–$200M per platform

- Validation: >$10M per complex component

- Time cost: months to >1 year

- Result: lower mid-cycle switching, steadier margins

Threat of OEM Vertical Integration

OEMs are increasingly evaluating backward integration for EV parts—Ford, GM and Tesla disclosed in 2024 plans or pilots to internalize battery enclosures or structural castings to cut costs; OEM vertical integration can shave supplier spend by 5–15% per part based on 2023 supplier margin benchmarks.

For Martinrea this raises pricing pressure; the company must show cost advantages (targeting sub-10% supplier margin) and proprietary tech—its 2024 R&D spend was US$61m—to keep OEMs from internalizing.

OEM-Driven Revenue (55–65%); High Switching Costs Shield Margins Amid 1–3% Price Pressure

OEMs (GM, Ford, Stellantis) held ~55–65% of Martinrea 2024 sales, giving them strong price and spec leverage; annual OEM price demands (~1–3%) and supplier margin compression (industry 6–8% in 2024) squeeze EBIT, while high mid-program switching costs (re-tooling $10–$200M; validation >$10M; months–>1yr) provide defensive stability; 2024 R&D was US$61m.

| Metric | Value |

|---|---|

| Top OEM share | 55–65% |

| Supplier margin (industry) | 6–8% |

| Annual OEM price cuts | 1–3% |

| Re-tooling | $10–$200M |

| Validation per component | >$10M |

| 2024 R&D | US$61m |

Preview Before You Purchase

Martinrea Porter's Five Forces Analysis

This preview shows the exact Martinrea Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders, no mockups.

The document displayed here is the full, professionally formatted analysis ready for download and use the moment you buy.

You’re previewing the final version: the same deliverable will be available to you instantly after payment, fully ready for your needs.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

Martinrea faces moderate supplier power and intense buyer pressure amid cyclical auto demand, with technology shifts raising substitute and entrant risks; competitive rivalry remains high across components and geographies.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Martinrea’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Raw Material Commodity Price Sensitivity

Martinrea depends heavily on steel and aluminum, which saw LME aluminum rise ~12% and hot-rolled coil steel up ~9% in 2024, so raw-material swings hit margins directly.

Index-based pricing and OEM pass-throughs cushion long-term exposure, but 30–90 day lag in adjustments can cut quarterly gross margin by 1–3 percentage points.

Primary-metal suppliers hold leverage because their materials are critical for automotive lightweighting and limited by concentrated global smelting capacity.

Energy and Utility Cost Fluctuations

The energy-intensive aluminum casting and metal forming at Martinrea makes the firm highly sensitive to electricity and natural gas price swings; for example, industrial electricity rates in Ontario rose ~8% in 2023–2024 and U.S. industrial natural gas averages moved between $3.50–$6.00/MMBtu in 2024, directly impacting COGS. Suppliers in the energy sector hold moderate bargaining power since industrial rates are often regulated or limited by regional grid capacity, reducing pure market leverage. By late 2025, contracts and cost models grew more complex as Martinrea negotiates green-energy premiums and renewable energy credits—corporate PPAs now cover ~12–20% of industrial demand in North America, raising short-term costs but lowering long-term price volatility.

Specialized Tooling and Equipment Providers

Suppliers of specialized tooling and high-tech machine tools exert strong leverage over Martinrea because their equipment is is critical to meet OEM specs for advanced manufacturing and fluid management systems.

The global market for precision machine tools is concentrated: the top 10 suppliers held about 62% of revenues in 2024, raising Martinrea’s dependency and bargaining costs.

This concentration can push CAPEX higher—Martinrea reported capital expenditures of US$172m in 2024—making supplier pricing and lead times key to margins.

Tier 2 and Tier 3 Component Dependencies

Martinrea relies on many Tier 2/3 suppliers for sub-components and specialized chemical coatings; in 2024 about 18% of its parts spend was with suppliers below Tier 1, raising concentration risk.

Disruptions in these tiers can halt assembly lines, giving niche suppliers tactical bargaining power during shortages—Martinrea reported a 7% production hit from supplier delays in 2023.

Active supplier monitoring, dual-sourcing and inventory buffers are required to protect delivery schedules to OEMs and avoid penalties.

- 18% parts spend with Tier 2/3 (2024)

- 7% production impact from delays (2023)

- Mitigations: dual-sourcing, buffers, supplier audits

Labor Market Dynamics and Skilled Trades

The scarcity of skilled labor for specialized manufacturing roles is a binding constraint for Martinrea; as EV architectures rise, demand for battery, powertrain and software-tuned technicians and engineers grew ~22% industry-wide in 2023–2024, pushing wage premiums 8–15% and raising production costs; specialized recruiters and unions thus hold greater pricing power, increasing OEM supplier margins and capitalizing hiring bottlenecks.

- Skilled labor shortage binds capacity

- EV-related roles up ~22% (2023–24)

- Wage premiums rose 8–15%

- Recruiters/unions gain negotiation leverage

Rising metal, tool and labor costs squeeze Martinrea margins and boost supplier power

Suppliers hold moderate-to-high bargaining power for Martinrea: raw metals (aluminum up ~12% in 2024) and concentrated precision-tool markets (top 10 = 62% revenues in 2024) lift input and CAPEX costs; Tier‑2/3 concentration (18% spend) and a 7% 2023 production hit amplify tactical power; skilled‑labor shortages (EV roles +22% in 2023–24) raise wages 8–15%, further pressuring margins.

| Metric | Value |

|---|---|

| Aluminum price move (2024) | +12% |

| Top10 machine‑tool share (2024) | 62% |

| Tier2/3 spend (2024) | 18% |

| Production hit (2023) | 7% |

| EV role demand (2023–24) | +22% |

| Wage premium | 8–15% |

What is included in the product

Tailored Porter's Five Forces analysis for Martinrea that uncovers competitive drivers, supplier and buyer power, entry barriers, substitutes, and disruptive threats, with actionable strategic insights to inform investor and management decisions.

A concise Porter's Five Forces snapshot for Martinrea—clarifies competitive pressures at a glance to speed strategic decisions.

Customers Bargaining Power

Concentration of Major Global OEMs

Strenuous Annual Price Reduction Demands

Automotive OEMs demand annual productivity gains and price cuts—often 1–3% yearly—pressuring Martinrea's margins and forcing continuous innovation and cost-savings; this contributed to the industry average supplier margin compression to roughly 6–8% in 2024. OEMs' audit rights and cost-transparency demands amplify customer power, enabling them to verify supplier cost models and extract further concessions, so Martinrea must prioritize automation and lean projects to protect EBIT.

Rigorous Quality and Safety Certifications

Customers set technical benchmarks that give them strong leverage over Martinrea; global OEMs demand IATF 16949 automotive quality certification and strict PPAP (production part approval process) compliance, and noncompliance can drop a supplier from approved lists within months.

Failing standards risks costly recalls—automotive recalls cost OEMs and suppliers an average $2,000–$10,000 per vehicle in direct charges in recent large recalls—and can exclude Martinrea from contracts worth millions.

This buyer-driven dynamic makes excellence the baseline: OEMs can demand defect rates under 50 PPM (parts per million) and warranty exposure limits, keeping bargaining power firmly with customers.

Switching Costs and Long-Term Program Ties

OEMs hold strong bargaining power, but high mid-program switching costs give Martinrea defensive stability; re-tooling a platform often costs tens to hundreds of millions and validation can add months and >$10m per component, so OEMs avoid changes mid-cycle.

This integration creates mutual dependency that tempers customer leverage across a model lifecycle, reducing effective price pressure and securing recurring volume for Martinrea.

- Re-tooling: $10–$200M per platform

- Validation: >$10M per complex component

- Time cost: months to >1 year

- Result: lower mid-cycle switching, steadier margins

Threat of OEM Vertical Integration

OEMs are increasingly evaluating backward integration for EV parts—Ford, GM and Tesla disclosed in 2024 plans or pilots to internalize battery enclosures or structural castings to cut costs; OEM vertical integration can shave supplier spend by 5–15% per part based on 2023 supplier margin benchmarks.

For Martinrea this raises pricing pressure; the company must show cost advantages (targeting sub-10% supplier margin) and proprietary tech—its 2024 R&D spend was US$61m—to keep OEMs from internalizing.

OEM-Driven Revenue (55–65%); High Switching Costs Shield Margins Amid 1–3% Price Pressure

OEMs (GM, Ford, Stellantis) held ~55–65% of Martinrea 2024 sales, giving them strong price and spec leverage; annual OEM price demands (~1–3%) and supplier margin compression (industry 6–8% in 2024) squeeze EBIT, while high mid-program switching costs (re-tooling $10–$200M; validation >$10M; months–>1yr) provide defensive stability; 2024 R&D was US$61m.

| Metric | Value |

|---|---|

| Top OEM share | 55–65% |

| Supplier margin (industry) | 6–8% |

| Annual OEM price cuts | 1–3% |

| Re-tooling | $10–$200M |

| Validation per component | >$10M |

| 2024 R&D | US$61m |

Preview Before You Purchase

Martinrea Porter's Five Forces Analysis

This preview shows the exact Martinrea Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders, no mockups.

The document displayed here is the full, professionally formatted analysis ready for download and use the moment you buy.

You’re previewing the final version: the same deliverable will be available to you instantly after payment, fully ready for your needs.