MasterCraft Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

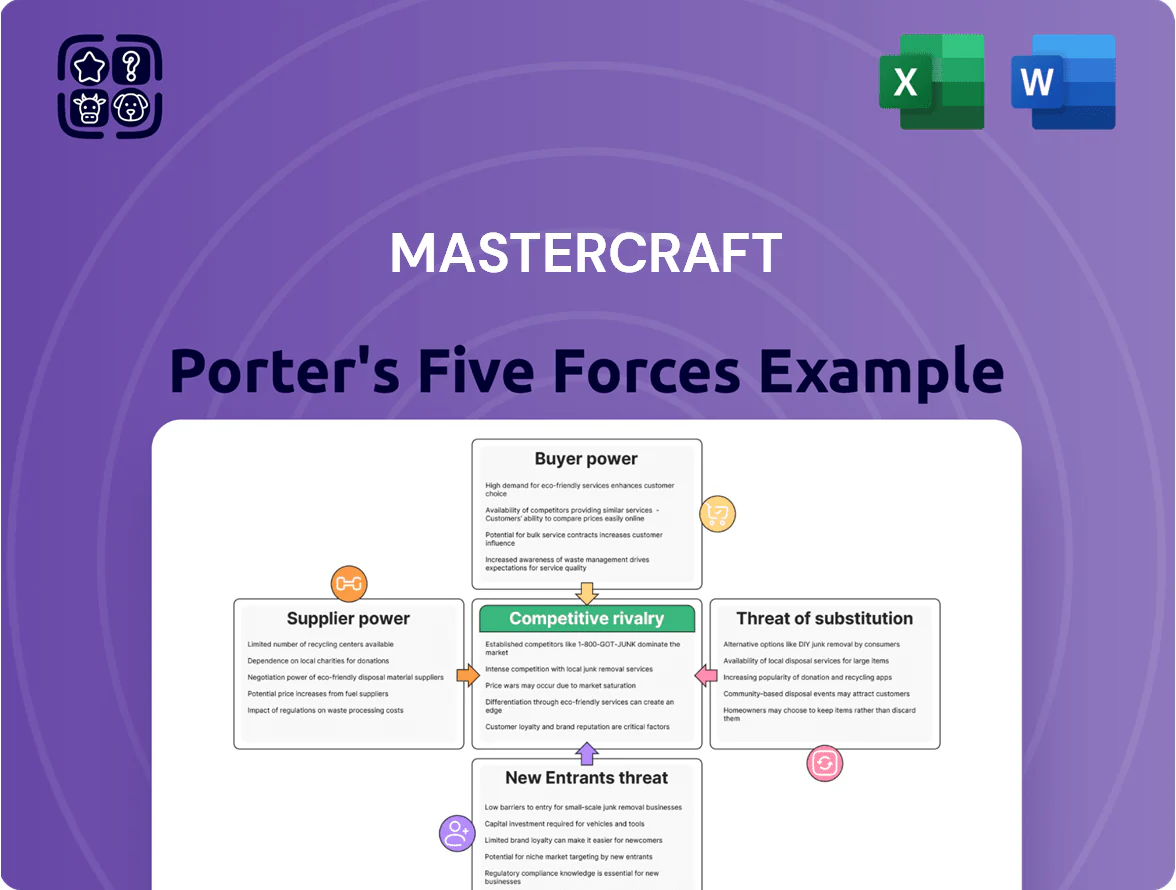

MasterCraft faces moderate supplier leverage, niche buyer expectations, and growing substitute pressures from alternative watercraft and rental platforms, shaping a competitive yet opportunity-rich landscape; this snapshot highlights core dynamics but omits force-specific ratings and implications.

Suppliers Bargaining Power

Concentration of Marine Engine Manufacturers

The high-performance marine engine market is concentrated: Ilmor, Mercury Marine, and Volvo Penta held an estimated 68% share of OEM supply to premium towboat builders in 2025, limiting MasterCraft’s switch options.

These engines carry tight specs and CE/IMO emissions rules, so switching costs and lead times exceed 6–9 months, giving suppliers leverage on price and delivery.

Suppliers set innovation timetables; in 2024–25 Mercury raised OEM prices ~4–7%, squeezing margins for builders like MasterCraft.

Specialized Raw Material Costs

Production needs high-grade resins, fiberglass, and marine upholstery, whose prices rose ~18% for composites and 12% for PU foam in 2024, driven by feedstock shortages and freight costs. Suppliers of specialized chemicals and reinforced plastics typically pass through price hikes, squeezing OEM margins; MasterCraft reported material cost inflation added about $3.4M to COGS in FY2024. Reliance on specific marine-grade specs limits MasterCraft’s negotiating leverage without hurting quality.

Proprietary Technology and Components

Many components for MasterCraft’s digital dash and wake-shaping tech come from niche electronics vendors and are custom-engineered, raising switching costs; replacing a supplier can add 6–12 months and $1.2–3.5M in integration costs per model.

Because software is tightly integrated with hardware, supplier disruption or price hikes risk 4–8% margin compression; only 1–2 alternate suppliers exist for key chips as of 2025, limiting quick options.

Labor Market Constraints

Suppliers of skilled components face a tightening labor market for specialized marine technicians, pushing subcontractor lead times up 15–25% and input costs roughly 6–9% year-over-year for comparable boatmakers in 2024–2025.

This secondary labor squeeze raises MasterCraft’s production risk: moderate threat to throughput and margins given limited backfill talent and rising pay rates for craftsmanship.

- Lead times +15–25%

- Input costs +6–9% YoY

- Scarcity = moderate threat (late 2025)

Forward Integration Risk

Forward integration risk is low because boat manufacturing needs large capital and dealer networks, but engine makers like Mercury (Brunswick Corp subsidiary) and Volvo Penta have pushed integrated propulsion and hull-management suites since 2023, giving them leverage over brands like MasterCraft.

When suppliers control the boat’s control systems (the 'brain'), they can limit MasterCraft’s engineering differentiation and capture higher margins—Brunswick reported 2024 engine-related revenue of $3.9 billion, showing scale that raises strategic risk for OEMs.

- Capital barriers keep full vertical entry rare

- Large engine suppliers offer integrated systems since 2023

- Supplier-controlled 'brains' reduce MasterCraft product differentiation

- Brunswick’s $3.9B 2024 engine revenue signals strong supplier power

Supplier power squeezes margins: 68% OEM concentration, $3.4M inflating COGS

Suppliers hold high bargaining power: 68% OEM engine concentration (Ilmor, Mercury, Volvo Penta) and long 6–9+ month switch times raise costs; 2024–25 material inflation (composites +18%, PU foam +12%) added ~$3.4M to MasterCraft COGS; niche electronics limited to 1–2 chip suppliers risk 4–8% margin hit; Brunswick engine revenue $3.9B (2024) underscores supplier scale.

| Metric | Value |

|---|---|

| Engine OEM share | 68% |

| Switch lead time | 6–9+ months |

| Material inflation 2024 | Composites +18%, PU +12% |

| COGS impact FY2024 | $3.4M |

| Brunswick engine rev | $3.9B (2024) |

What is included in the product

Comprehensive Porter's Five Forces assessment for MasterCraft, pinpointing competitive rivalry, buyer and supplier power, substitutes, and entry barriers, with strategic insights on disruptive threats and pricing leverage to inform investor materials and internal strategy.

A concise one-sheet MasterCraft Porter’s Five Forces summary that highlights key competitive pressures and relief strategies—ideal for quick boardroom decisions and deck-ready use.

Customers Bargaining Power

Dealer Network Dependency

MasterCraft relies on an independent dealer network for ~85% of U.S. sales; large regional dealer groups controlling ~40–60% of local inventories can shift floor-planning to competitors if MasterCraft’s dealer incentives or inventory turns lag industry averages (typical boat inventory turn ~2–3x/year). This concentration raises customer bargaining power and elevates risk to MasterCraft’s revenue and margins.

High Price Sensitivity in Premium Segments

As interest rates rose to about 5% in 2025, luxury boat buyers grew price-sensitive, demanding clearer value and financing options; JPMorgan data show 42% of high-net-worth buyers delayed purchases for better terms.

Online comparison tools let buyers match specs, warranties, and resale values across competitors, increasing transparency and shortening decision cycles.

This forces MasterCraft to either cut effective prices or add features—recall 2024 models saw a 3–5% premium yet lagged resale forecasts by 1.2 percentage points.

Low Switching Costs Between Brands

While wakeboarders show brand loyalty, switching costs from MasterCraft to Malibu or Nautique are low: 2024 industry data show top-tier wake boats converge on specs, and comparable models range $100k–$200k, so buyers focus on promotions and dealer incentives (average discount 5–8% in 2024).

Impact of Secondary Market Inventory

The 2024 surge in late-model used boats—NADA showing a 12% increase in certified pre-owned listings for towboats—raises buyer leverage, since customers can opt for near-new MasterCraft equivalents at 20–35% lower prices.

Saturated secondary inventory forces MasterCraft and dealers to increase incentives (finance rates, trade‑in credits) and push product differentiation like new SmartCraft tech to defend new-unit margins.

Influence of Professional and Influencer Endorsements

Professional athletes and social media personalities drive purchase decisions for MasterCraft; Nielsen Sports found athlete endorsements lift brand consideration by 18% on average in 2024.

If top influencers switch to rival brands, MasterCraft’s perceived value can fall quickly—retention risk rises and retail sell-through can drop 6–12% within a quarter, per industry cases in 2023–2024.

This social leverage forces MasterCraft to spend heavily on marketing and athlete deals—company-level sponsorship and promotion budgets often reach 5–8% of revenue in premium marine brands; MasterCraft must match or exceed that to keep pull.

- Endorsements raise consideration +18% (Nielsen Sports 2024)

- Influencer defections can cut sell-through 6–12% in a quarter

- Marketing/partnership spend ~5–8% of revenue for premium marine brands

Dealer Power Squeezes MasterCraft: High Concentration, Rising CPO Supply & Price Pressure

MasterCraft faces high customer bargaining power: ~85% U.S. sales via dealers, 40–60% local dealer inventory concentration, and typical inventory turns 2–3x/yr increasing leverage; 2024–25 data: 12% rise in certified pre-owned listings (NADA 2024), 20–35% price gap vs new, average dealer discount 5–8%, and influencer-driven consideration +18% (Nielsen Sports 2024).

| Metric | Value |

|---|---|

| Dealer sales share | ~85% |

| Dealer concentration | 40–60% |

| Inventory turns | 2–3x/yr |

| Pre-owned listings change (2024) | +12% |

| Price gap (new vs near-new) | 20–35% |

| Avg dealer discount (2024) | 5–8% |

| Influencer lift | +18% |

What You See Is What You Get

MasterCraft Porter's Five Forces Analysis

This preview shows the exact MasterCraft Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or summaries; the full, professionally formatted document is ready for download and use the moment you buy.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

MasterCraft faces moderate supplier leverage, niche buyer expectations, and growing substitute pressures from alternative watercraft and rental platforms, shaping a competitive yet opportunity-rich landscape; this snapshot highlights core dynamics but omits force-specific ratings and implications.

Suppliers Bargaining Power

Concentration of Marine Engine Manufacturers

The high-performance marine engine market is concentrated: Ilmor, Mercury Marine, and Volvo Penta held an estimated 68% share of OEM supply to premium towboat builders in 2025, limiting MasterCraft’s switch options.

These engines carry tight specs and CE/IMO emissions rules, so switching costs and lead times exceed 6–9 months, giving suppliers leverage on price and delivery.

Suppliers set innovation timetables; in 2024–25 Mercury raised OEM prices ~4–7%, squeezing margins for builders like MasterCraft.

Specialized Raw Material Costs

Production needs high-grade resins, fiberglass, and marine upholstery, whose prices rose ~18% for composites and 12% for PU foam in 2024, driven by feedstock shortages and freight costs. Suppliers of specialized chemicals and reinforced plastics typically pass through price hikes, squeezing OEM margins; MasterCraft reported material cost inflation added about $3.4M to COGS in FY2024. Reliance on specific marine-grade specs limits MasterCraft’s negotiating leverage without hurting quality.

Proprietary Technology and Components

Many components for MasterCraft’s digital dash and wake-shaping tech come from niche electronics vendors and are custom-engineered, raising switching costs; replacing a supplier can add 6–12 months and $1.2–3.5M in integration costs per model.

Because software is tightly integrated with hardware, supplier disruption or price hikes risk 4–8% margin compression; only 1–2 alternate suppliers exist for key chips as of 2025, limiting quick options.

Labor Market Constraints

Suppliers of skilled components face a tightening labor market for specialized marine technicians, pushing subcontractor lead times up 15–25% and input costs roughly 6–9% year-over-year for comparable boatmakers in 2024–2025.

This secondary labor squeeze raises MasterCraft’s production risk: moderate threat to throughput and margins given limited backfill talent and rising pay rates for craftsmanship.

- Lead times +15–25%

- Input costs +6–9% YoY

- Scarcity = moderate threat (late 2025)

Forward Integration Risk

Forward integration risk is low because boat manufacturing needs large capital and dealer networks, but engine makers like Mercury (Brunswick Corp subsidiary) and Volvo Penta have pushed integrated propulsion and hull-management suites since 2023, giving them leverage over brands like MasterCraft.

When suppliers control the boat’s control systems (the 'brain'), they can limit MasterCraft’s engineering differentiation and capture higher margins—Brunswick reported 2024 engine-related revenue of $3.9 billion, showing scale that raises strategic risk for OEMs.

- Capital barriers keep full vertical entry rare

- Large engine suppliers offer integrated systems since 2023

- Supplier-controlled 'brains' reduce MasterCraft product differentiation

- Brunswick’s $3.9B 2024 engine revenue signals strong supplier power

Supplier power squeezes margins: 68% OEM concentration, $3.4M inflating COGS

Suppliers hold high bargaining power: 68% OEM engine concentration (Ilmor, Mercury, Volvo Penta) and long 6–9+ month switch times raise costs; 2024–25 material inflation (composites +18%, PU foam +12%) added ~$3.4M to MasterCraft COGS; niche electronics limited to 1–2 chip suppliers risk 4–8% margin hit; Brunswick engine revenue $3.9B (2024) underscores supplier scale.

| Metric | Value |

|---|---|

| Engine OEM share | 68% |

| Switch lead time | 6–9+ months |

| Material inflation 2024 | Composites +18%, PU +12% |

| COGS impact FY2024 | $3.4M |

| Brunswick engine rev | $3.9B (2024) |

What is included in the product

Comprehensive Porter's Five Forces assessment for MasterCraft, pinpointing competitive rivalry, buyer and supplier power, substitutes, and entry barriers, with strategic insights on disruptive threats and pricing leverage to inform investor materials and internal strategy.

A concise one-sheet MasterCraft Porter’s Five Forces summary that highlights key competitive pressures and relief strategies—ideal for quick boardroom decisions and deck-ready use.

Customers Bargaining Power

Dealer Network Dependency

MasterCraft relies on an independent dealer network for ~85% of U.S. sales; large regional dealer groups controlling ~40–60% of local inventories can shift floor-planning to competitors if MasterCraft’s dealer incentives or inventory turns lag industry averages (typical boat inventory turn ~2–3x/year). This concentration raises customer bargaining power and elevates risk to MasterCraft’s revenue and margins.

High Price Sensitivity in Premium Segments

As interest rates rose to about 5% in 2025, luxury boat buyers grew price-sensitive, demanding clearer value and financing options; JPMorgan data show 42% of high-net-worth buyers delayed purchases for better terms.

Online comparison tools let buyers match specs, warranties, and resale values across competitors, increasing transparency and shortening decision cycles.

This forces MasterCraft to either cut effective prices or add features—recall 2024 models saw a 3–5% premium yet lagged resale forecasts by 1.2 percentage points.

Low Switching Costs Between Brands

While wakeboarders show brand loyalty, switching costs from MasterCraft to Malibu or Nautique are low: 2024 industry data show top-tier wake boats converge on specs, and comparable models range $100k–$200k, so buyers focus on promotions and dealer incentives (average discount 5–8% in 2024).

Impact of Secondary Market Inventory

The 2024 surge in late-model used boats—NADA showing a 12% increase in certified pre-owned listings for towboats—raises buyer leverage, since customers can opt for near-new MasterCraft equivalents at 20–35% lower prices.

Saturated secondary inventory forces MasterCraft and dealers to increase incentives (finance rates, trade‑in credits) and push product differentiation like new SmartCraft tech to defend new-unit margins.

Influence of Professional and Influencer Endorsements

Professional athletes and social media personalities drive purchase decisions for MasterCraft; Nielsen Sports found athlete endorsements lift brand consideration by 18% on average in 2024.

If top influencers switch to rival brands, MasterCraft’s perceived value can fall quickly—retention risk rises and retail sell-through can drop 6–12% within a quarter, per industry cases in 2023–2024.

This social leverage forces MasterCraft to spend heavily on marketing and athlete deals—company-level sponsorship and promotion budgets often reach 5–8% of revenue in premium marine brands; MasterCraft must match or exceed that to keep pull.

- Endorsements raise consideration +18% (Nielsen Sports 2024)

- Influencer defections can cut sell-through 6–12% in a quarter

- Marketing/partnership spend ~5–8% of revenue for premium marine brands

Dealer Power Squeezes MasterCraft: High Concentration, Rising CPO Supply & Price Pressure

MasterCraft faces high customer bargaining power: ~85% U.S. sales via dealers, 40–60% local dealer inventory concentration, and typical inventory turns 2–3x/yr increasing leverage; 2024–25 data: 12% rise in certified pre-owned listings (NADA 2024), 20–35% price gap vs new, average dealer discount 5–8%, and influencer-driven consideration +18% (Nielsen Sports 2024).

| Metric | Value |

|---|---|

| Dealer sales share | ~85% |

| Dealer concentration | 40–60% |

| Inventory turns | 2–3x/yr |

| Pre-owned listings change (2024) | +12% |

| Price gap (new vs near-new) | 20–35% |

| Avg dealer discount (2024) | 5–8% |

| Influencer lift | +18% |

What You See Is What You Get

MasterCraft Porter's Five Forces Analysis

This preview shows the exact MasterCraft Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or summaries; the full, professionally formatted document is ready for download and use the moment you buy.