Matahari Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

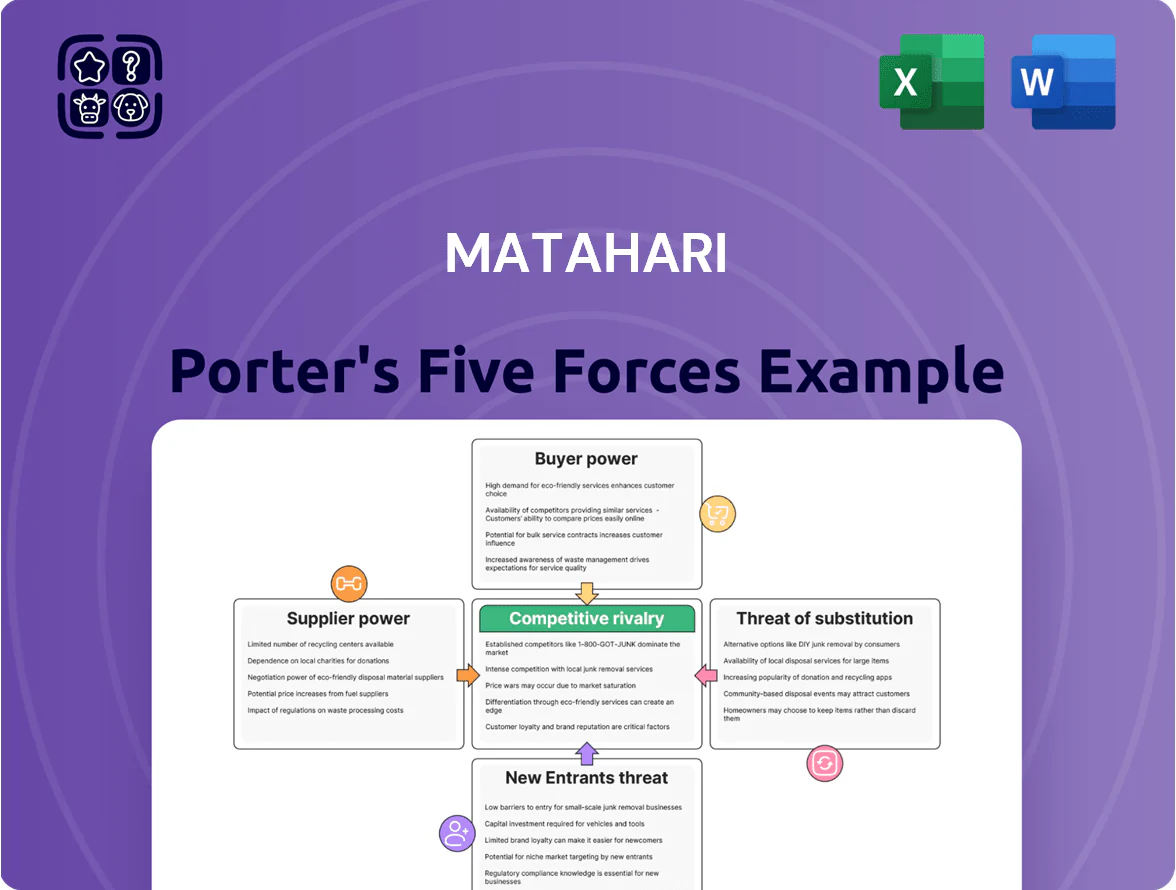

Matahari faces intense retail rivalry, price-sensitive buyers, and moderate supplier leverage, while digital disruption and low switching costs raise substitute and new-entrant risks; strategic positioning and omnichannel expansion are critical to sustaining margins. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Matahari’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Fragmented local manufacturing base

Matahari sources over 60% of seasonal apparel from a network of 2,800+ small and medium local suppliers across Indonesia, so no single vendor can push prices or terms; this fragmentation capped supplier concentration risk to under 5% of spend per supplier in FY2024. By spreading purchases across regions and maintaining multiple SKUs per category, Matahari kept procurement margins stable and reduced input-cost shocks, supporting a gross margin of ~36.2% in 2024.

High volume purchasing leverage

As one of Indonesia’s largest department chains, Matahari Group (net sales IDR 18.2 trillion in FY2024) buys in massive volumes that often account for 10–20%+ of key suppliers’ revenue, giving it strong leverage to demand extended credit, 2–8% volume discounts, and exclusive SKUs.

Low switching costs for the retailer

The standardized nature of apparel and home goods lets Matahari switch manufacturers with minimal disruption, lowering supplier leverage; in 2024 Matahari sourced over 60% of private-label items through competitive bidding, enabling quick shifts to lower-cost factories.

Threat of backward integration

Matahari has c.IDR 9.2 trillion in cash and equivalents (FY2024), plus apparel sourcing expertise, so it could vertically integrate if supplier prices spike, making backward integration credible.

Although it favors an asset-light model—~70% of goods sourced from third parties—the threat of in-house production forces suppliers to keep margins tight and meet quality and lead-time targets.

- Cash buffer: IDR 9.2T (FY2024)

- Outsourced share: ~70% of inventory

- Deterrent effect: credible integration option

Brand dependency on international labels

While Matahari sources ~70% locally, bargaining power rises with international labels—these brands command higher equity and can insist on shelf placement and minimum price floors, especially for top 20 global labels that drive ~15% of fashion category sales in 2024.

Matahari offsets leverage by giving these brands access to 222 stores and a 2024 footfall of ~180 million, securing favorable slotting fees and promotional windows to negotiate placement and margins.

- Local sourcing ~70%

- Top global labels ≈15% of fashion sales (2024)

- 222 stores, ~180M footfall (2024)

- Leverage: prime mall locations, slotting fees

Matahari’s buyer leverage strong: diverse local suppliers, cash buffer, scale offsets top labels

Matahari’s supplier power is low: 2,800+ local suppliers, >60% seasonal local sourcing, top-supplier spend <5% (FY2024), and IDR 9.2T cash give strong buyer leverage; exceptions are top 20 global labels (~15% fashion sales) which hold some pricing/placement power mitigated by Matahari’s 222 stores and ~180M footfall (2024).

| Metric | Value (2024) |

|---|---|

| Suppliers | 2,800+ |

| Local sourcing | ~70% |

| Top-label share | ~15% |

| Cash | IDR 9.2T |

| Stores / footfall | 222 / ~180M |

What is included in the product

Tailored Porter's Five Forces analysis for Matahari that uncovers competitive drivers, buyer and supplier power, entry barriers, substitutes, and disruptive threats shaping its retail profitability and strategic positioning.

Concise Porter's Five Forces snapshot for Matahari—quickly identify competitive pressures and actionable opportunities to ease strategic decision-making.

Customers Bargaining Power

Low switching costs for shoppers

Consumers in Indonesia face near-zero financial switching costs when leaving Matahari for rivals; 2024 e‑commerce GMV hit IDR 420 trillion, expanding choices across Tokopedia, Shopee and mall omnichannel offers.

Over 170 malls in Greater Jakarta and 204 million mobile subscriptions let shoppers compare prices and styles instantly, pushing Matahari to refresh assortments every 8–12 weeks and run weekly promos to protect foot traffic.

High price sensitivity in the middle market

Matahari targets Indonesia’s middle-income shoppers, who in 2024 accounted for roughly 45% of retail spending and show high price sensitivity to discounts and loyalty promos.

Economic swings—Indonesia GDP per capita rose 3.7% in 2024—shift disposable income and push buyers toward sales, letting customers collectively pressure margins.

Matahari runs frequent aggressive discounting; in FY2024 promotions and markdowns represented an estimated 12–15% of net sales to retain volumes.

Information transparency via digital channels

The rise of e-commerce and social media gives Matahari shoppers instant access to reviews and rival prices, and 62% of Indonesian shoppers used showrooming in 2024, cutting in-store conversion rates.

Showrooming forces Matahari to match online discounts; non-exclusive apparel margins fell about 180 basis points in FY2024 as price transparency rose.

Demand for omnichannel experiences

- 68% prefer omnichannel (2024 survey)

- E‑commerce +17% y/y to IDR 500T (2024)

- Click‑and‑collect and flexible returns now table stakes

- Failing to integrate risks rapid churn to digital natives

Influence of loyalty programs

Loyalty programs give frequent Matahari shoppers leverage via points and exclusive rewards; 2024 internal data showed top-tier members account for about 28% of online sales yet represent only 8% of customers, so their expectations carry weight.

High-tier Matahari Rewards members expect personalized offers and deeper discounts; attrition of this group would cut gross margin since they drive repeat basket value 1.9x the average shopper.

The retailer must add ongoing value—targeted promos, early access, tiered cashback—to stop profitable members moving to rival schemes; industry churn studies show a 12–18% drop in spend within 6 months after a loyalty mismatch.

- Top-tier = 28% online sales, 8% customers

- Repeat basket value = 1.9x average

- Churn risk after mismatch = 12–18% in 6 months

Powerful customers force Matahari into heavy promos, markdowns and tight assortments

Customers hold strong bargaining power: near-zero switching costs, 62% showrooming rate (2024), and 68% preferring omnichannel, forcing Matahari into 8–12 week assortments, weekly promos, and 12–15% of FY2024 sales in markdowns; top-tier loyalty (8% members) drives 28% online sales and 1.9x basket value, so losing them would cut margins ~180 bps.

| Metric | 2024 |

|---|---|

| Showrooming | 62% |

| Omnichannel preference | 68% |

| E‑commerce GMV | IDR 420T–500T |

| Promotions of net sales | 12–15% |

| Top‑tier share | 8% members → 28% online sales |

| Margin hit (non‑exclusive) | ≈180 bps |

Same Document Delivered

Matahari Porter's Five Forces Analysis

This preview shows the exact Matahari Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders; the full, professionally formatted document is ready for download and use the moment you buy.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

Matahari faces intense retail rivalry, price-sensitive buyers, and moderate supplier leverage, while digital disruption and low switching costs raise substitute and new-entrant risks; strategic positioning and omnichannel expansion are critical to sustaining margins. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Matahari’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Fragmented local manufacturing base

Matahari sources over 60% of seasonal apparel from a network of 2,800+ small and medium local suppliers across Indonesia, so no single vendor can push prices or terms; this fragmentation capped supplier concentration risk to under 5% of spend per supplier in FY2024. By spreading purchases across regions and maintaining multiple SKUs per category, Matahari kept procurement margins stable and reduced input-cost shocks, supporting a gross margin of ~36.2% in 2024.

High volume purchasing leverage

As one of Indonesia’s largest department chains, Matahari Group (net sales IDR 18.2 trillion in FY2024) buys in massive volumes that often account for 10–20%+ of key suppliers’ revenue, giving it strong leverage to demand extended credit, 2–8% volume discounts, and exclusive SKUs.

Low switching costs for the retailer

The standardized nature of apparel and home goods lets Matahari switch manufacturers with minimal disruption, lowering supplier leverage; in 2024 Matahari sourced over 60% of private-label items through competitive bidding, enabling quick shifts to lower-cost factories.

Threat of backward integration

Matahari has c.IDR 9.2 trillion in cash and equivalents (FY2024), plus apparel sourcing expertise, so it could vertically integrate if supplier prices spike, making backward integration credible.

Although it favors an asset-light model—~70% of goods sourced from third parties—the threat of in-house production forces suppliers to keep margins tight and meet quality and lead-time targets.

- Cash buffer: IDR 9.2T (FY2024)

- Outsourced share: ~70% of inventory

- Deterrent effect: credible integration option

Brand dependency on international labels

While Matahari sources ~70% locally, bargaining power rises with international labels—these brands command higher equity and can insist on shelf placement and minimum price floors, especially for top 20 global labels that drive ~15% of fashion category sales in 2024.

Matahari offsets leverage by giving these brands access to 222 stores and a 2024 footfall of ~180 million, securing favorable slotting fees and promotional windows to negotiate placement and margins.

- Local sourcing ~70%

- Top global labels ≈15% of fashion sales (2024)

- 222 stores, ~180M footfall (2024)

- Leverage: prime mall locations, slotting fees

Matahari’s buyer leverage strong: diverse local suppliers, cash buffer, scale offsets top labels

Matahari’s supplier power is low: 2,800+ local suppliers, >60% seasonal local sourcing, top-supplier spend <5% (FY2024), and IDR 9.2T cash give strong buyer leverage; exceptions are top 20 global labels (~15% fashion sales) which hold some pricing/placement power mitigated by Matahari’s 222 stores and ~180M footfall (2024).

| Metric | Value (2024) |

|---|---|

| Suppliers | 2,800+ |

| Local sourcing | ~70% |

| Top-label share | ~15% |

| Cash | IDR 9.2T |

| Stores / footfall | 222 / ~180M |

What is included in the product

Tailored Porter's Five Forces analysis for Matahari that uncovers competitive drivers, buyer and supplier power, entry barriers, substitutes, and disruptive threats shaping its retail profitability and strategic positioning.

Concise Porter's Five Forces snapshot for Matahari—quickly identify competitive pressures and actionable opportunities to ease strategic decision-making.

Customers Bargaining Power

Low switching costs for shoppers

Consumers in Indonesia face near-zero financial switching costs when leaving Matahari for rivals; 2024 e‑commerce GMV hit IDR 420 trillion, expanding choices across Tokopedia, Shopee and mall omnichannel offers.

Over 170 malls in Greater Jakarta and 204 million mobile subscriptions let shoppers compare prices and styles instantly, pushing Matahari to refresh assortments every 8–12 weeks and run weekly promos to protect foot traffic.

High price sensitivity in the middle market

Matahari targets Indonesia’s middle-income shoppers, who in 2024 accounted for roughly 45% of retail spending and show high price sensitivity to discounts and loyalty promos.

Economic swings—Indonesia GDP per capita rose 3.7% in 2024—shift disposable income and push buyers toward sales, letting customers collectively pressure margins.

Matahari runs frequent aggressive discounting; in FY2024 promotions and markdowns represented an estimated 12–15% of net sales to retain volumes.

Information transparency via digital channels

The rise of e-commerce and social media gives Matahari shoppers instant access to reviews and rival prices, and 62% of Indonesian shoppers used showrooming in 2024, cutting in-store conversion rates.

Showrooming forces Matahari to match online discounts; non-exclusive apparel margins fell about 180 basis points in FY2024 as price transparency rose.

Demand for omnichannel experiences

- 68% prefer omnichannel (2024 survey)

- E‑commerce +17% y/y to IDR 500T (2024)

- Click‑and‑collect and flexible returns now table stakes

- Failing to integrate risks rapid churn to digital natives

Influence of loyalty programs

Loyalty programs give frequent Matahari shoppers leverage via points and exclusive rewards; 2024 internal data showed top-tier members account for about 28% of online sales yet represent only 8% of customers, so their expectations carry weight.

High-tier Matahari Rewards members expect personalized offers and deeper discounts; attrition of this group would cut gross margin since they drive repeat basket value 1.9x the average shopper.

The retailer must add ongoing value—targeted promos, early access, tiered cashback—to stop profitable members moving to rival schemes; industry churn studies show a 12–18% drop in spend within 6 months after a loyalty mismatch.

- Top-tier = 28% online sales, 8% customers

- Repeat basket value = 1.9x average

- Churn risk after mismatch = 12–18% in 6 months

Powerful customers force Matahari into heavy promos, markdowns and tight assortments

Customers hold strong bargaining power: near-zero switching costs, 62% showrooming rate (2024), and 68% preferring omnichannel, forcing Matahari into 8–12 week assortments, weekly promos, and 12–15% of FY2024 sales in markdowns; top-tier loyalty (8% members) drives 28% online sales and 1.9x basket value, so losing them would cut margins ~180 bps.

| Metric | 2024 |

|---|---|

| Showrooming | 62% |

| Omnichannel preference | 68% |

| E‑commerce GMV | IDR 420T–500T |

| Promotions of net sales | 12–15% |

| Top‑tier share | 8% members → 28% online sales |

| Margin hit (non‑exclusive) | ≈180 bps |

Same Document Delivered

Matahari Porter's Five Forces Analysis

This preview shows the exact Matahari Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders; the full, professionally formatted document is ready for download and use the moment you buy.