Johnson Matthey PESTLE Analysis

Your Competitive Advantage Starts with This Report

Gain a strategic advantage with our concise PESTLE Analysis of Johnson Matthey—spot regulatory risks, technology shifts, and market drivers shaping its future, and turn those insights into action. Download the full report for a complete, ready-to-use breakdown ideal for investors, consultants, and strategists. Purchase now to get instant access to expert analysis and editable formats.

Political factors

Green Subsidy Frameworks

Governments globally are increasing green subsidies—EU allocated €210bn for hydrogen and sustainable fuels under RePowerEU and the UK committed £1.6bn to hydrogen by 2025—boosting demand for Johnson Matthey’s catalysts and electrolysis tech.

As a key technology provider in the UK and EU, Johnson Matthey stands to capture higher margins from subsidy-driven project pipelines and increased orderbooks.

However, political shifts in major economies (e.g., EU elections, US policy changes) could alter the longevity and scale of these support schemes, introducing revenue volatility for JM tied to policy continuity.

Geopolitical Supply Chain Risks

Dependence on South Africa and Russia for ~70% of global platinum group metals supply exposes Johnson Matthey to regional instability; South Africa accounted for ~40% and Russia ~30% of PGM mine output in 2024, risking disruptions to catalyst production. Trade sanctions or export curbs—such as 2022–24 Russian export restrictions—can spike prices (platinum rose ~28% in 2022–23) and squeeze margins. Johnson Matthey must manage diplomatic risks, diversify sourcing and hedge to preserve operational continuity and price stability.

Hydrogen Economy Prioritization

Trade Policy and Tariffs

Evolving UK-EU-China trade agreements influence Johnson Matthey’s export costs for specialty chemicals; UK goods exports to EU fell 1.6% in 2024 while China-EU trade rose 3.8%, altering supply-chain expenses.

Tariffs on high-tech components—averaging 2–8% across key markets in 2025—can erode JM’s price competitiveness versus local producers, affecting margins on catalytic and battery materials.

Strategic hub placement (UK, EU, China) and a 12% cost-savings target from regional sourcing are vital to mitigate tariffs and preserve global market share.

- Evolving trade flows: UK exports to EU down 1.6% (2024), China-EU +3.8% (2024)

- Average high-tech tariffs: 2–8% (2025)

- Target regional sourcing savings: 12% to offset tariffs

- Manufacturing hubs: UK, EU, China for risk diversification

Industrial Decarbonization Mandates

Political pressure on heavy industries to cut emissions is expanding demand for Johnson Matthey’s carbon capture and sustainable catalyst solutions; EU Fit for 55 and UK’s Net Zero Growth Plan target industrial cuts of 55%+ by 2030, creating multi-billion euro market opportunities.

National legislative roadmaps for industrial clusters (e.g., UK CCUS clusters with £20bn+ projected investment) list JM as a key technical partner for engineering low-carbon chemical processes.

Rising political support for carbon pricing—EU ETS prices averaging €90–€100/tCO2 in 2024—favors adoption of JM’s high-efficiency catalysts that lower emissions and operating costs.

- EU ETS ~€90–100/tCO2 (2024)

- UK CCUS investment pipeline £20bn+

- Fit for 55: 55% GHG reduction target by 2030

Policy tailwinds lift Johnson Matthey but PGM supply and tariffs threaten margins

Political support for hydrogen, CCUS and carbon pricing (EU ETS ~€90–100/tCO2 in 2024) and national funds (UK £1.6bn hydrogen to 2025; UK CCUS pipeline £20bn+) boosts Johnson Matthey’s demand, but reliance on South Africa/Russia for ~70% of PGMs and 2–8% high-tech tariffs (2025) create supply and margin risks.

| Metric | 2024/25 |

|---|---|

| EU ETS price | €90–100/tCO2 (2024) |

| UK hydrogen funding | £1.6bn to 2025 |

| PGM supply concentration | ~70% South Africa/Russia |

| High-tech tariffs | 2–8% (2025) |

What is included in the product

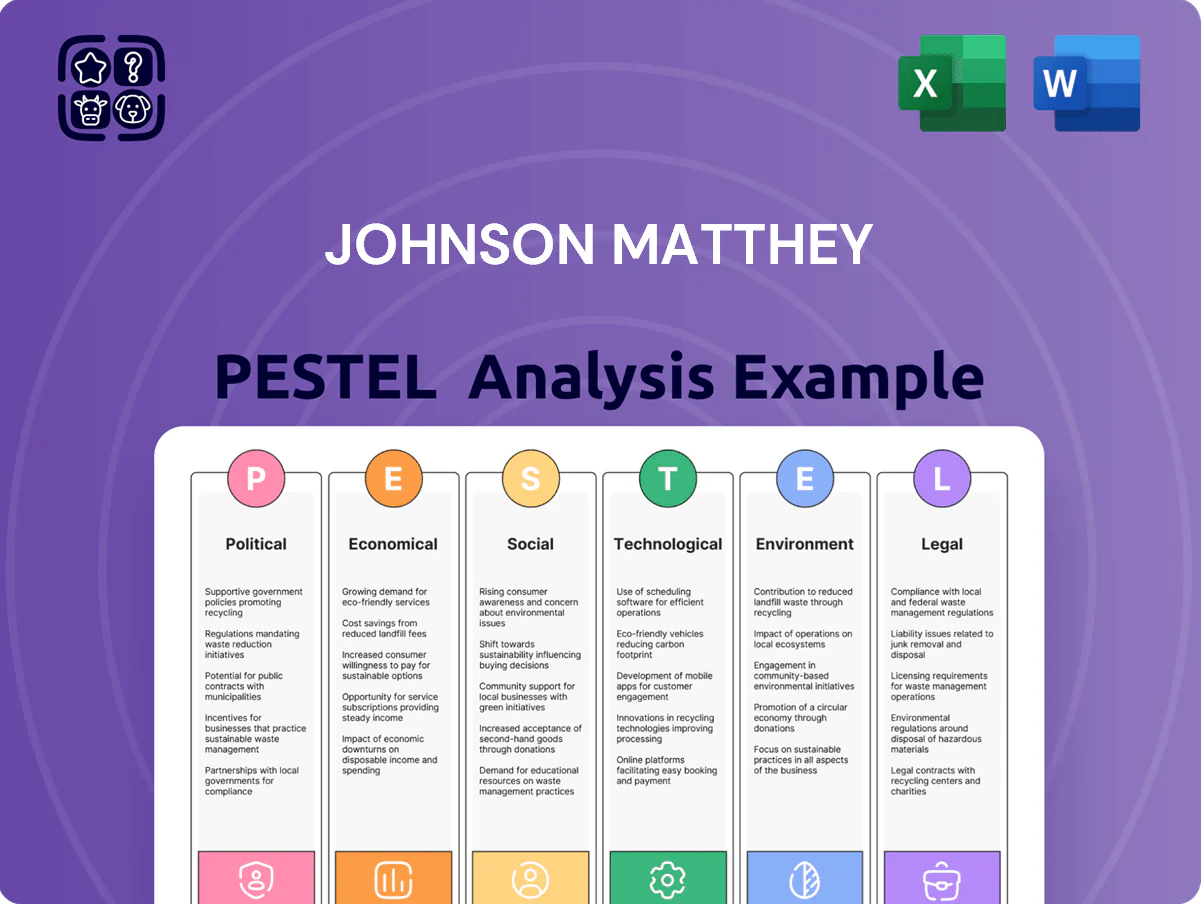

Explores how Political, Economic, Social, Technological, Environmental, and Legal factors uniquely impact Johnson Matthey’s catalytic, battery materials and chemicals businesses, backed by current market data and regulatory trends to pinpoint risks and opportunities for executives, investors, and strategists.

Condenses Johnson Matthey's PESTLE insights into a sharp, meeting-ready summary that highlights external risks and opportunities for quick strategic decisions.

Economic factors

Precious Metal Price Volatility

Fluctuations in platinum, palladium and rhodium prices—platinum down ~12% and rhodium up ~8% in 2024 YTD—directly alter Johnson Matthey’s production costs and inventory valuations, impacting gross margins on PGM sales (JM reported PGM margins swinging 200–400 bps in 2023–24). As a global PGM manager, JM is exposed to speculation and mining shocks (SA and Russia supply risks). Hedging programs and scaling recycling—JM’s recycled PGMs rose ~15% in 2024—are vital to mitigate this financial exposure.

Transition in Automotive Markets

The shift from internal combustion engines to EVs, with global EV sales reaching 14.2 million in 2024 (up ~35% year-on-year) and projected to be 30–40% of new car sales by 2030, reduces long-term demand for Johnson Matthey's traditional autocatalysts, risking legacy revenue streams.

Conversely, demand for battery materials (lithium, nickel, cobalt) and hydrogen fuel cell catalysts offers significant upside—battery material markets grew ~22% in 2024 to an estimated $230bn, while green hydrogen capacity targets hit 100 GW+ by 2030 in major economies.

The transition pace—regional EV penetration, 2024 EU ~25%, China ~35%, US ~10%—will drive JM's capital allocation between catalyst legacy units and growth in battery and hydrogen, potentially necessitating restructuring if ICE decline accelerates faster than anticipated.

Inflation and Operational Costs

Rising energy and raw material prices—Brent crude up ~15% in 2024 YTD to ~$90/bbl and nickel up ~22% in 2024—risk squeezing Johnson Matthey margins if price recovery cannot be passed to industrial customers; FY2024 gross margin was 28.6%, showing sensitivity to input costs.

Global manufacturing PMI cycles drive catalyst demand: global manufacturing PMI averaged ~50.2 in 2024, correlating with JM’s FY2024 catalytic demand trends and 3% organic revenue decline in Chemicals.

Maintaining cost efficiency via lean manufacturing and supply-chain optimization remains critical—JM reported a 4% reduction in manufacturing overheads in FY2024 from targeted productivity and procurement initiatives.

R&D Investment Capital

High interest rates raised UK base rate to 5.25% (Jan 2026), increasing borrowing costs for Johnson Matthey’s large-scale R&D in sustainable tech and hydrogen electrolysis projects.

Access to green bonds and equity markets—green bond issuance hit $580bn globally in 2025—remains crucial to commercialize hydrogen and circular-economy solutions.

UK financial stability, reflected in resilient bank CET1 ratios (~14% in 2025), underpins JM’s long-term investment planning.

- Higher rates raise project financing costs

- Green bond market $580bn (2025) vital for commercialization

- UK bank CET1 ~14% supports investment confidence

Currency Exchange Fluctuations

As a multinational, Johnson Matthey faces GBP, USD and EUR volatility; in FY2024 roughly 30% of revenue was USD/EUR-linked, meaning a 5% GBP move could swing reported sterling earnings by ~£40–60m.

Effective treasury management and hedging are essential: JM disclosed in 2024 rolling forward hedges covering a significant portion of near-term FX exposure to stabilize cash flows across regions.

- ~30% revenue USD/EUR-linked (FY2024)

- 5% GBP move ≈ £40–60m P&L impact

- Use of rolling forward hedges to reduce short-term FX volatility

PGM volatility trims margins as EVs cut catalyst demand; batteries & hydrogen offset

PGM price swings (platinum -12%, rhodium +8% 2024 YTD) and 15% recycled PGM growth drove 200–400bps margin volatility; EVs (14.2m sales 2024) cut autocatalyst demand while batteries ($230bn, +22% 2024) and hydrogen (100+ GW by 2030) offer growth; input cost rises (Brent ~$90/bbl, nickel +22% 2024) and FX (30% USD/EUR-linked revenue) plus UK base rate 5.25% raise financing costs.

| Metric | Value |

|---|---|

| Platinum | -12% |

| Rhodium | +8% |

| Recycled PGMs | +15% |

| EV sales 2024 | 14.2m (+35%) |

| Batt. market 2024 | $230bn (+22%) |

| Brent 2024 | ~$90/bbl |

| USD/EUR-linked rev | ~30% |

Preview the Actual Deliverable

Johnson Matthey PESTLE Analysis

The preview shown here is the exact Johnson Matthey PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic insight and decision-making.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Competitive Advantage Starts with This Report

Gain a strategic advantage with our concise PESTLE Analysis of Johnson Matthey—spot regulatory risks, technology shifts, and market drivers shaping its future, and turn those insights into action. Download the full report for a complete, ready-to-use breakdown ideal for investors, consultants, and strategists. Purchase now to get instant access to expert analysis and editable formats.

Political factors

Green Subsidy Frameworks

Governments globally are increasing green subsidies—EU allocated €210bn for hydrogen and sustainable fuels under RePowerEU and the UK committed £1.6bn to hydrogen by 2025—boosting demand for Johnson Matthey’s catalysts and electrolysis tech.

As a key technology provider in the UK and EU, Johnson Matthey stands to capture higher margins from subsidy-driven project pipelines and increased orderbooks.

However, political shifts in major economies (e.g., EU elections, US policy changes) could alter the longevity and scale of these support schemes, introducing revenue volatility for JM tied to policy continuity.

Geopolitical Supply Chain Risks

Dependence on South Africa and Russia for ~70% of global platinum group metals supply exposes Johnson Matthey to regional instability; South Africa accounted for ~40% and Russia ~30% of PGM mine output in 2024, risking disruptions to catalyst production. Trade sanctions or export curbs—such as 2022–24 Russian export restrictions—can spike prices (platinum rose ~28% in 2022–23) and squeeze margins. Johnson Matthey must manage diplomatic risks, diversify sourcing and hedge to preserve operational continuity and price stability.

Hydrogen Economy Prioritization

Trade Policy and Tariffs

Evolving UK-EU-China trade agreements influence Johnson Matthey’s export costs for specialty chemicals; UK goods exports to EU fell 1.6% in 2024 while China-EU trade rose 3.8%, altering supply-chain expenses.

Tariffs on high-tech components—averaging 2–8% across key markets in 2025—can erode JM’s price competitiveness versus local producers, affecting margins on catalytic and battery materials.

Strategic hub placement (UK, EU, China) and a 12% cost-savings target from regional sourcing are vital to mitigate tariffs and preserve global market share.

- Evolving trade flows: UK exports to EU down 1.6% (2024), China-EU +3.8% (2024)

- Average high-tech tariffs: 2–8% (2025)

- Target regional sourcing savings: 12% to offset tariffs

- Manufacturing hubs: UK, EU, China for risk diversification

Industrial Decarbonization Mandates

Political pressure on heavy industries to cut emissions is expanding demand for Johnson Matthey’s carbon capture and sustainable catalyst solutions; EU Fit for 55 and UK’s Net Zero Growth Plan target industrial cuts of 55%+ by 2030, creating multi-billion euro market opportunities.

National legislative roadmaps for industrial clusters (e.g., UK CCUS clusters with £20bn+ projected investment) list JM as a key technical partner for engineering low-carbon chemical processes.

Rising political support for carbon pricing—EU ETS prices averaging €90–€100/tCO2 in 2024—favors adoption of JM’s high-efficiency catalysts that lower emissions and operating costs.

- EU ETS ~€90–100/tCO2 (2024)

- UK CCUS investment pipeline £20bn+

- Fit for 55: 55% GHG reduction target by 2030

Policy tailwinds lift Johnson Matthey but PGM supply and tariffs threaten margins

Political support for hydrogen, CCUS and carbon pricing (EU ETS ~€90–100/tCO2 in 2024) and national funds (UK £1.6bn hydrogen to 2025; UK CCUS pipeline £20bn+) boosts Johnson Matthey’s demand, but reliance on South Africa/Russia for ~70% of PGMs and 2–8% high-tech tariffs (2025) create supply and margin risks.

| Metric | 2024/25 |

|---|---|

| EU ETS price | €90–100/tCO2 (2024) |

| UK hydrogen funding | £1.6bn to 2025 |

| PGM supply concentration | ~70% South Africa/Russia |

| High-tech tariffs | 2–8% (2025) |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal factors uniquely impact Johnson Matthey’s catalytic, battery materials and chemicals businesses, backed by current market data and regulatory trends to pinpoint risks and opportunities for executives, investors, and strategists.

Condenses Johnson Matthey's PESTLE insights into a sharp, meeting-ready summary that highlights external risks and opportunities for quick strategic decisions.

Economic factors

Precious Metal Price Volatility

Fluctuations in platinum, palladium and rhodium prices—platinum down ~12% and rhodium up ~8% in 2024 YTD—directly alter Johnson Matthey’s production costs and inventory valuations, impacting gross margins on PGM sales (JM reported PGM margins swinging 200–400 bps in 2023–24). As a global PGM manager, JM is exposed to speculation and mining shocks (SA and Russia supply risks). Hedging programs and scaling recycling—JM’s recycled PGMs rose ~15% in 2024—are vital to mitigate this financial exposure.

Transition in Automotive Markets

The shift from internal combustion engines to EVs, with global EV sales reaching 14.2 million in 2024 (up ~35% year-on-year) and projected to be 30–40% of new car sales by 2030, reduces long-term demand for Johnson Matthey's traditional autocatalysts, risking legacy revenue streams.

Conversely, demand for battery materials (lithium, nickel, cobalt) and hydrogen fuel cell catalysts offers significant upside—battery material markets grew ~22% in 2024 to an estimated $230bn, while green hydrogen capacity targets hit 100 GW+ by 2030 in major economies.

The transition pace—regional EV penetration, 2024 EU ~25%, China ~35%, US ~10%—will drive JM's capital allocation between catalyst legacy units and growth in battery and hydrogen, potentially necessitating restructuring if ICE decline accelerates faster than anticipated.

Inflation and Operational Costs

Rising energy and raw material prices—Brent crude up ~15% in 2024 YTD to ~$90/bbl and nickel up ~22% in 2024—risk squeezing Johnson Matthey margins if price recovery cannot be passed to industrial customers; FY2024 gross margin was 28.6%, showing sensitivity to input costs.

Global manufacturing PMI cycles drive catalyst demand: global manufacturing PMI averaged ~50.2 in 2024, correlating with JM’s FY2024 catalytic demand trends and 3% organic revenue decline in Chemicals.

Maintaining cost efficiency via lean manufacturing and supply-chain optimization remains critical—JM reported a 4% reduction in manufacturing overheads in FY2024 from targeted productivity and procurement initiatives.

R&D Investment Capital

High interest rates raised UK base rate to 5.25% (Jan 2026), increasing borrowing costs for Johnson Matthey’s large-scale R&D in sustainable tech and hydrogen electrolysis projects.

Access to green bonds and equity markets—green bond issuance hit $580bn globally in 2025—remains crucial to commercialize hydrogen and circular-economy solutions.

UK financial stability, reflected in resilient bank CET1 ratios (~14% in 2025), underpins JM’s long-term investment planning.

- Higher rates raise project financing costs

- Green bond market $580bn (2025) vital for commercialization

- UK bank CET1 ~14% supports investment confidence

Currency Exchange Fluctuations

As a multinational, Johnson Matthey faces GBP, USD and EUR volatility; in FY2024 roughly 30% of revenue was USD/EUR-linked, meaning a 5% GBP move could swing reported sterling earnings by ~£40–60m.

Effective treasury management and hedging are essential: JM disclosed in 2024 rolling forward hedges covering a significant portion of near-term FX exposure to stabilize cash flows across regions.

- ~30% revenue USD/EUR-linked (FY2024)

- 5% GBP move ≈ £40–60m P&L impact

- Use of rolling forward hedges to reduce short-term FX volatility

PGM volatility trims margins as EVs cut catalyst demand; batteries & hydrogen offset

PGM price swings (platinum -12%, rhodium +8% 2024 YTD) and 15% recycled PGM growth drove 200–400bps margin volatility; EVs (14.2m sales 2024) cut autocatalyst demand while batteries ($230bn, +22% 2024) and hydrogen (100+ GW by 2030) offer growth; input cost rises (Brent ~$90/bbl, nickel +22% 2024) and FX (30% USD/EUR-linked revenue) plus UK base rate 5.25% raise financing costs.

| Metric | Value |

|---|---|

| Platinum | -12% |

| Rhodium | +8% |

| Recycled PGMs | +15% |

| EV sales 2024 | 14.2m (+35%) |

| Batt. market 2024 | $230bn (+22%) |

| Brent 2024 | ~$90/bbl |

| USD/EUR-linked rev | ~30% |

Preview the Actual Deliverable

Johnson Matthey PESTLE Analysis

The preview shown here is the exact Johnson Matthey PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic insight and decision-making.