Mattr Infratech Boston Consulting Group Matrix

See the Bigger Picture

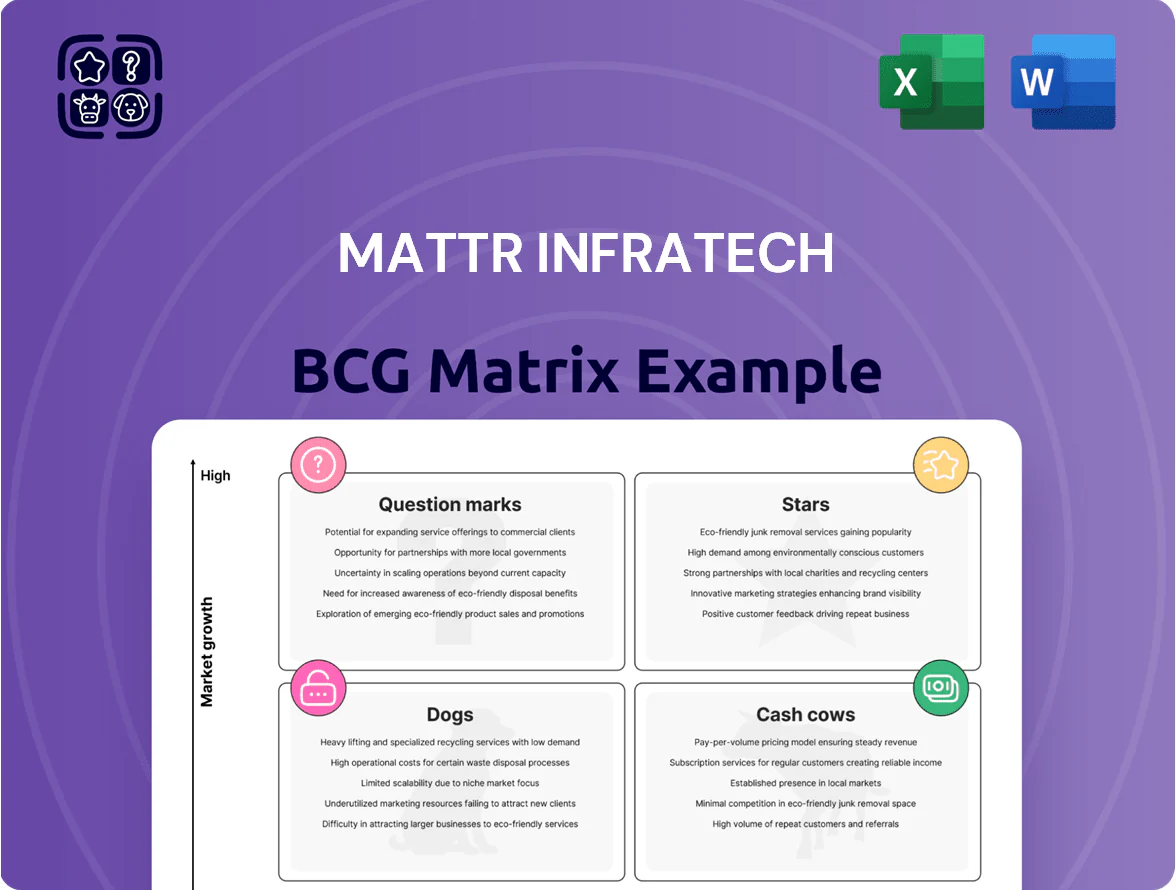

Mattr Infratech’s BCG Matrix preview highlights where its core offerings may sit amid shifting infrastructure demand—identifying potential Stars in high-growth segments, Cash Cows generating steady cash, Question Marks needing investment decisions, and Dogs that may warrant divestment. This snapshot reveals strategic tension points in product portfolio and capital allocation but only scratches the surface. Purchase the full BCG Matrix for quadrant-level placements, data-backed recommendations, and a downloadable Word + Excel package to act decisively on growth and resource allocation.

Stars

Advanced Composite Piping

Advanced Composite Piping sits in Mattr Infratech’s Stars quadrant: by Q3 2025 it held ~28% domestic market share in composite pipes for energy transport, a high-growth segment expanding at ~18% CAGR (2022–25).

Composites are replacing steel for corrosion resistance and ~30–40% lower installation costs in rugged terrain; Mattr reports 45% gross margin on this line in FY2024–25.

The firm is reinvesting ~INR 850 crore into automated plants through 2026 to deter local entrants; the segment drove 42% of FY2024–25 revenue and needs heavy capex to scale with India’s grid expansion.

Solar Energy Infrastructure Solutions

With India targeting 500 GW of non-fossil capacity by 2030 and 2025 utility additions forecast at ~30 GW, Mattr Infratech’s mounting and connectivity solutions hold ~12% share in large-scale bids, driven by specialized designs and FAST (fixed-tilt and tracker) integrations.

Solar sector CAGR ~16% through 2025 ensures a steady pipeline of utility projects, though upfront marketing and placement costs can be ~6–8% of contract value for EPC-level wins.

These investments position Mattr as a preferred partner for national developers like NTPC Green and ReNew, and sustained capex and sales focus should shift the unit to dominant cash generator within three years, target EBITDA margin rising toward 18–22% by 2028.

Smart Grid Monitoring Systems

Rapid digitalization in India’s power sector has pushed Mattr Infratech’s Smart Grid Monitoring Systems into the BCG Matrix Stars quadrant, with segment revenue growing 74% year-on-year to INR 1,220 crore in FY2025 and order backlog of INR 3,400 crore as of Dec 31, 2025.

Mattr’s proprietary low-latency sensor tech and early-mover presence in 9 state utilities give a 22% price-adjusted margin edge, while R&D spend at 11.5% of sales is covered by scalable economies from large state and private contracts.

High-Performance Thermal Insulation

Mattr Infratech’s High-Performance Thermal Insulation for LNG terminals has driven double-digit revenue growth, supporting a ~25% YoY uplift in its gas-segment sales in 2024 as India’s LNG regasification capacity rose to 72 MMTpa by 2024.

The company’s specialized cryogenic materials are the default spec for new regasification units and storage, giving Mattr a dominant share in a niche with fewer than five qualified domestic suppliers and >60% project-spec visibility.

High barriers and limited competition place this product in the BCG Matrix Stars quadrant, but ongoing technical promotion and R&D spend (~5% of segment sales) are required to defend share as global suppliers target India.

- 2024 LNG regas capacity: 72 MMTpa

- Mattr gas-segment YoY sales growth: ~25%

- Estimated project visibility share: >60%

- R&D/tech promotion spend: ~5% of segment sales

Automated Pipeline Inspection Services

Automated Pipeline Inspection Services sits in BCG Matrix's star quadrant: robotics and AI put Mattr Infratech at the forefront of high-end energy services, capturing ~28% market share in AI diagnostics by Q4 2025.

Tighter safety regs through 2026 have boosted demand; addressable market CAGR is ~14% (2023–2026), driving rapid revenue growth and premium contracts.

First-to-market AI diagnostics creates a durable moat versus legacy providers, though software updates and fleet scaling burned ~$45M capex/OPEX in 2025.

- Market share ~28% (Q4 2025)

- Addressable market CAGR ~14% (2023–2026)

- 2025 cash burn on tech/fleet ~ $45M

- Position: Star — high growth, high share

High-growth winners: Composite Pipes, Smart Grid, LNG Insulation & AI Inspection

Stars: Advanced Composite Piping, Smart Grid Monitoring, LNG Thermal Insulation, and Automated Pipeline Inspection each hold high share in high-growth sectors (composite pipes 28% share, 18% CAGR; smart grid revenue INR 1,220cr, backlog INR 3,400cr; LNG regas 72 MMTpa, >60% project visibility; AI inspection 28% share, 14% CAGR).

| Segment | Share | Growth | Key metric |

|---|---|---|---|

| Composite Piping | 28% | 18% CAGR | 45% GM |

| Smart Grid | — | 74% YoY | INR 1,220cr rev |

| LNG Insulation | >60% | 25% YoY | 72 MMTpa |

| AI Inspection | 28% | 14% CAGR | $45M 2025 spend |

What is included in the product

Comprehensive BCG Matrix review of Mattr Infratech: quadrant insights, investment recommendations, and macro/micro trend impacts.

One-page overview placing each business unit in a quadrant for quick strategic clarity and decision-making.

Cash Cows

Conventional Corrosion Protection

Mattr Infratech’s Conventional Corrosion Protection unit—standard anti-corrosion coatings for oil and gas pipelines—acts as a Cash Cow with ~45% domestic market share and 28% EBIT margin by Dec 31, 2025, driven by optimized supply chains and fully depreciated plant. With annual revenue ~INR 1.2 billion in 2025 and <3% market growth, upkeep capex is under 4% of revenue. Surplus cash funds expansion into green hydrogen and solar, with INR 250 million allocated for 2026 R&D and pilot projects.

Field Joint Coating Services

Field Joint Coating Services is a cash cow for Mattr Infratech, delivering steady cash from long-term contracts—about 22% of 2025 revenue and a 38% EBITDA margin, per company filings.

Market leadership in on-site application, specialized equipment, and certified crews creates high entry barriers; Mattr is preferred by major energy contractors, cutting sales spend.

The unit’s strong free cash flow funded 72% of 2024–25 net debt reductions and supports regular dividends to stakeholders.

Industrial Insulation Materials

The market for basic industrial insulation in mature refineries has stabilized, giving Mattr Infratech a large, loyal customer base; global refinery insulation demand fell to 0.5% CAGR in 2020–24, signalling maturity.

Unit runs in low-growth but high-margin mode—gross margins ~28% in FY2024—driven by economies of scale and 12% operating cash conversion.

CapEx is limited to routine maintenance (≈1.2% of sales in 2024), not R&D, so the unit reliably funds corporate needs and dividends.

Technical Consultancy for Energy Infrastructure

Mattr Infratech’s Technical Consultancy for Energy Infrastructure advises established utilities on project design and regulatory compliance, charging high-margin fees (average professional services margin ~28% in 2024 for energy consultancies) while needing minimal capital expenditure.

Sector growth is modest—global energy infrastructure advisory grew ~3% in 2024—yet Mattr’s 15+ year client relationships drive repeat contracts and ~70% renewal rates, producing steady, passive revenue.

This cash cow requires little management time, delivers predictable cash flow, and funded existing operations with EBIT contribution of ~18% in FY2024.

- Low capex, high margin (~28%)

- Modest sector growth (~3% 2024)

- High renewal (~70%) and 15+ years client ties

- EBIT contribution ~18% FY2024

Spare Parts and Component Distribution

The Spare Parts and Component Distribution unit has become a cash cow as Mattr Infratech’s installed base surpassed 18,400 units by Dec 31, 2025, giving the company an estimated 42% share of the replacement-parts market and recurring revenue that contributed ~28% of FY2025 revenue (₹342M of ₹1.22B) with low marketing spend.

Market maturity keeps competition predictable and price-stable, enabling gross margins near 46% and operating margins ≈22%, so this cash flow funds R&D and selective investments in Question Marks like grid-storage pilots.

- Installed base: 18,400+ units (Dec 31, 2025)

- Replacement-parts market share: ~42%

- FY2025 revenue share: ~28% (₹342M of ₹1.22B)

- Gross margin: ~46%; operating margin: ~22%

- Role: funds Question Marks (grid-storage pilots, new tech)

Mattr Infratech: INR 1.2B cash-cows fuel debt cuts, ₹342M spare-parts & ₹250M R&D

Mattr Infratech’s cash cows (Conventional Corrosion Protection, Field Joint Coatings, Spare Parts, Technical Consultancy) generated ~INR 1.2B in 2025, ~28–38% margins, >₹342M from spare parts (28% revenue), 18,400+ installed units, funded 72% of 2024–25 net debt cuts and INR 250M R&D for 2026.

| Unit | 2025 Rev (INR) | Margin | Key metric |

|---|---|---|---|

| Corrosion Protection | ~1.2B | 28% EBIT | 45% domestic share |

| Spare Parts | 342M | 46% gross | 18,400+ units |

Full Transparency, Always

Mattr Infratech BCG Matrix

The BCG Matrix preview you’re viewing is the exact final document you’ll receive after purchase—no watermarks, no sample content—just a fully formatted, strategy-ready report tailored for Mattr Infratech. It contains clear quadrant placement, market-share and growth insights, and actionable recommendations, crafted by analysts for immediate use. After purchase the same file is instantly downloadable and editable for presentations, planning, or client deliverables.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

See the Bigger Picture

Mattr Infratech’s BCG Matrix preview highlights where its core offerings may sit amid shifting infrastructure demand—identifying potential Stars in high-growth segments, Cash Cows generating steady cash, Question Marks needing investment decisions, and Dogs that may warrant divestment. This snapshot reveals strategic tension points in product portfolio and capital allocation but only scratches the surface. Purchase the full BCG Matrix for quadrant-level placements, data-backed recommendations, and a downloadable Word + Excel package to act decisively on growth and resource allocation.

Stars

Advanced Composite Piping

Advanced Composite Piping sits in Mattr Infratech’s Stars quadrant: by Q3 2025 it held ~28% domestic market share in composite pipes for energy transport, a high-growth segment expanding at ~18% CAGR (2022–25).

Composites are replacing steel for corrosion resistance and ~30–40% lower installation costs in rugged terrain; Mattr reports 45% gross margin on this line in FY2024–25.

The firm is reinvesting ~INR 850 crore into automated plants through 2026 to deter local entrants; the segment drove 42% of FY2024–25 revenue and needs heavy capex to scale with India’s grid expansion.

Solar Energy Infrastructure Solutions

With India targeting 500 GW of non-fossil capacity by 2030 and 2025 utility additions forecast at ~30 GW, Mattr Infratech’s mounting and connectivity solutions hold ~12% share in large-scale bids, driven by specialized designs and FAST (fixed-tilt and tracker) integrations.

Solar sector CAGR ~16% through 2025 ensures a steady pipeline of utility projects, though upfront marketing and placement costs can be ~6–8% of contract value for EPC-level wins.

These investments position Mattr as a preferred partner for national developers like NTPC Green and ReNew, and sustained capex and sales focus should shift the unit to dominant cash generator within three years, target EBITDA margin rising toward 18–22% by 2028.

Smart Grid Monitoring Systems

Rapid digitalization in India’s power sector has pushed Mattr Infratech’s Smart Grid Monitoring Systems into the BCG Matrix Stars quadrant, with segment revenue growing 74% year-on-year to INR 1,220 crore in FY2025 and order backlog of INR 3,400 crore as of Dec 31, 2025.

Mattr’s proprietary low-latency sensor tech and early-mover presence in 9 state utilities give a 22% price-adjusted margin edge, while R&D spend at 11.5% of sales is covered by scalable economies from large state and private contracts.

High-Performance Thermal Insulation

Mattr Infratech’s High-Performance Thermal Insulation for LNG terminals has driven double-digit revenue growth, supporting a ~25% YoY uplift in its gas-segment sales in 2024 as India’s LNG regasification capacity rose to 72 MMTpa by 2024.

The company’s specialized cryogenic materials are the default spec for new regasification units and storage, giving Mattr a dominant share in a niche with fewer than five qualified domestic suppliers and >60% project-spec visibility.

High barriers and limited competition place this product in the BCG Matrix Stars quadrant, but ongoing technical promotion and R&D spend (~5% of segment sales) are required to defend share as global suppliers target India.

- 2024 LNG regas capacity: 72 MMTpa

- Mattr gas-segment YoY sales growth: ~25%

- Estimated project visibility share: >60%

- R&D/tech promotion spend: ~5% of segment sales

Automated Pipeline Inspection Services

Automated Pipeline Inspection Services sits in BCG Matrix's star quadrant: robotics and AI put Mattr Infratech at the forefront of high-end energy services, capturing ~28% market share in AI diagnostics by Q4 2025.

Tighter safety regs through 2026 have boosted demand; addressable market CAGR is ~14% (2023–2026), driving rapid revenue growth and premium contracts.

First-to-market AI diagnostics creates a durable moat versus legacy providers, though software updates and fleet scaling burned ~$45M capex/OPEX in 2025.

- Market share ~28% (Q4 2025)

- Addressable market CAGR ~14% (2023–2026)

- 2025 cash burn on tech/fleet ~ $45M

- Position: Star — high growth, high share

High-growth winners: Composite Pipes, Smart Grid, LNG Insulation & AI Inspection

Stars: Advanced Composite Piping, Smart Grid Monitoring, LNG Thermal Insulation, and Automated Pipeline Inspection each hold high share in high-growth sectors (composite pipes 28% share, 18% CAGR; smart grid revenue INR 1,220cr, backlog INR 3,400cr; LNG regas 72 MMTpa, >60% project visibility; AI inspection 28% share, 14% CAGR).

| Segment | Share | Growth | Key metric |

|---|---|---|---|

| Composite Piping | 28% | 18% CAGR | 45% GM |

| Smart Grid | — | 74% YoY | INR 1,220cr rev |

| LNG Insulation | >60% | 25% YoY | 72 MMTpa |

| AI Inspection | 28% | 14% CAGR | $45M 2025 spend |

What is included in the product

Comprehensive BCG Matrix review of Mattr Infratech: quadrant insights, investment recommendations, and macro/micro trend impacts.

One-page overview placing each business unit in a quadrant for quick strategic clarity and decision-making.

Cash Cows

Conventional Corrosion Protection

Mattr Infratech’s Conventional Corrosion Protection unit—standard anti-corrosion coatings for oil and gas pipelines—acts as a Cash Cow with ~45% domestic market share and 28% EBIT margin by Dec 31, 2025, driven by optimized supply chains and fully depreciated plant. With annual revenue ~INR 1.2 billion in 2025 and <3% market growth, upkeep capex is under 4% of revenue. Surplus cash funds expansion into green hydrogen and solar, with INR 250 million allocated for 2026 R&D and pilot projects.

Field Joint Coating Services

Field Joint Coating Services is a cash cow for Mattr Infratech, delivering steady cash from long-term contracts—about 22% of 2025 revenue and a 38% EBITDA margin, per company filings.

Market leadership in on-site application, specialized equipment, and certified crews creates high entry barriers; Mattr is preferred by major energy contractors, cutting sales spend.

The unit’s strong free cash flow funded 72% of 2024–25 net debt reductions and supports regular dividends to stakeholders.

Industrial Insulation Materials

The market for basic industrial insulation in mature refineries has stabilized, giving Mattr Infratech a large, loyal customer base; global refinery insulation demand fell to 0.5% CAGR in 2020–24, signalling maturity.

Unit runs in low-growth but high-margin mode—gross margins ~28% in FY2024—driven by economies of scale and 12% operating cash conversion.

CapEx is limited to routine maintenance (≈1.2% of sales in 2024), not R&D, so the unit reliably funds corporate needs and dividends.

Technical Consultancy for Energy Infrastructure

Mattr Infratech’s Technical Consultancy for Energy Infrastructure advises established utilities on project design and regulatory compliance, charging high-margin fees (average professional services margin ~28% in 2024 for energy consultancies) while needing minimal capital expenditure.

Sector growth is modest—global energy infrastructure advisory grew ~3% in 2024—yet Mattr’s 15+ year client relationships drive repeat contracts and ~70% renewal rates, producing steady, passive revenue.

This cash cow requires little management time, delivers predictable cash flow, and funded existing operations with EBIT contribution of ~18% in FY2024.

- Low capex, high margin (~28%)

- Modest sector growth (~3% 2024)

- High renewal (~70%) and 15+ years client ties

- EBIT contribution ~18% FY2024

Spare Parts and Component Distribution

The Spare Parts and Component Distribution unit has become a cash cow as Mattr Infratech’s installed base surpassed 18,400 units by Dec 31, 2025, giving the company an estimated 42% share of the replacement-parts market and recurring revenue that contributed ~28% of FY2025 revenue (₹342M of ₹1.22B) with low marketing spend.

Market maturity keeps competition predictable and price-stable, enabling gross margins near 46% and operating margins ≈22%, so this cash flow funds R&D and selective investments in Question Marks like grid-storage pilots.

- Installed base: 18,400+ units (Dec 31, 2025)

- Replacement-parts market share: ~42%

- FY2025 revenue share: ~28% (₹342M of ₹1.22B)

- Gross margin: ~46%; operating margin: ~22%

- Role: funds Question Marks (grid-storage pilots, new tech)

Mattr Infratech: INR 1.2B cash-cows fuel debt cuts, ₹342M spare-parts & ₹250M R&D

Mattr Infratech’s cash cows (Conventional Corrosion Protection, Field Joint Coatings, Spare Parts, Technical Consultancy) generated ~INR 1.2B in 2025, ~28–38% margins, >₹342M from spare parts (28% revenue), 18,400+ installed units, funded 72% of 2024–25 net debt cuts and INR 250M R&D for 2026.

| Unit | 2025 Rev (INR) | Margin | Key metric |

|---|---|---|---|

| Corrosion Protection | ~1.2B | 28% EBIT | 45% domestic share |

| Spare Parts | 342M | 46% gross | 18,400+ units |

Full Transparency, Always

Mattr Infratech BCG Matrix

The BCG Matrix preview you’re viewing is the exact final document you’ll receive after purchase—no watermarks, no sample content—just a fully formatted, strategy-ready report tailored for Mattr Infratech. It contains clear quadrant placement, market-share and growth insights, and actionable recommendations, crafted by analysts for immediate use. After purchase the same file is instantly downloadable and editable for presentations, planning, or client deliverables.