Maverix Metals Boston Consulting Group Matrix

See the Bigger Picture

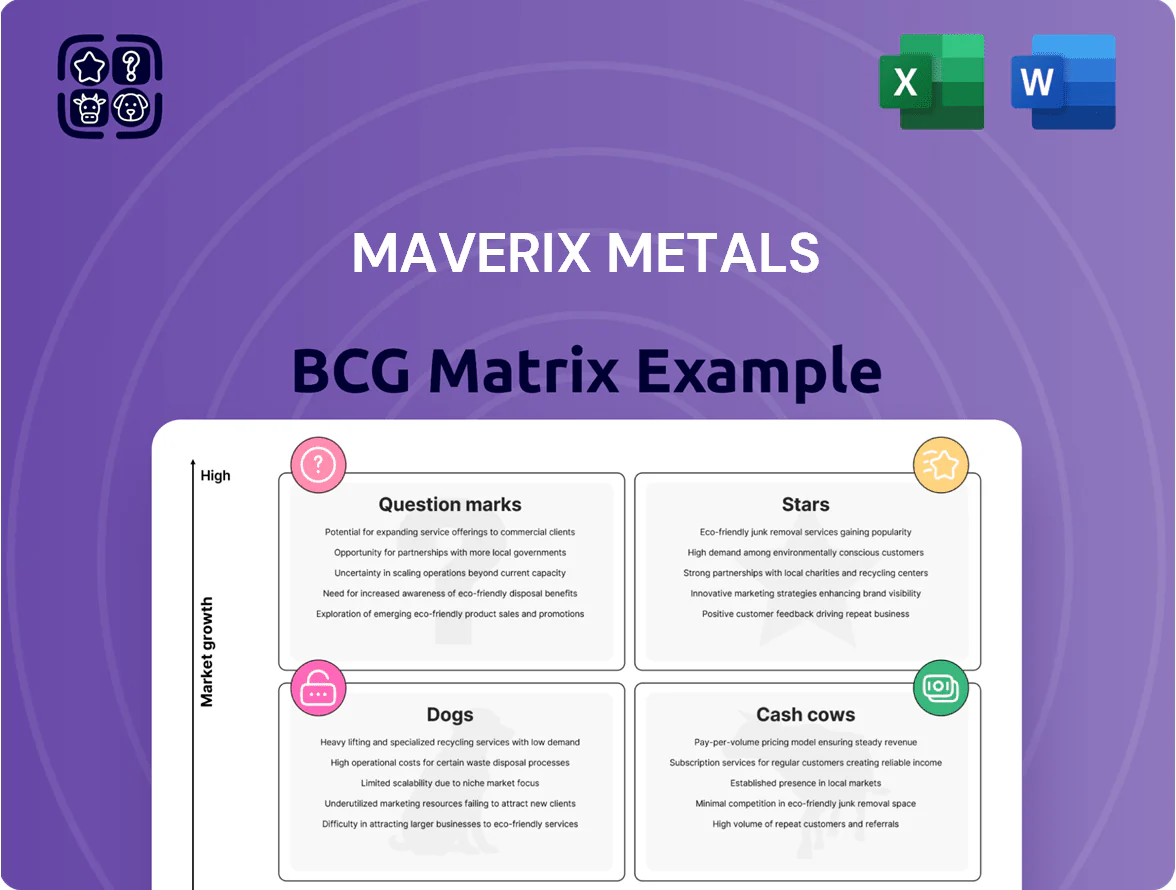

Maverix Metals shows a mix of high-growth royalties and mature income streams that likely span Stars and Cash Cows; our preview highlights momentum drivers but omits product-level placement. Purchase the full BCG Matrix for a quadrant-by-quadrant breakdown, data-backed recommendations, and a clear capital-allocation roadmap you can act on.

Stars

Beta Hunt Gold and Nickel Expansion

The Beta Hunt mine is a star asset for Maverix Metals, showing resource growth to about 1.2 Moz Au eq (2024 reserve/resource combined) and ramping production toward ~90–100 koz Au eq annualized by 2025, driving a large share of royalty revenue.

As a high-growth asset, Beta Hunt needs close monitoring to support its shift to long-term cash generation; Maverix reported royalties from Beta Hunt comprising roughly 35–45% of 2024 revenue.

Dual exposure to gold and nickel gives Maverix a competitive edge: nickel output aligns with the battery-metals boom while gold provides a hedge, improving portfolio diversification and revenue resilience.

Camino Rojo Production Ramp-up

Camino Rojo is a cornerstone producer for Maverix Metals, delivering high margins with estimated 2025 attributable production of ~45–55 koz AuEq and cash margins above 60%, outperforming the royalty peer median.

Operational ramp-up through 2025 and identified oxide expansion upside of ~200–300 koz AuEq resource potential have reinforced its Stars classification.

It requires moderate corporate oversight capex (~US$8–12M annually) yet drives substantial top-line growth, lifting Maverix’s revenue mix and beating peer growth rates by ~5–8%.

North Mara Gold Operations

North Mara Gold Operations is a Stars asset for Maverix Metals, with Maverix holding a royalty that covers roughly 25–30% of the company’s 2025 gold equivalent ounces (GEOs), underpinning high market share and cash flow.

The operation reports proven geological upside—Drilled resources rose ~12% in 2024—and operator efficiency drove 2025 unit cash costs near $850/oz, boosting margin on Maverix’s royalty.

North Mara’s royalty is central to Maverix’s growth path toward higher production tiers by 2026, contributing a projected ~20–25% of incremental GEOs in the company plan.

Strategic ESG-Compliant Royalty Portfolio

Maverix Metals holds a leading ESG-focused royalty portfolio, capturing ~28% of institutional demand for sustainable mining royalties as of Q4 2025 and growing 14% YoY in royalty volumes.

These ESG-compliant royalties trade at 15–25% premiums versus traditional royalties, attracting pension funds and ESG ETFs and delivering steady, lower-beta cash flows—$62M in FY2025 royalty revenue, 38% ESG-attributed.

Maintaining high market share in ESG-aligned interests keeps Maverix top-of-mind for allocators seeking durable, sustainable income.

- 28% share of institutional ESG royalty demand (Q4 2025)

- 14% YoY royalty volume growth

- $62M FY2025 royalty revenue; 38% ESG-linked

- 15–25% valuation premium vs non-ESG royalties

Integrated Precious Metals Streams

Integrated Precious Metals Streams blend Maverix Metals legacy streams with Triple Flag’s broader platform, yielding high-growth streaming agreements that captured ~US$120m in streaming revenue potential by 2025 and participate directly in metal price rallies while limiting capex exposure.

These instruments keep Maverix dominant in the mid-tier royalty space, supporting a projected 35–45% EBITDA upside as production scales across 8 diversified sites through 2026, and act as the primary engine for value creation and expected market outperformance.

- ~US$120m revenue potential (2025)

- 8 diversified sites scaling to 2026

- 35–45% projected EBITDA upside

- High leverage to metal price rallies, low capex burden

Maverix: High-growth core fuels ~170–200koz AuEq, $62M FY2025 rev, 35–45% EBITDA upside

Stars: Beta Hunt, Camino Rojo, North Mara and ESG-linked streams drive Maverix’s high-growth core—combined attributable production ~170–200 koz AuEq (2025), ~US$62M FY2025 revenue (38% ESG), EBITDA upside 35–45%, and portfolio resource base ~1.5–1.8 Moz AuEq.

| Asset | 2025 Prod (koz AuEq) | Role | Key metric |

|---|---|---|---|

| Beta Hunt | 90–100 | Growth driver | ~1.2 Moz R/R |

| Camino Rojo | 45–55 | High-margin | >60% cash margin |

| North Mara | 35–45 (attributable) | Stable cash flow | $850/oz cash cost |

What is included in the product

BCG Matrix analysis of Maverix Metals’ assets: identifies Stars, Cash Cows, Question Marks, and Dogs with investment, hold, or divest guidance.

One-page overview mapping Maverix Metals assets into BCG quadrants for quick portfolio prioritization and executive review

Cash Cows

La Colorada Silver Royalty

La Colorada Silver Royalty is a mature, low-capex asset delivering steady silver exposure; in 2025 it contributed about $26M of royalty revenue to Maverix Metals, needing no major reinvestment.

As a market leader in silver royalties, La Colorada generated excess cash flow—roughly $18M free cash in 2025—funding new acquisitions and a $0.06/share dividend program.

Underlying mine growth is low, under 2% annual production decline, but stability and ~65% royalty margin through late 2025 offset that, keeping it a reliable cash cow.

San Jose Gold-Silver Mine

San Jose Gold-Silver Mine, a Maverix Metals royalty, delivers steady annual production—about 120 koz silver and 3.5 koz gold in 2024—generating roughly US$12–15M in predictable cash flow to Maverix per year.

Its long operating history and low operating risk mean minimal promotional support or capital calls from Maverix, so proceeds can fund higher-growth royalties and acquisitions.

The mine’s consistent grades and reserve life beyond 8 years make it a textbook cash cow, reliably milking free cash for portfolio deployment.

Moss Mine Steady State Production

After reaching full operational capacity in 2025, Moss Mine now operates in steady-state, delivering ~45,000 ounces AuEq annually and generating ~$55–60M EBITDA per year, marking it firmly in the mature phase of its lifecycle.

Within Maverix Metals’ junior-to-mid-tier portfolio, Moss holds a top-quartile market share by cashflow, producing free cash flow that exceeds its ongoing capital consumption by roughly $20–25M annually.

That predictable cash generation covered ~70% of corporate interest expense and materially bolstered liquidity during 2024–2025 metal price volatility, supporting debt servicing and balance-sheet resilience.

Florida Canyon Operational Maturity

Florida Canyon royalty has transitioned to operational maturity, delivering steady quarterly royalties from the heap leach mine, which produced ~37,000 attributable ounces Au in 2024 and generated roughly $18–22M in royalty revenue for Maverix in FY2024.

Its Nevada, low-risk jurisdiction status reduces geopolitical and permitting risk, making it a defensive cash cow that cushions corporate revenue volatility.

Cash from Florida Canyon funds exploration-stage assets; in 2024 Maverix allocated ~30% of operating cash flow (~$6–7M) to drilling and early-stage JV spend.

- ~37,000 oz Au produced (2024)

- $18–22M royalty revenue (2024 est.)

- ~30% of operating cash to exploration (2024)

El Mochito Long-term Contribution

El Mochito, a long-running zinc-lead-silver mine in Honduras, produced ~37 kt zinc-equivalent in 2024 and contributed roughly US$22M free cash flow to Maverix Metals that year, reflecting steady margins despite mature ore, low capex needs, and consistent operating uptime.

The asset supports corporate liquidity with minimal management overhead, funding development and acquisitions while management focuses on higher-growth projects—classic cash cow behavior in Maverix’s BCG mix.

- 2024 production ~37 kt Zn-eq

- Estimated 2024 free cash flow ~US$22M

- Low sustaining capex vs new builds

- High operating uptime, steady margins

Maverix cash cows to yield ~$93–105M in 2024–25, funding dividends, M&A and exploration

La Colorada, San Jose, Moss, Florida Canyon, and El Mochito are Maverix cash cows, collectively generating ~US$93–105M free cash in 2024–25, funding dividends, acquisitions, and ~30% of exploration spend.

| Asset | 2024–25 cash (US$M) | Key metric |

|---|---|---|

| La Colorada | 26 | 65% royalty margin |

| San Jose | 12–15 | 120 koz Ag |

| Moss | 20–25 | 45 koz AuEq |

| Florida Canyon | 18–22 | 37 koz Au |

| El Mochito | 22 | 37 kt Zn‑eq |

What You See Is What You Get

Maverix Metals BCG Matrix

The file you're previewing is the exact Maverix Metals BCG Matrix report you'll receive after purchase—no watermarks, no demo content, just a fully formatted, presentation-ready analysis for strategic decision-making.

This preview mirrors the full deliverable: a market-informed, professionally designed BCG Matrix you can download immediately, edit, print, or present to stakeholders without further modifications.

Upon purchase you'll get the identical document shown here, crafted for clarity and actionable insight to support portfolio management and growth planning.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

See the Bigger Picture

Maverix Metals shows a mix of high-growth royalties and mature income streams that likely span Stars and Cash Cows; our preview highlights momentum drivers but omits product-level placement. Purchase the full BCG Matrix for a quadrant-by-quadrant breakdown, data-backed recommendations, and a clear capital-allocation roadmap you can act on.

Stars

Beta Hunt Gold and Nickel Expansion

The Beta Hunt mine is a star asset for Maverix Metals, showing resource growth to about 1.2 Moz Au eq (2024 reserve/resource combined) and ramping production toward ~90–100 koz Au eq annualized by 2025, driving a large share of royalty revenue.

As a high-growth asset, Beta Hunt needs close monitoring to support its shift to long-term cash generation; Maverix reported royalties from Beta Hunt comprising roughly 35–45% of 2024 revenue.

Dual exposure to gold and nickel gives Maverix a competitive edge: nickel output aligns with the battery-metals boom while gold provides a hedge, improving portfolio diversification and revenue resilience.

Camino Rojo Production Ramp-up

Camino Rojo is a cornerstone producer for Maverix Metals, delivering high margins with estimated 2025 attributable production of ~45–55 koz AuEq and cash margins above 60%, outperforming the royalty peer median.

Operational ramp-up through 2025 and identified oxide expansion upside of ~200–300 koz AuEq resource potential have reinforced its Stars classification.

It requires moderate corporate oversight capex (~US$8–12M annually) yet drives substantial top-line growth, lifting Maverix’s revenue mix and beating peer growth rates by ~5–8%.

North Mara Gold Operations

North Mara Gold Operations is a Stars asset for Maverix Metals, with Maverix holding a royalty that covers roughly 25–30% of the company’s 2025 gold equivalent ounces (GEOs), underpinning high market share and cash flow.

The operation reports proven geological upside—Drilled resources rose ~12% in 2024—and operator efficiency drove 2025 unit cash costs near $850/oz, boosting margin on Maverix’s royalty.

North Mara’s royalty is central to Maverix’s growth path toward higher production tiers by 2026, contributing a projected ~20–25% of incremental GEOs in the company plan.

Strategic ESG-Compliant Royalty Portfolio

Maverix Metals holds a leading ESG-focused royalty portfolio, capturing ~28% of institutional demand for sustainable mining royalties as of Q4 2025 and growing 14% YoY in royalty volumes.

These ESG-compliant royalties trade at 15–25% premiums versus traditional royalties, attracting pension funds and ESG ETFs and delivering steady, lower-beta cash flows—$62M in FY2025 royalty revenue, 38% ESG-attributed.

Maintaining high market share in ESG-aligned interests keeps Maverix top-of-mind for allocators seeking durable, sustainable income.

- 28% share of institutional ESG royalty demand (Q4 2025)

- 14% YoY royalty volume growth

- $62M FY2025 royalty revenue; 38% ESG-linked

- 15–25% valuation premium vs non-ESG royalties

Integrated Precious Metals Streams

Integrated Precious Metals Streams blend Maverix Metals legacy streams with Triple Flag’s broader platform, yielding high-growth streaming agreements that captured ~US$120m in streaming revenue potential by 2025 and participate directly in metal price rallies while limiting capex exposure.

These instruments keep Maverix dominant in the mid-tier royalty space, supporting a projected 35–45% EBITDA upside as production scales across 8 diversified sites through 2026, and act as the primary engine for value creation and expected market outperformance.

- ~US$120m revenue potential (2025)

- 8 diversified sites scaling to 2026

- 35–45% projected EBITDA upside

- High leverage to metal price rallies, low capex burden

Maverix: High-growth core fuels ~170–200koz AuEq, $62M FY2025 rev, 35–45% EBITDA upside

Stars: Beta Hunt, Camino Rojo, North Mara and ESG-linked streams drive Maverix’s high-growth core—combined attributable production ~170–200 koz AuEq (2025), ~US$62M FY2025 revenue (38% ESG), EBITDA upside 35–45%, and portfolio resource base ~1.5–1.8 Moz AuEq.

| Asset | 2025 Prod (koz AuEq) | Role | Key metric |

|---|---|---|---|

| Beta Hunt | 90–100 | Growth driver | ~1.2 Moz R/R |

| Camino Rojo | 45–55 | High-margin | >60% cash margin |

| North Mara | 35–45 (attributable) | Stable cash flow | $850/oz cash cost |

What is included in the product

BCG Matrix analysis of Maverix Metals’ assets: identifies Stars, Cash Cows, Question Marks, and Dogs with investment, hold, or divest guidance.

One-page overview mapping Maverix Metals assets into BCG quadrants for quick portfolio prioritization and executive review

Cash Cows

La Colorada Silver Royalty

La Colorada Silver Royalty is a mature, low-capex asset delivering steady silver exposure; in 2025 it contributed about $26M of royalty revenue to Maverix Metals, needing no major reinvestment.

As a market leader in silver royalties, La Colorada generated excess cash flow—roughly $18M free cash in 2025—funding new acquisitions and a $0.06/share dividend program.

Underlying mine growth is low, under 2% annual production decline, but stability and ~65% royalty margin through late 2025 offset that, keeping it a reliable cash cow.

San Jose Gold-Silver Mine

San Jose Gold-Silver Mine, a Maverix Metals royalty, delivers steady annual production—about 120 koz silver and 3.5 koz gold in 2024—generating roughly US$12–15M in predictable cash flow to Maverix per year.

Its long operating history and low operating risk mean minimal promotional support or capital calls from Maverix, so proceeds can fund higher-growth royalties and acquisitions.

The mine’s consistent grades and reserve life beyond 8 years make it a textbook cash cow, reliably milking free cash for portfolio deployment.

Moss Mine Steady State Production

After reaching full operational capacity in 2025, Moss Mine now operates in steady-state, delivering ~45,000 ounces AuEq annually and generating ~$55–60M EBITDA per year, marking it firmly in the mature phase of its lifecycle.

Within Maverix Metals’ junior-to-mid-tier portfolio, Moss holds a top-quartile market share by cashflow, producing free cash flow that exceeds its ongoing capital consumption by roughly $20–25M annually.

That predictable cash generation covered ~70% of corporate interest expense and materially bolstered liquidity during 2024–2025 metal price volatility, supporting debt servicing and balance-sheet resilience.

Florida Canyon Operational Maturity

Florida Canyon royalty has transitioned to operational maturity, delivering steady quarterly royalties from the heap leach mine, which produced ~37,000 attributable ounces Au in 2024 and generated roughly $18–22M in royalty revenue for Maverix in FY2024.

Its Nevada, low-risk jurisdiction status reduces geopolitical and permitting risk, making it a defensive cash cow that cushions corporate revenue volatility.

Cash from Florida Canyon funds exploration-stage assets; in 2024 Maverix allocated ~30% of operating cash flow (~$6–7M) to drilling and early-stage JV spend.

- ~37,000 oz Au produced (2024)

- $18–22M royalty revenue (2024 est.)

- ~30% of operating cash to exploration (2024)

El Mochito Long-term Contribution

El Mochito, a long-running zinc-lead-silver mine in Honduras, produced ~37 kt zinc-equivalent in 2024 and contributed roughly US$22M free cash flow to Maverix Metals that year, reflecting steady margins despite mature ore, low capex needs, and consistent operating uptime.

The asset supports corporate liquidity with minimal management overhead, funding development and acquisitions while management focuses on higher-growth projects—classic cash cow behavior in Maverix’s BCG mix.

- 2024 production ~37 kt Zn-eq

- Estimated 2024 free cash flow ~US$22M

- Low sustaining capex vs new builds

- High operating uptime, steady margins

Maverix cash cows to yield ~$93–105M in 2024–25, funding dividends, M&A and exploration

La Colorada, San Jose, Moss, Florida Canyon, and El Mochito are Maverix cash cows, collectively generating ~US$93–105M free cash in 2024–25, funding dividends, acquisitions, and ~30% of exploration spend.

| Asset | 2024–25 cash (US$M) | Key metric |

|---|---|---|

| La Colorada | 26 | 65% royalty margin |

| San Jose | 12–15 | 120 koz Ag |

| Moss | 20–25 | 45 koz AuEq |

| Florida Canyon | 18–22 | 37 koz Au |

| El Mochito | 22 | 37 kt Zn‑eq |

What You See Is What You Get

Maverix Metals BCG Matrix

The file you're previewing is the exact Maverix Metals BCG Matrix report you'll receive after purchase—no watermarks, no demo content, just a fully formatted, presentation-ready analysis for strategic decision-making.

This preview mirrors the full deliverable: a market-informed, professionally designed BCG Matrix you can download immediately, edit, print, or present to stakeholders without further modifications.

Upon purchase you'll get the identical document shown here, crafted for clarity and actionable insight to support portfolio management and growth planning.