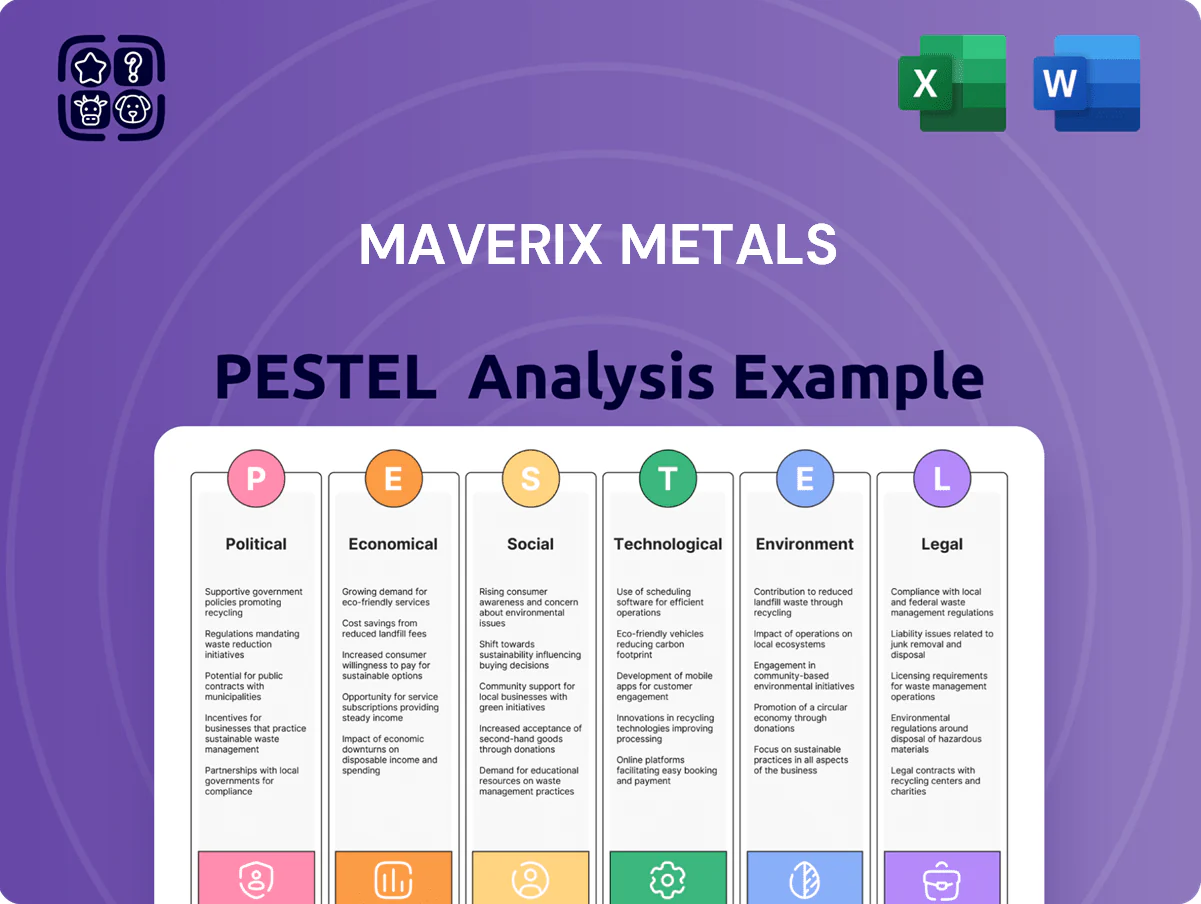

Maverix Metals PESTLE Analysis

Your Competitive Advantage Starts with This Report

Our Maverix Metals PESTLE Analysis reveals how regulatory shifts, commodity cycles, ESG pressures, and technology trends are shaping its strategic outlook—insights vital for investors and strategists alike. Ready-made and research-backed, this briefing highlights risks and opportunities you can act on immediately. Purchase the full PESTLE to get the complete, editable report and make smarter, faster decisions.

Political factors

Geopolitical stability in Tier 1 jurisdictions

Maverix Metals holds over 70% of its royalty portfolio in Tier 1 jurisdictions—Australia, Canada and the United States—providing a stable legal and fiscal environment through 2025 and protecting recurring cash flows from sudden expropriation risks.

This concentration supports predictability: these markets accounted for roughly 68% of Maverix’s FY2024 revenue and underpin projected 2025 cash royalties estimated at US$45–50 million.

Focusing on politically stable jurisdictions mitigates exposure to regulatory volatility and security risks common in emerging mining frontiers, preserving asset values and financing access.

Resource nationalism in emerging markets

While Maverix Metals’ core royalties sit in stable jurisdictions, exposure to projects in developing nations faces increased resource nationalism; IMF data shows 18% of emerging-market governments revised mining codes upward since 2020, raising fiscal take and renegotiation risk.

Higher state participation or royalty rate hikes can delay operator production; PwC reported average project delays of 12–24 months after policy shifts in 2022–2024, affecting Maverix cash flows.

Constant monitoring of local legislative trends is essential to ensure royalty enforceability and margins; in 2024 Maverix reported 6% sensitivity in NAV to a 5 percentage-point increase in government take on select assets.

Government incentives for critical and precious metals

By late 2025, over 20 countries launched strategic initiatives to boost domestic critical and precious metals output; Canada and Australia expanded mine support programs totaling roughly CAD 3.4bn and AUD 2.1bn respectively, increasing project permitting and financing activity.

Governments offer tax credits, grants and low-interest loans that lower capex for Maverix partners, indirectly accelerating royalty cashflows as mine builds shorten; studies show incentives can cut upfront project costs by 10–25%.

Political backing reduces financing hurdles for expansions, improving portfolio NPV; for typical mid-tier projects, incentive-driven capex reductions translate into 5–15% higher long-term royalty values.

Trade policies and export restrictions

Global trade tensions in 2025 raised tariffs on mining equipment by up to 15% between major blocs, while export quotas on gold and silver from some producing countries tightened supply, lifting average spot gold volatility to 22% YTD and increasing capital expenditure per mine by ~8%.

Tariffs and quotas compress margins for miners supplying stream agreements; a 5–10% rise in input costs can reduce streaming yields materially, pushing Maverix to favor counterparties with diversified export routes and low geopolitical exposure.

- Equipment tariffs up to 15% in 2025

- Gold volatility ~22% YTD

- Mine capex +8% vs prior year

- Streaming yields vulnerable to 5–10% input cost rise

Stability of international tax regimes

The business must navigate complex international tax laws governing cross-border royalty and streaming income; in 2025 the OECD two-pillar BEPS reforms and a 15% global minimum tax affect mining cash flows, with modelled impacts reducing after-tax receipts by up to 3–8% in higher-tax jurisdictions.

Changes in withholding tax treaties and recent treaty updates in 2024–25 can raise withholding rates on royalties, potentially cutting Maverix Metals’ foreign net cash flow; maintaining a robust corporate structure is essential to preserve shareholder returns.

- OECD global minimum tax 15% in force (2024–25) may reduce after-tax income 3–8%

- Withholding tax treaty changes in 2024–25 raise royalty rates in select jurisdictions

- Robust corporate structure and tax planning needed to protect shareholder cash flows

Maverix: 70% Tier‑1 Exposure Secures ~68% FY24 Revenue; 2025 Royalties US$45–50M

Maverix’s 70% exposure to Australia, Canada, US secures ~68% of FY2024 revenue and projected 2025 royalties of US$45–50M, reducing expropriation risk; IMF shows 18% of emerging markets raised mining taxes since 2020, causing 12–24 month delays (PwC) and NAV sensitivity ~6% to a 5pp government take; OECD 15% minimum tax may cut after-tax receipts 3–8%.

| Metric | Value |

|---|---|

| Tier‑1 portfolio % | 70% |

| FY2024 revenue from Tier‑1 | ~68% |

| 2025 projected royalties | US$45–50M |

| Emerging-market tax hikes since 2020 | 18% |

| OECD minimum tax impact | -3–8% after‑tax |

What is included in the product

Explores how external macro-environmental factors uniquely affect Maverix Metals across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven insights and region-specific trends.

A concise, shareable PESTLE snapshot of Maverix Metals that highlights external risks and opportunities for quick inclusion in presentations, team briefings, or advisor reports.

Economic factors

Precious metal price volatility

Revenue for Maverix Metals is highly correlated with gold and silver prices; gold averaged about 2,140 USD/oz and silver 26 USD/oz in 2024, and by end-2025 central bank rate moves and safe-haven flows caused quarterly revenue swings of ±18-25% year-over-year.

Because Maverix pays no operating costs to producers, it is effectively leveraged to price increases—each 10% rise in gold spot adds roughly 9–12% to gross revenue—while being insulated from mine-level inflation reported at ~6% in 2024.

Inflationary pressures on mine operating costs

Although Maverix Metals’ royalty model shields it from direct operating costs, extreme inflation—Canada CPI rose 3.4% in 2025 vs 2024—can render hosted mines uneconomic, risking closures that cut royalty tonnage. Surging diesel (up ~20% YoY in 2024) and labor cost inflation squeeze operator margins, prompting production suspensions or deferred expansions that lower metal delivered to Maverix. Monitoring partner margin metrics, including AISC and EBITDA trends, is critical to forecast royalty cash flow stability.

Interest rate environment and cost of capital

At end-2025, global policy rates averaged ~5.1% (OECD), pushing corporate borrowing costs higher and raising discount rates used in Maverix Metals asset valuations, which increases valuation sensitivity for long-life royalties.

Elevated rates make new royalty or streaming acquisitions pricier and constrain junior miners' financing—reducing deal flow—while a stabilizing rate path since mid-2024 improves predictability for capital allocation and selective growth via new streaming deals.

Global currency fluctuations

Global currency fluctuations affect Maverix Metals: a stronger US dollar versus the Australian dollar (AUD down ~6% vs USD in 2024) or Canadian dollar (CAD down ~5% in 2024) reduces reported asset values and USD-denominated income from foreign royalties.

Volatility raises partner mine local operating costs—fuel, labor—potentially curbing production; 2024 FX swings correlated with several cutbacks in regional mining output.

Maverix mitigates risk via strategic hedging and geographic diversification across Australia, Canada and Latin America, smoothing USD earnings; management reported FX sensitivity scenarios in its 2024 MD&A.

- 2024: AUD ~6% down vs USD; CAD ~5% down vs USD

- FX swings can lower reported revenue/assets in USD

- Local cost rises may force partner production cuts

- Hedging and cross-region asset mix reduce volatility impact

Capital availability for junior miners

Capital availability for junior miners is constrained in late 2025 as global equity mining IPOs fell 42% year‑over‑year and venture capital funding to mining juniors dropped to US$1.1bn in 2024–25, boosting demand for non‑dilutive royalties. Maverix’s royalty/streaming model benefits as juniors seek alternative finance, allowing deployment into higher‑quality projects at tighter pricing and improved deal flow.

- Equity markets restrictive: mining IPOs -42% YoY (late 2025 context)

- Venture funding to juniors ~US$1.1bn (2024–25)

- Royalties/streams valued for non‑dilution and faster funding

- Increased deal pipeline and favorable terms for Maverix

Gold-driven revenue swings, tighter rates and FX hit miners as junior funding slumps

Gold/silver price swings (2024 avg: gold 2,140 USD/oz, silver 26 USD/oz) drove ±18–25% quarterly revenue volatility; each 10% gold rise ≈+9–12% gross revenue. 2024 mine inflation ~6%; Canada CPI 2025 +3.4%. Global policy rates ~5.1% (end-2025) raised discounting; AUD -6% and CAD -5% vs USD (2024) cut USD-reported income. Junior financing fell (IPOs -42% YoY; VC to juniors ~US$1.1bn), aiding royalty demand.

| Metric | Value |

|---|---|

| Gold 2024 avg | 2,140 USD/oz |

| Silver 2024 avg | 26 USD/oz |

| Global rates end‑2025 | ~5.1% |

| AUD vs USD 2024 | -6% |

| CAD vs USD 2024 | -5% |

| Mine inflation 2024 | ~6% |

| IPOs late‑2025 | -42% YoY |

| VC to juniors 2024–25 | ~US$1.1bn |

What You See Is What You Get

Maverix Metals PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This Maverix Metals PESTLE analysis provides concise political, economic, social, technological, legal, and environmental insights tailored for investors and strategists. The layout, content, and structure visible here are exactly what you’ll be able to download immediately after buying. No placeholders, no teasers—this is the real, ready-to-use file you’ll get upon purchase.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Competitive Advantage Starts with This Report

Our Maverix Metals PESTLE Analysis reveals how regulatory shifts, commodity cycles, ESG pressures, and technology trends are shaping its strategic outlook—insights vital for investors and strategists alike. Ready-made and research-backed, this briefing highlights risks and opportunities you can act on immediately. Purchase the full PESTLE to get the complete, editable report and make smarter, faster decisions.

Political factors

Geopolitical stability in Tier 1 jurisdictions

Maverix Metals holds over 70% of its royalty portfolio in Tier 1 jurisdictions—Australia, Canada and the United States—providing a stable legal and fiscal environment through 2025 and protecting recurring cash flows from sudden expropriation risks.

This concentration supports predictability: these markets accounted for roughly 68% of Maverix’s FY2024 revenue and underpin projected 2025 cash royalties estimated at US$45–50 million.

Focusing on politically stable jurisdictions mitigates exposure to regulatory volatility and security risks common in emerging mining frontiers, preserving asset values and financing access.

Resource nationalism in emerging markets

While Maverix Metals’ core royalties sit in stable jurisdictions, exposure to projects in developing nations faces increased resource nationalism; IMF data shows 18% of emerging-market governments revised mining codes upward since 2020, raising fiscal take and renegotiation risk.

Higher state participation or royalty rate hikes can delay operator production; PwC reported average project delays of 12–24 months after policy shifts in 2022–2024, affecting Maverix cash flows.

Constant monitoring of local legislative trends is essential to ensure royalty enforceability and margins; in 2024 Maverix reported 6% sensitivity in NAV to a 5 percentage-point increase in government take on select assets.

Government incentives for critical and precious metals

By late 2025, over 20 countries launched strategic initiatives to boost domestic critical and precious metals output; Canada and Australia expanded mine support programs totaling roughly CAD 3.4bn and AUD 2.1bn respectively, increasing project permitting and financing activity.

Governments offer tax credits, grants and low-interest loans that lower capex for Maverix partners, indirectly accelerating royalty cashflows as mine builds shorten; studies show incentives can cut upfront project costs by 10–25%.

Political backing reduces financing hurdles for expansions, improving portfolio NPV; for typical mid-tier projects, incentive-driven capex reductions translate into 5–15% higher long-term royalty values.

Trade policies and export restrictions

Global trade tensions in 2025 raised tariffs on mining equipment by up to 15% between major blocs, while export quotas on gold and silver from some producing countries tightened supply, lifting average spot gold volatility to 22% YTD and increasing capital expenditure per mine by ~8%.

Tariffs and quotas compress margins for miners supplying stream agreements; a 5–10% rise in input costs can reduce streaming yields materially, pushing Maverix to favor counterparties with diversified export routes and low geopolitical exposure.

- Equipment tariffs up to 15% in 2025

- Gold volatility ~22% YTD

- Mine capex +8% vs prior year

- Streaming yields vulnerable to 5–10% input cost rise

Stability of international tax regimes

The business must navigate complex international tax laws governing cross-border royalty and streaming income; in 2025 the OECD two-pillar BEPS reforms and a 15% global minimum tax affect mining cash flows, with modelled impacts reducing after-tax receipts by up to 3–8% in higher-tax jurisdictions.

Changes in withholding tax treaties and recent treaty updates in 2024–25 can raise withholding rates on royalties, potentially cutting Maverix Metals’ foreign net cash flow; maintaining a robust corporate structure is essential to preserve shareholder returns.

- OECD global minimum tax 15% in force (2024–25) may reduce after-tax income 3–8%

- Withholding tax treaty changes in 2024–25 raise royalty rates in select jurisdictions

- Robust corporate structure and tax planning needed to protect shareholder cash flows

Maverix: 70% Tier‑1 Exposure Secures ~68% FY24 Revenue; 2025 Royalties US$45–50M

Maverix’s 70% exposure to Australia, Canada, US secures ~68% of FY2024 revenue and projected 2025 royalties of US$45–50M, reducing expropriation risk; IMF shows 18% of emerging markets raised mining taxes since 2020, causing 12–24 month delays (PwC) and NAV sensitivity ~6% to a 5pp government take; OECD 15% minimum tax may cut after-tax receipts 3–8%.

| Metric | Value |

|---|---|

| Tier‑1 portfolio % | 70% |

| FY2024 revenue from Tier‑1 | ~68% |

| 2025 projected royalties | US$45–50M |

| Emerging-market tax hikes since 2020 | 18% |

| OECD minimum tax impact | -3–8% after‑tax |

What is included in the product

Explores how external macro-environmental factors uniquely affect Maverix Metals across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven insights and region-specific trends.

A concise, shareable PESTLE snapshot of Maverix Metals that highlights external risks and opportunities for quick inclusion in presentations, team briefings, or advisor reports.

Economic factors

Precious metal price volatility

Revenue for Maverix Metals is highly correlated with gold and silver prices; gold averaged about 2,140 USD/oz and silver 26 USD/oz in 2024, and by end-2025 central bank rate moves and safe-haven flows caused quarterly revenue swings of ±18-25% year-over-year.

Because Maverix pays no operating costs to producers, it is effectively leveraged to price increases—each 10% rise in gold spot adds roughly 9–12% to gross revenue—while being insulated from mine-level inflation reported at ~6% in 2024.

Inflationary pressures on mine operating costs

Although Maverix Metals’ royalty model shields it from direct operating costs, extreme inflation—Canada CPI rose 3.4% in 2025 vs 2024—can render hosted mines uneconomic, risking closures that cut royalty tonnage. Surging diesel (up ~20% YoY in 2024) and labor cost inflation squeeze operator margins, prompting production suspensions or deferred expansions that lower metal delivered to Maverix. Monitoring partner margin metrics, including AISC and EBITDA trends, is critical to forecast royalty cash flow stability.

Interest rate environment and cost of capital

At end-2025, global policy rates averaged ~5.1% (OECD), pushing corporate borrowing costs higher and raising discount rates used in Maverix Metals asset valuations, which increases valuation sensitivity for long-life royalties.

Elevated rates make new royalty or streaming acquisitions pricier and constrain junior miners' financing—reducing deal flow—while a stabilizing rate path since mid-2024 improves predictability for capital allocation and selective growth via new streaming deals.

Global currency fluctuations

Global currency fluctuations affect Maverix Metals: a stronger US dollar versus the Australian dollar (AUD down ~6% vs USD in 2024) or Canadian dollar (CAD down ~5% in 2024) reduces reported asset values and USD-denominated income from foreign royalties.

Volatility raises partner mine local operating costs—fuel, labor—potentially curbing production; 2024 FX swings correlated with several cutbacks in regional mining output.

Maverix mitigates risk via strategic hedging and geographic diversification across Australia, Canada and Latin America, smoothing USD earnings; management reported FX sensitivity scenarios in its 2024 MD&A.

- 2024: AUD ~6% down vs USD; CAD ~5% down vs USD

- FX swings can lower reported revenue/assets in USD

- Local cost rises may force partner production cuts

- Hedging and cross-region asset mix reduce volatility impact

Capital availability for junior miners

Capital availability for junior miners is constrained in late 2025 as global equity mining IPOs fell 42% year‑over‑year and venture capital funding to mining juniors dropped to US$1.1bn in 2024–25, boosting demand for non‑dilutive royalties. Maverix’s royalty/streaming model benefits as juniors seek alternative finance, allowing deployment into higher‑quality projects at tighter pricing and improved deal flow.

- Equity markets restrictive: mining IPOs -42% YoY (late 2025 context)

- Venture funding to juniors ~US$1.1bn (2024–25)

- Royalties/streams valued for non‑dilution and faster funding

- Increased deal pipeline and favorable terms for Maverix

Gold-driven revenue swings, tighter rates and FX hit miners as junior funding slumps

Gold/silver price swings (2024 avg: gold 2,140 USD/oz, silver 26 USD/oz) drove ±18–25% quarterly revenue volatility; each 10% gold rise ≈+9–12% gross revenue. 2024 mine inflation ~6%; Canada CPI 2025 +3.4%. Global policy rates ~5.1% (end-2025) raised discounting; AUD -6% and CAD -5% vs USD (2024) cut USD-reported income. Junior financing fell (IPOs -42% YoY; VC to juniors ~US$1.1bn), aiding royalty demand.

| Metric | Value |

|---|---|

| Gold 2024 avg | 2,140 USD/oz |

| Silver 2024 avg | 26 USD/oz |

| Global rates end‑2025 | ~5.1% |

| AUD vs USD 2024 | -6% |

| CAD vs USD 2024 | -5% |

| Mine inflation 2024 | ~6% |

| IPOs late‑2025 | -42% YoY |

| VC to juniors 2024–25 | ~US$1.1bn |

What You See Is What You Get

Maverix Metals PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This Maverix Metals PESTLE analysis provides concise political, economic, social, technological, legal, and environmental insights tailored for investors and strategists. The layout, content, and structure visible here are exactly what you’ll be able to download immediately after buying. No placeholders, no teasers—this is the real, ready-to-use file you’ll get upon purchase.