MFS Business Model Canvas

Download MFS’s concise Business Model Canvas: investor-ready insights & editable templates

Unlock the full strategic blueprint behind MFS's business model—this concise Business Model Canvas shows how MFS creates value, scales distribution, and sustains competitive advantage across products and channels.

Perfect for investors, consultants, and founders, the full download breaks down all nine building blocks with company-specific insights, financial implications, and practical recommendations.

Download the editable Word and Excel files to benchmark, adapt, and accelerate your strategy with a proven, investor-ready framework.

Partnerships

Strategic Axis Bank Alliance

Axis Bank, as co-promoter and primary bancassurance partner, gives Max Life access to 4,500+ branches and 14 million monthly transactions across India, embedding insurance offers into the banking journey and driving consistent cross-sell. This long-term tie supplies a high-volume, hard-to-replicate sales funnel—Max Life reported ~25% of new individual annualized premium equivalent (APE) via bancassurance in FY2024—securing stable distribution and scale.

Bancassurance Network Expansion

Beyond Axis Bank, Max Life partners with Yes Bank and IDFC First Bank, broadening reach across urban and semi-urban segments and adding over 25% incremental channel distribution versus relying on a single bancassurance partner as of FY2024-25.

These tie-ups let Max Life avoid branch capex, tap bank-client trust to lift conversion rates (reported ~18–22% higher via bancassurance) for protection and savings products, and expand geographically without new physical outlets.

Global Reinsurance Collaborations

Max Life partners with global reinsurers like Munich Re and Swiss Re to cede portions of high-value risk, supporting solvency—reinsurance covered ~18% of its peak risk exposure in FY2024—and enabling underwriting of policies >INR 100 crore while capping catastrophe losses; reinsurers supply global mortality datasets and actuarial models that trimmed pricing variance by ~12% in 2024, improving reserve accuracy and capital efficiency.

Digital and Fintech Aggregators

Collaborate with digital aggregators like PolicyBazaar to reach online-first consumers; PolicyBazaar intermediated ~27% of India’s retail life insurance digital leads in 2024, so listing Max Life’s competitive premiums and 98.3% claim settlement ratio increases conversions.

Maintain top-platform visibility to capture younger, self-directed investors—54% of digital insurance buyers in 2024 were aged 25–40.

- PolicyBazaar reach: ~27% digital leads (2024)

- Max Life claim settlement ratio: 98.3% (2024)

- 54% digital buyers aged 25–40 (2024)

- Focus: competitive premiums, clear disclosures, SEO on aggregator pages

Technology and Ecosystem Partners

Max Life partners with AI, cloud, and analytics vendors to digitize underwriting and claims; automation cut claim processing times by up to 40% in 2024 and reduced underwriting turnaround by 30%.

Integration with health and wellness platforms adds fitness-tracking rewards, driving a 12% rise in policyholder engagement and a 5% lower lapse rate in 2024.

- AI/cloud vendors: 30% of IT budget (2024)

- Claims automation: −40% processing time (2024)

- Underwriting speed: +30% faster (2024)

- Wellness tie-ins: +12% engagement (2024)

- Lapse reduction: −5% (2024)

Max Life’s partnerships drive scalable distribution, digital reach & cost-efficient risk transfer

Max Life’s key partnerships—Axis Bank (4,500+ branches, 14M monthly transactions; ~25% new APE via bancassurance FY2024), Yes Bank, IDFC First Bank, PolicyBazaar (~27% digital leads 2024), reinsurers (reinsurance ~18% peak risk FY2024), and AI/cloud vendors (30% IT budget)—secure scalable distribution, risk transfer, digital reach, and operational efficiency (claims −40% time; underwriting +30% speed).

| Partner | Key metric (2024) | Impact |

|---|---|---|

| Axis Bank | 4,500+ branches; 14M tx; ~25% new APE | High-volume bancassurance funnel |

| PolicyBazaar | ~27% digital leads | Digital customer reach |

| Reinsurers | ~18% peak risk ceded | Solvency, large sum underwriting |

| AI/Cloud vendors | 30% IT budget; claims −40% | Faster processing, lower costs |

What is included in the product

A comprehensive, pre-written Business Model Canvas for MFS that maps nine BMC blocks with detailed customer segments, channels, value propositions, revenue and cost structures, and operational plans, integrating SWOT-linked insights and competitive advantages to support presentations, funding discussions, and data-driven decision-making.

Condenses the MFS business model into a single editable canvas to save hours of structuring, enable quick comparisons, and provide a clean, shareable snapshot for team collaboration and rapid decision-making.

Activities

Product Innovation and Actuarial Design

The team develops savings, protection, and retirement products—e.g., unit-linked and fixed annuities—targeting 35–65 age cohorts; in 2024 global life premiums rose 3.5% to $2.1 trillion, showing sustained demand for savings-retirement solutions.

Actuaries use mortality, lapse, and interest-rate models to price competitively while keeping IFRS 17 reserve metrics and a 150%+ solvency margin; product innovation adds flexible riders and premium-holiday options to match life-stage shifts.

Multi-Channel Distribution Management

Managing a multi-channel distribution network—agents, 12 bank partners, and direct digital channels—is core, with agents handling ~65% of transactions and digital channels growing 28% YoY (2024). Continuous agent training ensures compliance with evolving regulations (AML/KYC updates in 2024) and sales ethics, while channel mix optimization targets a 15% improvement in customer acquisition cost (CAC) by H2 2025.

Underwriting and Risk Assessment

Max Life uses advanced underwriting—medical checks and financial scrutiny—plus data analytics and automated rules to issue low-risk policies within days while reserving manual review for complex cases; in 2024 its combined new-business auto-decision rate rose to ~62% and underwriting turnaround fell 28%, helping keep FY2024 claims ratio near 58%, protecting the policyholder fund.

Claims Management and Settlement

Max Life runs end-to-end claims management focused on speed and empathy; in FY2024 the company reported a claim settlement ratio of 99.28% and settled 109,000+ claims, which underpins brand trust and reduces reputational risk.

- 99.28% claim settlement ratio (FY2024)

- 109,000+ claims settled in FY2024

- Fast, empathetic processing to support beneficiaries

Investment and Asset Management

The firm manages over $120bn of policyholder assets (2025), allocating strategically across government bonds (45%), corporate debt (30%) and equities (25%) to target stable, long-term yields while meeting insurance regulations and capital buffers.

Strong investment returns fund liabilities and returns for participating and unit-linked products; a 2024 blended yield of ~3.8% supported solvency ratios above regulatory minima.

- Assets under management: $120bn (2025)

- Allocation: gov’t 45%, corp 30%, equity 25%

- Blended yield: ~3.8% (2024)

- Supports solvency and product returns

$120B AUM insurer: 3.8% yield, 150%+ solvency, 99.3% claims, 28% digital growth

Team builds savings, protection, retirement products for ages 35–65; AUM $120bn (2025), blended yield ~3.8% (2024), solvency 150%+. Distribution: agents 65%, 12 bank partners, digital +28% YoY (2024). Claims: settlement ratio 99.28%, 109,000+ claims (FY2024). Underwriting auto-decision ~62%, TAT down 28% (2024).

| Metric | Value |

|---|---|

| AUM | $120bn (2025) |

| Blended yield | ~3.8% (2024) |

| Solvency | 150%+ |

| Agents share | ~65% |

| Digital growth | +28% YoY (2024) |

| Claim settlement | 99.28% (FY2024) |

| Claims settled | 109,000+ (FY2024) |

| Auto-decision rate | ~62% (2024) |

Delivered as Displayed

Business Model Canvas

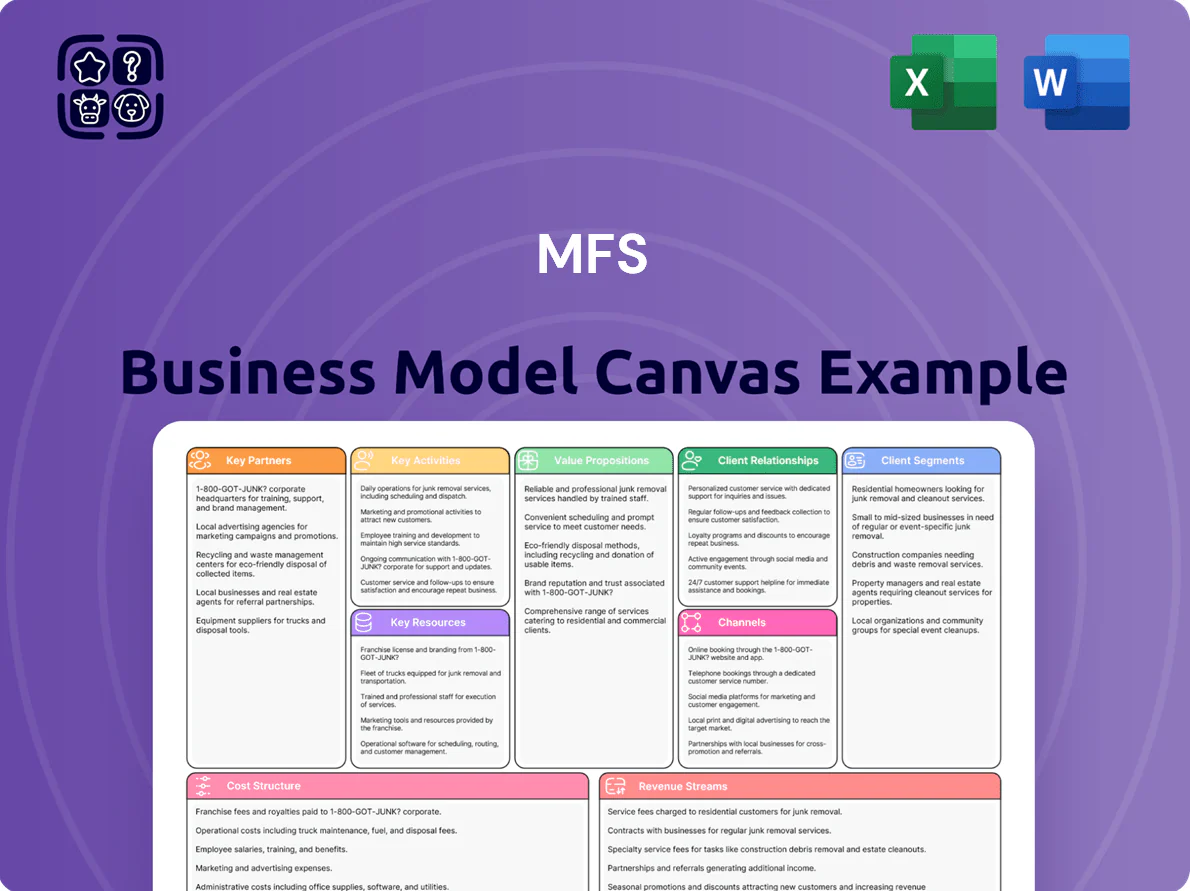

The preview you see is the exact MFS Business Model Canvas document you’ll receive after purchase—not a mockup or sample—and upon completing your order you’ll get the full, editable file formatted exactly as shown, ready for presentation and use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Download MFS’s concise Business Model Canvas: investor-ready insights & editable templates

Unlock the full strategic blueprint behind MFS's business model—this concise Business Model Canvas shows how MFS creates value, scales distribution, and sustains competitive advantage across products and channels.

Perfect for investors, consultants, and founders, the full download breaks down all nine building blocks with company-specific insights, financial implications, and practical recommendations.

Download the editable Word and Excel files to benchmark, adapt, and accelerate your strategy with a proven, investor-ready framework.

Partnerships

Strategic Axis Bank Alliance

Axis Bank, as co-promoter and primary bancassurance partner, gives Max Life access to 4,500+ branches and 14 million monthly transactions across India, embedding insurance offers into the banking journey and driving consistent cross-sell. This long-term tie supplies a high-volume, hard-to-replicate sales funnel—Max Life reported ~25% of new individual annualized premium equivalent (APE) via bancassurance in FY2024—securing stable distribution and scale.

Bancassurance Network Expansion

Beyond Axis Bank, Max Life partners with Yes Bank and IDFC First Bank, broadening reach across urban and semi-urban segments and adding over 25% incremental channel distribution versus relying on a single bancassurance partner as of FY2024-25.

These tie-ups let Max Life avoid branch capex, tap bank-client trust to lift conversion rates (reported ~18–22% higher via bancassurance) for protection and savings products, and expand geographically without new physical outlets.

Global Reinsurance Collaborations

Max Life partners with global reinsurers like Munich Re and Swiss Re to cede portions of high-value risk, supporting solvency—reinsurance covered ~18% of its peak risk exposure in FY2024—and enabling underwriting of policies >INR 100 crore while capping catastrophe losses; reinsurers supply global mortality datasets and actuarial models that trimmed pricing variance by ~12% in 2024, improving reserve accuracy and capital efficiency.

Digital and Fintech Aggregators

Collaborate with digital aggregators like PolicyBazaar to reach online-first consumers; PolicyBazaar intermediated ~27% of India’s retail life insurance digital leads in 2024, so listing Max Life’s competitive premiums and 98.3% claim settlement ratio increases conversions.

Maintain top-platform visibility to capture younger, self-directed investors—54% of digital insurance buyers in 2024 were aged 25–40.

- PolicyBazaar reach: ~27% digital leads (2024)

- Max Life claim settlement ratio: 98.3% (2024)

- 54% digital buyers aged 25–40 (2024)

- Focus: competitive premiums, clear disclosures, SEO on aggregator pages

Technology and Ecosystem Partners

Max Life partners with AI, cloud, and analytics vendors to digitize underwriting and claims; automation cut claim processing times by up to 40% in 2024 and reduced underwriting turnaround by 30%.

Integration with health and wellness platforms adds fitness-tracking rewards, driving a 12% rise in policyholder engagement and a 5% lower lapse rate in 2024.

- AI/cloud vendors: 30% of IT budget (2024)

- Claims automation: −40% processing time (2024)

- Underwriting speed: +30% faster (2024)

- Wellness tie-ins: +12% engagement (2024)

- Lapse reduction: −5% (2024)

Max Life’s partnerships drive scalable distribution, digital reach & cost-efficient risk transfer

Max Life’s key partnerships—Axis Bank (4,500+ branches, 14M monthly transactions; ~25% new APE via bancassurance FY2024), Yes Bank, IDFC First Bank, PolicyBazaar (~27% digital leads 2024), reinsurers (reinsurance ~18% peak risk FY2024), and AI/cloud vendors (30% IT budget)—secure scalable distribution, risk transfer, digital reach, and operational efficiency (claims −40% time; underwriting +30% speed).

| Partner | Key metric (2024) | Impact |

|---|---|---|

| Axis Bank | 4,500+ branches; 14M tx; ~25% new APE | High-volume bancassurance funnel |

| PolicyBazaar | ~27% digital leads | Digital customer reach |

| Reinsurers | ~18% peak risk ceded | Solvency, large sum underwriting |

| AI/Cloud vendors | 30% IT budget; claims −40% | Faster processing, lower costs |

What is included in the product

A comprehensive, pre-written Business Model Canvas for MFS that maps nine BMC blocks with detailed customer segments, channels, value propositions, revenue and cost structures, and operational plans, integrating SWOT-linked insights and competitive advantages to support presentations, funding discussions, and data-driven decision-making.

Condenses the MFS business model into a single editable canvas to save hours of structuring, enable quick comparisons, and provide a clean, shareable snapshot for team collaboration and rapid decision-making.

Activities

Product Innovation and Actuarial Design

The team develops savings, protection, and retirement products—e.g., unit-linked and fixed annuities—targeting 35–65 age cohorts; in 2024 global life premiums rose 3.5% to $2.1 trillion, showing sustained demand for savings-retirement solutions.

Actuaries use mortality, lapse, and interest-rate models to price competitively while keeping IFRS 17 reserve metrics and a 150%+ solvency margin; product innovation adds flexible riders and premium-holiday options to match life-stage shifts.

Multi-Channel Distribution Management

Managing a multi-channel distribution network—agents, 12 bank partners, and direct digital channels—is core, with agents handling ~65% of transactions and digital channels growing 28% YoY (2024). Continuous agent training ensures compliance with evolving regulations (AML/KYC updates in 2024) and sales ethics, while channel mix optimization targets a 15% improvement in customer acquisition cost (CAC) by H2 2025.

Underwriting and Risk Assessment

Max Life uses advanced underwriting—medical checks and financial scrutiny—plus data analytics and automated rules to issue low-risk policies within days while reserving manual review for complex cases; in 2024 its combined new-business auto-decision rate rose to ~62% and underwriting turnaround fell 28%, helping keep FY2024 claims ratio near 58%, protecting the policyholder fund.

Claims Management and Settlement

Max Life runs end-to-end claims management focused on speed and empathy; in FY2024 the company reported a claim settlement ratio of 99.28% and settled 109,000+ claims, which underpins brand trust and reduces reputational risk.

- 99.28% claim settlement ratio (FY2024)

- 109,000+ claims settled in FY2024

- Fast, empathetic processing to support beneficiaries

Investment and Asset Management

The firm manages over $120bn of policyholder assets (2025), allocating strategically across government bonds (45%), corporate debt (30%) and equities (25%) to target stable, long-term yields while meeting insurance regulations and capital buffers.

Strong investment returns fund liabilities and returns for participating and unit-linked products; a 2024 blended yield of ~3.8% supported solvency ratios above regulatory minima.

- Assets under management: $120bn (2025)

- Allocation: gov’t 45%, corp 30%, equity 25%

- Blended yield: ~3.8% (2024)

- Supports solvency and product returns

$120B AUM insurer: 3.8% yield, 150%+ solvency, 99.3% claims, 28% digital growth

Team builds savings, protection, retirement products for ages 35–65; AUM $120bn (2025), blended yield ~3.8% (2024), solvency 150%+. Distribution: agents 65%, 12 bank partners, digital +28% YoY (2024). Claims: settlement ratio 99.28%, 109,000+ claims (FY2024). Underwriting auto-decision ~62%, TAT down 28% (2024).

| Metric | Value |

|---|---|

| AUM | $120bn (2025) |

| Blended yield | ~3.8% (2024) |

| Solvency | 150%+ |

| Agents share | ~65% |

| Digital growth | +28% YoY (2024) |

| Claim settlement | 99.28% (FY2024) |

| Claims settled | 109,000+ (FY2024) |

| Auto-decision rate | ~62% (2024) |

Delivered as Displayed

Business Model Canvas

The preview you see is the exact MFS Business Model Canvas document you’ll receive after purchase—not a mockup or sample—and upon completing your order you’ll get the full, editable file formatted exactly as shown, ready for presentation and use.