Mazda Motor PESTLE Analysis

Skip the Research. Get the Strategy.

Discover how political shifts, economic cycles, and rapid tech innovation are reshaping Mazda Motor’s strategic landscape—our concise PESTLE snapshot reveals key external drivers and risks that matter to investors and planners; purchase the full PESTLE for a detailed, actionable roadmap you can use immediately.

Political factors

Global Trade Protectionism and Tariffs

As of late 2025, Mazda faces rising trade barriers: US light-vehicle tariffs rose to 12% on certain imports and EU provisional auto tariffs averaged 10%, pressuring margins and contributing to a projected $420–$520 per-unit cost increase for imported vehicles.

These tariffs force Mazda to accelerate local production—by 2026 it plans to shift ~30% more components to regional plants—to preserve price competitiveness versus US and EU domestic makers.

Geopolitical Stability in the Asia-Pacific

Heightened geopolitical tensions in East Asia—notably around the Taiwan Strait and South China Sea—threaten Mazda’s regional operations and logistics, with 2024 shipping delays raising component lead times by an estimated 12% for Japanese OEMs. Stability in these corridors is critical for flow of parts between Japan (≈1.3 million vehicles produced in 2023) and overseas assembly plants; diplomatic disruptions could drive supply-chain bottlenecks and raise operational costs by several percentage points.

Government Subsidies for Electrification

Mazda’s EV shift is shaped by diverse subsidy regimes—e.g., Japan’s subsidies up to ¥1.6m per EV and the US Inflation Reduction Act offering up to $7,500 tax credits—changes in these can swing demand and force Mazda to revise 2025–2026 production targets (company aims ~500,000 electrified vehicles by 2030).

Japanese Industrial Policy and Support

Japan’s 2021 Strategic Energy Plan and 2023 Green Growth Strategy channel subsidies and tax incentives toward hydrogen and e-fuels; government R&D budgets for hydrogen exceeded ¥200 billion (~$1.4bn) 2022–2024, directly benefiting automakers like Mazda.

Mazda leverages national programs and university-industry consortia to access grants and pilot projects, supporting its Skyactiv-X and hydrogen engine work and reducing R&D costs.

Alignment with state industrial goals helps Mazda secure funding, accelerate technology transfer, and maintain competitive edge in decarbonization.

- ¥200bn+ hydrogen R&D funding (2022–24)

- Public–private pilot grants reduce Mazda R&D burden

- State incentives accelerate hydrogen/e-fuel deployment

Regulatory Pressure on Emission Standards

Regulatory mandates aiming for 100% zero-emission vehicle sales by 2030–2035 in multiple EU countries and US states force Mazda to accelerate ICE phase-out, reallocate R&D and capex toward EVs; EU CO2 targets tightened to a 55% fleet reduction by 2030 and 100% by 2035, while California and 15 states target similar timelines.

Noncompliance risks include heavy fines—EU CO2 penalties of €95 per g/km over target multiplied by fleet size—and effective market exclusion in key regions, pressuring Mazda’s long-term product roadmap and profitability metrics.

- 2030–2035 ZEV mandates in EU/US states

- EU: 55% CO2 cut by 2030, 100% by 2035

- Penalties: €95 per g/km over target

- Impacts: accelerated R&D, capex shift, market access risk

Mazda faces tariff shocks, longer lead-times, subsidy swings and strict ZEV fines

Political risks for Mazda include rising US/EU auto tariffs (≈10–12% in 2025) raising per-unit import costs $420–$520, East Asian geopolitical tensions increasing lead times ~12%, shifting subsidy regimes (Japan EV subsidy up to ¥1.6m; US IRA $7,500) that affect demand, and strict EU/US ZEV mandates (55% CO2 cut by 2030, 100% by 2035) imposing heavy fines (~€95/g·km).

| Item | Metric |

|---|---|

| Tariffs | 10–12% (2025) |

| Per-unit cost | $420–$520 |

| Lead-time rise | ~12% (2024) |

| Japan EV subsidy | ¥1.6m |

| US IRA credit | $7,500 |

| EU CO2 targets | −55% by 2030, 0% by 2035 |

What is included in the product

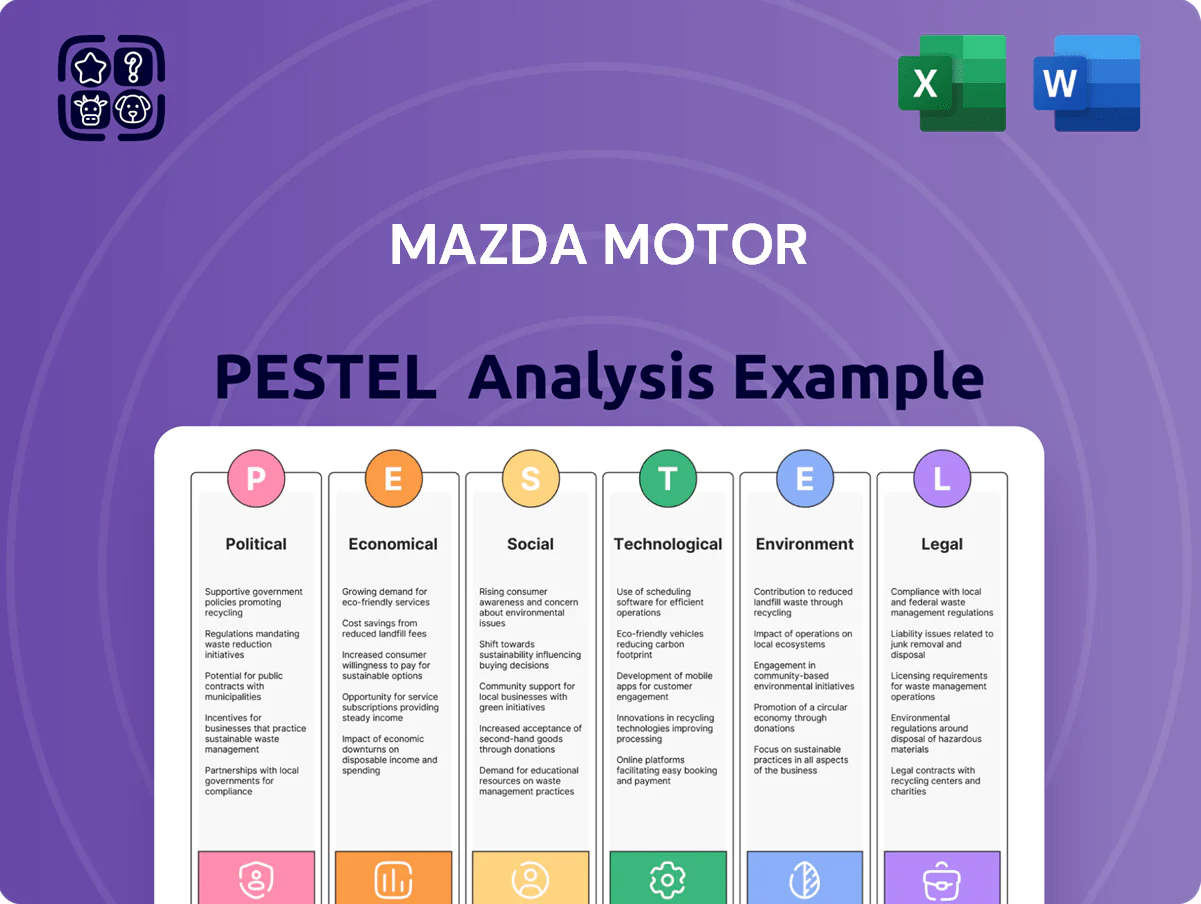

Explores how macro-environmental forces—Political, Economic, Social, Technological, Environmental, and Legal—specifically shape Mazda Motor’s strategy, operations, and competitive position, with data-driven trends and regional industry context.

A concise, shareable Mazda Motor PESTLE summary that’s visually segmented by category for quick interpretation during meetings and easily dropped into presentations or strategy packs.

Economic factors

Fluctuations in Foreign Exchange Rates

As a major Japanese exporter, Mazda’s profitability is highly sensitive to JPY movements versus USD and EUR; a 10% yen appreciation in 2022‑23 reduced reported operating profit for many automakers by mid‑single digits, a risk Mazda faces given FY2024 net sales of ¥4.7 trillion. Significant FX volatility affects reported earnings and overseas pricing, with 2023 USD/JPY swings of ~10% and EUR/JPY ~12% altering margins. Effective hedging—Mazda reported ¥60 billion in FX derivatives at end‑FY2024—is required to mitigate these economic shifts.

Global Interest Rate Environments

Central bank rate moves shape consumer auto loans and lease rates; as of December 2025 many major central banks kept policy rates elevated — US Fed funds at 5.25–5.50%, ECB depo at 4.00% — raising borrowing costs and loan APRs for buyers. High rates in late 2025 likely curb new-vehicle demand and raise Mazda’s weighted average cost of capital, increasing project financing costs. Monitoring these rates and indicators like 2025 global auto sales down ~3% YoY is vital for forecasting and debt management.

Raw Material and Energy Price Volatility

Rising prices for lithium (spot up ~45% in 2024), cobalt (up ~20% y/y) and specialty steels have tightened Mazda’s manufacturing margins, with raw material costs accounting for an estimated 12–15% of vehicle production costs in 2024.

Supply disruptions in 2023–24, including Indonesian nickel output curbs and Congo export volatility, drove sudden input cost spikes, increasing short‑term production costs by an estimated $400–$700 per EV equivalent.

Mazda must offset these inflationary pressures through engineering redesigns, material substitution and centralized procurement savings targets (aiming for 3–5% cost reduction per vehicle in 2025) to preserve profitability.

Labor Market Dynamics and Wage Growth

Rising labor costs in Japan—wages grew ~2.6% y/y in 2024 per Ministry of Health, Labour and Welfare—raise Mazda’s manufacturing overhead; similar increases in Mexico and Thailand add to unit labor cost pressure.

Competition for EV and software engineers pushed tech-sector salaries up ~8–12% in 2023–24, increasing Mazda’s recruitment and R&D staffing expenses as it scales EV development.

Balancing higher human capital costs with need for skilled talent is a key economic challenge affecting margins and CAPEX allocation for Mazda through 2024–25.

- Japan wage growth ~2.6% (2024)

- Tech salaries +8–12% (2023–24)

- Higher unit labor costs across MX/TH

- Margin and CAPEX pressure from hiring/R&D

Consumer Disposable Income Trends

- Global GDP 2024 ~3.1%

- Global unemployment ~5.6% (2024)

- US used-car sales +8% YoY (2024)

- EM disposable income growth ~4.5% (2024)

Mazda margins squeezed by FX, inflation & rising input costs despite ¥4.7T sales

FX volatility, elevated rates, raw-material and labor inflation squeezed Mazda’s margins in 2024–25: FY2024 sales ¥4.7T; USD/JPY ±10% swings; FX hedges ¥60B; global GDP 3.1% (2024); lithium +45% (2024); Japan wages +2.6% (2024); tech salaries +8–12% (2023–24); EM income growth ~4.5% (2024).

| Metric | Value (2024) |

|---|---|

| FY Sales | ¥4.7T |

| FX Hedging | ¥60B |

| Global GDP | 3.1% |

| Lithium spot | +45% YoY |

Full Version Awaits

Mazda Motor PESTLE Analysis

The preview shown here is the exact Mazda Motor PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic or investment decisions.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Skip the Research. Get the Strategy.

Discover how political shifts, economic cycles, and rapid tech innovation are reshaping Mazda Motor’s strategic landscape—our concise PESTLE snapshot reveals key external drivers and risks that matter to investors and planners; purchase the full PESTLE for a detailed, actionable roadmap you can use immediately.

Political factors

Global Trade Protectionism and Tariffs

As of late 2025, Mazda faces rising trade barriers: US light-vehicle tariffs rose to 12% on certain imports and EU provisional auto tariffs averaged 10%, pressuring margins and contributing to a projected $420–$520 per-unit cost increase for imported vehicles.

These tariffs force Mazda to accelerate local production—by 2026 it plans to shift ~30% more components to regional plants—to preserve price competitiveness versus US and EU domestic makers.

Geopolitical Stability in the Asia-Pacific

Heightened geopolitical tensions in East Asia—notably around the Taiwan Strait and South China Sea—threaten Mazda’s regional operations and logistics, with 2024 shipping delays raising component lead times by an estimated 12% for Japanese OEMs. Stability in these corridors is critical for flow of parts between Japan (≈1.3 million vehicles produced in 2023) and overseas assembly plants; diplomatic disruptions could drive supply-chain bottlenecks and raise operational costs by several percentage points.

Government Subsidies for Electrification

Mazda’s EV shift is shaped by diverse subsidy regimes—e.g., Japan’s subsidies up to ¥1.6m per EV and the US Inflation Reduction Act offering up to $7,500 tax credits—changes in these can swing demand and force Mazda to revise 2025–2026 production targets (company aims ~500,000 electrified vehicles by 2030).

Japanese Industrial Policy and Support

Japan’s 2021 Strategic Energy Plan and 2023 Green Growth Strategy channel subsidies and tax incentives toward hydrogen and e-fuels; government R&D budgets for hydrogen exceeded ¥200 billion (~$1.4bn) 2022–2024, directly benefiting automakers like Mazda.

Mazda leverages national programs and university-industry consortia to access grants and pilot projects, supporting its Skyactiv-X and hydrogen engine work and reducing R&D costs.

Alignment with state industrial goals helps Mazda secure funding, accelerate technology transfer, and maintain competitive edge in decarbonization.

- ¥200bn+ hydrogen R&D funding (2022–24)

- Public–private pilot grants reduce Mazda R&D burden

- State incentives accelerate hydrogen/e-fuel deployment

Regulatory Pressure on Emission Standards

Regulatory mandates aiming for 100% zero-emission vehicle sales by 2030–2035 in multiple EU countries and US states force Mazda to accelerate ICE phase-out, reallocate R&D and capex toward EVs; EU CO2 targets tightened to a 55% fleet reduction by 2030 and 100% by 2035, while California and 15 states target similar timelines.

Noncompliance risks include heavy fines—EU CO2 penalties of €95 per g/km over target multiplied by fleet size—and effective market exclusion in key regions, pressuring Mazda’s long-term product roadmap and profitability metrics.

- 2030–2035 ZEV mandates in EU/US states

- EU: 55% CO2 cut by 2030, 100% by 2035

- Penalties: €95 per g/km over target

- Impacts: accelerated R&D, capex shift, market access risk

Mazda faces tariff shocks, longer lead-times, subsidy swings and strict ZEV fines

Political risks for Mazda include rising US/EU auto tariffs (≈10–12% in 2025) raising per-unit import costs $420–$520, East Asian geopolitical tensions increasing lead times ~12%, shifting subsidy regimes (Japan EV subsidy up to ¥1.6m; US IRA $7,500) that affect demand, and strict EU/US ZEV mandates (55% CO2 cut by 2030, 100% by 2035) imposing heavy fines (~€95/g·km).

| Item | Metric |

|---|---|

| Tariffs | 10–12% (2025) |

| Per-unit cost | $420–$520 |

| Lead-time rise | ~12% (2024) |

| Japan EV subsidy | ¥1.6m |

| US IRA credit | $7,500 |

| EU CO2 targets | −55% by 2030, 0% by 2035 |

What is included in the product

Explores how macro-environmental forces—Political, Economic, Social, Technological, Environmental, and Legal—specifically shape Mazda Motor’s strategy, operations, and competitive position, with data-driven trends and regional industry context.

A concise, shareable Mazda Motor PESTLE summary that’s visually segmented by category for quick interpretation during meetings and easily dropped into presentations or strategy packs.

Economic factors

Fluctuations in Foreign Exchange Rates

As a major Japanese exporter, Mazda’s profitability is highly sensitive to JPY movements versus USD and EUR; a 10% yen appreciation in 2022‑23 reduced reported operating profit for many automakers by mid‑single digits, a risk Mazda faces given FY2024 net sales of ¥4.7 trillion. Significant FX volatility affects reported earnings and overseas pricing, with 2023 USD/JPY swings of ~10% and EUR/JPY ~12% altering margins. Effective hedging—Mazda reported ¥60 billion in FX derivatives at end‑FY2024—is required to mitigate these economic shifts.

Global Interest Rate Environments

Central bank rate moves shape consumer auto loans and lease rates; as of December 2025 many major central banks kept policy rates elevated — US Fed funds at 5.25–5.50%, ECB depo at 4.00% — raising borrowing costs and loan APRs for buyers. High rates in late 2025 likely curb new-vehicle demand and raise Mazda’s weighted average cost of capital, increasing project financing costs. Monitoring these rates and indicators like 2025 global auto sales down ~3% YoY is vital for forecasting and debt management.

Raw Material and Energy Price Volatility

Rising prices for lithium (spot up ~45% in 2024), cobalt (up ~20% y/y) and specialty steels have tightened Mazda’s manufacturing margins, with raw material costs accounting for an estimated 12–15% of vehicle production costs in 2024.

Supply disruptions in 2023–24, including Indonesian nickel output curbs and Congo export volatility, drove sudden input cost spikes, increasing short‑term production costs by an estimated $400–$700 per EV equivalent.

Mazda must offset these inflationary pressures through engineering redesigns, material substitution and centralized procurement savings targets (aiming for 3–5% cost reduction per vehicle in 2025) to preserve profitability.

Labor Market Dynamics and Wage Growth

Rising labor costs in Japan—wages grew ~2.6% y/y in 2024 per Ministry of Health, Labour and Welfare—raise Mazda’s manufacturing overhead; similar increases in Mexico and Thailand add to unit labor cost pressure.

Competition for EV and software engineers pushed tech-sector salaries up ~8–12% in 2023–24, increasing Mazda’s recruitment and R&D staffing expenses as it scales EV development.

Balancing higher human capital costs with need for skilled talent is a key economic challenge affecting margins and CAPEX allocation for Mazda through 2024–25.

- Japan wage growth ~2.6% (2024)

- Tech salaries +8–12% (2023–24)

- Higher unit labor costs across MX/TH

- Margin and CAPEX pressure from hiring/R&D

Consumer Disposable Income Trends

- Global GDP 2024 ~3.1%

- Global unemployment ~5.6% (2024)

- US used-car sales +8% YoY (2024)

- EM disposable income growth ~4.5% (2024)

Mazda margins squeezed by FX, inflation & rising input costs despite ¥4.7T sales

FX volatility, elevated rates, raw-material and labor inflation squeezed Mazda’s margins in 2024–25: FY2024 sales ¥4.7T; USD/JPY ±10% swings; FX hedges ¥60B; global GDP 3.1% (2024); lithium +45% (2024); Japan wages +2.6% (2024); tech salaries +8–12% (2023–24); EM income growth ~4.5% (2024).

| Metric | Value (2024) |

|---|---|

| FY Sales | ¥4.7T |

| FX Hedging | ¥60B |

| Global GDP | 3.1% |

| Lithium spot | +45% YoY |

Full Version Awaits

Mazda Motor PESTLE Analysis

The preview shown here is the exact Mazda Motor PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic or investment decisions.