Mitchells & Butlers PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Explore how regulatory changes, shifting consumer tastes, and rising operating costs are reshaping Mitchells & Butlers' prospects; our concise PESTLE highlights these forces and points to strategic responses you can act on today—download the full analysis for the complete, editable report and data-driven recommendations.

Political factors

Business Rates Reform

The UK government’s 2024–25 business rates review and proposed revaluations directly affect Mitchells & Butlers’ fixed costs across ~1,750 pubs and restaurants, with estimated annual rates expense ~£360m in FY2024; any 2025 relief rollbacks or new valuation methods could raise site-level costs by 5–10%, cutting EBITDA margins materially. Proactive fiscal planning, appeals, and capex-led rateable value reductions are essential to mitigate potential sector tax increases.

Alcohol Duty and Taxation

Changes in alcohol duty structures remain a critical political lever affecting Mitchells & Butlers pricing and demand; UK beer duty rose 5% in 2024 while spirits saw a 2% cut, shifting margin pressures across categories.

Recent budgets altered levies by category—cider duty fell 3% in 2025—forcing adjustments to procurement, menu pricing and SKU mix to protect gross margin (M&B reported 2024 gross margin ~57%).

Maintaining dialogue with trade bodies like the BII and UKHospitality is essential: their 2024 lobbying helped secure a £180m VAT relief extension that mitigated some fiscal impacts.

Immigration and Labor Policy

Post-Brexit immigration rules continue to constrain labor supply in UK hospitality, with net migration falling 12% in 2024 versus 2019 levels, tightening recruitment for Mitchells & Butlers across its 1,700+ sites.

Government policy on seasonal worker visas and the £38,700 minimum salary threshold for many skilled routes reduces eligible foreign hires, pressuring wage costs and recruitment timelines.

Mitchells & Butlers is scaling domestic training, investing in apprenticeship schemes that enrolled over 2,000 staff in 2024 to mitigate staffing shortages and lower agency spend.

Public Health Regulations

Government initiatives like mandatory calorie labeling and restrictions on HFSS products force Mitchells & Butlers to update menus and reformulate dishes; UK calorie labeling on large businesses has applied since April 2022 and HFSS marketing restrictions tightened in 2023, impacting menu engineering and supply chains.

Noncompliance risks fines and reputational damage—surveys show 62% of UK consumers consider health labeling important—and reformulation and menu redesign can raise COGS by an estimated 2–4%, affecting margins.

- Mandatory calorie labeling since Apr 2022

- HFSS restrictions tightened 2023

- 62% UK consumers value health labels

- Estimated 2–4% COGS increase from reformulation

Geopolitical Supply Chain Stability

Geopolitical instability in trade corridors raises import costs for ingredients and energy, contributing to UK food inflation peaking at 19.1% in 2022 and easing to ~6% by 2024 but still elevating input costs for Mitchells & Butlers’ 2024 food and beverage spend.

Mitchells & Butlers actively monitors trade agreements and risks—including UK-EU UKCA/NI checks and Black Sea grain disruptions—to anticipate supply interruptions for beer, wheat, and vegetable oils.

To mitigate shocks and price volatility, the company pursues strategic sourcing and supplier diversification, reducing reliance on single-origin suppliers and targeting procurement cost reductions consistent with its 2023–24 margin recovery initiatives.

- Food inflation: 19.1% (2022) → ~6% (2024)

- Focus commodities: beer, wheat, vegetable oils

- Actions: supplier diversification, strategic sourcing, procurement savings goals (2023–24)

Mitchells & Butlers faces rising rates, higher wages and duty/COGS pressures

Political factors for Mitchells & Butlers: business rates review (annual rates ~£360m FY2024) and potential 2025 revaluations could raise site costs 5–10%; alcohol duty shifts (beer +5% 2024, cider −3% 2025) alter margins; post‑Brexit labor rules cut net migration 12% vs 2019, tightening staffing and raising wages; calorie/HFSS rules since 2022–23 add 2–4% to COGS and compliance risk.

| Metric | Value |

|---|---|

| Annual rates expense (FY2024) | ~£360m |

| Potential site cost rise (2025) | 5–10% |

| Beer duty change (2024) | +5% |

| Cider duty change (2025) | −3% |

| Net migration vs 2019 (2024) | −12% |

| COGS increase from reformulation | 2–4% |

What is included in the product

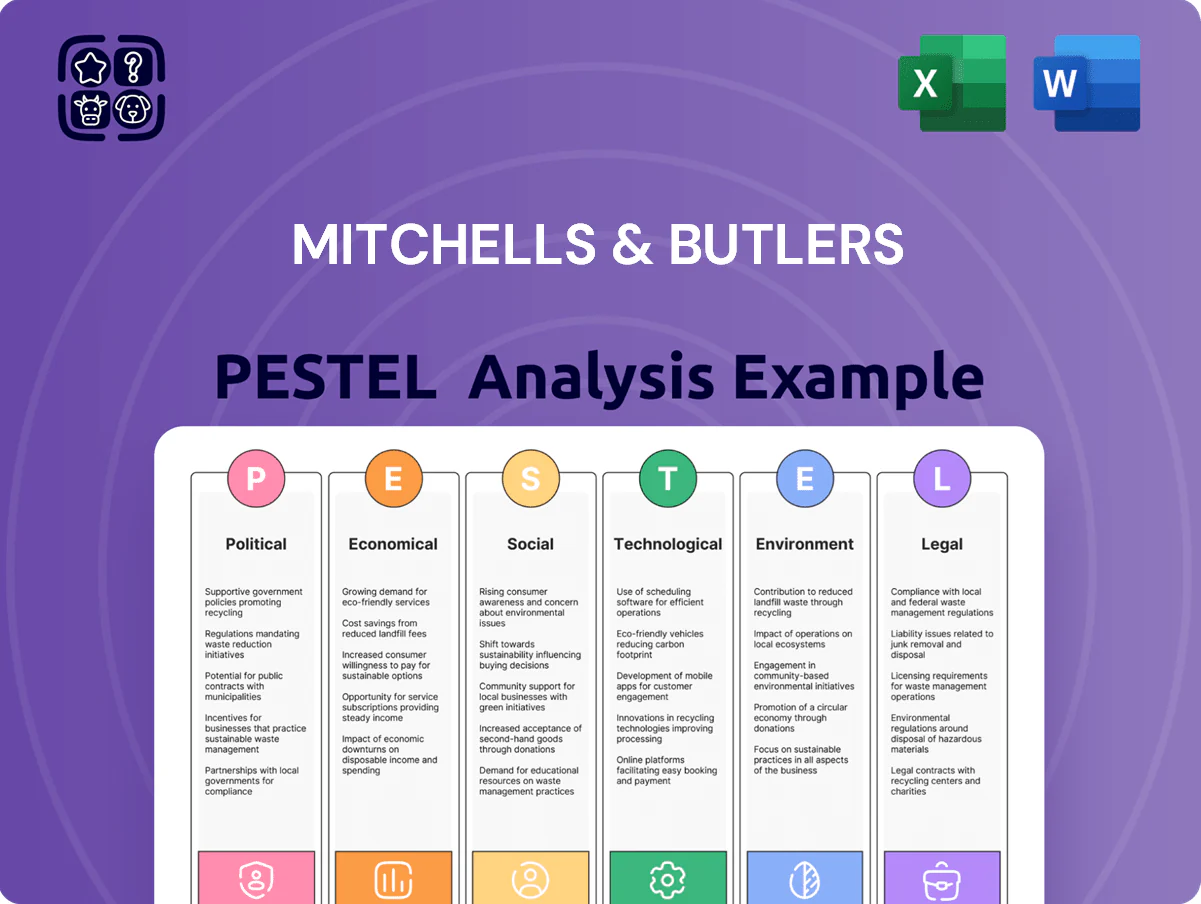

Explores how external macro-environmental factors uniquely affect Mitchells & Butlers across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven sections, industry-specific examples, forward-looking insights for scenario planning, and clean formatting ready for business plans, reports, or investor materials to help executives and advisors identify threats and opportunities.

A concise, neatly segmented PESTLE summary for Mitchells & Butlers that streamlines external risk assessment and market positioning discussions, easily dropped into presentations or shared across teams for quick alignment.

Economic factors

National Living Wage Increases

The sustained rise in the National Living Wage to 10.42 per hour in April 2025 exerts material inflationary pressure on Mitchells & Butlers’ operating margins, with the company reporting 2024 adjusted operating margin of 7.8% that is vulnerable to further wage-driven cost increases; management is balancing fair pay with cost control by targeting productivity gains and rollout of tech-led efficiencies (self-ordering, labour scheduling) to offset higher payroll, aiming to limit margin erosion.

Consumer Discretionary Spending

Interest Rate Environment

The prevailing interest rate environment affects Mitchells & Butlers' debt servicing costs and funding for capex; UK Bank Rate rose to 5.25% in Dec 2023 and averaged ~4.5% through 2024, raising borrowing costs. High rates can tighten cashflow and prompt caution on estate expansion and major refurbishments. M&B maintained net debt around £1.45bn at H1 2024/25 and prioritises a robust balance sheet to withstand monetary tightening.

Energy Cost Volatility

Energy cost volatility remains a material overhead for Mitchells & Butlers, with UK business energy prices up ~18% year-on-year in 2024 vs 2023, prompting use of hedging and targeted efficiency upgrades.

The company prioritises LED lighting, HVAC optimisation and building management systems across ~1,700 sites to lower consumption and exposure to wholesale swings.

Mitchells & Butlers increasingly signs multi-year energy contracts and pilots onsite solar and battery projects to lock rates and stabilise margins.

- 2024 UK business energy +18% y/y

- ~1,700 sites targeted for efficiency

- Use of long-term contracts + onsite solar/battery pilots

Food and Beverage Inflation

Food and beverage inflation, driven by 2024-25 spikes in meat (beef up ~18% YoY in UK 2024), dairy and grain prices, compresses Mitchells & Butlers' gross margins across its food-led brands, forcing margin recovery via pricing and cost control.

Mitchells & Butlers uses buying scale—procurement savings covered ~£30–40m in 2023–24 procurement efficiencies—but persistent inflation demands frequent menu engineering and SKU rationalization.

Tracking global harvest yields and input costs (wheat global output variance ±3–5% 2024) is essential for accurate forecasting and setting price tiers to protect EBITDA.

- Commodity volatility directly affects food COGS and margins

- Scale yields procurement leverage (c.£30–40m savings 2023–24)

- Frequent menu engineering needed to offset sustained inflation

- Monitoring global yields and input costs critical for pricing and forecasts

Rising NLW, costs and debt squeeze margins—procurement cuts £30–40m protect EBITDA

Wage inflation (NLW £10.42 Apr 2025) and Bank Rate (~4.5% avg 2024) pressure margins and debt costs; net debt ~£1.45bn H1 2024/25. CPI eased from ~6% (2023) to ~3.9% (2024), impacting spend; energy +18% y/y 2024 and food inflation (beef +18% YoY 2024) raise COGS; procurement saved ~£30–40m 2023–24 via scale, plus tech and efficiency measures to protect EBITDA.

| Metric | 2023 | 2024 | 2025 |

|---|---|---|---|

| NLW | - | £9.50 | £10.42 |

| CPI | ~6% | ~3.9% | - |

| Energy change | - | +18% y/y | - |

| Net debt | - | £1.45bn | - |

| Procurement savings | - | £30–40m | - |

What You See Is What You Get

Mitchells & Butlers PESTLE Analysis

The preview shown here is the exact Mitchells & Butlers PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic review and decision-making.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Explore how regulatory changes, shifting consumer tastes, and rising operating costs are reshaping Mitchells & Butlers' prospects; our concise PESTLE highlights these forces and points to strategic responses you can act on today—download the full analysis for the complete, editable report and data-driven recommendations.

Political factors

Business Rates Reform

The UK government’s 2024–25 business rates review and proposed revaluations directly affect Mitchells & Butlers’ fixed costs across ~1,750 pubs and restaurants, with estimated annual rates expense ~£360m in FY2024; any 2025 relief rollbacks or new valuation methods could raise site-level costs by 5–10%, cutting EBITDA margins materially. Proactive fiscal planning, appeals, and capex-led rateable value reductions are essential to mitigate potential sector tax increases.

Alcohol Duty and Taxation

Changes in alcohol duty structures remain a critical political lever affecting Mitchells & Butlers pricing and demand; UK beer duty rose 5% in 2024 while spirits saw a 2% cut, shifting margin pressures across categories.

Recent budgets altered levies by category—cider duty fell 3% in 2025—forcing adjustments to procurement, menu pricing and SKU mix to protect gross margin (M&B reported 2024 gross margin ~57%).

Maintaining dialogue with trade bodies like the BII and UKHospitality is essential: their 2024 lobbying helped secure a £180m VAT relief extension that mitigated some fiscal impacts.

Immigration and Labor Policy

Post-Brexit immigration rules continue to constrain labor supply in UK hospitality, with net migration falling 12% in 2024 versus 2019 levels, tightening recruitment for Mitchells & Butlers across its 1,700+ sites.

Government policy on seasonal worker visas and the £38,700 minimum salary threshold for many skilled routes reduces eligible foreign hires, pressuring wage costs and recruitment timelines.

Mitchells & Butlers is scaling domestic training, investing in apprenticeship schemes that enrolled over 2,000 staff in 2024 to mitigate staffing shortages and lower agency spend.

Public Health Regulations

Government initiatives like mandatory calorie labeling and restrictions on HFSS products force Mitchells & Butlers to update menus and reformulate dishes; UK calorie labeling on large businesses has applied since April 2022 and HFSS marketing restrictions tightened in 2023, impacting menu engineering and supply chains.

Noncompliance risks fines and reputational damage—surveys show 62% of UK consumers consider health labeling important—and reformulation and menu redesign can raise COGS by an estimated 2–4%, affecting margins.

- Mandatory calorie labeling since Apr 2022

- HFSS restrictions tightened 2023

- 62% UK consumers value health labels

- Estimated 2–4% COGS increase from reformulation

Geopolitical Supply Chain Stability

Geopolitical instability in trade corridors raises import costs for ingredients and energy, contributing to UK food inflation peaking at 19.1% in 2022 and easing to ~6% by 2024 but still elevating input costs for Mitchells & Butlers’ 2024 food and beverage spend.

Mitchells & Butlers actively monitors trade agreements and risks—including UK-EU UKCA/NI checks and Black Sea grain disruptions—to anticipate supply interruptions for beer, wheat, and vegetable oils.

To mitigate shocks and price volatility, the company pursues strategic sourcing and supplier diversification, reducing reliance on single-origin suppliers and targeting procurement cost reductions consistent with its 2023–24 margin recovery initiatives.

- Food inflation: 19.1% (2022) → ~6% (2024)

- Focus commodities: beer, wheat, vegetable oils

- Actions: supplier diversification, strategic sourcing, procurement savings goals (2023–24)

Mitchells & Butlers faces rising rates, higher wages and duty/COGS pressures

Political factors for Mitchells & Butlers: business rates review (annual rates ~£360m FY2024) and potential 2025 revaluations could raise site costs 5–10%; alcohol duty shifts (beer +5% 2024, cider −3% 2025) alter margins; post‑Brexit labor rules cut net migration 12% vs 2019, tightening staffing and raising wages; calorie/HFSS rules since 2022–23 add 2–4% to COGS and compliance risk.

| Metric | Value |

|---|---|

| Annual rates expense (FY2024) | ~£360m |

| Potential site cost rise (2025) | 5–10% |

| Beer duty change (2024) | +5% |

| Cider duty change (2025) | −3% |

| Net migration vs 2019 (2024) | −12% |

| COGS increase from reformulation | 2–4% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Mitchells & Butlers across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven sections, industry-specific examples, forward-looking insights for scenario planning, and clean formatting ready for business plans, reports, or investor materials to help executives and advisors identify threats and opportunities.

A concise, neatly segmented PESTLE summary for Mitchells & Butlers that streamlines external risk assessment and market positioning discussions, easily dropped into presentations or shared across teams for quick alignment.

Economic factors

National Living Wage Increases

The sustained rise in the National Living Wage to 10.42 per hour in April 2025 exerts material inflationary pressure on Mitchells & Butlers’ operating margins, with the company reporting 2024 adjusted operating margin of 7.8% that is vulnerable to further wage-driven cost increases; management is balancing fair pay with cost control by targeting productivity gains and rollout of tech-led efficiencies (self-ordering, labour scheduling) to offset higher payroll, aiming to limit margin erosion.

Consumer Discretionary Spending

Interest Rate Environment

The prevailing interest rate environment affects Mitchells & Butlers' debt servicing costs and funding for capex; UK Bank Rate rose to 5.25% in Dec 2023 and averaged ~4.5% through 2024, raising borrowing costs. High rates can tighten cashflow and prompt caution on estate expansion and major refurbishments. M&B maintained net debt around £1.45bn at H1 2024/25 and prioritises a robust balance sheet to withstand monetary tightening.

Energy Cost Volatility

Energy cost volatility remains a material overhead for Mitchells & Butlers, with UK business energy prices up ~18% year-on-year in 2024 vs 2023, prompting use of hedging and targeted efficiency upgrades.

The company prioritises LED lighting, HVAC optimisation and building management systems across ~1,700 sites to lower consumption and exposure to wholesale swings.

Mitchells & Butlers increasingly signs multi-year energy contracts and pilots onsite solar and battery projects to lock rates and stabilise margins.

- 2024 UK business energy +18% y/y

- ~1,700 sites targeted for efficiency

- Use of long-term contracts + onsite solar/battery pilots

Food and Beverage Inflation

Food and beverage inflation, driven by 2024-25 spikes in meat (beef up ~18% YoY in UK 2024), dairy and grain prices, compresses Mitchells & Butlers' gross margins across its food-led brands, forcing margin recovery via pricing and cost control.

Mitchells & Butlers uses buying scale—procurement savings covered ~£30–40m in 2023–24 procurement efficiencies—but persistent inflation demands frequent menu engineering and SKU rationalization.

Tracking global harvest yields and input costs (wheat global output variance ±3–5% 2024) is essential for accurate forecasting and setting price tiers to protect EBITDA.

- Commodity volatility directly affects food COGS and margins

- Scale yields procurement leverage (c.£30–40m savings 2023–24)

- Frequent menu engineering needed to offset sustained inflation

- Monitoring global yields and input costs critical for pricing and forecasts

Rising NLW, costs and debt squeeze margins—procurement cuts £30–40m protect EBITDA

Wage inflation (NLW £10.42 Apr 2025) and Bank Rate (~4.5% avg 2024) pressure margins and debt costs; net debt ~£1.45bn H1 2024/25. CPI eased from ~6% (2023) to ~3.9% (2024), impacting spend; energy +18% y/y 2024 and food inflation (beef +18% YoY 2024) raise COGS; procurement saved ~£30–40m 2023–24 via scale, plus tech and efficiency measures to protect EBITDA.

| Metric | 2023 | 2024 | 2025 |

|---|---|---|---|

| NLW | - | £9.50 | £10.42 |

| CPI | ~6% | ~3.9% | - |

| Energy change | - | +18% y/y | - |

| Net debt | - | £1.45bn | - |

| Procurement savings | - | £30–40m | - |

What You See Is What You Get

Mitchells & Butlers PESTLE Analysis

The preview shown here is the exact Mitchells & Butlers PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic review and decision-making.