Mcbride PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Get a competitive edge with our targeted PESTLE Analysis for McBride—uncover how political shifts, economic pressures, and environmental trends are reshaping the company's prospects and find actionable insights to inform investment or strategy decisions; purchase the full report for the complete, ready-to-use breakdown.

Political factors

Trade policy stability

The continued evolution of UK-EU trade agreements remains a primary focus for McBride given its manufacturing footprint; by late 2025 regulatory cooperation has largely stabilized, reducing tariff uncertainty after goods trade between UK and EU fell 2.8% in 2023 but began recovering in 2024–25. Any shifts in customs procedures can still delay movement of finished goods and add border compliance costs—UK border checks increased average clearance times by ~12% in 2022. Management must monitor frameworks to maintain seamless cross-border logistics and protect distribution margins across core European markets where McBride reported ~65% of European revenue in FY2024.

Geopolitical energy risks

Ongoing tensions in the Black Sea, Middle East and Russia-Ukraine region keep European gas and oil prices volatile; EU wholesale gas averaged around €60/MWh in 2024 versus €40/MWh in 2020, raising input costs for manufacturers like McBride.

McBride’s high-capacity sites are energy-intensive, so a 20–30% uptick in energy prices can erode margins materially; in 2024 energy accounted for an estimated 5–8% of COGS for similar FMCG manufacturers.

Political instability risks sudden overhead spikes, necessitating agile pricing and hedging; firms that used forward energy contracts reduced volatility by ~15–25% in 2023–24.

Government sustainability mandates

Corporate tax shifts

Changes in corporate tax regimes across European jurisdictions can shift McBride’s net margins; for example, a 1 percentage-point rise in effective tax rate on FY2024 adjusted pre-tax profit of £40m would reduce net income by ~£0.4m.

Post-inflation fiscal tightening raises the risk of new levies on large manufacturers—OECD data showed EU government net borrowing fell to 2.6% of GDP in 2024, prompting revenue measures.

Strategic tax planning and geographic diversification—McBride’s 2024 footprint across the UK, Ireland and mainland Europe—is essential to mitigate localized fiscal shocks and preserve group cashflow.

- 1 pp tax rise ≈ £0.4m impact on FY2024 adjusted pre-tax profit

- EU net borrowing 2024: 2.6% of GDP, increasing levy risk

- Mitigants: strategic tax planning, operational diversification across UK, Ireland, mainland Europe

Supply chain security

- 2024: 18% increase in EU supplier contracts

- Procurement cost rise: ~6–9%

- FY2024 capex on supply resilience: ~£12m

Political shocks squeeze McBride: energy, trade & tax drive rising costs and resilience spend

Political risks (trade rules, energy shocks, green regs, tax shifts, reshoring) materially affect McBride: UK-EU trade volatility; EU gas €60/MWh (2024); energy = 5–8% COGS; 18% rise in EU supplier contracts (2024); £12m capex on resilience (FY2024); 1pp tax ≈ £0.4m hit.

| Metric | 2024 |

|---|---|

| EU gas | €60/MWh |

| Energy %COGS | 5–8% |

| EU suppliers | +18% |

| Capex resilience | £12m |

| 1pp tax impact | £0.4m |

What is included in the product

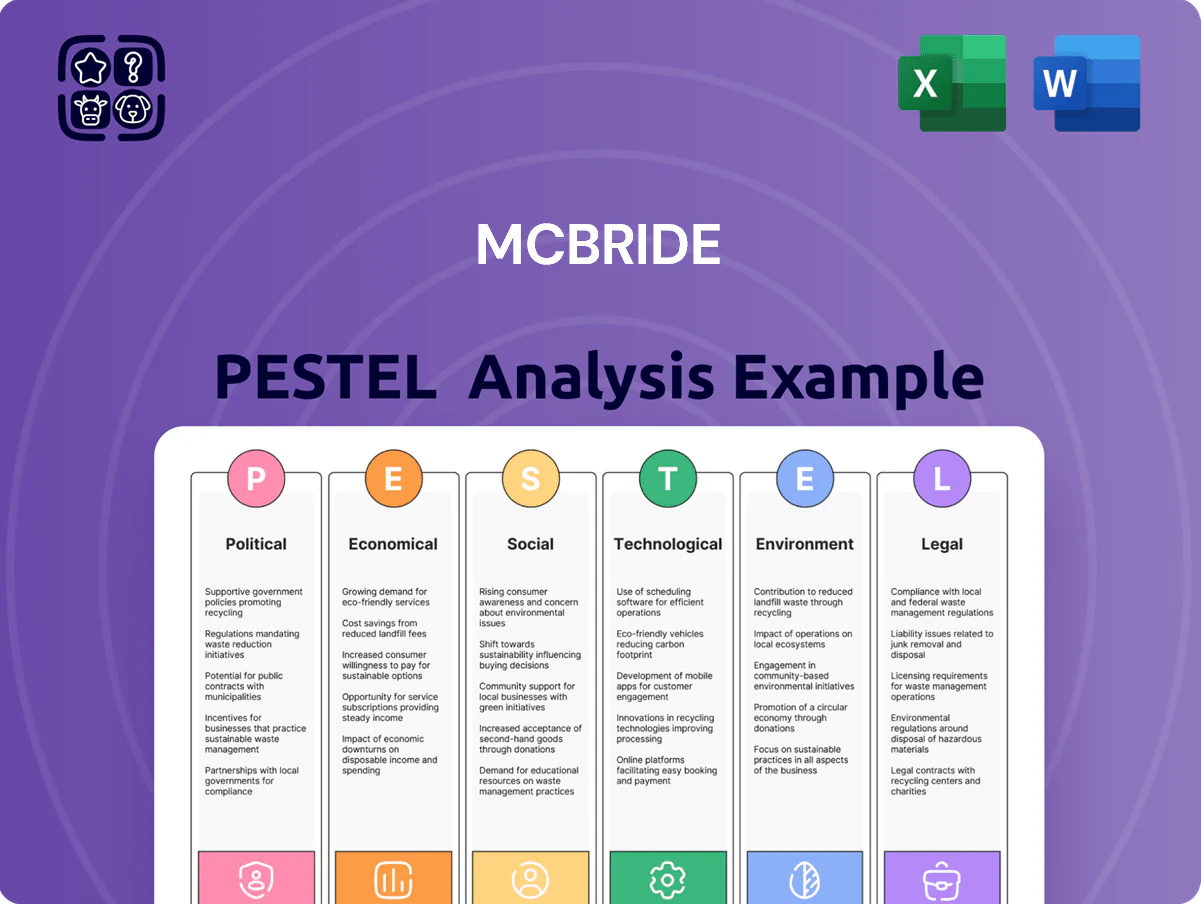

Explores how external macro-environmental factors uniquely affect McBride across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify threats and opportunities.

A concise, visually segmented PESTLE summary tailored for McBride that streamlines external risk discussions and can be dropped into presentations or shared across teams for quick alignment.

Economic factors

Private label market growth

In late 2025 private label penetration in Europe reached about 48% of grocery value, up from 45% in 2022, as consumers prioritize value; McBride, supplying detergent and household categories, benefits from retailers expanding own-brand assortments. Retailers’ private label investments grew ~6% CAGR 2022–25, supporting McBride’s stable revenue—reported FY2024 private-label sales approx. £700m—reinforcing its role as a key supplier to major chains.

Raw material price volatility

Raw material costs for chemicals, surfactants and plastic resins drive McBride’s COGS, with global resin prices up ~12% YTD in 2025 and surfactant spot indices swinging ±15% over 2023–25, increasing margin risk.

Inflation has eased to ~3% UK CPI in 2024–25, but commodity sensitivity persists amid geopolitical supply shocks that can spike input costs.

Robust hedging and centralized procurement reduced McBride’s input-cost volatility by an estimated 20% in 2024, key to preserving private-label pricing competitiveness.

Labor market tightness

Persistent labor shortages in European manufacturing have pushed average manufacturing wages up about 6–8% YoY in 2024, squeezing McBride’s margins as labor is ~20–25% of COGS; the firm must balance market-competitive pay with capex for automation—McBride’s announced 2024 productivity investments of ~£30–40m aim to offset rising human capital costs. Attracting/retaining skilled technicians remains critical to sustain consistent volumes.

Interest rate impact

Though global policy rates began normalizing toward 3.5–4.5% by end-2025, average corporate borrowing costs remain above the low-1% era, raising McBride’s interest burden on existing debt and new capex.

McBride must manage its balance sheet and cash flow tightly to prevent interest obligations from crowding out long-term growth, prioritizing disciplined capital allocation and targeted debt restructuring.

- Average policy rate range end-2025: 3.5–4.5%

- Corporate borrowing costs up vs 2010s low-1% levels

- Focus: cash flow management, capital allocation, debt restructuring

Currency exchange fluctuations

As a business operating across the Eurozone and UK, McBride faces material EUR/GBP volatility; the pair moved ~6.5% in 2024 and averaged 0.86 in 2025 YTD, affecting translated revenue and margins.

FX swings alter internal transfer costs and working capital; McBride reports using forwards, options and netting to hedge exposures and smooth reported EPS.

- EUR/GBP ~0.86 (2025 YTD)

- ~6.5% 2024 range

- Hedging via forwards, options, netting

McBride: Private‑label tailwinds vs. input, wage and FX margin pressure

Economic drivers: rising private-label share (Europe ~48% grocery value 2025) supports McBride; input-cost volatility (resins +12% YTD 2025; surfactant swings ±15% 2023–25) and wage inflation (manufacturing +6–8% YoY 2024) pressure margins; policy rates ~3.5–4.5% end-2025 lift borrowing costs; EUR/GBP ~0.86 (2025 YTD) adds FX translation risk.

| Metric | Value |

|---|---|

| EU private-label grocery share | ~48% (2025) |

| McBride FY2024 private-label sales | ~£700m |

| Resin price change | +12% YTD 2025 |

| Surfactant volatility | ±15% (2023–25) |

| Manufacturing wage rise | +6–8% YoY 2024 |

| Policy rates | 3.5–4.5% (end-2025) |

| EUR/GBP | ~0.86 (2025 YTD) |

Same Document Delivered

Mcbride PESTLE Analysis

The preview shown here is the exact McBride PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

The layout, content, and structure visible in this preview are identical to the file you’ll download immediately after buying, with no placeholders or surprises.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Get a competitive edge with our targeted PESTLE Analysis for McBride—uncover how political shifts, economic pressures, and environmental trends are reshaping the company's prospects and find actionable insights to inform investment or strategy decisions; purchase the full report for the complete, ready-to-use breakdown.

Political factors

Trade policy stability

The continued evolution of UK-EU trade agreements remains a primary focus for McBride given its manufacturing footprint; by late 2025 regulatory cooperation has largely stabilized, reducing tariff uncertainty after goods trade between UK and EU fell 2.8% in 2023 but began recovering in 2024–25. Any shifts in customs procedures can still delay movement of finished goods and add border compliance costs—UK border checks increased average clearance times by ~12% in 2022. Management must monitor frameworks to maintain seamless cross-border logistics and protect distribution margins across core European markets where McBride reported ~65% of European revenue in FY2024.

Geopolitical energy risks

Ongoing tensions in the Black Sea, Middle East and Russia-Ukraine region keep European gas and oil prices volatile; EU wholesale gas averaged around €60/MWh in 2024 versus €40/MWh in 2020, raising input costs for manufacturers like McBride.

McBride’s high-capacity sites are energy-intensive, so a 20–30% uptick in energy prices can erode margins materially; in 2024 energy accounted for an estimated 5–8% of COGS for similar FMCG manufacturers.

Political instability risks sudden overhead spikes, necessitating agile pricing and hedging; firms that used forward energy contracts reduced volatility by ~15–25% in 2023–24.

Government sustainability mandates

Corporate tax shifts

Changes in corporate tax regimes across European jurisdictions can shift McBride’s net margins; for example, a 1 percentage-point rise in effective tax rate on FY2024 adjusted pre-tax profit of £40m would reduce net income by ~£0.4m.

Post-inflation fiscal tightening raises the risk of new levies on large manufacturers—OECD data showed EU government net borrowing fell to 2.6% of GDP in 2024, prompting revenue measures.

Strategic tax planning and geographic diversification—McBride’s 2024 footprint across the UK, Ireland and mainland Europe—is essential to mitigate localized fiscal shocks and preserve group cashflow.

- 1 pp tax rise ≈ £0.4m impact on FY2024 adjusted pre-tax profit

- EU net borrowing 2024: 2.6% of GDP, increasing levy risk

- Mitigants: strategic tax planning, operational diversification across UK, Ireland, mainland Europe

Supply chain security

- 2024: 18% increase in EU supplier contracts

- Procurement cost rise: ~6–9%

- FY2024 capex on supply resilience: ~£12m

Political shocks squeeze McBride: energy, trade & tax drive rising costs and resilience spend

Political risks (trade rules, energy shocks, green regs, tax shifts, reshoring) materially affect McBride: UK-EU trade volatility; EU gas €60/MWh (2024); energy = 5–8% COGS; 18% rise in EU supplier contracts (2024); £12m capex on resilience (FY2024); 1pp tax ≈ £0.4m hit.

| Metric | 2024 |

|---|---|

| EU gas | €60/MWh |

| Energy %COGS | 5–8% |

| EU suppliers | +18% |

| Capex resilience | £12m |

| 1pp tax impact | £0.4m |

What is included in the product

Explores how external macro-environmental factors uniquely affect McBride across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify threats and opportunities.

A concise, visually segmented PESTLE summary tailored for McBride that streamlines external risk discussions and can be dropped into presentations or shared across teams for quick alignment.

Economic factors

Private label market growth

In late 2025 private label penetration in Europe reached about 48% of grocery value, up from 45% in 2022, as consumers prioritize value; McBride, supplying detergent and household categories, benefits from retailers expanding own-brand assortments. Retailers’ private label investments grew ~6% CAGR 2022–25, supporting McBride’s stable revenue—reported FY2024 private-label sales approx. £700m—reinforcing its role as a key supplier to major chains.

Raw material price volatility

Raw material costs for chemicals, surfactants and plastic resins drive McBride’s COGS, with global resin prices up ~12% YTD in 2025 and surfactant spot indices swinging ±15% over 2023–25, increasing margin risk.

Inflation has eased to ~3% UK CPI in 2024–25, but commodity sensitivity persists amid geopolitical supply shocks that can spike input costs.

Robust hedging and centralized procurement reduced McBride’s input-cost volatility by an estimated 20% in 2024, key to preserving private-label pricing competitiveness.

Labor market tightness

Persistent labor shortages in European manufacturing have pushed average manufacturing wages up about 6–8% YoY in 2024, squeezing McBride’s margins as labor is ~20–25% of COGS; the firm must balance market-competitive pay with capex for automation—McBride’s announced 2024 productivity investments of ~£30–40m aim to offset rising human capital costs. Attracting/retaining skilled technicians remains critical to sustain consistent volumes.

Interest rate impact

Though global policy rates began normalizing toward 3.5–4.5% by end-2025, average corporate borrowing costs remain above the low-1% era, raising McBride’s interest burden on existing debt and new capex.

McBride must manage its balance sheet and cash flow tightly to prevent interest obligations from crowding out long-term growth, prioritizing disciplined capital allocation and targeted debt restructuring.

- Average policy rate range end-2025: 3.5–4.5%

- Corporate borrowing costs up vs 2010s low-1% levels

- Focus: cash flow management, capital allocation, debt restructuring

Currency exchange fluctuations

As a business operating across the Eurozone and UK, McBride faces material EUR/GBP volatility; the pair moved ~6.5% in 2024 and averaged 0.86 in 2025 YTD, affecting translated revenue and margins.

FX swings alter internal transfer costs and working capital; McBride reports using forwards, options and netting to hedge exposures and smooth reported EPS.

- EUR/GBP ~0.86 (2025 YTD)

- ~6.5% 2024 range

- Hedging via forwards, options, netting

McBride: Private‑label tailwinds vs. input, wage and FX margin pressure

Economic drivers: rising private-label share (Europe ~48% grocery value 2025) supports McBride; input-cost volatility (resins +12% YTD 2025; surfactant swings ±15% 2023–25) and wage inflation (manufacturing +6–8% YoY 2024) pressure margins; policy rates ~3.5–4.5% end-2025 lift borrowing costs; EUR/GBP ~0.86 (2025 YTD) adds FX translation risk.

| Metric | Value |

|---|---|

| EU private-label grocery share | ~48% (2025) |

| McBride FY2024 private-label sales | ~£700m |

| Resin price change | +12% YTD 2025 |

| Surfactant volatility | ±15% (2023–25) |

| Manufacturing wage rise | +6–8% YoY 2024 |

| Policy rates | 3.5–4.5% (end-2025) |

| EUR/GBP | ~0.86 (2025 YTD) |

Same Document Delivered

Mcbride PESTLE Analysis

The preview shown here is the exact McBride PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

The layout, content, and structure visible in this preview are identical to the file you’ll download immediately after buying, with no placeholders or surprises.