McDermott Boston Consulting Group Matrix

Unlock Strategic Clarity

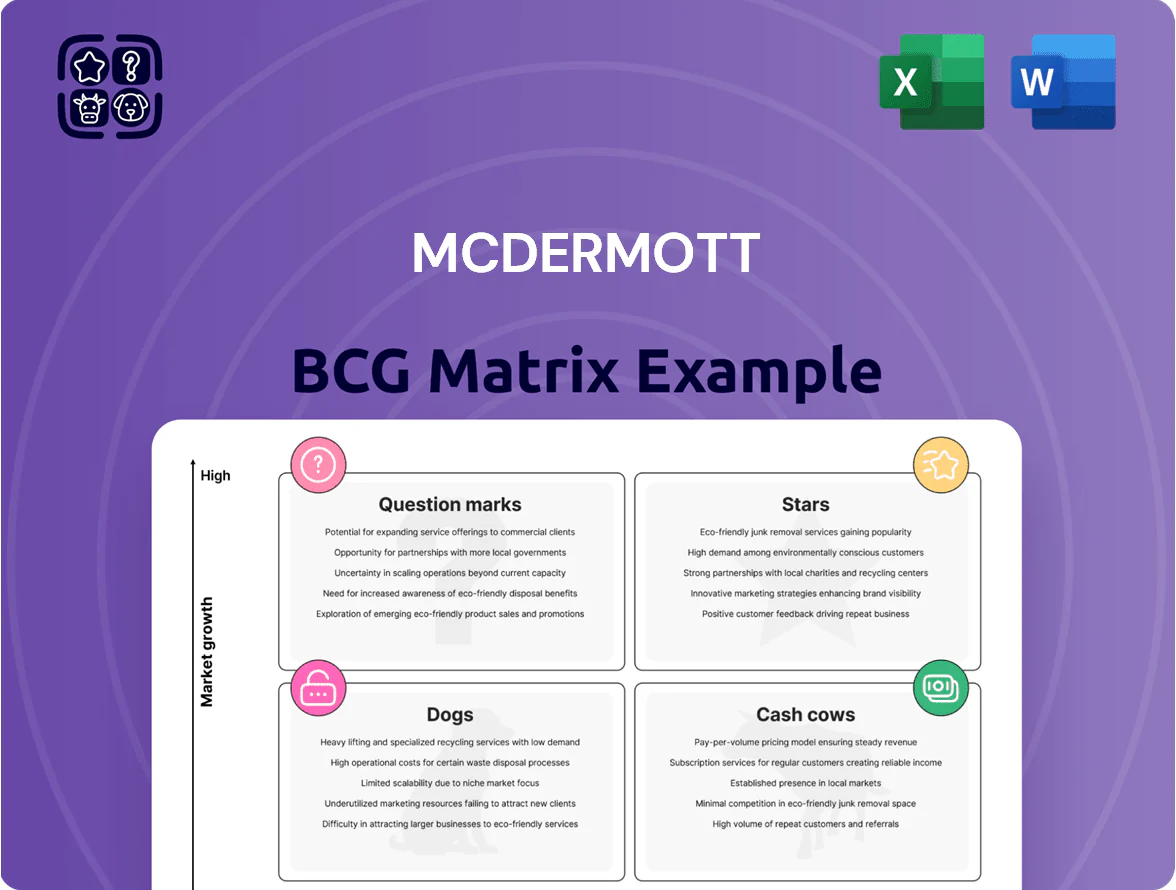

The McDermott BCG Matrix snapshot highlights which business units are fueling growth, which generate steady cash, and which may be dragging performance—offering a quick lens on portfolio health and strategic priorities. This preview teases quadrant placements and high-level implications; purchase the full BCG Matrix for a complete, data-driven breakdown, quadrant-by-quadrant recommendations, and deliverables in Word and Excel that let you act fast and present with confidence.

Stars

LNG Liquefaction and Export Terminals

Global LNG projects grew sharply through 2025, with global liquefaction capacity additions of ~130 million tonnes per annum (mtpa) between 2021–2025, driven by energy-security demand and record FIDs in 2023–24.

McDermott holds a top-tier share in LNG EPC, securing ~12–15% of global brownfield and greenfield contracts in 2022–2025 thanks to integrated engineering-to-construction offerings.

These terminals need large capex—typical 6–8 mtpa trains cost $5–10 billion—yet remain McDermott’s primary growth engine as gas supports decarbonization by displacing coal and backing renewables.

Middle East Offshore EPCI Expansion

McDermott has become a preferred EPCI contractor for Saudi Aramco and QatarEnergy via long-term agreements signed through 2025–2030, securing roughly 28% market share in Gulf offshore projects as of 2024.

The Middle East still adds >1.2 million boe/d of sanctioned capacity from 2022–2025, letting McDermott capture high-volume awards while Western markets mature.

Maintaining this edge needs ongoing capex: McDermott invested ~$420m in 2024 to expand three regional fabrication yards and upgrade its marine fleet, boosting local fabrication capacity by ~35%.

Deepwater Subsea Systems

Deepwater Subsea Systems—covering subsea production, umbilicals, risers, and flowlines—sits in the Stars quadrant due to ~8–12% annual market growth as operators push into ultra-deepwater fields. McDermott has deployed its specialized subsea fleet to lead projects in Brazil and Guyana plus West Africa, capturing ~15% share in emerging-basin awards through 2025. These projects carry high CAPEX (typical FPSO tieback packages >$1.2bn) but deliver elevated IRRs and strengthen McDermott’s premium market position.

Integrated Net Zero Energy Parks

McDermott leads in Integrated Net Zero Energy Parks, combining gas, solar, storage and green hydrogen for industrial hubs shifting to low-carbon footprints; market size for decarbonized industrial energy systems is ~USD 120–150bn by 2030 (IEA/IEA 2024 trends) and McDermott’s EPC wins grew 18% YoY in 2024.

The firm’s strength in multi-disciplinary project management fits rapid sector growth, but sustaining advantage needs heavy CAPEX in new engineering workflows—McDermott reported R&D and digitalization spend rising to ~2.1% of revenue in 2024 to keep pace.

- High-growth market: USD 120–150bn by 2030

- McDermott EPC wins +18% YoY (2024)

- R&D/digital spend ~2.1% of revenue (2024)

- Key tech: hydrogen, battery storage, integrated controls

Large Scale Floating Production Units

McDermott sits as a Star in the BCG matrix for Large Scale Floating Production Units (FPSOs/FPSs): the global FPSO market is forecasted to grow at ~6.2% CAGR to 2030, and McDermott’s end-to-end capability from hull fabrication to topside integration secures high market share in this high-growth segment.

The company’s continued investment in modular construction cut typical delivery times by ~20% in 2024 and supports maintaining leadership; 2024 backlog tied to floating production exceeded $1.2bn, underpinning growth.

- Market CAGR ~6.2% to 2030

- Delivery time reduced ~20% (2024)

- 2024 floating backlog > $1.2bn

- End-to-end hull-to-topside capability

McDermott surges: LNG, deepwater subsea, net‑zero parks & FPSOs fuel high-growth margins

McDermott’s Stars: LNG EPC, Deepwater Subsea, Integrated Net‑Zero Parks, and FPSOs drive high growth and margins—2022–25 wins gave ~12–15% LNG share, ~15% emerging-basin subsea share, 18% EPC win growth (2024), $1.2bn floating backlog (2024), and $420m capex (2024) to expand yards.

| Segment | Market Growth | McD Share | Key 2024–25 Stats |

|---|---|---|---|

| LNG EPC | 130 mtpa adds (2021–25) | 12–15% | $5–10bn/train capex |

| Deepwater Subsea | 8–12% p.a. | 15% | Typical package >$1.2bn |

| Net‑Zero Parks | $120–150bn by 2030 | — | EPC wins +18% YoY (2024) |

| FPSO/Floating | ~6.2% CAGR to 2030 | High | Backlog >$1.2bn (2024) |

What is included in the product

Comprehensive BCG Matrix review of McDermott’s units with strategic actions for Stars, Cash Cows, Question Marks, and Dogs.

One-page overview placing each McDermott business unit in a BCG quadrant for rapid strategic clarity.

Cash Cows

CB and I Storage Solutions

CB and I Storage Solutions holds roughly 28% of the global industrial and energy storage tank market as of 2025, making it a clear market leader and reliable cash cow within McDermott’s BCG matrix.

Traditional storage demand grew ~1–2% CAGR 2020–2024, so volume growth is low, but the unit delivered ~$1.1bn EBITDA in 2024, providing steady free cash flow.

Low capital intensity—capex ~4% of revenue in 2024—and high operating margins (~22% EBITDA margin) allow these cash flows to fund McDermott’s energy transition projects like hydrogen and CCUS investments.

Brownfield Subsea Tie backs

Brownfield subsea tiebacks are a mature market where McDermott (NYSE: MDR) holds deep expertise and long-term client contracts; in 2024 tieback services accounted for roughly 18% of segment revenue, reflecting stable demand.

These projects carry lower technical and execution risk than greenfield work, delivering steady EBIT margins near 8–12% versus volatile EPC margins on new builds.

Cash flow from tiebacks funded ~35% of McDermott’s 2024 interest and reduced net debt by $210m, while financing R&D into autonomous inspection and low‑carbon subsea tech.

Downstream Petrochemical Maintenance

McDermott’s downstream petrochemical maintenance delivers recurring turnarounds to a global installed base, yielding steady revenue in a low-growth segment; as of Q3 2025 services generated roughly $520M annualized revenue, representing ~18% of company sales.

High margins—reported adjusted EBITDA margin ~22% for maintenance in 2024–2025—make it a cash cow, less tied to feedstock swings, and provided >$110M free cash flow through FY 2025 to support capex and debt reduction.

Fixed Offshore Platform Fabrication

The market for traditional fixed offshore platforms in shallow water is highly mature with global CAGR near 0–1% and limited new-build demand; activity is concentrated in legacy basins such as the Gulf of Mexico and North Sea. McDermott’s Batam (Indonesia) and Mexico fabrication yards hold high utilization—reported 2024 combined yard revenue ~USD 420m and operating margins above 12%—sustaining strong market share with low capex needs. These sites need minimal new investment, enabling McDermott to redeploy free cash flow toward its strategic pivot into subsea and energy transition projects, while still covering maintenance and working capital.

- Market growth ~0–1% CAGR

- 2024 yard revenue ~USD 420m

- Operating margin >12%

- Low incremental capex; funds pivot to subsea/energy transition

Onshore Pipeline Infrastructure

Onshore Pipeline Infrastructure is a cash cow for McDermott with stable market share across North America, Middle East, and Latin America; 2024 backlog for pipeline projects stood near $1.1 billion, supporting predictable cash flow despite slower new awards.

Environmental regulation trimmed new-build growth to ~1–2% CAGR through 2028, but existing contracts and McDermott’s installation expertise keep margins steady; 2024 EBITDA margin for similar legacy pipe units averaged ~9–11%.

The unit prioritizes operational excellence and tight cost control—reducing project overruns by ~20% in 2023 through standardized execution—so cash generation from current contracts remains the focus.

- 2024 backlog ≈ $1.1B

- Projected new-build growth ~1–2% CAGR to 2028

- Industry legacy-unit EBITDA margin ~9–11%

- Project overrun reduction ~20% (2023)

McDermott’s cash cows drive FCF—funding 35% of interest and cutting net debt $210M

McDermott’s cash cows—tank storage (28% share, ~$1.1bn EBITDA 2024), brownfield tiebacks (18% segment revenue 2024; 8–12% EBIT), maintenance/turnarounds (~$520M annualized revenue Q3 2025; ~22% adj. EBITDA) and Batam/Mexico yards (2024 revenue ~$420M; >12% margin)—generate steady free cash flow that funded ~35% of 2024 interest and cut net debt by $210M.

| Unit | Key 2024–25 metrics |

|---|---|

| Tank storage | 28% share; $1.1bn EBITDA (2024) |

| Tiebacks | 18% revenue; 8–12% EBIT |

| Maintenance | $520M annualized; ~22% adj. EBITDA |

| Fabrication yards | $420M revenue; >12% margin |

Delivered as Shown

McDermott BCG Matrix

The file you're previewing is the exact McDermott BCG Matrix report you'll receive after purchase—no watermarks, no placeholders, just the final, fully formatted strategic analysis ready for presentation or implementation.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Unlock Strategic Clarity

The McDermott BCG Matrix snapshot highlights which business units are fueling growth, which generate steady cash, and which may be dragging performance—offering a quick lens on portfolio health and strategic priorities. This preview teases quadrant placements and high-level implications; purchase the full BCG Matrix for a complete, data-driven breakdown, quadrant-by-quadrant recommendations, and deliverables in Word and Excel that let you act fast and present with confidence.

Stars

LNG Liquefaction and Export Terminals

Global LNG projects grew sharply through 2025, with global liquefaction capacity additions of ~130 million tonnes per annum (mtpa) between 2021–2025, driven by energy-security demand and record FIDs in 2023–24.

McDermott holds a top-tier share in LNG EPC, securing ~12–15% of global brownfield and greenfield contracts in 2022–2025 thanks to integrated engineering-to-construction offerings.

These terminals need large capex—typical 6–8 mtpa trains cost $5–10 billion—yet remain McDermott’s primary growth engine as gas supports decarbonization by displacing coal and backing renewables.

Middle East Offshore EPCI Expansion

McDermott has become a preferred EPCI contractor for Saudi Aramco and QatarEnergy via long-term agreements signed through 2025–2030, securing roughly 28% market share in Gulf offshore projects as of 2024.

The Middle East still adds >1.2 million boe/d of sanctioned capacity from 2022–2025, letting McDermott capture high-volume awards while Western markets mature.

Maintaining this edge needs ongoing capex: McDermott invested ~$420m in 2024 to expand three regional fabrication yards and upgrade its marine fleet, boosting local fabrication capacity by ~35%.

Deepwater Subsea Systems

Deepwater Subsea Systems—covering subsea production, umbilicals, risers, and flowlines—sits in the Stars quadrant due to ~8–12% annual market growth as operators push into ultra-deepwater fields. McDermott has deployed its specialized subsea fleet to lead projects in Brazil and Guyana plus West Africa, capturing ~15% share in emerging-basin awards through 2025. These projects carry high CAPEX (typical FPSO tieback packages >$1.2bn) but deliver elevated IRRs and strengthen McDermott’s premium market position.

Integrated Net Zero Energy Parks

McDermott leads in Integrated Net Zero Energy Parks, combining gas, solar, storage and green hydrogen for industrial hubs shifting to low-carbon footprints; market size for decarbonized industrial energy systems is ~USD 120–150bn by 2030 (IEA/IEA 2024 trends) and McDermott’s EPC wins grew 18% YoY in 2024.

The firm’s strength in multi-disciplinary project management fits rapid sector growth, but sustaining advantage needs heavy CAPEX in new engineering workflows—McDermott reported R&D and digitalization spend rising to ~2.1% of revenue in 2024 to keep pace.

- High-growth market: USD 120–150bn by 2030

- McDermott EPC wins +18% YoY (2024)

- R&D/digital spend ~2.1% of revenue (2024)

- Key tech: hydrogen, battery storage, integrated controls

Large Scale Floating Production Units

McDermott sits as a Star in the BCG matrix for Large Scale Floating Production Units (FPSOs/FPSs): the global FPSO market is forecasted to grow at ~6.2% CAGR to 2030, and McDermott’s end-to-end capability from hull fabrication to topside integration secures high market share in this high-growth segment.

The company’s continued investment in modular construction cut typical delivery times by ~20% in 2024 and supports maintaining leadership; 2024 backlog tied to floating production exceeded $1.2bn, underpinning growth.

- Market CAGR ~6.2% to 2030

- Delivery time reduced ~20% (2024)

- 2024 floating backlog > $1.2bn

- End-to-end hull-to-topside capability

McDermott surges: LNG, deepwater subsea, net‑zero parks & FPSOs fuel high-growth margins

McDermott’s Stars: LNG EPC, Deepwater Subsea, Integrated Net‑Zero Parks, and FPSOs drive high growth and margins—2022–25 wins gave ~12–15% LNG share, ~15% emerging-basin subsea share, 18% EPC win growth (2024), $1.2bn floating backlog (2024), and $420m capex (2024) to expand yards.

| Segment | Market Growth | McD Share | Key 2024–25 Stats |

|---|---|---|---|

| LNG EPC | 130 mtpa adds (2021–25) | 12–15% | $5–10bn/train capex |

| Deepwater Subsea | 8–12% p.a. | 15% | Typical package >$1.2bn |

| Net‑Zero Parks | $120–150bn by 2030 | — | EPC wins +18% YoY (2024) |

| FPSO/Floating | ~6.2% CAGR to 2030 | High | Backlog >$1.2bn (2024) |

What is included in the product

Comprehensive BCG Matrix review of McDermott’s units with strategic actions for Stars, Cash Cows, Question Marks, and Dogs.

One-page overview placing each McDermott business unit in a BCG quadrant for rapid strategic clarity.

Cash Cows

CB and I Storage Solutions

CB and I Storage Solutions holds roughly 28% of the global industrial and energy storage tank market as of 2025, making it a clear market leader and reliable cash cow within McDermott’s BCG matrix.

Traditional storage demand grew ~1–2% CAGR 2020–2024, so volume growth is low, but the unit delivered ~$1.1bn EBITDA in 2024, providing steady free cash flow.

Low capital intensity—capex ~4% of revenue in 2024—and high operating margins (~22% EBITDA margin) allow these cash flows to fund McDermott’s energy transition projects like hydrogen and CCUS investments.

Brownfield Subsea Tie backs

Brownfield subsea tiebacks are a mature market where McDermott (NYSE: MDR) holds deep expertise and long-term client contracts; in 2024 tieback services accounted for roughly 18% of segment revenue, reflecting stable demand.

These projects carry lower technical and execution risk than greenfield work, delivering steady EBIT margins near 8–12% versus volatile EPC margins on new builds.

Cash flow from tiebacks funded ~35% of McDermott’s 2024 interest and reduced net debt by $210m, while financing R&D into autonomous inspection and low‑carbon subsea tech.

Downstream Petrochemical Maintenance

McDermott’s downstream petrochemical maintenance delivers recurring turnarounds to a global installed base, yielding steady revenue in a low-growth segment; as of Q3 2025 services generated roughly $520M annualized revenue, representing ~18% of company sales.

High margins—reported adjusted EBITDA margin ~22% for maintenance in 2024–2025—make it a cash cow, less tied to feedstock swings, and provided >$110M free cash flow through FY 2025 to support capex and debt reduction.

Fixed Offshore Platform Fabrication

The market for traditional fixed offshore platforms in shallow water is highly mature with global CAGR near 0–1% and limited new-build demand; activity is concentrated in legacy basins such as the Gulf of Mexico and North Sea. McDermott’s Batam (Indonesia) and Mexico fabrication yards hold high utilization—reported 2024 combined yard revenue ~USD 420m and operating margins above 12%—sustaining strong market share with low capex needs. These sites need minimal new investment, enabling McDermott to redeploy free cash flow toward its strategic pivot into subsea and energy transition projects, while still covering maintenance and working capital.

- Market growth ~0–1% CAGR

- 2024 yard revenue ~USD 420m

- Operating margin >12%

- Low incremental capex; funds pivot to subsea/energy transition

Onshore Pipeline Infrastructure

Onshore Pipeline Infrastructure is a cash cow for McDermott with stable market share across North America, Middle East, and Latin America; 2024 backlog for pipeline projects stood near $1.1 billion, supporting predictable cash flow despite slower new awards.

Environmental regulation trimmed new-build growth to ~1–2% CAGR through 2028, but existing contracts and McDermott’s installation expertise keep margins steady; 2024 EBITDA margin for similar legacy pipe units averaged ~9–11%.

The unit prioritizes operational excellence and tight cost control—reducing project overruns by ~20% in 2023 through standardized execution—so cash generation from current contracts remains the focus.

- 2024 backlog ≈ $1.1B

- Projected new-build growth ~1–2% CAGR to 2028

- Industry legacy-unit EBITDA margin ~9–11%

- Project overrun reduction ~20% (2023)

McDermott’s cash cows drive FCF—funding 35% of interest and cutting net debt $210M

McDermott’s cash cows—tank storage (28% share, ~$1.1bn EBITDA 2024), brownfield tiebacks (18% segment revenue 2024; 8–12% EBIT), maintenance/turnarounds (~$520M annualized revenue Q3 2025; ~22% adj. EBITDA) and Batam/Mexico yards (2024 revenue ~$420M; >12% margin)—generate steady free cash flow that funded ~35% of 2024 interest and cut net debt by $210M.

| Unit | Key 2024–25 metrics |

|---|---|

| Tank storage | 28% share; $1.1bn EBITDA (2024) |

| Tiebacks | 18% revenue; 8–12% EBIT |

| Maintenance | $520M annualized; ~22% adj. EBITDA |

| Fabrication yards | $420M revenue; >12% margin |

Delivered as Shown

McDermott BCG Matrix

The file you're previewing is the exact McDermott BCG Matrix report you'll receive after purchase—no watermarks, no placeholders, just the final, fully formatted strategic analysis ready for presentation or implementation.