McKinsey & Company Porter's Five Forces Analysis

Don't Miss the Bigger Picture

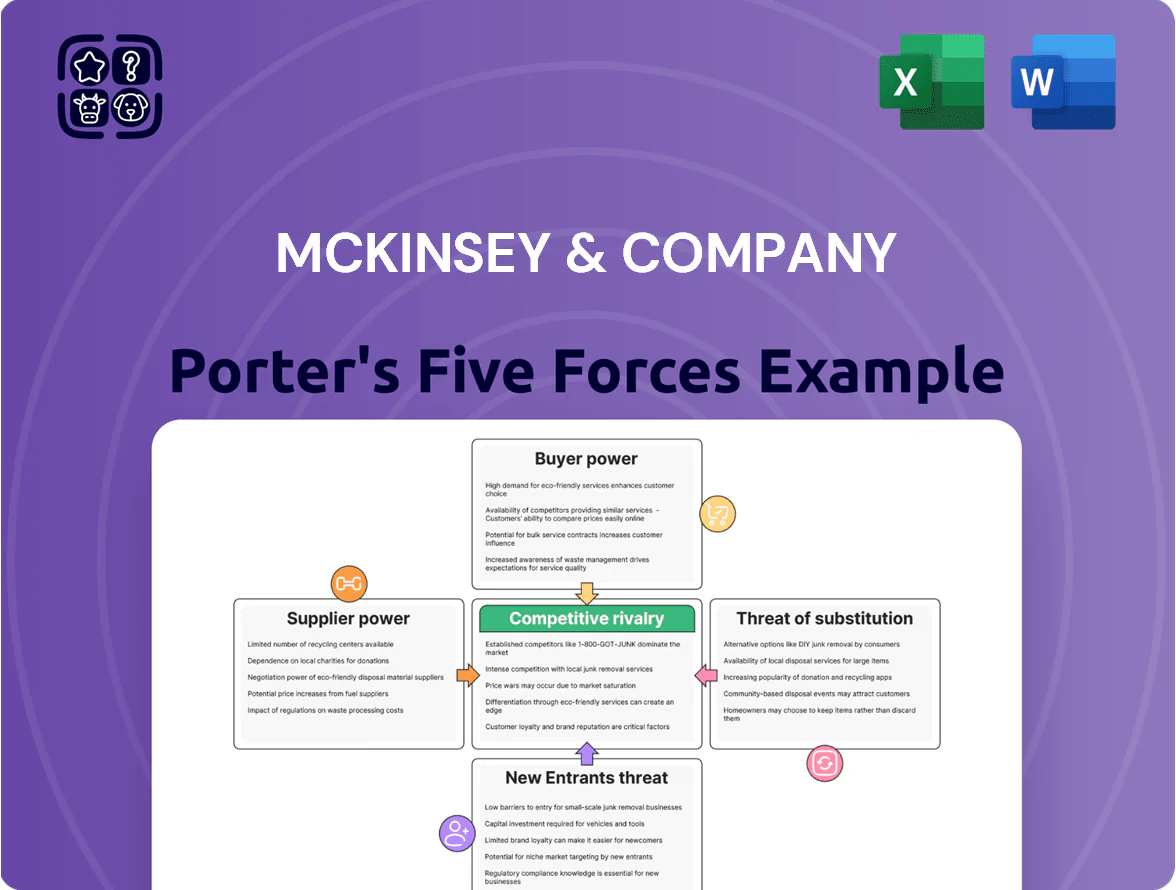

McKinsey & Company's Porter's Five Forces snapshot highlights intense competition among top consultancies, moderate buyer power driven by large corporate clients, high supplier (talent) influence, low threat of substitutes for complex strategic advisory, and barriers limiting new entrants; this brief overview points to nuanced strategic levers and risks worth exploring further. Unlock the full Porter's Five Forces Analysis to access force-by-force ratings, visuals, and actionable insights tailored to McKinsey & Company.

Suppliers Bargaining Power

Elite Talent Acquisition

Elite Talent Acquisition: Suppliers are top professionals and Ivy-League graduates; by Q4 2025 demand for AI/data-science skills rose ~38% year-over-year, per LinkedIn Economic Graph, pushing starting offers at McKinsey-level firms toward $250k–$350k total comp to compete with tech and private equity.

Specialized Technology and Cloud Providers

McKinsey depends on cloud and AI vendors—AWS, Microsoft Azure, Google Cloud, OpenAI—for core analytics; in 2024 cloud spend among top consultancies rose ~18% year-over-year, pushing supplier leverage up.

These platforms are essential, so suppliers can demand premium SLAs and licensing; high-performance compute costs and enterprise AI licenses can eat several percentage points of operating margin—est. 2–4% impact on peers in 2024.

Expert Network Platforms

McKinsey increasingly taps external expert networks for niche insights; in 2024 the firm’s project mix showed ~22% higher use of third-party SMEs on complex technical engagements versus 2019, raising supplier leverage. These networks control scarce, non-public industrial know-how and set premium rates—top-tier experts command $500–1,200 hourly in 2025—so supplier bargaining power rises as client needs get more technical.

Data and Information Vendors

Access to comprehensive global market and financial data is vital for McKinsey’s frameworks; major providers like Refinitiv, Bloomberg, and S&P Global can command high annual fees—Bloomberg Terminal costs ~USD 28,000 per seat in 2025—giving them strong supplier power.

Loss or degradation of continuous, high-quality feeds would weaken McKinsey’s benchmarking and model accuracy, raising client delivery risk and cost to replace data.

- Key vendors: Bloomberg, Refinitiv, S&P Global

- Bloomberg Terminal ~USD 28,000/seat (2025)

- High switching costs for proprietary datasets

- Data quality tied to consulting output credibility

Global Support and Infrastructure Services

Maintaining global offices forces McKinsey to contract premium real estate, travel, and specialized legal services; in 2024 McKinsey’s estimated global facilities and travel spend likely exceeded $1.2 billion, giving top-tier suppliers modest leverage due to security and high-end requirements.

These services are partly commoditized, so McKinsey can negotiate rates, but unique security, client confidentiality, and prestige-grade space sustain supplier bargaining power that translates into unavoidable brand-preservation costs.

- Estimated facilities & travel spend ≈ $1.2B (2024)

- Premium suppliers earn leverage from security/confidentiality needs

- Commoditization limits but does not eliminate leverage

- Costs tied to brand image and global reach are non-negotiable

Suppliers wield moderate-to-high power: talent, cloud, experts, data, travel drive costs

Suppliers (elite talent, cloud/AI vendors, expert networks, data providers, premium real estate) hold moderate-to-high bargaining power for McKinsey in 2024–25—key numbers: AI talent comp $250k–$350k, cloud spend +18% y/y (2024), expert rates $500–1,200/hr (2025), Bloomberg Terminal ≈ USD 28,000/seat (2025), facilities & travel ≈ $1.2B (2024).

| Supplier | Key metric |

|---|---|

| Talent | $250k–$350k comp |

| Cloud/AI | +18% spend (2024) |

| Expert networks | $500–$1,200/hr (2025) |

| Data providers | Bloomberg ≈ $28,000/seat (2025) |

| Facilities & travel | ≈ $1.2B (2024) |

What is included in the product

Tailored exclusively for McKinsey & Company, this Porter's Five Forces analysis uncovers key drivers of competition, customer and supplier influence, entry barriers, substitutes, and emerging disruptions that shape its profitability and strategic positioning.

Concise, one-sheet Porter’s Five Forces tailored by McKinsey—quickly assess competitive pressure and make faster strategic decisions.

Customers Bargaining Power

Corporate Client Concentration

A significant share of McKinsey & Company revenue—estimated at ~25–35% in 2024—comes from a small set of Fortune Global 500 firms and large governments, concentrating bargaining power. These clients can demand discounted fees, extended payment terms, and deep customization, raising delivery costs. Their ability to shift $50m+ engagements to rivals gives them leverage in fee and scope negotiations. This concentration raises client churn and margin pressure risks.

Increased Fee Transparency

By end-2025 clients benchmark consulting fees tightly: 62% of Fortune 500 procurement teams use value-based fee comparisons, per a 2025 Procurement Leaders survey, forcing McKinsey to show granular cost breakdowns and ROI estimates.

Procurement-led hiring rose to 48% of engagements in 2024–25, shrinking room for premium on standardized strategy work and compressing margins by an estimated 150–300 basis points on repeat playbooks.

Growth of Internal Strategy Teams

Low Switching Costs between Elite Firms

Despite McKinsey’s strong brand and global reach, switching costs to rivals like Boston Consulting Group (BCG) or Bain remain low for large clients, who often split engagements to maintain competitive tension; surveys show ~60% of Fortune 500 firms used multiple top-tier consultancies in 2024.

This dynamic forces McKinsey to prove superior ROI and outcomes continuously—client retention hinges on measurable impact, with repeat engagement rates reportedly near 70% but vulnerable to performance dips.

- ~60% Fortune 500 use multiple firms (2024)

- Repeat engagement ~70%

- Low contractual lock-in, high performance pressure

Shift Toward Outcome-Based Pricing

Clients increasingly demand outcome-based pricing, tying fees to milestones or ROI; McKinsey reported in 2024 that 28% of large clients sought at least one pay-for-performance element in engagements.

This shifts financial risk to consultants and boosts buyer control over profitability, pressuring margins as firms absorb downside when targets slip.

Buyers now resist high daily rates without guaranteed, measurable performance gains—surveys show 62% of C-suite execs prefer fee models linked to cost savings or revenue uplift.

- 28% of large clients requested pay-for-performance in 2024

- 62% of C-suite prefer outcome-linked fees

- Risk shifts to consultants, squeezing margins

Big clients, tight margins: 25–35% revenue concentration, rising outcome fees

Large clients concentrate leverage: 25–35% McKinsey revenue from Fortune Global 500/governments (2024), 60% use multiple top firms (2024), repeat engagements ~70%, 38% Fortune 500 have in-house strategy (2024). Procurement-led hires 48% (2024–25) compress margins ~150–300 bps. Pay-for-performance demand 28% (2024); 62% C-suite prefer outcome-linked fees.

| Metric | Value |

|---|---|

| Revenue concentration | 25–35% (2024) |

| Multiple firms | 60% (2024) |

| Repeat rate | ~70% (2024) |

| In-house strategy | 38% (2024) |

| Procurement-led | 48% (2024–25) |

| Pay-for-performance | 28% (2024) |

Preview Before You Purchase

McKinsey & Company Porter's Five Forces Analysis

This preview shows the exact McKinsey & Company Porter’s Five Forces analysis you’ll receive immediately after purchase—fully formatted, professionally written, and ready for use without placeholders or samples.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

McKinsey & Company's Porter's Five Forces snapshot highlights intense competition among top consultancies, moderate buyer power driven by large corporate clients, high supplier (talent) influence, low threat of substitutes for complex strategic advisory, and barriers limiting new entrants; this brief overview points to nuanced strategic levers and risks worth exploring further. Unlock the full Porter's Five Forces Analysis to access force-by-force ratings, visuals, and actionable insights tailored to McKinsey & Company.

Suppliers Bargaining Power

Elite Talent Acquisition

Elite Talent Acquisition: Suppliers are top professionals and Ivy-League graduates; by Q4 2025 demand for AI/data-science skills rose ~38% year-over-year, per LinkedIn Economic Graph, pushing starting offers at McKinsey-level firms toward $250k–$350k total comp to compete with tech and private equity.

Specialized Technology and Cloud Providers

McKinsey depends on cloud and AI vendors—AWS, Microsoft Azure, Google Cloud, OpenAI—for core analytics; in 2024 cloud spend among top consultancies rose ~18% year-over-year, pushing supplier leverage up.

These platforms are essential, so suppliers can demand premium SLAs and licensing; high-performance compute costs and enterprise AI licenses can eat several percentage points of operating margin—est. 2–4% impact on peers in 2024.

Expert Network Platforms

McKinsey increasingly taps external expert networks for niche insights; in 2024 the firm’s project mix showed ~22% higher use of third-party SMEs on complex technical engagements versus 2019, raising supplier leverage. These networks control scarce, non-public industrial know-how and set premium rates—top-tier experts command $500–1,200 hourly in 2025—so supplier bargaining power rises as client needs get more technical.

Data and Information Vendors

Access to comprehensive global market and financial data is vital for McKinsey’s frameworks; major providers like Refinitiv, Bloomberg, and S&P Global can command high annual fees—Bloomberg Terminal costs ~USD 28,000 per seat in 2025—giving them strong supplier power.

Loss or degradation of continuous, high-quality feeds would weaken McKinsey’s benchmarking and model accuracy, raising client delivery risk and cost to replace data.

- Key vendors: Bloomberg, Refinitiv, S&P Global

- Bloomberg Terminal ~USD 28,000/seat (2025)

- High switching costs for proprietary datasets

- Data quality tied to consulting output credibility

Global Support and Infrastructure Services

Maintaining global offices forces McKinsey to contract premium real estate, travel, and specialized legal services; in 2024 McKinsey’s estimated global facilities and travel spend likely exceeded $1.2 billion, giving top-tier suppliers modest leverage due to security and high-end requirements.

These services are partly commoditized, so McKinsey can negotiate rates, but unique security, client confidentiality, and prestige-grade space sustain supplier bargaining power that translates into unavoidable brand-preservation costs.

- Estimated facilities & travel spend ≈ $1.2B (2024)

- Premium suppliers earn leverage from security/confidentiality needs

- Commoditization limits but does not eliminate leverage

- Costs tied to brand image and global reach are non-negotiable

Suppliers wield moderate-to-high power: talent, cloud, experts, data, travel drive costs

Suppliers (elite talent, cloud/AI vendors, expert networks, data providers, premium real estate) hold moderate-to-high bargaining power for McKinsey in 2024–25—key numbers: AI talent comp $250k–$350k, cloud spend +18% y/y (2024), expert rates $500–1,200/hr (2025), Bloomberg Terminal ≈ USD 28,000/seat (2025), facilities & travel ≈ $1.2B (2024).

| Supplier | Key metric |

|---|---|

| Talent | $250k–$350k comp |

| Cloud/AI | +18% spend (2024) |

| Expert networks | $500–$1,200/hr (2025) |

| Data providers | Bloomberg ≈ $28,000/seat (2025) |

| Facilities & travel | ≈ $1.2B (2024) |

What is included in the product

Tailored exclusively for McKinsey & Company, this Porter's Five Forces analysis uncovers key drivers of competition, customer and supplier influence, entry barriers, substitutes, and emerging disruptions that shape its profitability and strategic positioning.

Concise, one-sheet Porter’s Five Forces tailored by McKinsey—quickly assess competitive pressure and make faster strategic decisions.

Customers Bargaining Power

Corporate Client Concentration

A significant share of McKinsey & Company revenue—estimated at ~25–35% in 2024—comes from a small set of Fortune Global 500 firms and large governments, concentrating bargaining power. These clients can demand discounted fees, extended payment terms, and deep customization, raising delivery costs. Their ability to shift $50m+ engagements to rivals gives them leverage in fee and scope negotiations. This concentration raises client churn and margin pressure risks.

Increased Fee Transparency

By end-2025 clients benchmark consulting fees tightly: 62% of Fortune 500 procurement teams use value-based fee comparisons, per a 2025 Procurement Leaders survey, forcing McKinsey to show granular cost breakdowns and ROI estimates.

Procurement-led hiring rose to 48% of engagements in 2024–25, shrinking room for premium on standardized strategy work and compressing margins by an estimated 150–300 basis points on repeat playbooks.

Growth of Internal Strategy Teams

Low Switching Costs between Elite Firms

Despite McKinsey’s strong brand and global reach, switching costs to rivals like Boston Consulting Group (BCG) or Bain remain low for large clients, who often split engagements to maintain competitive tension; surveys show ~60% of Fortune 500 firms used multiple top-tier consultancies in 2024.

This dynamic forces McKinsey to prove superior ROI and outcomes continuously—client retention hinges on measurable impact, with repeat engagement rates reportedly near 70% but vulnerable to performance dips.

- ~60% Fortune 500 use multiple firms (2024)

- Repeat engagement ~70%

- Low contractual lock-in, high performance pressure

Shift Toward Outcome-Based Pricing

Clients increasingly demand outcome-based pricing, tying fees to milestones or ROI; McKinsey reported in 2024 that 28% of large clients sought at least one pay-for-performance element in engagements.

This shifts financial risk to consultants and boosts buyer control over profitability, pressuring margins as firms absorb downside when targets slip.

Buyers now resist high daily rates without guaranteed, measurable performance gains—surveys show 62% of C-suite execs prefer fee models linked to cost savings or revenue uplift.

- 28% of large clients requested pay-for-performance in 2024

- 62% of C-suite prefer outcome-linked fees

- Risk shifts to consultants, squeezing margins

Big clients, tight margins: 25–35% revenue concentration, rising outcome fees

Large clients concentrate leverage: 25–35% McKinsey revenue from Fortune Global 500/governments (2024), 60% use multiple top firms (2024), repeat engagements ~70%, 38% Fortune 500 have in-house strategy (2024). Procurement-led hires 48% (2024–25) compress margins ~150–300 bps. Pay-for-performance demand 28% (2024); 62% C-suite prefer outcome-linked fees.

| Metric | Value |

|---|---|

| Revenue concentration | 25–35% (2024) |

| Multiple firms | 60% (2024) |

| Repeat rate | ~70% (2024) |

| In-house strategy | 38% (2024) |

| Procurement-led | 48% (2024–25) |

| Pay-for-performance | 28% (2024) |

Preview Before You Purchase

McKinsey & Company Porter's Five Forces Analysis

This preview shows the exact McKinsey & Company Porter’s Five Forces analysis you’ll receive immediately after purchase—fully formatted, professionally written, and ready for use without placeholders or samples.