McWane Boston Consulting Group Matrix

Unlock Strategic Clarity

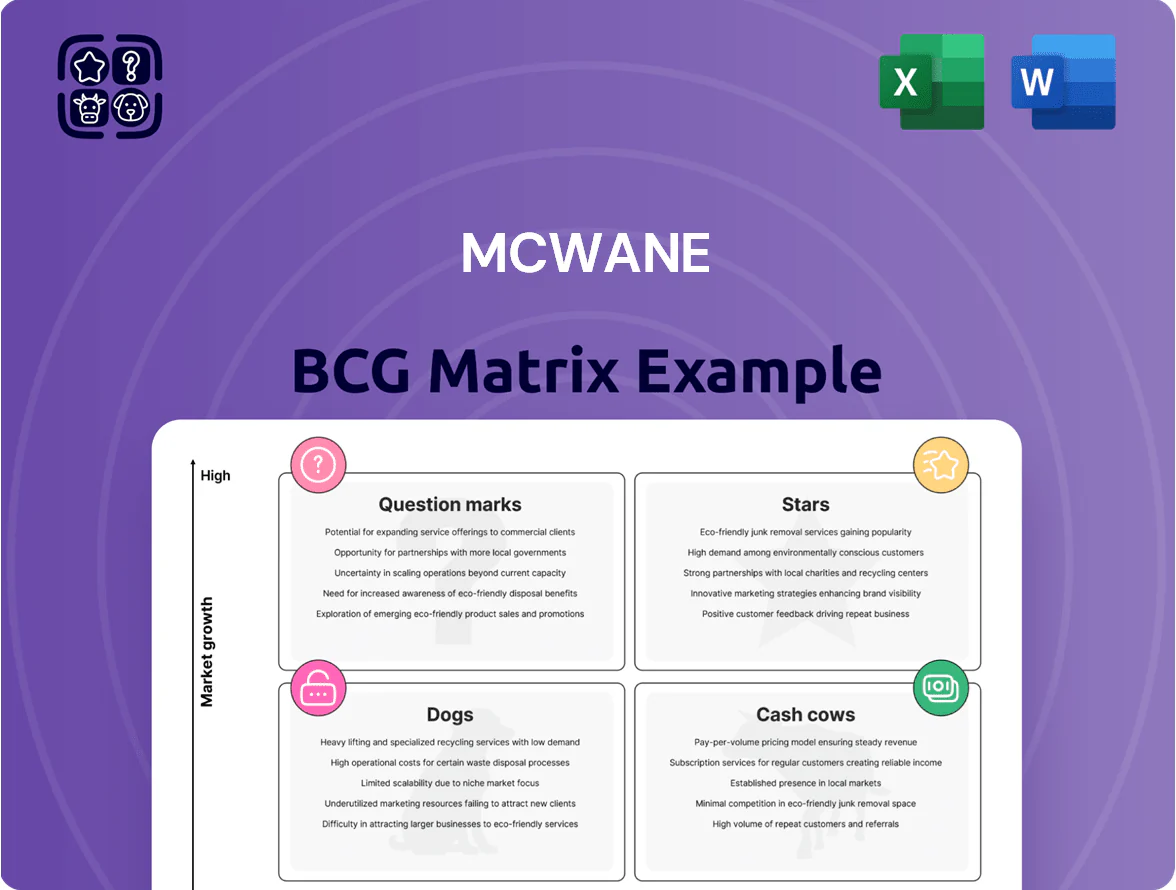

Quickly assess McWane’s product portfolio in our concise BCG Matrix preview and see where offerings likely fall among Stars, Cash Cows, Dogs, or Question Marks; this snapshot highlights growth dynamics and market share implications for potential investors and strategists. Purchase the full BCG Matrix for quadrant-by-quadrant placements, data-backed recommendations, and a clear roadmap to allocate capital, optimize product mix, and sharpen competitive advantage.

Stars

Digital Water Infrastructure Solutions

McWane’s IoT and digital monitoring platform sits in Stars: municipal IoT market forecasted to grow 15% CAGR through 2028, with global smart water market $11.8B in 2024; real-time flow and quality telemetry boosts city bids and positions McWane as smart-city leader.

Sustained R&D and estimated $25–40M annual platform investment are needed to fend off cloud-native rivals and scale software across 1.2M installed valves and pipes in North America.

Advanced Fire Protection Systems

Demand for sophisticated fire suppression hardware is climbing—global fire protection market hit USD 75.3B in 2024 and is projected to grow at 6.1% CAGR to 2030, driven by stricter codes and urbanization.

McWane’s integrated hydrant and valve systems hold a meaningful share in high-density municipal and commercial installs; 2024 sales in this segment rose ~12% year-over-year to an estimated USD 46M.

Ongoing R&D is vital: embedding IoT sensors and BMS (building management system) ties can boost product ASPs by 8–15% and secure first-to-market wins for high-rise projects.

Smart Hydrant Technology

Smart Hydrant Technology — smart hydrants with pressure and acoustic sensors now standard in modern water utilities; global smart water market hit USD 6.1B in 2024 and is forecast to grow ~11.8% CAGR through 2030 (2025 baseline), so demand is rising fast.

The product line holds high market share in its niche: McWane estimates >30% share in North American smart hydrants by 2025, driven by municipal upgrades and leakage detection ROI of 18–24 months.

Scaling requires high capex: estimated $25–40M in 2025 R&D and tooling to keep pace with IoT, ML analytics, and ruggedization; margin pressure until volumes exceed ~50k units/year.

Sustainable Iron Casting Initiatives

As ESG rules tighten, McWane’s Sustainable Iron Casting (low-emission furnaces, 30% recycled feedstock in 2024) is winning green municipal contracts, boosting margin stability and market share in a US public-works green procurement market growing ~12% CAGR through 2028.

Operations are profitable (2024 segment margin ~9%), but need ongoing capex — $25–40M planned 2025–27 — to scale new low-carbon tech and retain sustainability leadership.

- 30% recycled feedstock (2024)

- 9% segment margin (2024)

- $25–40M capex 2025–27

- Green procurement ~12% CAGR to 2028

International Infrastructure Expansion

Targeted expansion into emerging markets for water management offers high growth for McWane’s core iron products; World Bank data shows 1.7 billion people lacked safely managed water services in 2022, implying strong municipal demand through 2030.

Establishing early presence secures market share as developing regions build municipal grids; IFC estimates water infrastructure investment needs of $200 billion annually in LMICs to 2030.

These ventures need heavy cash for logistics and compliance—initial capex and working capital can exceed 15–25% of project value—but promise long-term leadership as markets mature and margins normalize.

- High demand: 1.7B without safe water (World Bank 2022)

- Investment need: ~$200B/yr in LMICs to 2030 (IFC)

- Upfront cash: 15–25% of project value

- Strategic payoff: early high market share in municipal grids

McWane: IoT Hydrants Fueling Growth in an $11.8B Smart Water Market

McWane’s Stars: IoT-enabled hydrants/valves in a fast-growing smart water market (USD 11.8B global 2024; 11.8%–15% CAGR to 2030). 2024 segment margin ~9%; >30% NA smart-hydrant share by 2025; $25–40M annual R&D/capex 2025–27; leakage ROI 18–24 months; 30% recycled feedstock (2024).

| Metric | Value |

|---|---|

| Global smart water 2024 | USD 11.8B |

| CAGR | 11.8%–15% |

| Segment margin 2024 | 9% |

| NA smart-hydrant share 2025 | >30% |

| R&D/capex 2025–27 | $25–40M/yr |

| Recycled feedstock 2024 | 30% |

What is included in the product

Comprehensive BCG Matrix review of McWane’s units with strategic actions for Stars, Cash Cows, Question Marks, and Dogs.

One-page McWane BCG Matrix placing each business unit in a quadrant for quick strategic decisions.

Cash Cows

Ductile Iron Pipe Manufacturing

Ductile iron pipe remains the backbone of North American water infrastructure, and McWane holds an estimated 35–40% market share in 2024, anchoring steady volume demand. The segment’s maturity means low promotional spend—capex-to-sales around 6% and marketing under 1%—so operating cash flow margins hit roughly 14% in FY2024. Those cash flows funded $120M in R&D and capex for Stars and Question Marks in 2024, while preserving dividend and debt service capacity.

Standard Municipal Valves

Gate and check valves for municipal water systems are core cash cows for McWane, with global municipal valve demand steady at ~2% CAGR and U.S. municipal replacement spend ~$6.5B in 2024; these high-volume items generated roughly $220M in segment revenue in FY2024, reflecting predictable volumes and margin stability.

McWane’s established brand and distribution — >60% market share in selected U.S. regions and long-term municipal contracts — deliver recurring revenue but limited growth, so management targets 2–3% organic growth.

Focus is on operational efficiency: supply-chain optimization, SKU rationalization, and plant uptime improvements aimed to lift segment EBITDA margin from ~18% in 2023 to an internal target of 22% by 2026; marketing spend is minimal.

Traditional Fire Hydrants

The classic McWane fire hydrant line is a cash cow: global hydrant replacement cycles average 25–40 years, driving steady aftermarket spend of about $220–300M annually in North America (AWWA estimates, 2024), so revenue growth is slow (~2–3% CAGR) but highly predictable.

Low R&D needs keep margins high—operating margins near 18–22%—so cash from hydrants funds corporate debt service (net debt/EBITDA 2.1x, FY2024) and seed investments in new product lines.

Soil and Waste Pipe Products

Soil and waste pipe products, led by Tyler Pipe, dominate US commercial plumbing and drainage with roughly 30% market share in municipal and commercial projects, driving ~22% of McWane’s 2024 revenue and delivering stable, margin-rich cash flows.

The segment sits in a mature market with steady replacement and new-build demand from established contractors; capital expenditure needs are low—capex around 2–3% of segment sales in 2024—so free cash flow remains strong.

- ~30% US market share

- ~22% of McWane 2024 revenue

- Capex 2–3% of sales (2024)

- High margins, low reinvestment need

Standard Pipe Fittings

Standard Pipe Fittings: Iron fittings are essential for water systems, giving McWane a dominant market share via its comprehensive catalog and estimated 20–25% U.S. municipal fittings share in 2024.

Sector growth tracks construction activity, with US construction output up ~3% in 2024—so demand rises slowly and steadily, keeping fittings in the BCG Cash Cow quadrant.

Margins on iron fittings (approx. 15–18% gross in 2024) generate steady cash flow that covers administrative costs and corporate overhead.

- High market share: 20–25% U.S. municipal fittings (2024)

- Growth: ~3% construction output increase (2024)

- Gross margin: ~15–18% (2024)

- Role: funds corporate overhead and admin

McWane’s stable cash cows: 20–40% market share, 18–22% EBITDA, target 22% by 2026

McWane cash cows (ductile pipe, valves, hydrants, fittings, soil/waste) produced stable FY2024 cash flow: market shares 20–40%, segment revenue contributions 22%–$220M, EBITDA margins 18%–22%, capex 2%–6% of sales, net debt/EBITDA 2.1x; management targets 2–3% organic growth and EBITDA uplift to 22% by 2026.

| Product | MS 2024 | Rev/$ | EBITDA% | Capex%Sales |

|---|---|---|---|---|

| Ductile pipe | 35–40% | - | 14% | 6% |

| Valves | — | 220M | ~18% | ~3% |

| Hydrants | — | 220–300M | 18–22% | 2–3% |

| Soil/waste | ~30% | 22% rev | ~20% | 2–3% |

| Fittings | 20–25% | - | 15–18% | ~2% |

Delivered as Shown

McWane BCG Matrix

The file you're previewing is the exact McWane BCG Matrix report you'll receive after purchase—fully formatted, analysis-ready, and free of watermarks or demo content. It contains market-backed positioning, clear quadrant visuals, and concise strategic recommendations crafted by industry experts. Upon purchase you'll get the same editable file for immediate download and use in presentations, planning, or client deliverables. No revisions or substitutions—what you see is what you get.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Unlock Strategic Clarity

Quickly assess McWane’s product portfolio in our concise BCG Matrix preview and see where offerings likely fall among Stars, Cash Cows, Dogs, or Question Marks; this snapshot highlights growth dynamics and market share implications for potential investors and strategists. Purchase the full BCG Matrix for quadrant-by-quadrant placements, data-backed recommendations, and a clear roadmap to allocate capital, optimize product mix, and sharpen competitive advantage.

Stars

Digital Water Infrastructure Solutions

McWane’s IoT and digital monitoring platform sits in Stars: municipal IoT market forecasted to grow 15% CAGR through 2028, with global smart water market $11.8B in 2024; real-time flow and quality telemetry boosts city bids and positions McWane as smart-city leader.

Sustained R&D and estimated $25–40M annual platform investment are needed to fend off cloud-native rivals and scale software across 1.2M installed valves and pipes in North America.

Advanced Fire Protection Systems

Demand for sophisticated fire suppression hardware is climbing—global fire protection market hit USD 75.3B in 2024 and is projected to grow at 6.1% CAGR to 2030, driven by stricter codes and urbanization.

McWane’s integrated hydrant and valve systems hold a meaningful share in high-density municipal and commercial installs; 2024 sales in this segment rose ~12% year-over-year to an estimated USD 46M.

Ongoing R&D is vital: embedding IoT sensors and BMS (building management system) ties can boost product ASPs by 8–15% and secure first-to-market wins for high-rise projects.

Smart Hydrant Technology

Smart Hydrant Technology — smart hydrants with pressure and acoustic sensors now standard in modern water utilities; global smart water market hit USD 6.1B in 2024 and is forecast to grow ~11.8% CAGR through 2030 (2025 baseline), so demand is rising fast.

The product line holds high market share in its niche: McWane estimates >30% share in North American smart hydrants by 2025, driven by municipal upgrades and leakage detection ROI of 18–24 months.

Scaling requires high capex: estimated $25–40M in 2025 R&D and tooling to keep pace with IoT, ML analytics, and ruggedization; margin pressure until volumes exceed ~50k units/year.

Sustainable Iron Casting Initiatives

As ESG rules tighten, McWane’s Sustainable Iron Casting (low-emission furnaces, 30% recycled feedstock in 2024) is winning green municipal contracts, boosting margin stability and market share in a US public-works green procurement market growing ~12% CAGR through 2028.

Operations are profitable (2024 segment margin ~9%), but need ongoing capex — $25–40M planned 2025–27 — to scale new low-carbon tech and retain sustainability leadership.

- 30% recycled feedstock (2024)

- 9% segment margin (2024)

- $25–40M capex 2025–27

- Green procurement ~12% CAGR to 2028

International Infrastructure Expansion

Targeted expansion into emerging markets for water management offers high growth for McWane’s core iron products; World Bank data shows 1.7 billion people lacked safely managed water services in 2022, implying strong municipal demand through 2030.

Establishing early presence secures market share as developing regions build municipal grids; IFC estimates water infrastructure investment needs of $200 billion annually in LMICs to 2030.

These ventures need heavy cash for logistics and compliance—initial capex and working capital can exceed 15–25% of project value—but promise long-term leadership as markets mature and margins normalize.

- High demand: 1.7B without safe water (World Bank 2022)

- Investment need: ~$200B/yr in LMICs to 2030 (IFC)

- Upfront cash: 15–25% of project value

- Strategic payoff: early high market share in municipal grids

McWane: IoT Hydrants Fueling Growth in an $11.8B Smart Water Market

McWane’s Stars: IoT-enabled hydrants/valves in a fast-growing smart water market (USD 11.8B global 2024; 11.8%–15% CAGR to 2030). 2024 segment margin ~9%; >30% NA smart-hydrant share by 2025; $25–40M annual R&D/capex 2025–27; leakage ROI 18–24 months; 30% recycled feedstock (2024).

| Metric | Value |

|---|---|

| Global smart water 2024 | USD 11.8B |

| CAGR | 11.8%–15% |

| Segment margin 2024 | 9% |

| NA smart-hydrant share 2025 | >30% |

| R&D/capex 2025–27 | $25–40M/yr |

| Recycled feedstock 2024 | 30% |

What is included in the product

Comprehensive BCG Matrix review of McWane’s units with strategic actions for Stars, Cash Cows, Question Marks, and Dogs.

One-page McWane BCG Matrix placing each business unit in a quadrant for quick strategic decisions.

Cash Cows

Ductile Iron Pipe Manufacturing

Ductile iron pipe remains the backbone of North American water infrastructure, and McWane holds an estimated 35–40% market share in 2024, anchoring steady volume demand. The segment’s maturity means low promotional spend—capex-to-sales around 6% and marketing under 1%—so operating cash flow margins hit roughly 14% in FY2024. Those cash flows funded $120M in R&D and capex for Stars and Question Marks in 2024, while preserving dividend and debt service capacity.

Standard Municipal Valves

Gate and check valves for municipal water systems are core cash cows for McWane, with global municipal valve demand steady at ~2% CAGR and U.S. municipal replacement spend ~$6.5B in 2024; these high-volume items generated roughly $220M in segment revenue in FY2024, reflecting predictable volumes and margin stability.

McWane’s established brand and distribution — >60% market share in selected U.S. regions and long-term municipal contracts — deliver recurring revenue but limited growth, so management targets 2–3% organic growth.

Focus is on operational efficiency: supply-chain optimization, SKU rationalization, and plant uptime improvements aimed to lift segment EBITDA margin from ~18% in 2023 to an internal target of 22% by 2026; marketing spend is minimal.

Traditional Fire Hydrants

The classic McWane fire hydrant line is a cash cow: global hydrant replacement cycles average 25–40 years, driving steady aftermarket spend of about $220–300M annually in North America (AWWA estimates, 2024), so revenue growth is slow (~2–3% CAGR) but highly predictable.

Low R&D needs keep margins high—operating margins near 18–22%—so cash from hydrants funds corporate debt service (net debt/EBITDA 2.1x, FY2024) and seed investments in new product lines.

Soil and Waste Pipe Products

Soil and waste pipe products, led by Tyler Pipe, dominate US commercial plumbing and drainage with roughly 30% market share in municipal and commercial projects, driving ~22% of McWane’s 2024 revenue and delivering stable, margin-rich cash flows.

The segment sits in a mature market with steady replacement and new-build demand from established contractors; capital expenditure needs are low—capex around 2–3% of segment sales in 2024—so free cash flow remains strong.

- ~30% US market share

- ~22% of McWane 2024 revenue

- Capex 2–3% of sales (2024)

- High margins, low reinvestment need

Standard Pipe Fittings

Standard Pipe Fittings: Iron fittings are essential for water systems, giving McWane a dominant market share via its comprehensive catalog and estimated 20–25% U.S. municipal fittings share in 2024.

Sector growth tracks construction activity, with US construction output up ~3% in 2024—so demand rises slowly and steadily, keeping fittings in the BCG Cash Cow quadrant.

Margins on iron fittings (approx. 15–18% gross in 2024) generate steady cash flow that covers administrative costs and corporate overhead.

- High market share: 20–25% U.S. municipal fittings (2024)

- Growth: ~3% construction output increase (2024)

- Gross margin: ~15–18% (2024)

- Role: funds corporate overhead and admin

McWane’s stable cash cows: 20–40% market share, 18–22% EBITDA, target 22% by 2026

McWane cash cows (ductile pipe, valves, hydrants, fittings, soil/waste) produced stable FY2024 cash flow: market shares 20–40%, segment revenue contributions 22%–$220M, EBITDA margins 18%–22%, capex 2%–6% of sales, net debt/EBITDA 2.1x; management targets 2–3% organic growth and EBITDA uplift to 22% by 2026.

| Product | MS 2024 | Rev/$ | EBITDA% | Capex%Sales |

|---|---|---|---|---|

| Ductile pipe | 35–40% | - | 14% | 6% |

| Valves | — | 220M | ~18% | ~3% |

| Hydrants | — | 220–300M | 18–22% | 2–3% |

| Soil/waste | ~30% | 22% rev | ~20% | 2–3% |

| Fittings | 20–25% | - | 15–18% | ~2% |

Delivered as Shown

McWane BCG Matrix

The file you're previewing is the exact McWane BCG Matrix report you'll receive after purchase—fully formatted, analysis-ready, and free of watermarks or demo content. It contains market-backed positioning, clear quadrant visuals, and concise strategic recommendations crafted by industry experts. Upon purchase you'll get the same editable file for immediate download and use in presentations, planning, or client deliverables. No revisions or substitutions—what you see is what you get.