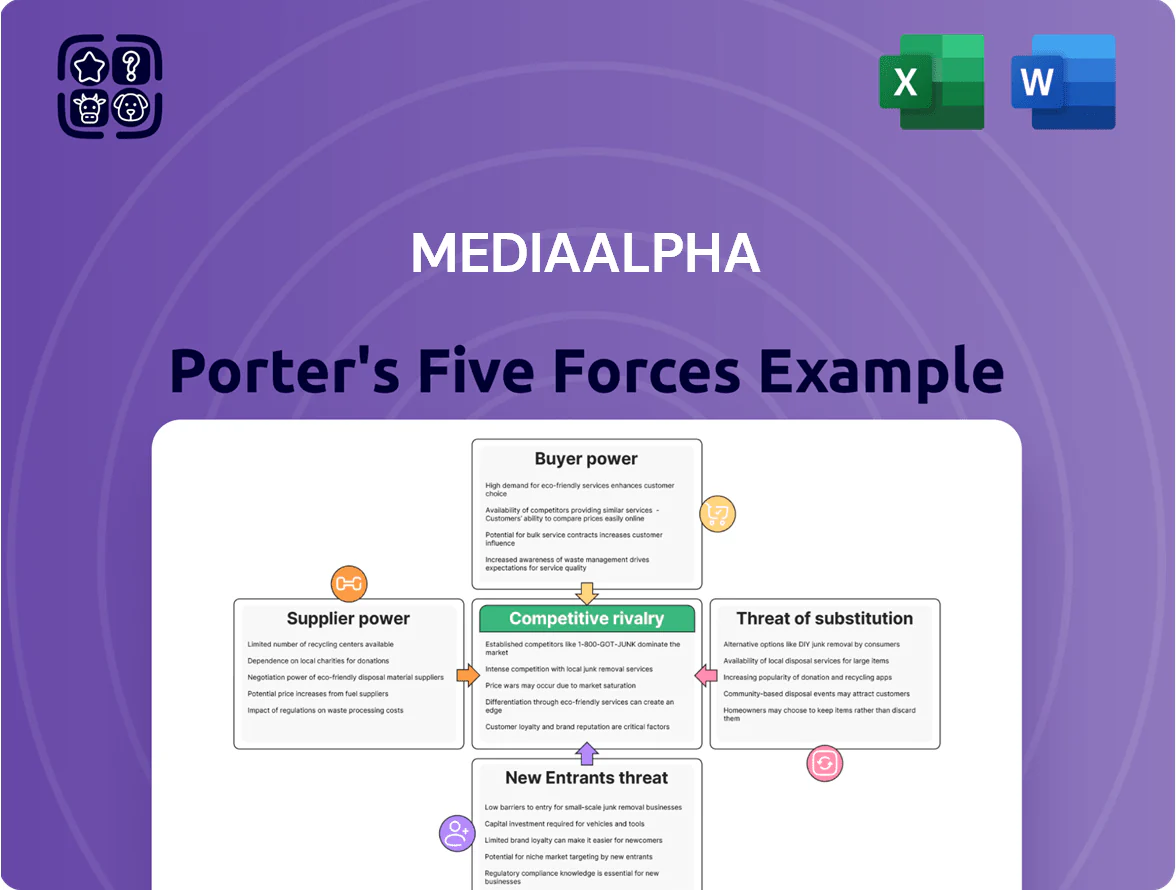

MediaAlpha Porter's Five Forces Analysis

Don't Miss the Bigger Picture

MediaAlpha faces intense buyer scrutiny and technological disruption, with supplier leverage moderate and substitutes rising as ad tech converges; new entrants face scale barriers but niche specialists can chip away at margins. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore MediaAlpha’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Dependency on Major Search Engines and Platforms

Major suppliers of consumer traffic for MediaAlpha are Google and Meta; together they accounted for an estimated 60–70% of digital ad impressions in 2024, giving them leverage over auction prices and targeting via algorithm and privacy changes. Their control raises acquisition costs—Google’s search ad CPC rose ~12% YoY in 2024—so MediaAlpha must continually update bidding algorithms and identity solutions to protect EBITDA margins.

Publisher Network Fragmentation

MediaAlpha benefits from publisher network fragmentation: it aggregates traffic from thousands of third-party sites, so individual small publishers hold little bargaining power versus the exchange; this helped gross margin resilience—MediaAlpha reported 2024 gross profit margin ~39% (Q4 2024).

Still, keeping quality across a diverse supplier base forces heavy investment in fraud detection and performance monitoring; MediaAlpha invested ~ $45m in tech and R&D in 2024 to limit spoofing and low-quality traffic.

Rising Costs of High-Intent Traffic

As digital insurance matures, competition for high-intent quote seekers raised CPA (cost per acquisition) by ~25% from 2020–2024, letting suppliers charge more for premium traffic, notably during Q4 and ACA open enrollment peaks.

Suppliers gain bargaining power because scarce, ready-to-buy users drive pricing; data providers can demand premiums and prefer long-term deals or higher rev-shares.

MediaAlpha cuts exposure by using real-time matching and supply-side optimization; in 2024 their bid optimization reportedly improved conversion yield by ~18%, lowering effective spend per converted lead.

Impact of Data Privacy Regulations

Suppliers of consumer data face tighter limits from laws like California Consumer Privacy Act (CCPA) and recent federal guidance, reducing third-party tracking and cutting available intent signals by an estimated 20–35% in ad markets during 2023–2024.

That shrinks actionable data supply and raises supplier bargaining power on price and terms; MediaAlpha needs stronger first-party ingestion and identity resolution to maintain CPMs and fill rates.

- Data supply fell ~20–35% (2023–24 ad market estimates)

- CCPA and federal guidelines restrict cross-site tracking

- First-party data & identity tools reduce supplier dependence

- Goal: protect CPMs and fill rates by shifting to owned signals

Technological Integration Requirements

Suppliers demand robust API integrations for real-time bidding, raising a technical barrier that favors established exchanges; 2024 IAB data shows 72% of programmatic spend flows through platforms with low-latency APIs.

This barrier lets top publishers favor exchanges with best support and fill rates; leading exchanges report median fill rates of 65–85% on premium inventory.

MediaAlpha’s 2024 capex and R&D spend of ~$48M keeps its infra competitive, helping retain high-volume suppliers.

- APIs: 72% programmatic spend via low-latency platforms

- Fill rates: top exchanges 65–85%

- MediaAlpha 2024 R&D/capex ≈ $48M

Google & Meta dominate ads; MediaAlpha boosts first‑party data, lifts bid yield +18%

Major suppliers (Google, Meta) held ~60–70% of ad impressions in 2024, raising CPCs (~+12% YoY) and supplier leverage; fragmented publishers reduce individual power (MediaAlpha 2024 gross margin ~39%) but force heavy fraud/detection spend (~$45–48M). Data limits (CCPA + federal guidance) cut third‑party signals ~20–35% (2023–24), increasing supplier bargaining and pushing MediaAlpha to grow first‑party identity and realtime matching (bid yield +18% in 2024).

| Metric | 2023–24 |

|---|---|

| Google+Meta impression share | 60–70% |

| Search ad CPC change | +12% YoY (2024) |

| Gross profit margin | ~39% (2024) |

| R&D/capex & fraud spend | ~$45–48M (2024) |

| Third‑party signal decline | 20–35% |

| Bid optimization lift | +18% (2024) |

What is included in the product

Tailored Porter's Five Forces analysis for MediaAlpha, uncovering key competitive drivers, buyer and supplier power, entry barriers, substitutes, and emerging disruptors affecting pricing, profitability, and market positioning.

A concise Porter's Five Forces one-sheet for MediaAlpha that highlights competitive pressures and relieves decision fatigue—easy to drop into decks or adapt for scenario analysis.

Customers Bargaining Power

Concentration of Large Insurance Carriers

A significant share of MediaAlpha's 2024 revenue—about 40% per company filings—comes from a handful of large carriers such as Progressive and Allstate, giving these buyers strong bargaining power to demand lower prices and strict lead-quality transparency; this concentration means a single carrier cutting digital marketing spend or reallocating budget could drop exchange liquidity sharply, as seen when Progressive reduced spend in Q3 2023 leading to a double-digit revenue swing for peers.

Low Switching Costs for Advertisers

Insurance carriers and distributors can shift ad spend quickly across exchanges or direct channels, driven by cost-per-acquisition (CPA) targets—industry data shows digital insurers reallocate up to 25% of media budgets quarterly when CPA rises. Buyers show low platform loyalty and chase the highest ROI, pressuring MediaAlpha on price. MediaAlpha reduces churn by offering advanced analytics and campaign-management tools that improve match rates and lower CPAs; clients using its platform reported up to 18% better conversion rates in 2024. This tech-driven stickiness raises effective switching costs despite low headline barriers.

Real-Time Bidding Transparency

The marketplace’s real-time bidding transparency lets buyers see exact prices and lead performance live, so in 2025 62% of MediaAlpha buyers report using real-time metrics to adjust bids within minutes, raising buyer selectivity.

Buyers bid only on consumers matching precise risk and underwriting slices, reducing broad purchases by 38% year-over-year and forcing tighter inventory targeting.

MediaAlpha must supply a steady stream of diverse, high-quality traffic—its Q4 2024 revenue mix showed 48% from top-tier carriers—so platform liquidity and yield quality remain critical.

Shift Toward Direct-to-Consumer Models

As carriers build in-house digital teams and spend—US insurance digital ad spend rose to an estimated $12.3B in 2024—many can bypass exchanges like MediaAlpha, reducing the platform’s leverage.

If carriers lower cost-per-acquisition by 10–30% via owned funnels, MediaAlpha must demonstrate equal or better CPA or higher-intent leads to retain volume.

Here’s the quick math: 10% CPA savings on a $400 LTV policy = $40 per policy; multiply by 100k policies = $4M saved.

- Carrier digital spend: $12.3B (2024)

- Needed: MediaAlpha CPA ≤ carrier CPA

- Win: higher lead intent or 10%+ cost edge

Demand for Performance-Based Pricing

Customers are shifting from click-based fees to performance pricing, demanding payment only for qualified leads or conversions; in programmatic media this trend rose 18% year-over-year in 2024 per IAB data, pressing MediaAlpha to prove consumer intent and accuracy.

Buyers leverage scale to require granular user-level data and advanced attribution; advertisers report 27% higher ROI when using multi-touch attribution, so MediaAlpha faces pricing pressure and must improve verification to retain contracts.

- Shift: 18% rise in performance pricing (2024 IAB)

- ROI lift: 27% with multi-touch attribution

- Need: stronger intent verification, better attribution

MediaAlpha faces carrier-driven CPA pressure—must beat 10–30% in‑house savings to keep volume

Major carriers (≈40% revenue in 2024) give MediaAlpha strong buyer power, pushing for lower CPAs and lead transparency; carrier digital spend hit $12.3B (2024) and 62% use real-time bidding (2025), increasing selectivity. Performance pricing rose 18% (2024 IAB); MediaAlpha must match or beat 10–30% CPA savings from in‑house channels to retain volume.

| Metric | Value |

|---|---|

| Carrier share | ≈40% |

| US insurer ad spend | $12.3B (2024) |

| Real-time bidders | 62% (2025) |

| Performance pricing rise | 18% (2024) |

What You See Is What You Get

MediaAlpha Porter's Five Forces Analysis

This preview shows the exact MediaAlpha Porter’s Five Forces analysis you’ll receive after purchase—no placeholders or samples—fully formatted and ready for immediate download and use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

MediaAlpha faces intense buyer scrutiny and technological disruption, with supplier leverage moderate and substitutes rising as ad tech converges; new entrants face scale barriers but niche specialists can chip away at margins. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore MediaAlpha’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Dependency on Major Search Engines and Platforms

Major suppliers of consumer traffic for MediaAlpha are Google and Meta; together they accounted for an estimated 60–70% of digital ad impressions in 2024, giving them leverage over auction prices and targeting via algorithm and privacy changes. Their control raises acquisition costs—Google’s search ad CPC rose ~12% YoY in 2024—so MediaAlpha must continually update bidding algorithms and identity solutions to protect EBITDA margins.

Publisher Network Fragmentation

MediaAlpha benefits from publisher network fragmentation: it aggregates traffic from thousands of third-party sites, so individual small publishers hold little bargaining power versus the exchange; this helped gross margin resilience—MediaAlpha reported 2024 gross profit margin ~39% (Q4 2024).

Still, keeping quality across a diverse supplier base forces heavy investment in fraud detection and performance monitoring; MediaAlpha invested ~ $45m in tech and R&D in 2024 to limit spoofing and low-quality traffic.

Rising Costs of High-Intent Traffic

As digital insurance matures, competition for high-intent quote seekers raised CPA (cost per acquisition) by ~25% from 2020–2024, letting suppliers charge more for premium traffic, notably during Q4 and ACA open enrollment peaks.

Suppliers gain bargaining power because scarce, ready-to-buy users drive pricing; data providers can demand premiums and prefer long-term deals or higher rev-shares.

MediaAlpha cuts exposure by using real-time matching and supply-side optimization; in 2024 their bid optimization reportedly improved conversion yield by ~18%, lowering effective spend per converted lead.

Impact of Data Privacy Regulations

Suppliers of consumer data face tighter limits from laws like California Consumer Privacy Act (CCPA) and recent federal guidance, reducing third-party tracking and cutting available intent signals by an estimated 20–35% in ad markets during 2023–2024.

That shrinks actionable data supply and raises supplier bargaining power on price and terms; MediaAlpha needs stronger first-party ingestion and identity resolution to maintain CPMs and fill rates.

- Data supply fell ~20–35% (2023–24 ad market estimates)

- CCPA and federal guidelines restrict cross-site tracking

- First-party data & identity tools reduce supplier dependence

- Goal: protect CPMs and fill rates by shifting to owned signals

Technological Integration Requirements

Suppliers demand robust API integrations for real-time bidding, raising a technical barrier that favors established exchanges; 2024 IAB data shows 72% of programmatic spend flows through platforms with low-latency APIs.

This barrier lets top publishers favor exchanges with best support and fill rates; leading exchanges report median fill rates of 65–85% on premium inventory.

MediaAlpha’s 2024 capex and R&D spend of ~$48M keeps its infra competitive, helping retain high-volume suppliers.

- APIs: 72% programmatic spend via low-latency platforms

- Fill rates: top exchanges 65–85%

- MediaAlpha 2024 R&D/capex ≈ $48M

Google & Meta dominate ads; MediaAlpha boosts first‑party data, lifts bid yield +18%

Major suppliers (Google, Meta) held ~60–70% of ad impressions in 2024, raising CPCs (~+12% YoY) and supplier leverage; fragmented publishers reduce individual power (MediaAlpha 2024 gross margin ~39%) but force heavy fraud/detection spend (~$45–48M). Data limits (CCPA + federal guidance) cut third‑party signals ~20–35% (2023–24), increasing supplier bargaining and pushing MediaAlpha to grow first‑party identity and realtime matching (bid yield +18% in 2024).

| Metric | 2023–24 |

|---|---|

| Google+Meta impression share | 60–70% |

| Search ad CPC change | +12% YoY (2024) |

| Gross profit margin | ~39% (2024) |

| R&D/capex & fraud spend | ~$45–48M (2024) |

| Third‑party signal decline | 20–35% |

| Bid optimization lift | +18% (2024) |

What is included in the product

Tailored Porter's Five Forces analysis for MediaAlpha, uncovering key competitive drivers, buyer and supplier power, entry barriers, substitutes, and emerging disruptors affecting pricing, profitability, and market positioning.

A concise Porter's Five Forces one-sheet for MediaAlpha that highlights competitive pressures and relieves decision fatigue—easy to drop into decks or adapt for scenario analysis.

Customers Bargaining Power

Concentration of Large Insurance Carriers

A significant share of MediaAlpha's 2024 revenue—about 40% per company filings—comes from a handful of large carriers such as Progressive and Allstate, giving these buyers strong bargaining power to demand lower prices and strict lead-quality transparency; this concentration means a single carrier cutting digital marketing spend or reallocating budget could drop exchange liquidity sharply, as seen when Progressive reduced spend in Q3 2023 leading to a double-digit revenue swing for peers.

Low Switching Costs for Advertisers

Insurance carriers and distributors can shift ad spend quickly across exchanges or direct channels, driven by cost-per-acquisition (CPA) targets—industry data shows digital insurers reallocate up to 25% of media budgets quarterly when CPA rises. Buyers show low platform loyalty and chase the highest ROI, pressuring MediaAlpha on price. MediaAlpha reduces churn by offering advanced analytics and campaign-management tools that improve match rates and lower CPAs; clients using its platform reported up to 18% better conversion rates in 2024. This tech-driven stickiness raises effective switching costs despite low headline barriers.

Real-Time Bidding Transparency

The marketplace’s real-time bidding transparency lets buyers see exact prices and lead performance live, so in 2025 62% of MediaAlpha buyers report using real-time metrics to adjust bids within minutes, raising buyer selectivity.

Buyers bid only on consumers matching precise risk and underwriting slices, reducing broad purchases by 38% year-over-year and forcing tighter inventory targeting.

MediaAlpha must supply a steady stream of diverse, high-quality traffic—its Q4 2024 revenue mix showed 48% from top-tier carriers—so platform liquidity and yield quality remain critical.

Shift Toward Direct-to-Consumer Models

As carriers build in-house digital teams and spend—US insurance digital ad spend rose to an estimated $12.3B in 2024—many can bypass exchanges like MediaAlpha, reducing the platform’s leverage.

If carriers lower cost-per-acquisition by 10–30% via owned funnels, MediaAlpha must demonstrate equal or better CPA or higher-intent leads to retain volume.

Here’s the quick math: 10% CPA savings on a $400 LTV policy = $40 per policy; multiply by 100k policies = $4M saved.

- Carrier digital spend: $12.3B (2024)

- Needed: MediaAlpha CPA ≤ carrier CPA

- Win: higher lead intent or 10%+ cost edge

Demand for Performance-Based Pricing

Customers are shifting from click-based fees to performance pricing, demanding payment only for qualified leads or conversions; in programmatic media this trend rose 18% year-over-year in 2024 per IAB data, pressing MediaAlpha to prove consumer intent and accuracy.

Buyers leverage scale to require granular user-level data and advanced attribution; advertisers report 27% higher ROI when using multi-touch attribution, so MediaAlpha faces pricing pressure and must improve verification to retain contracts.

- Shift: 18% rise in performance pricing (2024 IAB)

- ROI lift: 27% with multi-touch attribution

- Need: stronger intent verification, better attribution

MediaAlpha faces carrier-driven CPA pressure—must beat 10–30% in‑house savings to keep volume

Major carriers (≈40% revenue in 2024) give MediaAlpha strong buyer power, pushing for lower CPAs and lead transparency; carrier digital spend hit $12.3B (2024) and 62% use real-time bidding (2025), increasing selectivity. Performance pricing rose 18% (2024 IAB); MediaAlpha must match or beat 10–30% CPA savings from in‑house channels to retain volume.

| Metric | Value |

|---|---|

| Carrier share | ≈40% |

| US insurer ad spend | $12.3B (2024) |

| Real-time bidders | 62% (2025) |

| Performance pricing rise | 18% (2024) |

What You See Is What You Get

MediaAlpha Porter's Five Forces Analysis

This preview shows the exact MediaAlpha Porter’s Five Forces analysis you’ll receive after purchase—no placeholders or samples—fully formatted and ready for immediate download and use.