MediaTek Porter's Five Forces Analysis

Don't Miss the Bigger Picture

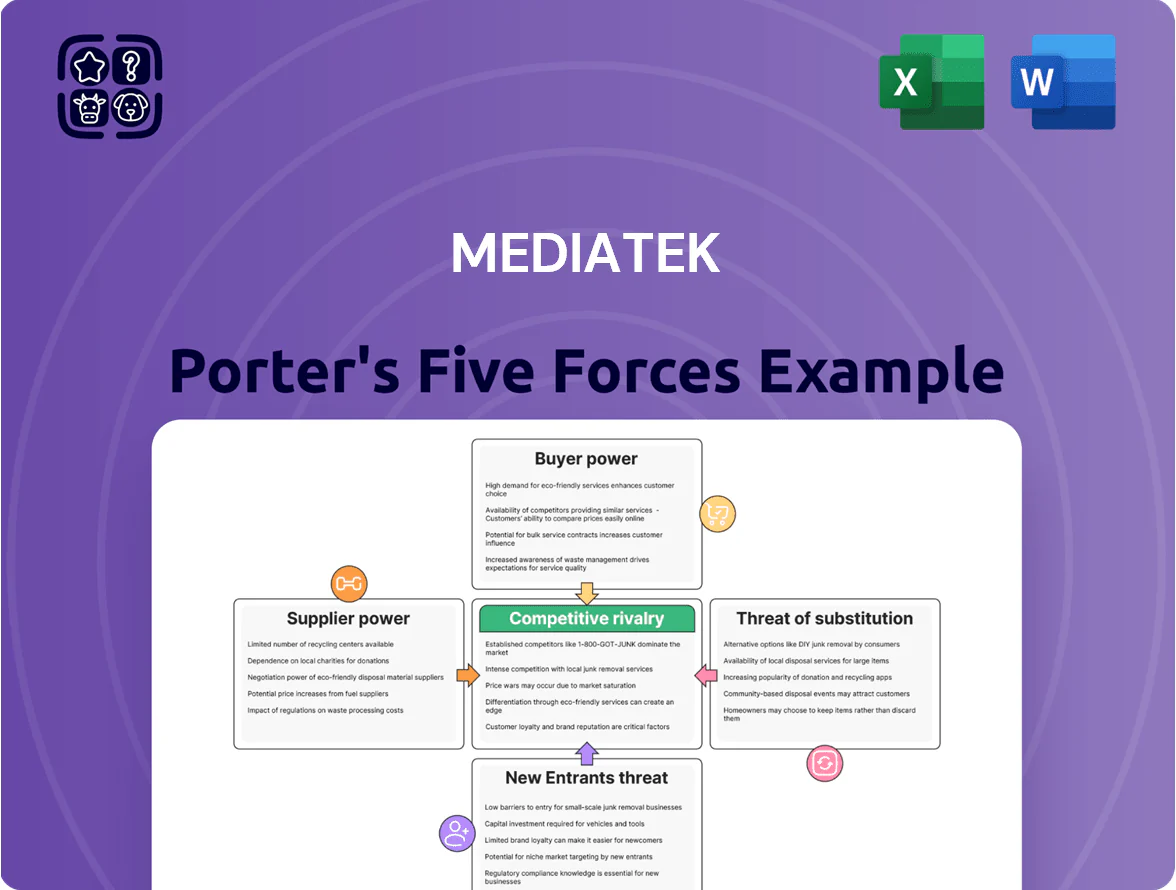

MediaTek faces intense rivalry from Qualcomm and Apple, strong supplier leverage for advanced process nodes, and moderate buyer power driven by OEM consolidation, while barriers to entry remain high but innovation and platform shifts (5G, AI) raise substitute risks; strategic positioning hinges on cost leadership, IP partnerships, and ecosystem scale. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore MediaTek’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Heavy reliance on advanced foundry capacity

MediaTek is fabless and depends on third-party foundries, chiefly TSMC, for advanced nodes; in 2025 TSMC held ~55% global advanced-node capacity and was the primary supplier for 3nm/2nm wafers.

Rising 2nm/3nm demand by late 2025 pushed utilization above 95% at leading foundries, giving them pricing power and priority allocation over fabless clients.

This concentration limited MediaTek’s negotiating leverage: wafer ASPs for 3nm rose an estimated 15–25% YoY in 2025, squeezing gross margins when capacity tightened.

Dominance of ARM architecture licensing

MediaTek depends heavily on ARM Holdings IP for CPUs/GPUs, with over 80% of its mobile SoCs in 2024 using ARM cores, so ARM wields pricing power and design control.

ARM’s 2023–25 shift toward per‑unit royalties and new Neoverse offerings raised MediaTek’s licensing cost risk, potentially squeezing gross margins by several percentage points per product line.

Few commercial alternatives exist in mobile; this limited substitution keeps ARM’s bargaining power high and forces MediaTek into close tech and fee negotiations.

Scarcity of specialized semiconductor materials

The production of high-performance SoCs needs scarce raw materials and chemicals held by few global suppliers; in 2024, about 70% of advanced substrates came from three firms, concentrating bargaining power. Geopolitical tensions in 2023–2025 intermittently disrupted rare earth and substrate shipments, raising spot prices by ~25% in 2024 and pushing upstream input costs higher. This price volatility lets material suppliers demand premiums, which can cut MediaTek’s gross margin—MediaTek reported a 2024 gross margin of 40.1%—if it cannot pass costs to OEM customers.

Influence of EDA tool providers

Electronic Design Automation (EDA) vendors like Synopsys and Cadence supply mission-critical tools that are tightly embedded in MediaTek’s R&D, creating high switching costs and concentrated supplier power.

In 2024 Synopsys reported $4.9B revenue and Cadence $3.9B, so price hikes or license shifts would directly raise MediaTek’s fixed R&D expenses and compress margins.

Strategic importance of back-end packaging partners

MediaTek relies on Outsourced Semiconductor Assembly and Test (OSAT) firms beyond wafer fabs; in 2024 OSAT revenue hit about $49B globally, underscoring scale.

As designs shift to 3D packaging and chiplets, OSAT technical know-how becomes critical, raising switching costs and time-to-market risks for MediaTek.

That technical edge boosts OSAT bargaining power—expect higher premiums and longer contract lead times versus legacy packaging.

- OSAT market ~$49B (2024)

- 3D/chiplet complexity increases test cycles ~20–40% (industry estimates)

- Higher switching costs, longer contracts, price premiums

Supplier squeeze: TSMC, ARM, substrate & EDA dominance ramps MediaTek costs

MediaTek faces high supplier power: TSMC (~55% advanced-node share in 2025) and ARM (used in >80% mobile SoCs) dominate key inputs, 3nm wafer ASPs rose ~15–25% YoY in 2025, substrates concentrated (~70% from three firms) and OSAT/EDA firms (OSAT market ~$49B in 2024; Synopsys $4.9B, Cadence $3.9B) add switching costs and margin pressure.

| Supplier | Metric | 2024–25 |

|---|---|---|

| TSMC | Advanced-node share | ~55% |

| 3nm wafers | ASP change | +15–25% YoY |

| ARM | SoC use | >80% |

| OSAT | Market | $49B (2024) |

| EDA | Top vendors rev | Synopsys $4.9B; Cadence $3.9B |

| Substrates | Concentration | ~70% from 3 firms |

What is included in the product

Tailored exclusively for MediaTek, this Porter's Five Forces analysis uncovers key competitive drivers, assesses supplier and buyer power, examines entry barriers and substitutes, and highlights disruptive threats shaping its pricing, profitability, and strategic positioning.

A concise Porter's Five Forces summary for MediaTek—visualizes competitive intensity and supplier/buyer power to speed strategic decisions and investor briefings.

Customers Bargaining Power

Concentration of major smartphone OEMs

A significant portion of MediaTek’s 2024 smartphone revenue—about 42% of its $12.7B chipset sales—came from a few OEMs including Xiaomi, Oppo, and Vivo, giving these high-volume customers strong leverage to push down unit prices. Their collective smartphone shipments exceeded 350 million units in 2024, so a single OEM shifting flagship orders to Qualcomm or Samsung could cut MediaTek’s revenue by several hundred million dollars in a year.

High price sensitivity in the mid-range segment

MediaTek leads price-sensitive mid-range and entry-level SoC markets, where 2024 ASPs fell ~8% while volumes rose 12%, squeezing gross margins to ~28% in FY2024. Buyers in emerging markets switch quickly for small price-to-performance gains, so MediaTek keeps aggressive pricing to protect share—its low-to-mid portfolio drove ~60% of handset chip shipments in 2024. This pricing pressure limits margin expansion and forces continuous cost and feature trade-offs.

Vertical integration by top-tier tech giants

Vertical integration by Apple, Samsung and Google—Apple moved ~80% of its 2023 iPhone SoC volume to in-house A-series/Bionic chips and Samsung and Google expanded Exynos and Tensor lines—shrinks merchant SoC TAM, cutting MediaTek’s premium opportunity; MediaTek’s FY2024 smartphone SoC ASP gap vs premium peers widened, forcing deeper competition for fewer external contracts.

Low switching costs for standardized components

Low switching costs for standardized components: in IoT and consumer electronics, reworking PCB designs to fit rival SoCs is common, so OEMs can switch if MediaTek raises prices; this caps MediaTek’s pricing power outside high-end mobile. In 2024, MediaTek held ~34% global smartphone SoC share but faced fierce price sensitivity in IoT where competitors like Unisoc and Broadcom push margins down.

- Easy PCB redesign enables substitution

- IoT device makers prioritize cost over brand

- 2024: MediaTek ~34% smartphone SoC share

- Competition from Unisoc, Broadcom, Qualcomm limits pricing

Demand for customized and co-developed solutions

As of 2025, top customers demand customized silicon for AI and advanced imaging, pushing MediaTek to increase client-specific engineering spending—estimated at a 12–18% rise in R&D per large account in 2024–25.

That deeper support gives customers greater sway over MediaTek’s development roadmap and lets them negotiate specific technical and pricing terms, raising bargaining power.

These bespoke partnerships create lock-in—repeat design wins and royalties—but also concentrate revenue risk: top 5 customers made ~48% of MediaTek’s FY2024 revenue.

- 12–18% R&D uplift per large account (2024–25)

- Top 5 customers ≈48% of FY2024 revenue

- Higher pricing/tech concessions in co-development deals

- Lock-in via IP/custom blocks vs. concentrated revenue risk

MediaTek: OEM concentration boosts leverage as ASPs fall, margins slip to ~28%

Large OEMs (Xiaomi/Oppo/Vivo) drove ~42% of MediaTek’s $12.7B FY2024 chipset sales; top 5 customers ≈48% revenue, giving strong price leverage. Mid/entry SoC ASPs fell ~8% in 2024 while volumes rose 12%, dragging gross margin to ~28%. Low switching costs in IoT and OEM demand for custom AI silicon (12–18% R&D uplift per large account) further raise customer bargaining power.

| Metric | 2024 |

|---|---|

| Chipset sales | $12.7B |

| Share from few OEMs | ~42% |

| Top 5 revenue | ~48% |

| ASP change | −8% |

| Volume change | +12% |

| Gross margin | ~28% |

| R&D uplift | 12–18% |

Preview the Actual Deliverable

MediaTek Porter's Five Forces Analysis

This preview shows the exact MediaTek Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders or samples. The file is the professionally written, fully formatted deliverable ready for download and use the moment you complete payment. You’re looking at the final document, with comprehensive force-by-force evaluation, strategic implications, and actionable insights included. No surprises—what you see is what you get.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

MediaTek faces intense rivalry from Qualcomm and Apple, strong supplier leverage for advanced process nodes, and moderate buyer power driven by OEM consolidation, while barriers to entry remain high but innovation and platform shifts (5G, AI) raise substitute risks; strategic positioning hinges on cost leadership, IP partnerships, and ecosystem scale. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore MediaTek’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Heavy reliance on advanced foundry capacity

MediaTek is fabless and depends on third-party foundries, chiefly TSMC, for advanced nodes; in 2025 TSMC held ~55% global advanced-node capacity and was the primary supplier for 3nm/2nm wafers.

Rising 2nm/3nm demand by late 2025 pushed utilization above 95% at leading foundries, giving them pricing power and priority allocation over fabless clients.

This concentration limited MediaTek’s negotiating leverage: wafer ASPs for 3nm rose an estimated 15–25% YoY in 2025, squeezing gross margins when capacity tightened.

Dominance of ARM architecture licensing

MediaTek depends heavily on ARM Holdings IP for CPUs/GPUs, with over 80% of its mobile SoCs in 2024 using ARM cores, so ARM wields pricing power and design control.

ARM’s 2023–25 shift toward per‑unit royalties and new Neoverse offerings raised MediaTek’s licensing cost risk, potentially squeezing gross margins by several percentage points per product line.

Few commercial alternatives exist in mobile; this limited substitution keeps ARM’s bargaining power high and forces MediaTek into close tech and fee negotiations.

Scarcity of specialized semiconductor materials

The production of high-performance SoCs needs scarce raw materials and chemicals held by few global suppliers; in 2024, about 70% of advanced substrates came from three firms, concentrating bargaining power. Geopolitical tensions in 2023–2025 intermittently disrupted rare earth and substrate shipments, raising spot prices by ~25% in 2024 and pushing upstream input costs higher. This price volatility lets material suppliers demand premiums, which can cut MediaTek’s gross margin—MediaTek reported a 2024 gross margin of 40.1%—if it cannot pass costs to OEM customers.

Influence of EDA tool providers

Electronic Design Automation (EDA) vendors like Synopsys and Cadence supply mission-critical tools that are tightly embedded in MediaTek’s R&D, creating high switching costs and concentrated supplier power.

In 2024 Synopsys reported $4.9B revenue and Cadence $3.9B, so price hikes or license shifts would directly raise MediaTek’s fixed R&D expenses and compress margins.

Strategic importance of back-end packaging partners

MediaTek relies on Outsourced Semiconductor Assembly and Test (OSAT) firms beyond wafer fabs; in 2024 OSAT revenue hit about $49B globally, underscoring scale.

As designs shift to 3D packaging and chiplets, OSAT technical know-how becomes critical, raising switching costs and time-to-market risks for MediaTek.

That technical edge boosts OSAT bargaining power—expect higher premiums and longer contract lead times versus legacy packaging.

- OSAT market ~$49B (2024)

- 3D/chiplet complexity increases test cycles ~20–40% (industry estimates)

- Higher switching costs, longer contracts, price premiums

Supplier squeeze: TSMC, ARM, substrate & EDA dominance ramps MediaTek costs

MediaTek faces high supplier power: TSMC (~55% advanced-node share in 2025) and ARM (used in >80% mobile SoCs) dominate key inputs, 3nm wafer ASPs rose ~15–25% YoY in 2025, substrates concentrated (~70% from three firms) and OSAT/EDA firms (OSAT market ~$49B in 2024; Synopsys $4.9B, Cadence $3.9B) add switching costs and margin pressure.

| Supplier | Metric | 2024–25 |

|---|---|---|

| TSMC | Advanced-node share | ~55% |

| 3nm wafers | ASP change | +15–25% YoY |

| ARM | SoC use | >80% |

| OSAT | Market | $49B (2024) |

| EDA | Top vendors rev | Synopsys $4.9B; Cadence $3.9B |

| Substrates | Concentration | ~70% from 3 firms |

What is included in the product

Tailored exclusively for MediaTek, this Porter's Five Forces analysis uncovers key competitive drivers, assesses supplier and buyer power, examines entry barriers and substitutes, and highlights disruptive threats shaping its pricing, profitability, and strategic positioning.

A concise Porter's Five Forces summary for MediaTek—visualizes competitive intensity and supplier/buyer power to speed strategic decisions and investor briefings.

Customers Bargaining Power

Concentration of major smartphone OEMs

A significant portion of MediaTek’s 2024 smartphone revenue—about 42% of its $12.7B chipset sales—came from a few OEMs including Xiaomi, Oppo, and Vivo, giving these high-volume customers strong leverage to push down unit prices. Their collective smartphone shipments exceeded 350 million units in 2024, so a single OEM shifting flagship orders to Qualcomm or Samsung could cut MediaTek’s revenue by several hundred million dollars in a year.

High price sensitivity in the mid-range segment

MediaTek leads price-sensitive mid-range and entry-level SoC markets, where 2024 ASPs fell ~8% while volumes rose 12%, squeezing gross margins to ~28% in FY2024. Buyers in emerging markets switch quickly for small price-to-performance gains, so MediaTek keeps aggressive pricing to protect share—its low-to-mid portfolio drove ~60% of handset chip shipments in 2024. This pricing pressure limits margin expansion and forces continuous cost and feature trade-offs.

Vertical integration by top-tier tech giants

Vertical integration by Apple, Samsung and Google—Apple moved ~80% of its 2023 iPhone SoC volume to in-house A-series/Bionic chips and Samsung and Google expanded Exynos and Tensor lines—shrinks merchant SoC TAM, cutting MediaTek’s premium opportunity; MediaTek’s FY2024 smartphone SoC ASP gap vs premium peers widened, forcing deeper competition for fewer external contracts.

Low switching costs for standardized components

Low switching costs for standardized components: in IoT and consumer electronics, reworking PCB designs to fit rival SoCs is common, so OEMs can switch if MediaTek raises prices; this caps MediaTek’s pricing power outside high-end mobile. In 2024, MediaTek held ~34% global smartphone SoC share but faced fierce price sensitivity in IoT where competitors like Unisoc and Broadcom push margins down.

- Easy PCB redesign enables substitution

- IoT device makers prioritize cost over brand

- 2024: MediaTek ~34% smartphone SoC share

- Competition from Unisoc, Broadcom, Qualcomm limits pricing

Demand for customized and co-developed solutions

As of 2025, top customers demand customized silicon for AI and advanced imaging, pushing MediaTek to increase client-specific engineering spending—estimated at a 12–18% rise in R&D per large account in 2024–25.

That deeper support gives customers greater sway over MediaTek’s development roadmap and lets them negotiate specific technical and pricing terms, raising bargaining power.

These bespoke partnerships create lock-in—repeat design wins and royalties—but also concentrate revenue risk: top 5 customers made ~48% of MediaTek’s FY2024 revenue.

- 12–18% R&D uplift per large account (2024–25)

- Top 5 customers ≈48% of FY2024 revenue

- Higher pricing/tech concessions in co-development deals

- Lock-in via IP/custom blocks vs. concentrated revenue risk

MediaTek: OEM concentration boosts leverage as ASPs fall, margins slip to ~28%

Large OEMs (Xiaomi/Oppo/Vivo) drove ~42% of MediaTek’s $12.7B FY2024 chipset sales; top 5 customers ≈48% revenue, giving strong price leverage. Mid/entry SoC ASPs fell ~8% in 2024 while volumes rose 12%, dragging gross margin to ~28%. Low switching costs in IoT and OEM demand for custom AI silicon (12–18% R&D uplift per large account) further raise customer bargaining power.

| Metric | 2024 |

|---|---|

| Chipset sales | $12.7B |

| Share from few OEMs | ~42% |

| Top 5 revenue | ~48% |

| ASP change | −8% |

| Volume change | +12% |

| Gross margin | ~28% |

| R&D uplift | 12–18% |

Preview the Actual Deliverable

MediaTek Porter's Five Forces Analysis

This preview shows the exact MediaTek Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders or samples. The file is the professionally written, fully formatted deliverable ready for download and use the moment you complete payment. You’re looking at the final document, with comprehensive force-by-force evaluation, strategic implications, and actionable insights included. No surprises—what you see is what you get.