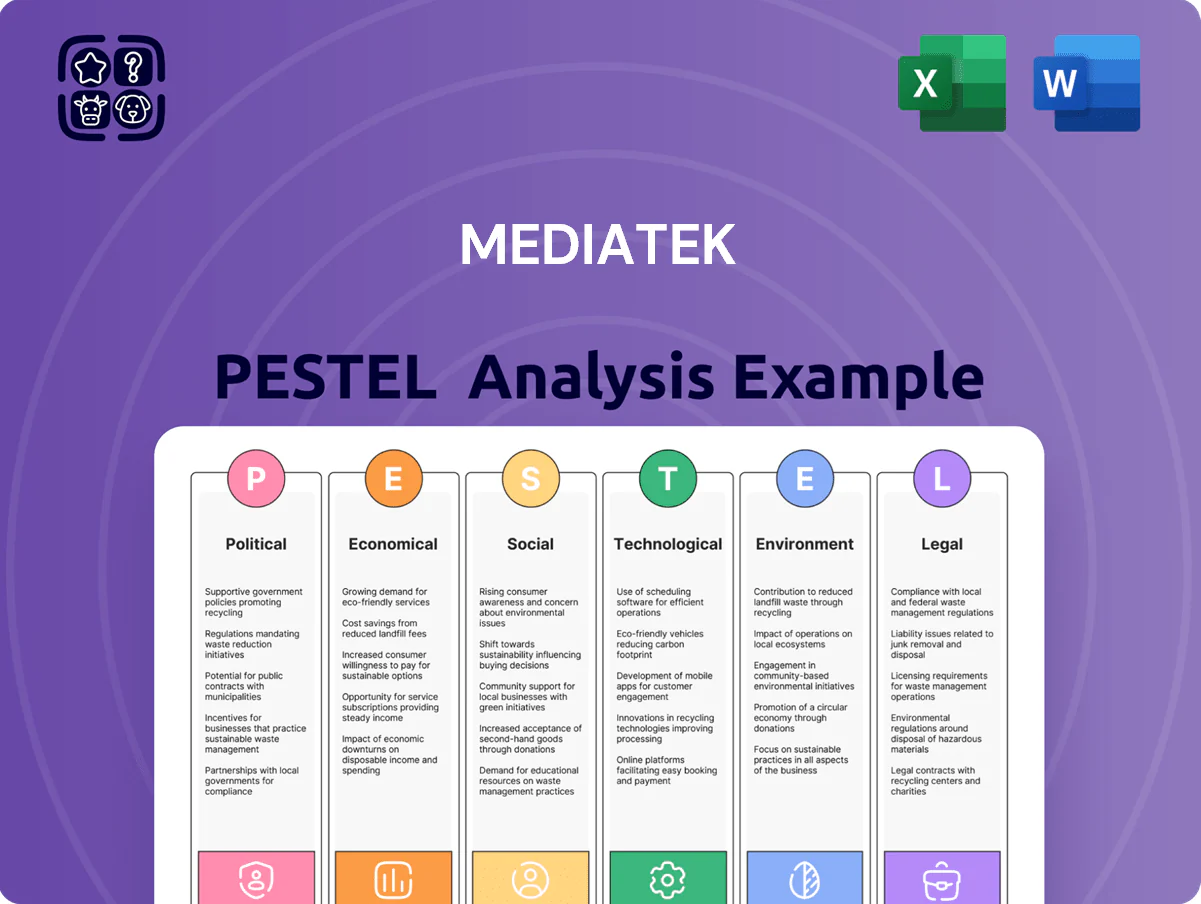

MediaTek PESTLE Analysis

Skip the Research. Get the Strategy.

Discover how geopolitical shifts, supply-chain dynamics, and rapid tech innovation are reshaping MediaTek’s prospects—our concise PESTLE highlights key risks and opportunities to inform smarter strategy and investment calls; purchase the full analysis for a complete, downloadable breakdown with actionable insights.

Political factors

US-China Trade Relations

The US-China trade tensions materially affect MediaTek, with Taiwan-based chipmaker exposed to export controls that curbed certain high-end chip transfers; in 2024 MediaTek reported 2023 revenue of US$15.6B, with about 40% from smartphone SoCs tied to Chinese OEMs, making compliance crucial to avoid supplier disruptions.

Taiwan Strait Geopolitical Stability

The political stability of the Taiwan Strait is critical for MediaTek, headquartered in Hsinchu, as 60%+ of global advanced chip assembly and testing capacity sits in Taiwan and nearby Asia-Pacific nodes; any escalation could halt production lines tied to TSMC (MediaTek’s main foundry partner) which handled ~65% of MediaTek wafer volume in 2024. Investors monitor diplomatic moves for supply-chain interruption risk and potential revenue impact on MediaTek’s 2024 revenue of US$17.1B.

Government Semiconductor Subsidies

Governments are scaling industrial policies—US CHIPS Act alone authorized about $280 billion including $52B for domestic fabs—boosting demand for foundry partners and advanced IP, which benefits MediaTek through larger global fabs demand. Taiwan provided R&D tax credits and subsidies; MediaTek reported R&D spend of NT$70.3bn (2024) supporting its leadership in 5G/AI chips. Rising protectionism in EU/US and export controls on advanced nodes may hinder MediaTek’s market access and supply-chain collaboration.

Global Export Control Compliance

Global export controls on dual-use tech force MediaTek to invest in legal and compliance systems; in 2024 the company reported R&D of NT$58.6bn (≈US$1.8bn), underscoring dependence on sensitive chip IP and tools.

MediaTek must ensure its AI and connectivity chips meet evolving security rules from the US, EU and Japan to avoid penalties and supply restrictions that could disrupt production.

Non-compliance risks include fines, export bans or loss of access to semiconductor equipment—recent export-control actions since 2022 have affected firms' revenue and supply chains.

- 2024 R&D: NT$58.6bn (~US$1.8bn)

- Exposure to US/EU/Japan controls on advanced node tools

- Penalties or equipment access loss can materially impact production and revenue

Regional Trade Agreements

MediaTek's competitiveness is influenced by Taiwan's participation in trade pacts: preferential tariffs in CPTPP-lead talks and ASEAN EFTA arrangements could lower component costs by up to 5-8%, improving gross margins versus non-preferential rivals.

Favorable terms in Southeast Asia and EU markets supported MediaTek's 2024 international revenue growth of ~12%, and shifts in alliances through 2025 expect to alter semiconductor tariff lines affecting supply-chain costs.

- Preferential tariffs can cut component costs 5-8%

- 2024 international revenue growth ~12%

- Trade shifts through 2025 reshape semiconductor tariff landscape

MediaTek faces China export controls, Taiwan risks—$17.1B revenue, 65% TSMC wafers

US-China export controls and Taiwan Strait risks directly threaten MediaTek’s supply chain and revenue—2024 revenue reported US$17.1B with ~40% from Chinese OEM smartphone SoCs; ~65% wafer volume via TSMC; R&D NT$58.6–70.3bn supports compliance and tech resilience.

| Metric | 2024 |

|---|---|

| Revenue | US$17.1B |

| Smartphone SoC share from China | ~40% |

| Wafer volume via TSMC | ~65% |

| R&D | NT$58.6–70.3bn |

What is included in the product

Explores how macro-environmental factors uniquely affect MediaTek across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify threats and opportunities.

A concise, PESTLE-segmented MediaTek summary that’s easily dropped into presentations or shared across teams to streamline discussions on regulatory, economic, technological, social, and environmental risks and opportunities.

Economic factors

Global Consumer Spending Power

MediaTek's revenue fell 4% YoY to NT$482.5B in 2024 H1 as weaker global consumer spending and rising inflation reduced device purchases, showing direct sensitivity to disposable income changes.

Global inflation averaging 5.8% in 2024 and central bank hikes pushed smartphone upgrade cycles longer, lowering chipset ASPs and unit growth in 2024 by ~3–5% versus 2023.

As a leader in mid-range and budget segments, MediaTek is exposed in emerging markets—APAC smartphone shipments slid ~6% YoY in 2024—amplifying revenue volatility tied to regional economic shifts.

Currency Exchange Rate Volatility

Reporting in New Taiwan Dollars while earning significant revenue in US Dollars and Renminbi exposes MediaTek to notable forex risk; a 10% TWD appreciation versus USD in 2024 would have reduced reported USD-linked revenue materially, given ~45% of 2024 revenue was dollar-denominated. Sharp swings also affect costs for components and foundry services priced in USD and RMB, with 2024 chip procurement showing price sensitivity to FX changes. MediaTek uses layered hedging—forwards, options, and natural hedges—to limit volatility, noting hedges covered roughly 30–50% of forecasted FX exposure in recent quarters.

Rising Research and Development Costs

The shift to 3nm/2nm nodes demands R&D and design capital exceeding $1–2 billion per node generation; MediaTek faces pressure to fund this while preserving 2024 net margin of ~12.5% and target returns for shareholders.

Specialized engineering salaries and EDA/licensing costs rose ~15–25% in 2024–2025, adding material operating expense inflation that could compress MediaTek’s margins if not offset by higher ASPs or volume gains.

Emerging Market Growth Trends

- ~1.2B new smartphone users by 2025 in EMs

- India 5G ~30% connections by 2026

- Southeast Asia 5G adoption 25–35% by 2026–27

- High-volume demand for affordable 5G SoCs fuels MediaTek's long-term volume strategy

Semiconductor Industry Cyclicality

The semiconductor sector shows recurrent cycles of oversupply and inventory corrections that compress ASPs; global chip industry revenue dropped 8.5% in 2023 then rebounded ~12% in 2024 as inventories normalized.

MediaTek must tightly manage inventory turns—ending 2024 days inventory was ~78 days for major fabless peers—to avoid margin erosion during demand shocks.

By end-2025 the market shifted toward supply-demand stabilization with foundry utilization rising to ~85% and price pressure easing.

- 2023 revenue decline ~8.5%

- 2024 rebound ~12%

- Fabless peers DI ~78 days

- Foundry utilization ~85% by end-2025

Macro drag trims H1 revenue; FX, rising R&D squeeze margins as EM 5G offers upside

Economic headwinds—4% H1 2024 revenue decline to NT$482.5B, 2024 inflation ~5.8%, APAC smartphone shipments -6% YoY—compressed ASPs and margins (~12.5% net margin in 2024). FX exposure (≈45% USD revenue; hedges cover 30–50%) and rising R&D (~$1–2B/node) plus 15–25% higher engineering costs pressure margins; EM 5G adoption (India ~30% by 2026) supports volume upside.

| Metric | Value |

|---|---|

| 2024 H1 rev | NT$482.5B |

| 2024 inflation | 5.8% |

| Net margin 2024 | ~12.5% |

| FX USD rev | ~45% |

Same Document Delivered

MediaTek PESTLE Analysis

The preview shown here is the exact MediaTek PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. It contains the same content, structure, and professional layout visible in the preview with no placeholders or teasers. After checkout you’ll instantly download this final, ready-to-use file. What you see is what you’ll own.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Skip the Research. Get the Strategy.

Discover how geopolitical shifts, supply-chain dynamics, and rapid tech innovation are reshaping MediaTek’s prospects—our concise PESTLE highlights key risks and opportunities to inform smarter strategy and investment calls; purchase the full analysis for a complete, downloadable breakdown with actionable insights.

Political factors

US-China Trade Relations

The US-China trade tensions materially affect MediaTek, with Taiwan-based chipmaker exposed to export controls that curbed certain high-end chip transfers; in 2024 MediaTek reported 2023 revenue of US$15.6B, with about 40% from smartphone SoCs tied to Chinese OEMs, making compliance crucial to avoid supplier disruptions.

Taiwan Strait Geopolitical Stability

The political stability of the Taiwan Strait is critical for MediaTek, headquartered in Hsinchu, as 60%+ of global advanced chip assembly and testing capacity sits in Taiwan and nearby Asia-Pacific nodes; any escalation could halt production lines tied to TSMC (MediaTek’s main foundry partner) which handled ~65% of MediaTek wafer volume in 2024. Investors monitor diplomatic moves for supply-chain interruption risk and potential revenue impact on MediaTek’s 2024 revenue of US$17.1B.

Government Semiconductor Subsidies

Governments are scaling industrial policies—US CHIPS Act alone authorized about $280 billion including $52B for domestic fabs—boosting demand for foundry partners and advanced IP, which benefits MediaTek through larger global fabs demand. Taiwan provided R&D tax credits and subsidies; MediaTek reported R&D spend of NT$70.3bn (2024) supporting its leadership in 5G/AI chips. Rising protectionism in EU/US and export controls on advanced nodes may hinder MediaTek’s market access and supply-chain collaboration.

Global Export Control Compliance

Global export controls on dual-use tech force MediaTek to invest in legal and compliance systems; in 2024 the company reported R&D of NT$58.6bn (≈US$1.8bn), underscoring dependence on sensitive chip IP and tools.

MediaTek must ensure its AI and connectivity chips meet evolving security rules from the US, EU and Japan to avoid penalties and supply restrictions that could disrupt production.

Non-compliance risks include fines, export bans or loss of access to semiconductor equipment—recent export-control actions since 2022 have affected firms' revenue and supply chains.

- 2024 R&D: NT$58.6bn (~US$1.8bn)

- Exposure to US/EU/Japan controls on advanced node tools

- Penalties or equipment access loss can materially impact production and revenue

Regional Trade Agreements

MediaTek's competitiveness is influenced by Taiwan's participation in trade pacts: preferential tariffs in CPTPP-lead talks and ASEAN EFTA arrangements could lower component costs by up to 5-8%, improving gross margins versus non-preferential rivals.

Favorable terms in Southeast Asia and EU markets supported MediaTek's 2024 international revenue growth of ~12%, and shifts in alliances through 2025 expect to alter semiconductor tariff lines affecting supply-chain costs.

- Preferential tariffs can cut component costs 5-8%

- 2024 international revenue growth ~12%

- Trade shifts through 2025 reshape semiconductor tariff landscape

MediaTek faces China export controls, Taiwan risks—$17.1B revenue, 65% TSMC wafers

US-China export controls and Taiwan Strait risks directly threaten MediaTek’s supply chain and revenue—2024 revenue reported US$17.1B with ~40% from Chinese OEM smartphone SoCs; ~65% wafer volume via TSMC; R&D NT$58.6–70.3bn supports compliance and tech resilience.

| Metric | 2024 |

|---|---|

| Revenue | US$17.1B |

| Smartphone SoC share from China | ~40% |

| Wafer volume via TSMC | ~65% |

| R&D | NT$58.6–70.3bn |

What is included in the product

Explores how macro-environmental factors uniquely affect MediaTek across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify threats and opportunities.

A concise, PESTLE-segmented MediaTek summary that’s easily dropped into presentations or shared across teams to streamline discussions on regulatory, economic, technological, social, and environmental risks and opportunities.

Economic factors

Global Consumer Spending Power

MediaTek's revenue fell 4% YoY to NT$482.5B in 2024 H1 as weaker global consumer spending and rising inflation reduced device purchases, showing direct sensitivity to disposable income changes.

Global inflation averaging 5.8% in 2024 and central bank hikes pushed smartphone upgrade cycles longer, lowering chipset ASPs and unit growth in 2024 by ~3–5% versus 2023.

As a leader in mid-range and budget segments, MediaTek is exposed in emerging markets—APAC smartphone shipments slid ~6% YoY in 2024—amplifying revenue volatility tied to regional economic shifts.

Currency Exchange Rate Volatility

Reporting in New Taiwan Dollars while earning significant revenue in US Dollars and Renminbi exposes MediaTek to notable forex risk; a 10% TWD appreciation versus USD in 2024 would have reduced reported USD-linked revenue materially, given ~45% of 2024 revenue was dollar-denominated. Sharp swings also affect costs for components and foundry services priced in USD and RMB, with 2024 chip procurement showing price sensitivity to FX changes. MediaTek uses layered hedging—forwards, options, and natural hedges—to limit volatility, noting hedges covered roughly 30–50% of forecasted FX exposure in recent quarters.

Rising Research and Development Costs

The shift to 3nm/2nm nodes demands R&D and design capital exceeding $1–2 billion per node generation; MediaTek faces pressure to fund this while preserving 2024 net margin of ~12.5% and target returns for shareholders.

Specialized engineering salaries and EDA/licensing costs rose ~15–25% in 2024–2025, adding material operating expense inflation that could compress MediaTek’s margins if not offset by higher ASPs or volume gains.

Emerging Market Growth Trends

- ~1.2B new smartphone users by 2025 in EMs

- India 5G ~30% connections by 2026

- Southeast Asia 5G adoption 25–35% by 2026–27

- High-volume demand for affordable 5G SoCs fuels MediaTek's long-term volume strategy

Semiconductor Industry Cyclicality

The semiconductor sector shows recurrent cycles of oversupply and inventory corrections that compress ASPs; global chip industry revenue dropped 8.5% in 2023 then rebounded ~12% in 2024 as inventories normalized.

MediaTek must tightly manage inventory turns—ending 2024 days inventory was ~78 days for major fabless peers—to avoid margin erosion during demand shocks.

By end-2025 the market shifted toward supply-demand stabilization with foundry utilization rising to ~85% and price pressure easing.

- 2023 revenue decline ~8.5%

- 2024 rebound ~12%

- Fabless peers DI ~78 days

- Foundry utilization ~85% by end-2025

Macro drag trims H1 revenue; FX, rising R&D squeeze margins as EM 5G offers upside

Economic headwinds—4% H1 2024 revenue decline to NT$482.5B, 2024 inflation ~5.8%, APAC smartphone shipments -6% YoY—compressed ASPs and margins (~12.5% net margin in 2024). FX exposure (≈45% USD revenue; hedges cover 30–50%) and rising R&D (~$1–2B/node) plus 15–25% higher engineering costs pressure margins; EM 5G adoption (India ~30% by 2026) supports volume upside.

| Metric | Value |

|---|---|

| 2024 H1 rev | NT$482.5B |

| 2024 inflation | 5.8% |

| Net margin 2024 | ~12.5% |

| FX USD rev | ~45% |

Same Document Delivered

MediaTek PESTLE Analysis

The preview shown here is the exact MediaTek PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. It contains the same content, structure, and professional layout visible in the preview with no placeholders or teasers. After checkout you’ll instantly download this final, ready-to-use file. What you see is what you’ll own.