MPT Business Model Canvas

Ready-to-Use MPT Business Model Canvas: Strategic Blueprint for Investors & Founders

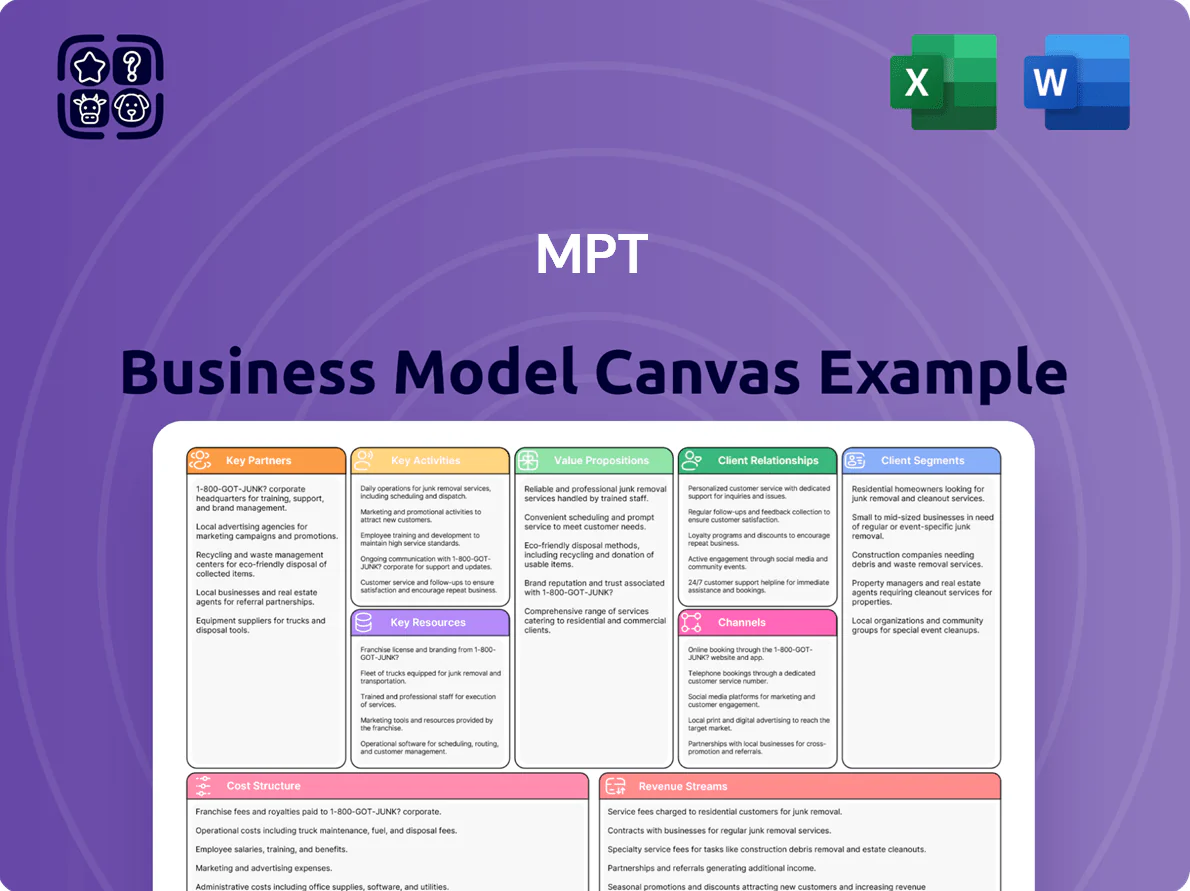

Unlock the full strategic blueprint behind MPT's business model — a concise, actionable Business Model Canvas that maps value propositions, customer segments, key partners, revenue streams, and cost structure. Ideal for investors, consultants, and founders seeking a ready-to-use analysis, the complete download (Word + Excel) lets you benchmark, adapt, and execute proven strategies with confidence.

Partnerships

Strategic Hospital Operators

Medical Properties Trust relies on major operators such as Lifepoint Health and Circle Health as primary tenants who run clinical operations and protect local reputations; these partnerships accounted for roughly 28% of MPT’s leased EBITDA through Q3 2025. By late 2025 MPT targets reducing single-tenant exposure via new deals and asset rotations, letting MPT focus on real estate while operators handle medical services.

Institutional Financial Lenders

Institutional financial lenders—commercial banks and investment firms—provide revolving credit facilities that preserve MPT’s access to global capital markets and liquidity for acquisitions and $85–120m annual capex in 2025.

In 2025 these partners emphasize covenant compliance and balance-sheet optimization; MPT coordinates refinancing of maturing debt (≈$300m due 2025–2026) and hedges to stabilize capital structure amid rising short-term rates.

Joint Venture Equity Partners

MPT formed joint ventures with sovereign wealth funds and private equity groups to co-invest in hospital portfolios, recycling capital by selling 20–40% stakes while keeping management control and earning 1.5–2.0% asset management fees; by H2 2025 this tactic unlocked ~USD 420m in proceeds and funded 60% of planned 2026 expansion without equity dilution.

Healthcare Real Estate Developers

Strategic collaborations with specialized healthcare real estate developers let MPT do build-to-suit projects, tapping firms with expertise in healthcare architecture and local zoning so facilities meet modern standards and open faster.

Partnering lets MPT acquire turnkey, state-of-the-art hospitals on completion, keeping the portfolio tech-relevant and attractive to premium medical tenants; US healthcare construction spending hit $95.6B in 2024.

- Build-to-suit reduces vacancy risk

- Access to zoning/clinical design expertise

- Acquire new assets on completion

- Supports higher rents from quality tenants

- 2024 US healthcare construction: $95.6B

Regulatory and Legal Consultants

MPT keeps continuous engagement with specialized legal and compliance advisors to manage healthcare and REIT rules across the US, UK, and Germany, ensuring lease structures meet evolving mandates and REIT tax rules.

In 2025 these consultants are critical for tenant restructurings and divestitures; for example, they helped navigate 12 cross‑border transactions in 2024, preserving REIT tax status and avoiding estimated €6.2m in potential tax liabilities.

- Ongoing advice across US/UK/DE

- Lease compliance and REIT tax upkeep

- Supported 12 cross‑border deals in 2024

- Estimated €6.2m tax liability mitigation

MPT partners unlock $420M, fund $85–120M capex & rotate assets to tackle $300M refinancing

MPT’s key partners—major hospital operators (28% leased EBITDA through Q3 2025), banks (credit lines for $85–120m capex in 2025), and JV investors (sold 20–40% stakes unlocking ~$420m H2 2025)—enable asset rotation, refinancing (≈$300m due 2025–26) and build-to-suit growth while advisors managed 12 cross‑border deals in 2024, saving ~€6.2m.

| Partner | Key metric | 2024–25 |

|---|---|---|

| Major operators | Leased EBITDA share | 28% |

| Financial lenders | Annual capex funding | $85–120m (2025) |

| JV investors | Proceeds unlocked | $420m (H2 2025) |

| Advisors | Deals supported | 12 (2024), €6.2m tax saved |

What is included in the product

A ready-to-use MPT Business Model Canvas detailing customer segments, value propositions, channels, revenue streams, key activities, resources, partnerships, cost structure, and metrics, with integrated SWOT and competitive advantage analysis to support presentations, funding discussions, and validation of strategies using real-world company data.

Compact one-page MPT Business Model Canvas that condenses strategy into editable cells—ideal for quick boardroom reviews, team collaboration, and saving hours of formatting while comparing or adapting multiple company models.

Activities

Strategic Real Estate Acquisition

MPT scouts and acquires essential hospital properties serving local communities, prioritizing sites with clear clinical demand and stable payer mix; by 2025 MPT targeted acute care and behavioral health, which made up ~65% of new purchases in 2024–25.

Each deal follows strict due diligence on utilization, EBITDA and demographics—typical covenants include 12–24 month revenue recourse and cap rates around 6.5%–7.5%—so assets retain value across operator changes.

Portfolio Diversification and Optimization

MPT actively manages its portfolio to balance geographic reach and facility types—like inpatient rehabilitation and mental-health centers—while tracking tenant concentration to keep any single provider below 20% of NOI. In 2025 the firm cut exposure in four struggling U.S. markets and added 14 stable international assets, selling $185M of underperforming properties to lift portfolio occupancy to 94.3%.

Underwriting and Operator Monitoring

A core activity is continuous financial monitoring of hospital tenants to ensure they meet long-term lease obligations; MPT tracks admission rates, EBITDAR coverage, and liquidity using proprietary data and industry benchmarks—showing, for example, a median EBITDAR coverage target of 1.5x and monitoring admission variance within ±8% versus 2019 baselines. This proactive surveillance identifies distress early so MPT can deploy strategic interventions to protect revenue stability and investor returns.

Capital Recycling and Debt Management

MPT sold $420m of noncore assets in 2025 to cut net debt by 18% and slash blended interest cost from 6.8% to 5.4%, improving its credit metrics and raising pro forma NAV per share by ~6%.

Efficient capital recycling via divestitures and JV deals keeps liquidity up, lowers WACC, and preserves agility in a high-rate market.

- 2025 asset sales $420m

- Net debt down 18%

- Blended interest 6.8%→5.4%

- Pro forma NAV +6%

- Focus: deleveraging, JVs, lower WACC

Lease Structuring and Negotiation

MPT structures long-term triple-net leases so tenants pay maintenance, taxes, and insurance, with annual rent escalations tied to CPI or fixed 2–3% steps to preserve cash flow.

Negotiations secure tenant financial reporting and transparency; by 2025 MPT reports 95% of new leases include reporting covenants and lease yields average 6.2% NOI.

- Triple-net: tenant pays OPEX

- Escalations: CPI or 2–3% annually

- 2025: 95% leases require reporting

- Average lease yield 6.2% NOI

MPT trims debt, boosts NAV 6% after $420M sales; occupancy 94.3%, yield 6.2%

MPT acquires and manages hospital properties, using strict due diligence (EBITDAR target 1.5x, admission variance ±8%) and portfolio limits (single provider <20% NOI); in 2025 it sold $420M, cut net debt 18%, cut blended interest 6.8%→5.4%, and raised pro forma NAV ~6%, keeping occupancy 94.3% and average lease yield 6.2%.

| Metric | 2025 |

|---|---|

| Asset sales | $420M |

| Net debt change | -18% |

| Blended interest | 6.8%→5.4% |

| Pro forma NAV | +6% |

| Occupancy | 94.3% |

| Avg lease yield | 6.2% NOI |

| EBITDAR target | 1.5x |

Full Document Unlocks After Purchase

Business Model Canvas

The document you're previewing is the actual MPT Business Model Canvas you'll receive—no mockups or samples—presented exactly as in the final file.

When you complete your purchase, you'll instantly get this same professional, ready-to-edit document in both Word and Excel formats, with all sections and content included.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Ready-to-Use MPT Business Model Canvas: Strategic Blueprint for Investors & Founders

Unlock the full strategic blueprint behind MPT's business model — a concise, actionable Business Model Canvas that maps value propositions, customer segments, key partners, revenue streams, and cost structure. Ideal for investors, consultants, and founders seeking a ready-to-use analysis, the complete download (Word + Excel) lets you benchmark, adapt, and execute proven strategies with confidence.

Partnerships

Strategic Hospital Operators

Medical Properties Trust relies on major operators such as Lifepoint Health and Circle Health as primary tenants who run clinical operations and protect local reputations; these partnerships accounted for roughly 28% of MPT’s leased EBITDA through Q3 2025. By late 2025 MPT targets reducing single-tenant exposure via new deals and asset rotations, letting MPT focus on real estate while operators handle medical services.

Institutional Financial Lenders

Institutional financial lenders—commercial banks and investment firms—provide revolving credit facilities that preserve MPT’s access to global capital markets and liquidity for acquisitions and $85–120m annual capex in 2025.

In 2025 these partners emphasize covenant compliance and balance-sheet optimization; MPT coordinates refinancing of maturing debt (≈$300m due 2025–2026) and hedges to stabilize capital structure amid rising short-term rates.

Joint Venture Equity Partners

MPT formed joint ventures with sovereign wealth funds and private equity groups to co-invest in hospital portfolios, recycling capital by selling 20–40% stakes while keeping management control and earning 1.5–2.0% asset management fees; by H2 2025 this tactic unlocked ~USD 420m in proceeds and funded 60% of planned 2026 expansion without equity dilution.

Healthcare Real Estate Developers

Strategic collaborations with specialized healthcare real estate developers let MPT do build-to-suit projects, tapping firms with expertise in healthcare architecture and local zoning so facilities meet modern standards and open faster.

Partnering lets MPT acquire turnkey, state-of-the-art hospitals on completion, keeping the portfolio tech-relevant and attractive to premium medical tenants; US healthcare construction spending hit $95.6B in 2024.

- Build-to-suit reduces vacancy risk

- Access to zoning/clinical design expertise

- Acquire new assets on completion

- Supports higher rents from quality tenants

- 2024 US healthcare construction: $95.6B

Regulatory and Legal Consultants

MPT keeps continuous engagement with specialized legal and compliance advisors to manage healthcare and REIT rules across the US, UK, and Germany, ensuring lease structures meet evolving mandates and REIT tax rules.

In 2025 these consultants are critical for tenant restructurings and divestitures; for example, they helped navigate 12 cross‑border transactions in 2024, preserving REIT tax status and avoiding estimated €6.2m in potential tax liabilities.

- Ongoing advice across US/UK/DE

- Lease compliance and REIT tax upkeep

- Supported 12 cross‑border deals in 2024

- Estimated €6.2m tax liability mitigation

MPT partners unlock $420M, fund $85–120M capex & rotate assets to tackle $300M refinancing

MPT’s key partners—major hospital operators (28% leased EBITDA through Q3 2025), banks (credit lines for $85–120m capex in 2025), and JV investors (sold 20–40% stakes unlocking ~$420m H2 2025)—enable asset rotation, refinancing (≈$300m due 2025–26) and build-to-suit growth while advisors managed 12 cross‑border deals in 2024, saving ~€6.2m.

| Partner | Key metric | 2024–25 |

|---|---|---|

| Major operators | Leased EBITDA share | 28% |

| Financial lenders | Annual capex funding | $85–120m (2025) |

| JV investors | Proceeds unlocked | $420m (H2 2025) |

| Advisors | Deals supported | 12 (2024), €6.2m tax saved |

What is included in the product

A ready-to-use MPT Business Model Canvas detailing customer segments, value propositions, channels, revenue streams, key activities, resources, partnerships, cost structure, and metrics, with integrated SWOT and competitive advantage analysis to support presentations, funding discussions, and validation of strategies using real-world company data.

Compact one-page MPT Business Model Canvas that condenses strategy into editable cells—ideal for quick boardroom reviews, team collaboration, and saving hours of formatting while comparing or adapting multiple company models.

Activities

Strategic Real Estate Acquisition

MPT scouts and acquires essential hospital properties serving local communities, prioritizing sites with clear clinical demand and stable payer mix; by 2025 MPT targeted acute care and behavioral health, which made up ~65% of new purchases in 2024–25.

Each deal follows strict due diligence on utilization, EBITDA and demographics—typical covenants include 12–24 month revenue recourse and cap rates around 6.5%–7.5%—so assets retain value across operator changes.

Portfolio Diversification and Optimization

MPT actively manages its portfolio to balance geographic reach and facility types—like inpatient rehabilitation and mental-health centers—while tracking tenant concentration to keep any single provider below 20% of NOI. In 2025 the firm cut exposure in four struggling U.S. markets and added 14 stable international assets, selling $185M of underperforming properties to lift portfolio occupancy to 94.3%.

Underwriting and Operator Monitoring

A core activity is continuous financial monitoring of hospital tenants to ensure they meet long-term lease obligations; MPT tracks admission rates, EBITDAR coverage, and liquidity using proprietary data and industry benchmarks—showing, for example, a median EBITDAR coverage target of 1.5x and monitoring admission variance within ±8% versus 2019 baselines. This proactive surveillance identifies distress early so MPT can deploy strategic interventions to protect revenue stability and investor returns.

Capital Recycling and Debt Management

MPT sold $420m of noncore assets in 2025 to cut net debt by 18% and slash blended interest cost from 6.8% to 5.4%, improving its credit metrics and raising pro forma NAV per share by ~6%.

Efficient capital recycling via divestitures and JV deals keeps liquidity up, lowers WACC, and preserves agility in a high-rate market.

- 2025 asset sales $420m

- Net debt down 18%

- Blended interest 6.8%→5.4%

- Pro forma NAV +6%

- Focus: deleveraging, JVs, lower WACC

Lease Structuring and Negotiation

MPT structures long-term triple-net leases so tenants pay maintenance, taxes, and insurance, with annual rent escalations tied to CPI or fixed 2–3% steps to preserve cash flow.

Negotiations secure tenant financial reporting and transparency; by 2025 MPT reports 95% of new leases include reporting covenants and lease yields average 6.2% NOI.

- Triple-net: tenant pays OPEX

- Escalations: CPI or 2–3% annually

- 2025: 95% leases require reporting

- Average lease yield 6.2% NOI

MPT trims debt, boosts NAV 6% after $420M sales; occupancy 94.3%, yield 6.2%

MPT acquires and manages hospital properties, using strict due diligence (EBITDAR target 1.5x, admission variance ±8%) and portfolio limits (single provider <20% NOI); in 2025 it sold $420M, cut net debt 18%, cut blended interest 6.8%→5.4%, and raised pro forma NAV ~6%, keeping occupancy 94.3% and average lease yield 6.2%.

| Metric | 2025 |

|---|---|

| Asset sales | $420M |

| Net debt change | -18% |

| Blended interest | 6.8%→5.4% |

| Pro forma NAV | +6% |

| Occupancy | 94.3% |

| Avg lease yield | 6.2% NOI |

| EBITDAR target | 1.5x |

Full Document Unlocks After Purchase

Business Model Canvas

The document you're previewing is the actual MPT Business Model Canvas you'll receive—no mockups or samples—presented exactly as in the final file.

When you complete your purchase, you'll instantly get this same professional, ready-to-edit document in both Word and Excel formats, with all sections and content included.