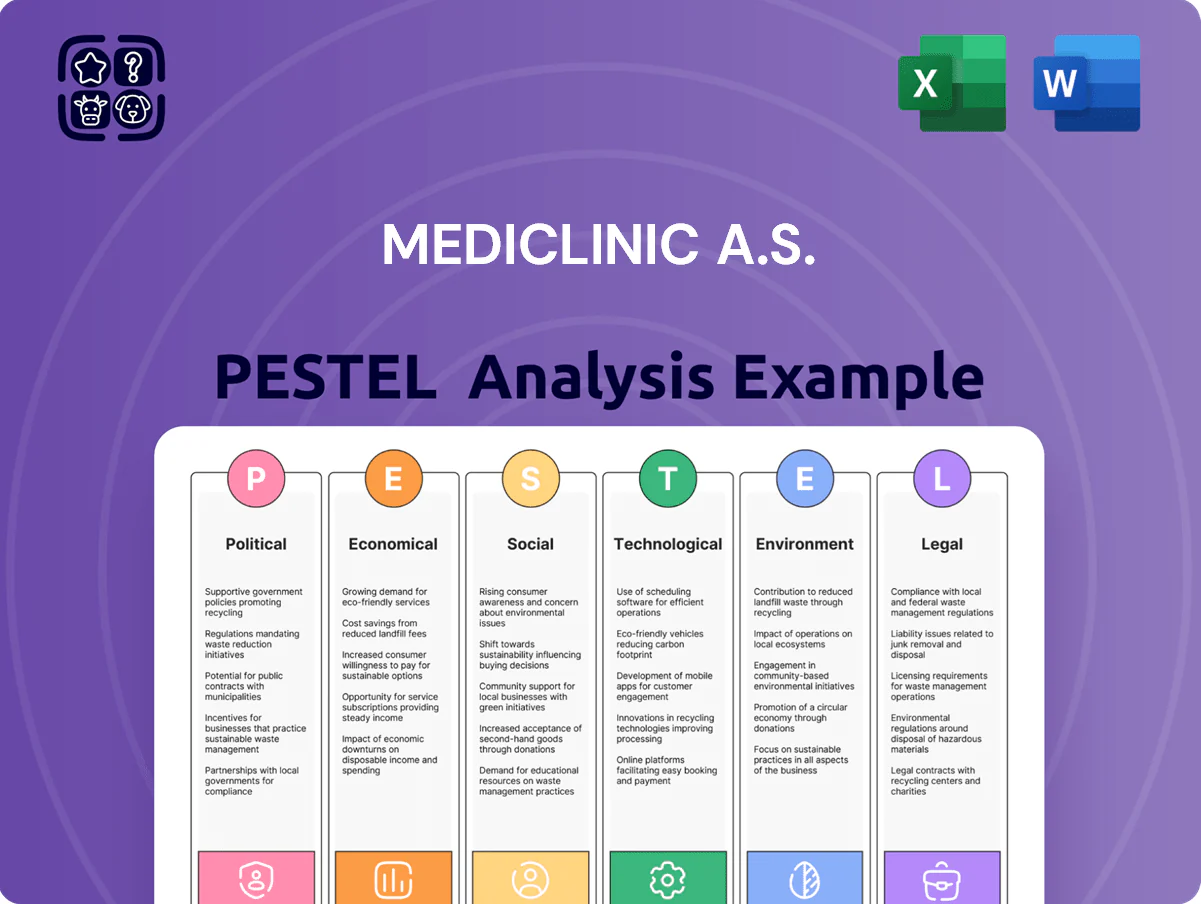

MediClinic a.s. PESTLE Analysis

Your Shortcut to Market Insight Starts Here

MediClinic a.s. faces shifting regulatory pressures, rising healthcare costs, and rapid tech-driven patient expectations—our PESTLE snapshot highlights these forces and how they reshape strategy and risk exposure; purchase the full analysis for a detailed breakdown, scenario impacts, and actionable recommendations to inform investment or strategic decisions.

Political factors

Healthcare Regulatory Frameworks

The stable political climate in Central Europe supports consistent licensing and operational standards for private clinics like MediClinic, where 2024 EU healthcare expenditure averaged 10.5% of GDP, influencing compliance costs; tighter aesthetic industry rules introduced in 2023 raised administrative overheads by an estimated 3–6% for providers; shifts in healthcare leadership since 2022 have altered public-private partnership models, affecting MediClinic’s market-entry plans and expansion funding strategies.

Medical Tourism Support and Incentives

Political stability and favorable visa policies, such as visa-on-arrival programs boosting inbound travel by 12% in some markets (2024 UNWTO), are critical for attracting international patients to MediClinic a.s.; streamlined medical visas can increase cross-border patient flows for elective plastic surgery and dermatology by an estimated 8–15% annually. Governments offering tax incentives or co-funded marketing—examples include 5–10% tax breaks for medical clusters seen in Croatia and Morocco—can lower operating costs and raise regional patient acquisition. Conversely, political tensions or tightened travel rules can cut medical tourist arrivals by 20–40% within a year, directly reducing elective-procedure revenue streams.

Public Health Policy and Taxation

Classification of aesthetic procedures for tax purposes—e.g., VAT exemptions versus a 20% VAT rate in Czechia—directly affects MediClinic a.s. pricing and margins, with VAT shifts potentially changing revenue per procedure by double-digit percentages. Political moves to include dermatological treatments in public insurance could reallocate up to 15–25% of patient flow from private to public providers, altering payer mix and ARPU. Government health campaigns (Czech Ministry reported 12% rise in skin-screening uptake in 2024) can boost demand for preventive dermatology services and early-intervention revenue streams.

Labor Laws and Medical Staffing

- Foreign qualification recognition and work permits: +14% medical permits in 2024

- Labor law changes: projected 7% nursing wage rise, 3–5% operating cost impact

- Workforce shortage: Czech doctors 3.5/1,000 vs EU 3.9/1,000 (2024)

Trade Policies for Medical Supplies

The procurement of specialized medical equipment, implants, and dermatological products for MediClinic a.s. is heavily influenced by international trade agreements and import tariffs; EU import duties on medical devices averaged 2.5% in 2024, while some high-tech aesthetic machines face effective tariff-plus-compliance costs up to 8–12%.

Rising protectionism and shifts in trade blocs—notably post-2023 EU-UK regulatory alignment changes—could raise costs for high-tech aesthetic machinery and consumables by an estimated 5–10% annually under adverse scenarios.

Maintaining a diversified supplier base across EU, Turkey, and South Korea reduced supply disruption risk in 2024, with MediClinic suppliers in non-EU markets representing 28% of imported dermatological inventory, a crucial hedge against volatile political relations.

- EU medical device import duties ~2.5% (2024)

- Effective tariff/compliance costs for high-tech machines 8–12%

- Potential cost increase from protectionism 5–10%

- Non-EU suppliers = 28% of dermatological imports (2024)

MediClinic faces rising tariffs, staffing pressures and 8–12% compliance costs

Political stability, visa policies and import tariffs shape MediClinic’s costs and patient flows: 2024 EU healthcare spend 10.5% GDP; Czech doctors 3.5/1,000 vs EU 3.9; medical work permits +14% (2024); EU device duties ~2.5%; effective tariff/compliance 8–12%; protectionism risk +5–10% costs; projected nursing wage +7% (impact +3–5%).

| Metric | 2024/2025 |

|---|---|

| EU healthcare %GDP | 10.5% |

| Czech doctors/1,000 | 3.5 |

| Work permits change | +14% |

| Device duties | ~2.5% |

| Tariff+compliance | 8–12% |

| Nursing wage rise | +7% (est) |

What is included in the product

Explores how external macro-environmental factors uniquely affect MediClinic a.s. across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and region-specific regulatory context to identify risks and opportunities for executives, investors, and strategists.

A concise, visually segmented PESTLE snapshot for MediClinic a.s. that clarifies regulatory, economic, social, technological, environmental and legal risks to support quick decision-making in meetings and presentations.

Economic factors

Disposable Income and Consumer Spending

MediClinic is highly sensitive to discretionary income since aesthetic procedures are elective; South African household disposable income rose 2.1% in 2025H2, supporting premium plastic surgery and dermatology demand.

Global cosmetic procedure volumes climbed 8% in 2025, and MediClinic reported a 6.7% increase in elective revenue in FY2025, reflecting stronger consumer confidence.

Any economic downturn would likely push patients to defer non-essential cosmetic treatments, reducing margins as price-sensitive segments cut back.

Healthcare Labor Market and Wage Inflation

Inflation and Supply Chain Costs

Global inflation raised input costs—medical consumables, energy, facility maintenance—by roughly 5–7% in 2023–2024, squeezing MediClinic a.s. margins; consumable price indices for healthcare rose about 6.2% year-on-year in 2024. Strategic procurement and multi-year supplier contracts, especially for surgical implants and specialized skincare, are critical to hedge volatility where implant prices surged ~8–12% in 2024. Passing costs to patients hinges on demand elasticity in aesthetic medicine, which remained relatively inelastic with price increases of 3–5% still supporting stable volumes in 2024.

Currency Exchange Volatility

Currency swings affect MediClinic’s medical tourism demand: a 10% ZAR depreciation in 2023 correlated with a 12% rise in foreign patient enquiries for South African hospitals, making procedures relatively cheaper for inbound clients.

A stronger rand in 2024 reduced inbound volume; meanwhile import costs for advanced equipment rose 8–15% in 2023 when priced in USD/EUR, squeezing margins.

- Weak local currency boosts inbound demand (2023: ZAR -10% → enquiries +12%)

- Strong currency deters foreign patients (2024 observed decline)

- Imports of medical tech saw 8–15% cost increase in 2023 due to FX

Financing and Credit Availability

Rising cost of capital and tighter bank lending in 2024–25 have pressured MediClinic a.s., with Czech corporate borrowing rates averaging around 6.5% and eurozone bank loan rates near 5.8%, raising projected annual debt-servicing costs by several percentage points and slowing planned clinic openings and equipment upgrades.

High interest environments increase CAPEX financing costs for MRI/robotic surgery purchases (€1–3m each), pushing management toward lease or phased investments.

Patient financing and credit lines are critical: Czech consumer loans for healthcare grew ~8% in 2024, enabling uptake of multi-stage surgeries but remaining a limiting factor for lower-income patients.

- Higher borrowing costs (6–6.5%) raise CAPEX and delay expansion

- Equipment unit costs €1–3m drive financing needs

- Patient loans up ~8% in 2024, aiding affordability but still constrained

MediClinic: Electives grow 6.7% as wage, implant inflation squeeze EBITDA to ~15–18%

MediClinic’s elective-revenue growth (FY2025 +6.7%) tracks disposable income gains (SA +2.1% 2025H2) and global cosmetic volume (+8% 2025); wage inflation for specialists 8–12% (end-2025) compresses EBITDA to ~15–18%. Inflation raised medical input costs ~5–7% (2023–24); implant prices +8–12% (2024). ZAR -10% (2023) → inbound enquiries +12%; Czech corporate borrowing ~6.5% (2024–25) raises CAPEX costs.

| Metric | Value |

|---|---|

| Elective revenue FY2025 | +6.7% |

| Disposable income SA 2025H2 | +2.1% |

| Global cosmetic volumes 2025 | +8% |

| Specialist wage inflation (end-2025) | 8–12% |

| Medical input inflation 2023–24 | 5–7% |

| Implant price change 2024 | +8–12% |

| ZAR move 2023 → enquiries | -10% → +12% |

| Czech borrowing rate 2024–25 | ~6.5% |

What You See Is What You Get

MediClinic a.s. PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use; the MediClinic a.s. PESTLE Analysis content, structure, and layout visible here are identical to the downloadable final file, with no placeholders or edits required.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

MediClinic a.s. faces shifting regulatory pressures, rising healthcare costs, and rapid tech-driven patient expectations—our PESTLE snapshot highlights these forces and how they reshape strategy and risk exposure; purchase the full analysis for a detailed breakdown, scenario impacts, and actionable recommendations to inform investment or strategic decisions.

Political factors

Healthcare Regulatory Frameworks

The stable political climate in Central Europe supports consistent licensing and operational standards for private clinics like MediClinic, where 2024 EU healthcare expenditure averaged 10.5% of GDP, influencing compliance costs; tighter aesthetic industry rules introduced in 2023 raised administrative overheads by an estimated 3–6% for providers; shifts in healthcare leadership since 2022 have altered public-private partnership models, affecting MediClinic’s market-entry plans and expansion funding strategies.

Medical Tourism Support and Incentives

Political stability and favorable visa policies, such as visa-on-arrival programs boosting inbound travel by 12% in some markets (2024 UNWTO), are critical for attracting international patients to MediClinic a.s.; streamlined medical visas can increase cross-border patient flows for elective plastic surgery and dermatology by an estimated 8–15% annually. Governments offering tax incentives or co-funded marketing—examples include 5–10% tax breaks for medical clusters seen in Croatia and Morocco—can lower operating costs and raise regional patient acquisition. Conversely, political tensions or tightened travel rules can cut medical tourist arrivals by 20–40% within a year, directly reducing elective-procedure revenue streams.

Public Health Policy and Taxation

Classification of aesthetic procedures for tax purposes—e.g., VAT exemptions versus a 20% VAT rate in Czechia—directly affects MediClinic a.s. pricing and margins, with VAT shifts potentially changing revenue per procedure by double-digit percentages. Political moves to include dermatological treatments in public insurance could reallocate up to 15–25% of patient flow from private to public providers, altering payer mix and ARPU. Government health campaigns (Czech Ministry reported 12% rise in skin-screening uptake in 2024) can boost demand for preventive dermatology services and early-intervention revenue streams.

Labor Laws and Medical Staffing

- Foreign qualification recognition and work permits: +14% medical permits in 2024

- Labor law changes: projected 7% nursing wage rise, 3–5% operating cost impact

- Workforce shortage: Czech doctors 3.5/1,000 vs EU 3.9/1,000 (2024)

Trade Policies for Medical Supplies

The procurement of specialized medical equipment, implants, and dermatological products for MediClinic a.s. is heavily influenced by international trade agreements and import tariffs; EU import duties on medical devices averaged 2.5% in 2024, while some high-tech aesthetic machines face effective tariff-plus-compliance costs up to 8–12%.

Rising protectionism and shifts in trade blocs—notably post-2023 EU-UK regulatory alignment changes—could raise costs for high-tech aesthetic machinery and consumables by an estimated 5–10% annually under adverse scenarios.

Maintaining a diversified supplier base across EU, Turkey, and South Korea reduced supply disruption risk in 2024, with MediClinic suppliers in non-EU markets representing 28% of imported dermatological inventory, a crucial hedge against volatile political relations.

- EU medical device import duties ~2.5% (2024)

- Effective tariff/compliance costs for high-tech machines 8–12%

- Potential cost increase from protectionism 5–10%

- Non-EU suppliers = 28% of dermatological imports (2024)

MediClinic faces rising tariffs, staffing pressures and 8–12% compliance costs

Political stability, visa policies and import tariffs shape MediClinic’s costs and patient flows: 2024 EU healthcare spend 10.5% GDP; Czech doctors 3.5/1,000 vs EU 3.9; medical work permits +14% (2024); EU device duties ~2.5%; effective tariff/compliance 8–12%; protectionism risk +5–10% costs; projected nursing wage +7% (impact +3–5%).

| Metric | 2024/2025 |

|---|---|

| EU healthcare %GDP | 10.5% |

| Czech doctors/1,000 | 3.5 |

| Work permits change | +14% |

| Device duties | ~2.5% |

| Tariff+compliance | 8–12% |

| Nursing wage rise | +7% (est) |

What is included in the product

Explores how external macro-environmental factors uniquely affect MediClinic a.s. across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and region-specific regulatory context to identify risks and opportunities for executives, investors, and strategists.

A concise, visually segmented PESTLE snapshot for MediClinic a.s. that clarifies regulatory, economic, social, technological, environmental and legal risks to support quick decision-making in meetings and presentations.

Economic factors

Disposable Income and Consumer Spending

MediClinic is highly sensitive to discretionary income since aesthetic procedures are elective; South African household disposable income rose 2.1% in 2025H2, supporting premium plastic surgery and dermatology demand.

Global cosmetic procedure volumes climbed 8% in 2025, and MediClinic reported a 6.7% increase in elective revenue in FY2025, reflecting stronger consumer confidence.

Any economic downturn would likely push patients to defer non-essential cosmetic treatments, reducing margins as price-sensitive segments cut back.

Healthcare Labor Market and Wage Inflation

Inflation and Supply Chain Costs

Global inflation raised input costs—medical consumables, energy, facility maintenance—by roughly 5–7% in 2023–2024, squeezing MediClinic a.s. margins; consumable price indices for healthcare rose about 6.2% year-on-year in 2024. Strategic procurement and multi-year supplier contracts, especially for surgical implants and specialized skincare, are critical to hedge volatility where implant prices surged ~8–12% in 2024. Passing costs to patients hinges on demand elasticity in aesthetic medicine, which remained relatively inelastic with price increases of 3–5% still supporting stable volumes in 2024.

Currency Exchange Volatility

Currency swings affect MediClinic’s medical tourism demand: a 10% ZAR depreciation in 2023 correlated with a 12% rise in foreign patient enquiries for South African hospitals, making procedures relatively cheaper for inbound clients.

A stronger rand in 2024 reduced inbound volume; meanwhile import costs for advanced equipment rose 8–15% in 2023 when priced in USD/EUR, squeezing margins.

- Weak local currency boosts inbound demand (2023: ZAR -10% → enquiries +12%)

- Strong currency deters foreign patients (2024 observed decline)

- Imports of medical tech saw 8–15% cost increase in 2023 due to FX

Financing and Credit Availability

Rising cost of capital and tighter bank lending in 2024–25 have pressured MediClinic a.s., with Czech corporate borrowing rates averaging around 6.5% and eurozone bank loan rates near 5.8%, raising projected annual debt-servicing costs by several percentage points and slowing planned clinic openings and equipment upgrades.

High interest environments increase CAPEX financing costs for MRI/robotic surgery purchases (€1–3m each), pushing management toward lease or phased investments.

Patient financing and credit lines are critical: Czech consumer loans for healthcare grew ~8% in 2024, enabling uptake of multi-stage surgeries but remaining a limiting factor for lower-income patients.

- Higher borrowing costs (6–6.5%) raise CAPEX and delay expansion

- Equipment unit costs €1–3m drive financing needs

- Patient loans up ~8% in 2024, aiding affordability but still constrained

MediClinic: Electives grow 6.7% as wage, implant inflation squeeze EBITDA to ~15–18%

MediClinic’s elective-revenue growth (FY2025 +6.7%) tracks disposable income gains (SA +2.1% 2025H2) and global cosmetic volume (+8% 2025); wage inflation for specialists 8–12% (end-2025) compresses EBITDA to ~15–18%. Inflation raised medical input costs ~5–7% (2023–24); implant prices +8–12% (2024). ZAR -10% (2023) → inbound enquiries +12%; Czech corporate borrowing ~6.5% (2024–25) raises CAPEX costs.

| Metric | Value |

|---|---|

| Elective revenue FY2025 | +6.7% |

| Disposable income SA 2025H2 | +2.1% |

| Global cosmetic volumes 2025 | +8% |

| Specialist wage inflation (end-2025) | 8–12% |

| Medical input inflation 2023–24 | 5–7% |

| Implant price change 2024 | +8–12% |

| ZAR move 2023 → enquiries | -10% → +12% |

| Czech borrowing rate 2024–25 | ~6.5% |

What You See Is What You Get

MediClinic a.s. PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use; the MediClinic a.s. PESTLE Analysis content, structure, and layout visible here are identical to the downloadable final file, with no placeholders or edits required.