Mega Financial Holding PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

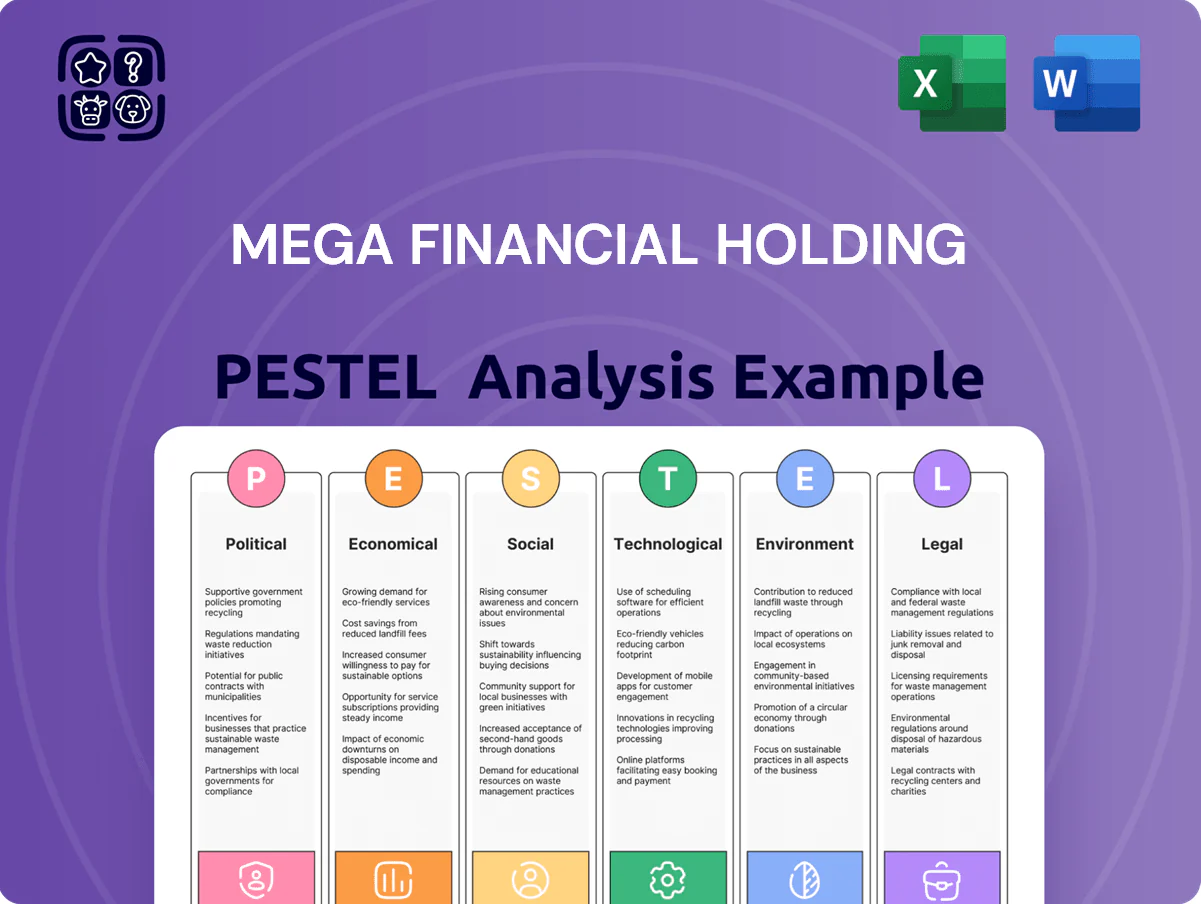

Our PESTLE snapshot reveals how political shifts, economic cycles, regulatory pressures, societal trends, technological disruption, and environmental risks converge to shape Mega Financial Holding’s strategic outlook—use this briefing to spot risks and opportunities fast. Purchase the full PESTLE to get the comprehensive, editable analysis investors and strategists rely on for confident decision-making.

Political factors

Geopolitical Cross-Strait Tensions

The ongoing geopolitical friction between Taiwan and mainland China remains a primary risk for Mega Financial Holding, where cross-Strait tensions contributed to a 12% volatility spike in regional equity flows in 2023 and a 7% FX reserve reallocation by Taiwan banks in 2024.

As a state-linked entity, Mega is sensitive to shifts in regional security that could disrupt trade—Taiwan's exports to China represented ~28% of GDP in 2023—threatening credit quality and capital stability.

Management must diversify international operations: Mega reported only 14% of revenue from Southeast Asia in 2024, indicating localized concentration risk that diversification could reduce.

Government Ownership and Influence

The Ministry of Finance of Taiwan holds about 12.47% of Mega Financial as of 2025, giving it decisive influence over board appointments and strategy; this state stake fosters stability and alignment with national policy but can shift priorities toward economic goals over profit, as seen in the 2024 directive favoring SME lending, which contributed to a 3.2% decline in ROE that year; investors watch for effects on dividend payout and capital allocation.

International Trade Relations

Mega Financial’s extensive overseas network is exposed to shifts in Taiwan’s diplomatic status and evolving US-China trade policies, which in 2024 saw US-China goods trade at about $690 billion, impacting regional supply chains and banking needs.

Potential Taiwan accession to CPTPP (11 members, GDP ~$13.5 trillion in 2023) would boost export-related corporate banking; export-oriented clients (Taiwan exports ~US$430 billion in 2024) may increase demand for trade finance.

The group leverages its 2025 global branch footprint to offer letters of credit and supply-chain financing, supporting clients through tariff changes and supply disruptions while capturing cross-border fee income.

Regulatory Oversight in Foreign Markets

- 35 jurisdictions covered

- 120 government-relations staff

- 22% faster time-to-compliance

- 18% rise in sector regulatory fines (2024)

Domestic Policy and Fiscal Stability

The Taiwanese government's fiscal surplus of NT$82.5 billion in 2024 and stable political environment underpin Mega Financial's core banking operations, reducing credit risk and supporting steady deposit growth.

Changes to corporate tax rates, housing policies or the NT$1.5 trillion 2024–2026 infrastructure package would shift demand for commercial and retail lending, affecting loan volumes and NIMs.

As a domestic financial pillar with NT$5.2 trillion in assets (2024), Mega Financial both supports and benefits from national economic resilience.

- 2024 fiscal surplus NT$82.5bn

- Infrastructure package NT$1.5tn (2024–2026)

- Mega Financial assets NT$5.2tn (2024)

China tensions, state stake dent ROE; Taiwan concentration, fines spike demand diversification

Geopolitical tensions with China elevate market and FX volatility (12% equity flow spike in 2023; 7% FX reserve shift in 2024), while state ownership (Ministry 12.47% in 2025) steers strategy toward policy goals, affecting ROE (−3.2% in 2024) and dividend signals; concentrated Taiwan revenue (86% domestic; 14% SEA in 2024) raises diversification need across 35 jurisdictions amid rising regulatory fines (+18% in 2024).

| Metric | Value |

|---|---|

| Equity flow volatility (2023) | +12% |

| FX reserve reallocation (2024) | 7% |

| Ministry stake (2025) | 12.47% |

| ROE impact (2024) | −3.2% |

| Domestic revenue (2024) | 86% |

| Jurisdictions | 35 |

| Regulatory fines rise (2024) | +18% |

What is included in the product

Explores how macro-environmental factors—Political, Economic, Social, Technological, Environmental, and Legal—specifically influence Mega Financial Holding, with data-driven trends and regional regulatory context to highlight risks and opportunities.

A concise PESTLE summary tailored for Mega Financial Holding that distills regulatory, economic, social, technological, environmental, and legal drivers into a meeting-ready format to speed decision-making and risk discussion.

Economic factors

Interest Rate Environment and NIM

The trajectory of global and domestic interest rates directly affects Mega Financial’s NIM—each 100bp rise in policy rates lifted peer bank NIMs by ~15–30bps in 2024; Mega’s USD assets (≈42% of loans) make Fed moves crucial after the Fed held 5.25–5.50% in late 2024. As central banks shift from inflation control toward growth support, Mega must shorten asset-liability duration and hedge rate risk to protect earnings and capital ratios.

Currency Exchange Rate Volatility

As a major player in foreign exchange and trade finance, Mega Financial is highly sensitive to NT$ valuation versus the USD and other majors; NT$ moved about 3.8% versus USD in 2024, amplifying translation risk for offshore holdings. Exchange-rate volatility directly alters valuation of overseas assets and raised hedging costs—Mega reported a 12% rise in FX hedging expenses across its insurance and investment units in 2024. Effective currency risk management is therefore essential to stabilize net income and limit VaR exposure.

Global Economic Growth Trends

Global GDP growth slowed to an estimated 3.1% in 2024, weighing on demand for Mega Financial’s corporate banking and investment services, especially from semiconductor and tech clients that account for roughly 28% of corporate loan exposure.

A downturn in major markets can cut credit demand and lift NPL ratios; export-heavy clients saw NPLs rise to 2.9% in 2024 vs 1.8% in 2022.

Diversified revenue—asset management fees (22% of 2024 revenue) and insurance premiums (15%)—helps buffer earnings against cyclical banking volatility.

Inflationary Pressures and Operating Costs

Persistent inflation in 2025 (US CPI ~3.4% YoY in Jan 2025) raises Mega Financial's operating expenses and erodes retail customers' purchasing power, reducing deposit growth and loan demand.

Rising wages (average private sector pay up ~4.2% in 2024) and higher tech/cloud costs compress margins unless offset by efficiency gains or fee income growth.

Mega Financial tracks CPI and PCE indexes to recalibrate product pricing and internal cost structures quarterly.

- 2025 CPI ~3.4% YoY — pressures pricing

- 2024 avg wages +4.2% — higher staff costs

- Tech spend up 10–15% YoY in banking — margin risk

- Quarterly CPI monitoring informs fee/pricing adjustments

Capital Market Performance

The Taiwan Stock Exchange's 2025 average daily turnover rose 12% year-over-year to NT$75.3 billion, boosting Mega Financial’s brokerage and wealth management fee income; global equity rebounds (MSCI World +9% in 2024) also lifted cross-border asset flows.

Heightened volatility in 2024–2025 increased mark-to-market swings across Mega’s proprietary portfolios, while client demand for diversified asset management products grew—non-interest income rose 8% in FY2024.

- TSE turnover +12% (2025 Y/Y) to NT$75.3bn

- MSCI World +9% (2024)

- Mega non-interest income +8% (FY2024)

- Higher volatility → larger portfolio valuation swings

Higher rates boost NIMs but FX costs and rising NPLs temper 2024 earnings

Higher global rates lift NIMs (100bp → +15–30bps in 2024); Fed 5.25–5.50% (late‑2024) critical for Mega’s USD ≈42% loan book. NT$ volatility (~3.8% vs USD in 2024) raised FX hedging costs (+12% in 2024). Global GDP 3.1% (2024) and sectoral slowdown pushed NPLs to 2.9% (2024); non‑interest income +8% (FY2024) cushions earnings.

| Metric | Value |

|---|---|

| Fed policy rate (late‑2024) | 5.25–5.50% |

| USD loan share | ≈42% |

| NT$ vs USD (2024) | ±3.8% |

| FX hedging cost change (2024) | +12% |

| Global GDP (2024) | 3.1% |

| NPL ratio (2024) | 2.9% |

| Non‑interest income (FY2024) | +8% |

What You See Is What You Get

Mega Financial Holding PESTLE Analysis

The preview shown here is the exact Mega Financial Holding PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Our PESTLE snapshot reveals how political shifts, economic cycles, regulatory pressures, societal trends, technological disruption, and environmental risks converge to shape Mega Financial Holding’s strategic outlook—use this briefing to spot risks and opportunities fast. Purchase the full PESTLE to get the comprehensive, editable analysis investors and strategists rely on for confident decision-making.

Political factors

Geopolitical Cross-Strait Tensions

The ongoing geopolitical friction between Taiwan and mainland China remains a primary risk for Mega Financial Holding, where cross-Strait tensions contributed to a 12% volatility spike in regional equity flows in 2023 and a 7% FX reserve reallocation by Taiwan banks in 2024.

As a state-linked entity, Mega is sensitive to shifts in regional security that could disrupt trade—Taiwan's exports to China represented ~28% of GDP in 2023—threatening credit quality and capital stability.

Management must diversify international operations: Mega reported only 14% of revenue from Southeast Asia in 2024, indicating localized concentration risk that diversification could reduce.

Government Ownership and Influence

The Ministry of Finance of Taiwan holds about 12.47% of Mega Financial as of 2025, giving it decisive influence over board appointments and strategy; this state stake fosters stability and alignment with national policy but can shift priorities toward economic goals over profit, as seen in the 2024 directive favoring SME lending, which contributed to a 3.2% decline in ROE that year; investors watch for effects on dividend payout and capital allocation.

International Trade Relations

Mega Financial’s extensive overseas network is exposed to shifts in Taiwan’s diplomatic status and evolving US-China trade policies, which in 2024 saw US-China goods trade at about $690 billion, impacting regional supply chains and banking needs.

Potential Taiwan accession to CPTPP (11 members, GDP ~$13.5 trillion in 2023) would boost export-related corporate banking; export-oriented clients (Taiwan exports ~US$430 billion in 2024) may increase demand for trade finance.

The group leverages its 2025 global branch footprint to offer letters of credit and supply-chain financing, supporting clients through tariff changes and supply disruptions while capturing cross-border fee income.

Regulatory Oversight in Foreign Markets

- 35 jurisdictions covered

- 120 government-relations staff

- 22% faster time-to-compliance

- 18% rise in sector regulatory fines (2024)

Domestic Policy and Fiscal Stability

The Taiwanese government's fiscal surplus of NT$82.5 billion in 2024 and stable political environment underpin Mega Financial's core banking operations, reducing credit risk and supporting steady deposit growth.

Changes to corporate tax rates, housing policies or the NT$1.5 trillion 2024–2026 infrastructure package would shift demand for commercial and retail lending, affecting loan volumes and NIMs.

As a domestic financial pillar with NT$5.2 trillion in assets (2024), Mega Financial both supports and benefits from national economic resilience.

- 2024 fiscal surplus NT$82.5bn

- Infrastructure package NT$1.5tn (2024–2026)

- Mega Financial assets NT$5.2tn (2024)

China tensions, state stake dent ROE; Taiwan concentration, fines spike demand diversification

Geopolitical tensions with China elevate market and FX volatility (12% equity flow spike in 2023; 7% FX reserve shift in 2024), while state ownership (Ministry 12.47% in 2025) steers strategy toward policy goals, affecting ROE (−3.2% in 2024) and dividend signals; concentrated Taiwan revenue (86% domestic; 14% SEA in 2024) raises diversification need across 35 jurisdictions amid rising regulatory fines (+18% in 2024).

| Metric | Value |

|---|---|

| Equity flow volatility (2023) | +12% |

| FX reserve reallocation (2024) | 7% |

| Ministry stake (2025) | 12.47% |

| ROE impact (2024) | −3.2% |

| Domestic revenue (2024) | 86% |

| Jurisdictions | 35 |

| Regulatory fines rise (2024) | +18% |

What is included in the product

Explores how macro-environmental factors—Political, Economic, Social, Technological, Environmental, and Legal—specifically influence Mega Financial Holding, with data-driven trends and regional regulatory context to highlight risks and opportunities.

A concise PESTLE summary tailored for Mega Financial Holding that distills regulatory, economic, social, technological, environmental, and legal drivers into a meeting-ready format to speed decision-making and risk discussion.

Economic factors

Interest Rate Environment and NIM

The trajectory of global and domestic interest rates directly affects Mega Financial’s NIM—each 100bp rise in policy rates lifted peer bank NIMs by ~15–30bps in 2024; Mega’s USD assets (≈42% of loans) make Fed moves crucial after the Fed held 5.25–5.50% in late 2024. As central banks shift from inflation control toward growth support, Mega must shorten asset-liability duration and hedge rate risk to protect earnings and capital ratios.

Currency Exchange Rate Volatility

As a major player in foreign exchange and trade finance, Mega Financial is highly sensitive to NT$ valuation versus the USD and other majors; NT$ moved about 3.8% versus USD in 2024, amplifying translation risk for offshore holdings. Exchange-rate volatility directly alters valuation of overseas assets and raised hedging costs—Mega reported a 12% rise in FX hedging expenses across its insurance and investment units in 2024. Effective currency risk management is therefore essential to stabilize net income and limit VaR exposure.

Global Economic Growth Trends

Global GDP growth slowed to an estimated 3.1% in 2024, weighing on demand for Mega Financial’s corporate banking and investment services, especially from semiconductor and tech clients that account for roughly 28% of corporate loan exposure.

A downturn in major markets can cut credit demand and lift NPL ratios; export-heavy clients saw NPLs rise to 2.9% in 2024 vs 1.8% in 2022.

Diversified revenue—asset management fees (22% of 2024 revenue) and insurance premiums (15%)—helps buffer earnings against cyclical banking volatility.

Inflationary Pressures and Operating Costs

Persistent inflation in 2025 (US CPI ~3.4% YoY in Jan 2025) raises Mega Financial's operating expenses and erodes retail customers' purchasing power, reducing deposit growth and loan demand.

Rising wages (average private sector pay up ~4.2% in 2024) and higher tech/cloud costs compress margins unless offset by efficiency gains or fee income growth.

Mega Financial tracks CPI and PCE indexes to recalibrate product pricing and internal cost structures quarterly.

- 2025 CPI ~3.4% YoY — pressures pricing

- 2024 avg wages +4.2% — higher staff costs

- Tech spend up 10–15% YoY in banking — margin risk

- Quarterly CPI monitoring informs fee/pricing adjustments

Capital Market Performance

The Taiwan Stock Exchange's 2025 average daily turnover rose 12% year-over-year to NT$75.3 billion, boosting Mega Financial’s brokerage and wealth management fee income; global equity rebounds (MSCI World +9% in 2024) also lifted cross-border asset flows.

Heightened volatility in 2024–2025 increased mark-to-market swings across Mega’s proprietary portfolios, while client demand for diversified asset management products grew—non-interest income rose 8% in FY2024.

- TSE turnover +12% (2025 Y/Y) to NT$75.3bn

- MSCI World +9% (2024)

- Mega non-interest income +8% (FY2024)

- Higher volatility → larger portfolio valuation swings

Higher rates boost NIMs but FX costs and rising NPLs temper 2024 earnings

Higher global rates lift NIMs (100bp → +15–30bps in 2024); Fed 5.25–5.50% (late‑2024) critical for Mega’s USD ≈42% loan book. NT$ volatility (~3.8% vs USD in 2024) raised FX hedging costs (+12% in 2024). Global GDP 3.1% (2024) and sectoral slowdown pushed NPLs to 2.9% (2024); non‑interest income +8% (FY2024) cushions earnings.

| Metric | Value |

|---|---|

| Fed policy rate (late‑2024) | 5.25–5.50% |

| USD loan share | ≈42% |

| NT$ vs USD (2024) | ±3.8% |

| FX hedging cost change (2024) | +12% |

| Global GDP (2024) | 3.1% |

| NPL ratio (2024) | 2.9% |

| Non‑interest income (FY2024) | +8% |

What You See Is What You Get

Mega Financial Holding PESTLE Analysis

The preview shown here is the exact Mega Financial Holding PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.