Meier Tobler PESTLE Analysis

Skip the Research. Get the Strategy.

Discover how political, economic, social, technological, legal, and environmental forces are shaping Meier Tobler’s strategy and risk profile—our concise PESTLE snapshot highlights critical external trends. Ready-made for investors and strategists, the full analysis delivers in-depth, actionable intelligence and editable tools. Purchase now to download the complete, expertly researched PESTLE report instantly.

Political factors

Swiss Energy Strategy 2050 Implementation

The Swiss federal Energy Strategy 2050 mandates a 50% reduction in building-sector fossil fuel use by 2035 and net-zero by 2050, creating sustained demand for heating-system renewals; Meier Tobler stands to benefit as cantonal subsidy programs (CHF 1.5–3.0bn annual allocations in 2024–25) and CO2 pricing drive replacement of oil/gas boilers with heat pumps and district heating, aligning national and cantonal regulations to accelerate retrofit volumes and recurring service revenue streams.

Cantonal Energy Regulations and MuKEn

Geopolitical Impact on Energy Security

Political instability in Eastern Europe and the Middle East has raised EU gas supply risk; EU gas imports from Russia fell 80% in 2023, pushing Switzerland to target 50% domestic electricity from renewables by 2035 and a 25% reduction in final energy consumption by 2030; this shifts Swiss policy toward electrification and away from gas HVAC, accelerating retrofit demand and positioning Meier Tobler—with its 2024 HVAC project pipeline and solutions—as a strategic partner for national energy resilience.

Subsidy Programs and Financial Incentives

Das Gebaeudeprogramm and related federal schemes offered CHF 1.2–1.5 billion in subsidies annually through 2023–2024, covering up to 30–40% of heat pump installation costs and significantly cutting upfront capital needs for homeowners and developers, boosting demand for Meier Tobler’s premium heat pump lines.

Continuation into 2025 is pivotal: modelled uptake drops ~25% if subsidies lapse, risking slower revenue growth for Meier Tobler amid Swiss market transition to low-carbon heating.

- CHF 1.2–1.5bn annual subsidies (2023–24)

- 30–40% cost coverage for heat pump installs

- ~25% projected demand decline if programs end 2025

- Directly increases market for Meier Tobler premium products

Trade Relations and Supply Chain Policy

Swiss-EU trade dynamics are critical for Meier Tobler, which sourced roughly 65% of its HVACR components from EU suppliers in 2024; disruptions or new technical barriers could raise input costs by an estimated 5–12% and extend lead times beyond current average 6–10 weeks.

Any revision to bilateral agreements or customs procedures risks margin pressure and inventory shortfalls; Meier Tobler must hedge via diversified suppliers, increased local inventory (targeting 3–4 months coverage) and supplier contracts with price/lead-time clauses to protect domestic pricing.

- 65% of components from EU (2024)

- Potential cost increase 5–12% if barriers arise

- Current lead times 6–10 weeks

- Target inventory cover 3–4 months

Swiss heat-pump surge driven by subsidies, electrification and EU supply risk

Federal Energy Strategy 2050, MuKEn uptake (20+ cantons by 2025) and CHF 1.2–3.0bn annual subsidies (2023–25) accelerate heat-pump demand (Swiss installations +12% in 2024 to ~230,000), while CO2 pricing and EU gas cuts shift policy to electrification; 65% EU-sourced components (2024) face 5–12% cost risk if trade barriers rise, prompting 3–4 months inventory target.

| Metric | 2024–25 |

|---|---|

| Subsidies | CHF 1.2–3.0bn |

| Heat pumps | ~230,000 (+12%) |

| EU sourcing | 65% |

| Cost risk | +5–12% |

What is included in the product

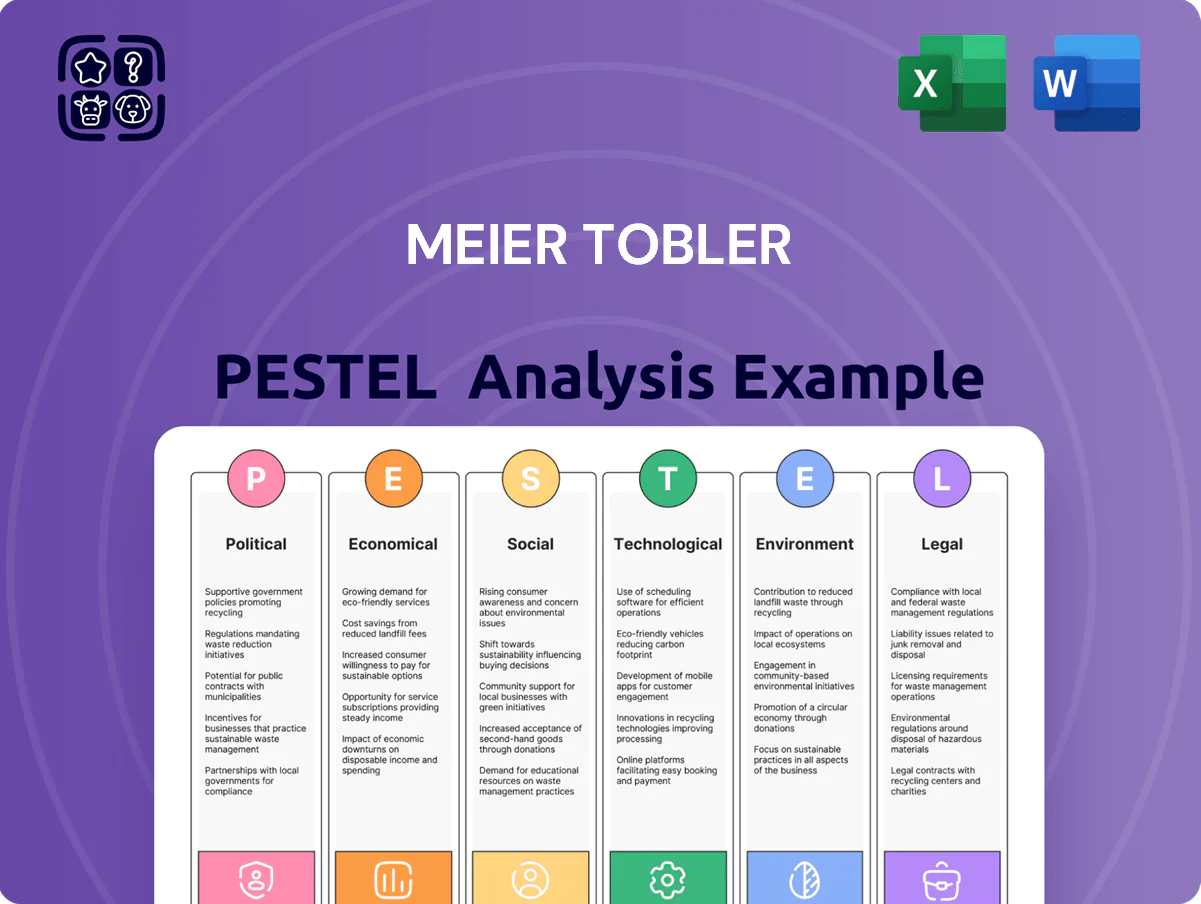

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely impact Meier Tobler, with data-driven insights and trend analysis to highlight risks and opportunities for strategic decision-making.

Meier Tobler PESTLE delivers a concise, visually segmented summary of external risks and market factors that can be dropped into presentations or shared across teams for fast alignment and decision-making.

Economic factors

Interest Rate Environment and Construction Activity

The Swiss National Bank’s policy drives borrowing costs for construction; after peak volatility in 2022–24, rates stabilized near 1.75%–2.00% by end-2025, easing financing for developers. Past rate swings trimmed new-build approvals—Swiss construction investment fell about 3.5% in 2023—making developers cautious on capital-intensive projects. Meier Tobler’s revenues closely track industry activity, so financing conditions materially affect orderbooks and margins.

Labor Shortages and Wage Inflation

The Swiss labor market faces a persistent shortage of skilled HVACR technicians and engineers, with the Federal Statistical Office reporting a structural vacancy rate of 3.5% in technical occupations in 2024, constraining installation and maintenance capacity for Meier Tobler.

This scarcity drives wage inflation—average annual technician salaries rose about 4.2% in 2024—pressuring gross margins and increasing service delivery costs.

To mitigate, Meier Tobler must scale recruitment and invest in training; in 2025 industry surveys show firms spending up to CHF 6,000 per hire on upskilling and retention strategies.

Currency Fluctuations and Import Costs

The Swiss franc appreciated about 2.8% vs the euro and 1.5% vs the US dollar in 2024, lowering import costs for Meier Tobler’s European-sourced components and potentially lifting gross margins if sales prices hold. Yet franc volatility—daily moves up to 1.2% in 2024—raises exposure to sudden COGS increases; active hedging (forwards/options) and a FX policy are needed to stabilize earnings and protect operating margin.

Inflationary Pressures on Raw Materials

Global supply-chain disruptions and 2024–25 commodity cycles raised copper and aluminum prices by ~18–24% YoY and steel by ~12% in 2024, directly increasing HVACR component costs for Meier Tobler.

Economic shifts in China and EU manufacturing hubs cause episodic spikes, forcing potential pass-throughs; Swiss inflation (~2.3% in 2024) limits full price recovery.

Procurement must hedge and optimize sourcing while sales balance margin retention and competitiveness in Switzerland.

- Copper +18–24% (2024)

- Aluminum similar range

- Steel +12% (2024)

- Swiss CPI ~2.3% (2024)

Evolution of the Service Economy

The market is shifting toward heat-as-a-service and long-term maintenance, with global equipment-as-a-service revenue growing ~8% CAGR 2020–2024 and service contracts now representing ~30–40% of revenues for leading HVAC firms in 2024; this gives Meier Tobler more predictable recurring revenue and higher customer lifetime value.

Prioritizing service and maintenance reduces exposure to the new-build cycle, where Swiss construction starts fell ~5% in 2023, while service spending remained stable, cushioning cash flow and margin volatility.

- Recurring revenue share rises customer LTV; service margins typically 15–25% vs product 5–10%

- Heat-as-a-service demand growing ~6–9% annually in Europe (2022–2024)

- Service focus hedges against new-build cyclical downturns (Swiss starts -5% in 2023)

Margins squeezed as CHF strength, rising metals & wages meet weak construction demand

SNB rates steady ~1.75–2.00% (end-2025); construction investment down 3.5% (2023) impacting orderbooks; technician vacancy 3.5% (2024) and wages +4.2% pressuring margins; CHF appreciated +2.8% vs EUR (2024) easing import costs but FX volatility persists; copper +18–24%, aluminum +18–24%, steel +12% (2024); service revenue share 30–40%, service margins 15–25%.

| Metric | Value (latest) |

|---|---|

| SNB rates | 1.75–2.00% |

| Construction inv. | -3.5% (2023) |

| Technician vacancy | 3.5% (2024) |

| Wage growth | +4.2% (2024) |

| CHF vs EUR | +2.8% (2024) |

| Copper/Al/Steel | +18–24% / +18–24% / +12% (2024) |

| Service revenue share | 30–40% |

Preview Before You Purchase

Meier Tobler PESTLE Analysis

The preview shown here is the exact Meier Tobler PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the content, layout, and insights visible in this preview are identical to the downloadable file delivered immediately after payment.

What you see is the finished document—concise, actionable, and prepared for presentation or integration into your strategic planning.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Skip the Research. Get the Strategy.

Discover how political, economic, social, technological, legal, and environmental forces are shaping Meier Tobler’s strategy and risk profile—our concise PESTLE snapshot highlights critical external trends. Ready-made for investors and strategists, the full analysis delivers in-depth, actionable intelligence and editable tools. Purchase now to download the complete, expertly researched PESTLE report instantly.

Political factors

Swiss Energy Strategy 2050 Implementation

The Swiss federal Energy Strategy 2050 mandates a 50% reduction in building-sector fossil fuel use by 2035 and net-zero by 2050, creating sustained demand for heating-system renewals; Meier Tobler stands to benefit as cantonal subsidy programs (CHF 1.5–3.0bn annual allocations in 2024–25) and CO2 pricing drive replacement of oil/gas boilers with heat pumps and district heating, aligning national and cantonal regulations to accelerate retrofit volumes and recurring service revenue streams.

Cantonal Energy Regulations and MuKEn

Geopolitical Impact on Energy Security

Political instability in Eastern Europe and the Middle East has raised EU gas supply risk; EU gas imports from Russia fell 80% in 2023, pushing Switzerland to target 50% domestic electricity from renewables by 2035 and a 25% reduction in final energy consumption by 2030; this shifts Swiss policy toward electrification and away from gas HVAC, accelerating retrofit demand and positioning Meier Tobler—with its 2024 HVAC project pipeline and solutions—as a strategic partner for national energy resilience.

Subsidy Programs and Financial Incentives

Das Gebaeudeprogramm and related federal schemes offered CHF 1.2–1.5 billion in subsidies annually through 2023–2024, covering up to 30–40% of heat pump installation costs and significantly cutting upfront capital needs for homeowners and developers, boosting demand for Meier Tobler’s premium heat pump lines.

Continuation into 2025 is pivotal: modelled uptake drops ~25% if subsidies lapse, risking slower revenue growth for Meier Tobler amid Swiss market transition to low-carbon heating.

- CHF 1.2–1.5bn annual subsidies (2023–24)

- 30–40% cost coverage for heat pump installs

- ~25% projected demand decline if programs end 2025

- Directly increases market for Meier Tobler premium products

Trade Relations and Supply Chain Policy

Swiss-EU trade dynamics are critical for Meier Tobler, which sourced roughly 65% of its HVACR components from EU suppliers in 2024; disruptions or new technical barriers could raise input costs by an estimated 5–12% and extend lead times beyond current average 6–10 weeks.

Any revision to bilateral agreements or customs procedures risks margin pressure and inventory shortfalls; Meier Tobler must hedge via diversified suppliers, increased local inventory (targeting 3–4 months coverage) and supplier contracts with price/lead-time clauses to protect domestic pricing.

- 65% of components from EU (2024)

- Potential cost increase 5–12% if barriers arise

- Current lead times 6–10 weeks

- Target inventory cover 3–4 months

Swiss heat-pump surge driven by subsidies, electrification and EU supply risk

Federal Energy Strategy 2050, MuKEn uptake (20+ cantons by 2025) and CHF 1.2–3.0bn annual subsidies (2023–25) accelerate heat-pump demand (Swiss installations +12% in 2024 to ~230,000), while CO2 pricing and EU gas cuts shift policy to electrification; 65% EU-sourced components (2024) face 5–12% cost risk if trade barriers rise, prompting 3–4 months inventory target.

| Metric | 2024–25 |

|---|---|

| Subsidies | CHF 1.2–3.0bn |

| Heat pumps | ~230,000 (+12%) |

| EU sourcing | 65% |

| Cost risk | +5–12% |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely impact Meier Tobler, with data-driven insights and trend analysis to highlight risks and opportunities for strategic decision-making.

Meier Tobler PESTLE delivers a concise, visually segmented summary of external risks and market factors that can be dropped into presentations or shared across teams for fast alignment and decision-making.

Economic factors

Interest Rate Environment and Construction Activity

The Swiss National Bank’s policy drives borrowing costs for construction; after peak volatility in 2022–24, rates stabilized near 1.75%–2.00% by end-2025, easing financing for developers. Past rate swings trimmed new-build approvals—Swiss construction investment fell about 3.5% in 2023—making developers cautious on capital-intensive projects. Meier Tobler’s revenues closely track industry activity, so financing conditions materially affect orderbooks and margins.

Labor Shortages and Wage Inflation

The Swiss labor market faces a persistent shortage of skilled HVACR technicians and engineers, with the Federal Statistical Office reporting a structural vacancy rate of 3.5% in technical occupations in 2024, constraining installation and maintenance capacity for Meier Tobler.

This scarcity drives wage inflation—average annual technician salaries rose about 4.2% in 2024—pressuring gross margins and increasing service delivery costs.

To mitigate, Meier Tobler must scale recruitment and invest in training; in 2025 industry surveys show firms spending up to CHF 6,000 per hire on upskilling and retention strategies.

Currency Fluctuations and Import Costs

The Swiss franc appreciated about 2.8% vs the euro and 1.5% vs the US dollar in 2024, lowering import costs for Meier Tobler’s European-sourced components and potentially lifting gross margins if sales prices hold. Yet franc volatility—daily moves up to 1.2% in 2024—raises exposure to sudden COGS increases; active hedging (forwards/options) and a FX policy are needed to stabilize earnings and protect operating margin.

Inflationary Pressures on Raw Materials

Global supply-chain disruptions and 2024–25 commodity cycles raised copper and aluminum prices by ~18–24% YoY and steel by ~12% in 2024, directly increasing HVACR component costs for Meier Tobler.

Economic shifts in China and EU manufacturing hubs cause episodic spikes, forcing potential pass-throughs; Swiss inflation (~2.3% in 2024) limits full price recovery.

Procurement must hedge and optimize sourcing while sales balance margin retention and competitiveness in Switzerland.

- Copper +18–24% (2024)

- Aluminum similar range

- Steel +12% (2024)

- Swiss CPI ~2.3% (2024)

Evolution of the Service Economy

The market is shifting toward heat-as-a-service and long-term maintenance, with global equipment-as-a-service revenue growing ~8% CAGR 2020–2024 and service contracts now representing ~30–40% of revenues for leading HVAC firms in 2024; this gives Meier Tobler more predictable recurring revenue and higher customer lifetime value.

Prioritizing service and maintenance reduces exposure to the new-build cycle, where Swiss construction starts fell ~5% in 2023, while service spending remained stable, cushioning cash flow and margin volatility.

- Recurring revenue share rises customer LTV; service margins typically 15–25% vs product 5–10%

- Heat-as-a-service demand growing ~6–9% annually in Europe (2022–2024)

- Service focus hedges against new-build cyclical downturns (Swiss starts -5% in 2023)

Margins squeezed as CHF strength, rising metals & wages meet weak construction demand

SNB rates steady ~1.75–2.00% (end-2025); construction investment down 3.5% (2023) impacting orderbooks; technician vacancy 3.5% (2024) and wages +4.2% pressuring margins; CHF appreciated +2.8% vs EUR (2024) easing import costs but FX volatility persists; copper +18–24%, aluminum +18–24%, steel +12% (2024); service revenue share 30–40%, service margins 15–25%.

| Metric | Value (latest) |

|---|---|

| SNB rates | 1.75–2.00% |

| Construction inv. | -3.5% (2023) |

| Technician vacancy | 3.5% (2024) |

| Wage growth | +4.2% (2024) |

| CHF vs EUR | +2.8% (2024) |

| Copper/Al/Steel | +18–24% / +18–24% / +12% (2024) |

| Service revenue share | 30–40% |

Preview Before You Purchase

Meier Tobler PESTLE Analysis

The preview shown here is the exact Meier Tobler PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the content, layout, and insights visible in this preview are identical to the downloadable file delivered immediately after payment.

What you see is the finished document—concise, actionable, and prepared for presentation or integration into your strategic planning.