Meijer Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

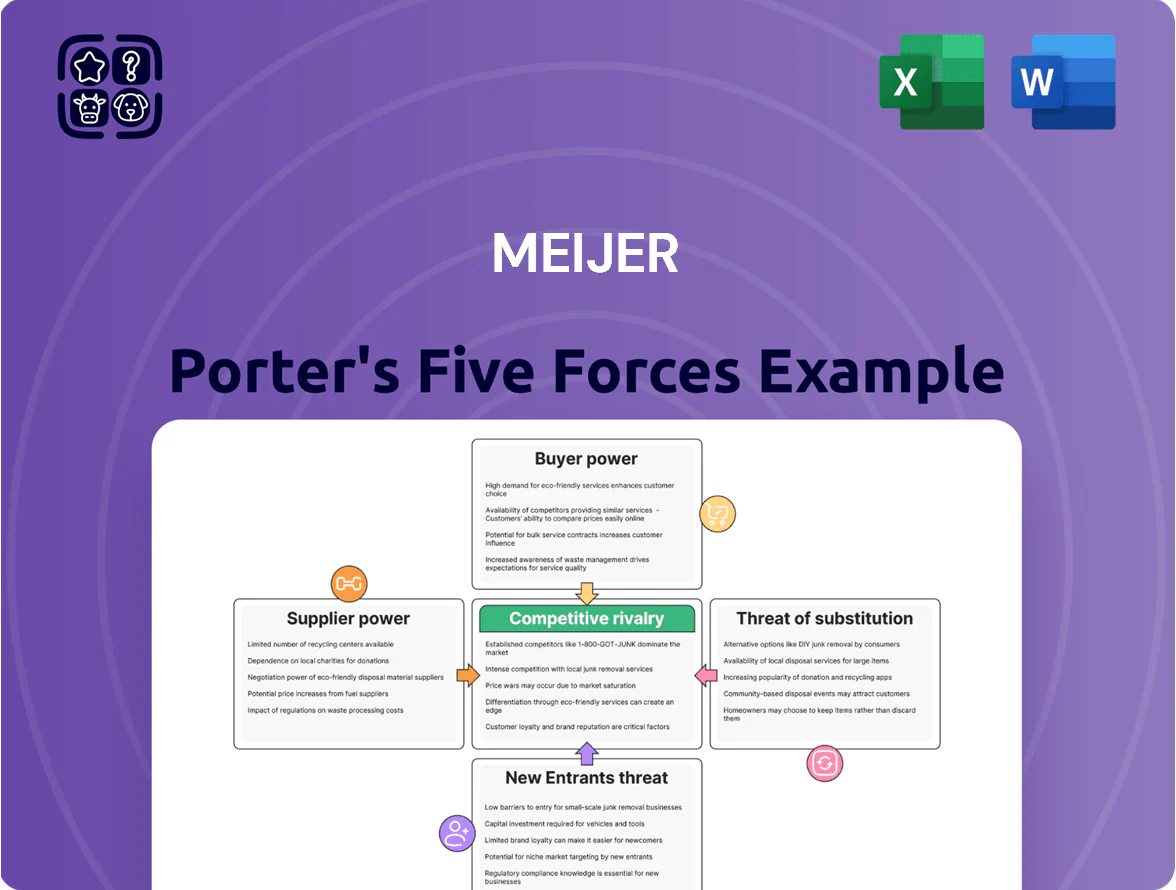

Meijer faces intense rivalry from national grocers and discounters, moderate supplier leverage due to private-label growth, rising buyer power via price transparency, manageable threat of new entrants, and evolving substitute threats from online retailers and meal-delivery services.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Meijer’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Dominance of Global Consumer Goods Giants

Large multinationals like Procter & Gamble and PepsiCo hold strong leverage with Meijer because their brands drive foot traffic; P&G and PepsiCo account for roughly 8–12% of unit sales in U.S. grocery categories, so Meijer needs them to be a one-stop supercenter for Midwestern families.

That reliance lets suppliers push for higher prices or paid shelf placement; NielsenIQ data show branded items capture about 60% of dollar sales in CPG, enabling suppliers to extract slotting fees or favorable margins during negotiations.

Expansion of Private Label Offerings

Meijer has expanded private-label sales to about 18% of grocery sales by 2024, cutting reliance on national brands and boosting gross margins—private label margins typically 4–8 percentage points higher than national brands. By offering higher-quality in-house alternatives and exclusive value lines, Meijer pressures suppliers to lower prices or co-develop products, shrinking suppliers’ leverage over shelf placement and promotional terms.

Regional Sourcing and Local Producer Leverage

Meijer sources heavily from Midwestern farms to appeal to community shoppers, supporting regional economies while creating a fragmented supplier base with lower bargaining power than national brands; in 2024 Meijer reported over $10 billion in grocery sales, letting it secure better pricing and payment terms from smaller producers. This scale gives Meijer leverage to negotiate volume discounts, faster pay cycles, and cooperative marketing, though dependency on local crops can raise supply variability risk.

Supply Chain Digitalization and Predictive Analytics

By end-2025 Meijer deploys AI-driven inventory giving real-time SKU movement and stock levels, cutting shrink and OOS (out-of-stock) rates; internal pilots report a 12% inventory carrying reduction and 8% waste drop year-on-year.

That visibility shortens reorder cycles and supports data-led bargaining—Meijer uses POS and forecast precision to demand tighter margins and service SLAs from suppliers.

Suppliers must meet Meijer digital standards (EDI/API, forecast sharing); non-compliant vendors risk delisting as 65% of Meijer volume flows through digitally integrated partners.

- 12% lower carrying costs

- 8% waste reduction

- 65% supplier volume digitally integrated

- Shorter reorder cycles → stronger negotiation leverage

Impact of Logistics and Commodity Fluctuations

Suppliers of fresh produce and meat face volatile fuel and input costs—fuel rose ~20% in 2023-24 and fertilizer prices spiked 15% in 2024—pressuring suppliers to push higher wholesale rates onto Meijer, though Meijer’s $11.5B grocery sales scale in 2024 and centralized procurement give it leverage to limit pass-throughs.

This creates recurring contract renegotiations and short-term price variance; suppliers seek flexible pricing clauses while Meijer demands volume discounts and category-specific caps, keeping margins contested.

- Fuel +20% (2023-24)

- Fertilizer +15% (2024)

- Meijer grocery sales $11.5B (2024)

- Frequent contract repricing, volume discounts enforced

Meijer gains supplier leverage via scale, AI cuts—yet input shocks keep renegotiations frequent

Suppliers hold moderate power: national brands (P&G, PepsiCo) drive traffic and can demand slotting/price concessions, but Meijer’s $11.5B grocery scale (2024), 18% private-label mix, regional sourcing, and 65% supplier digital integration shift leverage to Meijer; AI-driven inventory cut carrying costs 12% and waste 8%, enabling tougher margin and SLA demands while fresh-produce input shocks (fuel +20% 2023–24; fertilizer +15% 2024) keep renegotiations frequent.

| Metric | Value |

|---|---|

| Meijer grocery sales (2024) | $11.5B |

| Private-label mix (2024) | 18% |

| Supplier digital integration | 65% |

| Inventory carrying reduction (pilot) | 12% |

| Waste reduction (pilot) | 8% |

| Fuel change (2023–24) | +20% |

| Fertilizer change (2024) | +15% |

What is included in the product

Uncovers key drivers of competition, customer influence, supplier power, and market entry risks tailored to Meijer, identifying disruptive substitutes and strategic levers that affect pricing, profitability, and market share.

One-sheet Porter's Five Forces for Meijer—fast visibility into supplier, buyer, and competitive pressures to guide pricing and expansion decisions.

Customers Bargaining Power

Low Switching Costs for Grocery and General Goods

Consumers in the Midwest face many options—from independent grocers to Walmart and Kroger—so switching is easy; 2024 Nielsen data shows 43% of U.S. grocery shoppers visited three or more chains monthly. With no contracts or lock-in, Meijer must keep prices, private-label share (now ~18% company-wide in 2023) and service competitive to avoid churn. That ease of switching gives customers high bargaining power as they hunt lower prices and promotions.

High Price Sensitivity in a Post-Inflationary Market

By late 2025 Meijer faces high customer price sensitivity: 72% of US grocery shoppers say price transparency drives purchase decisions, per 2025 IRI data, and inflation normalization left consumers hunting value. Shoppers use mobile apps—36% compare prices in-store in 2025 according to NielsenIQ—forcing Meijer to match or undercut rivals in real time. Meijer responds with frequent promotions, loyalty-only discounts, and price-match policies; these tactics protect share but compress gross margins by an estimated 40–80 basis points.

Digital Integration and mPerks Loyalty Program

The mPerks loyalty program reduces customer bargaining power by driving repeat visits with personalized digital rewards; as of 2024 Meijer reported over 5 million active mPerks users, boosting basket frequency by about 8% year-over-year. By collecting purchase data and preferences, Meijer tailors coupons and assortments, increasing relevance and "stickiness" so shoppers are less likely to switch for a single trip. This data-driven targeting improves retention and raises the cost of defection for customers.

Demand for One-Stop Shopping Convenience

The Meijer hybrid supercenter model bundles groceries, pharmacy, and general merchandise, matching busy families’ demand for one-stop shopping and reducing customer bargaining power by creating a convenience premium few niche retailers can offer.

Still, consumers expect high service across departments; Meijer reported 2024 same-store sales growth of about 2.5% and pharmacy volumes up ~3%, so service lapses would quickly erode that convenience advantage.

- Convenience premium reduces price-only bargaining

- 2024 same-store sales +2.5%, pharmacy +3%

- High service levels required across categories

Influence of Online Reviews and Social Media

- 72% of shoppers use reviews

- 24-hour responses cut damage ~30%

- Viral hits can move same-store sales by low single digits

Price‑savvy shoppers force Meijer promotions, trimming margins 40–80 bps

Customers hold high bargaining power: easy switching (43% visit 3+ chains, 2024 Nielsen), price-sensitivity (72% value price transparency, 2025 IRI), and in-store price checks (36%, 2025 NielsenIQ) force Meijer into promotions that cut gross margins ~40–80 bps; mPerks (5M users, 2024) and supercenter convenience blunt but don't eliminate this pressure.

| Metric | Value |

|---|---|

| Multi-chain shoppers (2024) | 43% |

| Price transparency importance (2025) | 72% |

| In-store price checks (2025) | 36% |

| mPerks users (2024) | 5M |

| Margin compression | 40–80 bps |

What You See Is What You Get

Meijer Porter's Five Forces Analysis

This preview shows the exact Meijer Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups—fully formatted and ready for use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

Meijer faces intense rivalry from national grocers and discounters, moderate supplier leverage due to private-label growth, rising buyer power via price transparency, manageable threat of new entrants, and evolving substitute threats from online retailers and meal-delivery services.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Meijer’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Dominance of Global Consumer Goods Giants

Large multinationals like Procter & Gamble and PepsiCo hold strong leverage with Meijer because their brands drive foot traffic; P&G and PepsiCo account for roughly 8–12% of unit sales in U.S. grocery categories, so Meijer needs them to be a one-stop supercenter for Midwestern families.

That reliance lets suppliers push for higher prices or paid shelf placement; NielsenIQ data show branded items capture about 60% of dollar sales in CPG, enabling suppliers to extract slotting fees or favorable margins during negotiations.

Expansion of Private Label Offerings

Meijer has expanded private-label sales to about 18% of grocery sales by 2024, cutting reliance on national brands and boosting gross margins—private label margins typically 4–8 percentage points higher than national brands. By offering higher-quality in-house alternatives and exclusive value lines, Meijer pressures suppliers to lower prices or co-develop products, shrinking suppliers’ leverage over shelf placement and promotional terms.

Regional Sourcing and Local Producer Leverage

Meijer sources heavily from Midwestern farms to appeal to community shoppers, supporting regional economies while creating a fragmented supplier base with lower bargaining power than national brands; in 2024 Meijer reported over $10 billion in grocery sales, letting it secure better pricing and payment terms from smaller producers. This scale gives Meijer leverage to negotiate volume discounts, faster pay cycles, and cooperative marketing, though dependency on local crops can raise supply variability risk.

Supply Chain Digitalization and Predictive Analytics

By end-2025 Meijer deploys AI-driven inventory giving real-time SKU movement and stock levels, cutting shrink and OOS (out-of-stock) rates; internal pilots report a 12% inventory carrying reduction and 8% waste drop year-on-year.

That visibility shortens reorder cycles and supports data-led bargaining—Meijer uses POS and forecast precision to demand tighter margins and service SLAs from suppliers.

Suppliers must meet Meijer digital standards (EDI/API, forecast sharing); non-compliant vendors risk delisting as 65% of Meijer volume flows through digitally integrated partners.

- 12% lower carrying costs

- 8% waste reduction

- 65% supplier volume digitally integrated

- Shorter reorder cycles → stronger negotiation leverage

Impact of Logistics and Commodity Fluctuations

Suppliers of fresh produce and meat face volatile fuel and input costs—fuel rose ~20% in 2023-24 and fertilizer prices spiked 15% in 2024—pressuring suppliers to push higher wholesale rates onto Meijer, though Meijer’s $11.5B grocery sales scale in 2024 and centralized procurement give it leverage to limit pass-throughs.

This creates recurring contract renegotiations and short-term price variance; suppliers seek flexible pricing clauses while Meijer demands volume discounts and category-specific caps, keeping margins contested.

- Fuel +20% (2023-24)

- Fertilizer +15% (2024)

- Meijer grocery sales $11.5B (2024)

- Frequent contract repricing, volume discounts enforced

Meijer gains supplier leverage via scale, AI cuts—yet input shocks keep renegotiations frequent

Suppliers hold moderate power: national brands (P&G, PepsiCo) drive traffic and can demand slotting/price concessions, but Meijer’s $11.5B grocery scale (2024), 18% private-label mix, regional sourcing, and 65% supplier digital integration shift leverage to Meijer; AI-driven inventory cut carrying costs 12% and waste 8%, enabling tougher margin and SLA demands while fresh-produce input shocks (fuel +20% 2023–24; fertilizer +15% 2024) keep renegotiations frequent.

| Metric | Value |

|---|---|

| Meijer grocery sales (2024) | $11.5B |

| Private-label mix (2024) | 18% |

| Supplier digital integration | 65% |

| Inventory carrying reduction (pilot) | 12% |

| Waste reduction (pilot) | 8% |

| Fuel change (2023–24) | +20% |

| Fertilizer change (2024) | +15% |

What is included in the product

Uncovers key drivers of competition, customer influence, supplier power, and market entry risks tailored to Meijer, identifying disruptive substitutes and strategic levers that affect pricing, profitability, and market share.

One-sheet Porter's Five Forces for Meijer—fast visibility into supplier, buyer, and competitive pressures to guide pricing and expansion decisions.

Customers Bargaining Power

Low Switching Costs for Grocery and General Goods

Consumers in the Midwest face many options—from independent grocers to Walmart and Kroger—so switching is easy; 2024 Nielsen data shows 43% of U.S. grocery shoppers visited three or more chains monthly. With no contracts or lock-in, Meijer must keep prices, private-label share (now ~18% company-wide in 2023) and service competitive to avoid churn. That ease of switching gives customers high bargaining power as they hunt lower prices and promotions.

High Price Sensitivity in a Post-Inflationary Market

By late 2025 Meijer faces high customer price sensitivity: 72% of US grocery shoppers say price transparency drives purchase decisions, per 2025 IRI data, and inflation normalization left consumers hunting value. Shoppers use mobile apps—36% compare prices in-store in 2025 according to NielsenIQ—forcing Meijer to match or undercut rivals in real time. Meijer responds with frequent promotions, loyalty-only discounts, and price-match policies; these tactics protect share but compress gross margins by an estimated 40–80 basis points.

Digital Integration and mPerks Loyalty Program

The mPerks loyalty program reduces customer bargaining power by driving repeat visits with personalized digital rewards; as of 2024 Meijer reported over 5 million active mPerks users, boosting basket frequency by about 8% year-over-year. By collecting purchase data and preferences, Meijer tailors coupons and assortments, increasing relevance and "stickiness" so shoppers are less likely to switch for a single trip. This data-driven targeting improves retention and raises the cost of defection for customers.

Demand for One-Stop Shopping Convenience

The Meijer hybrid supercenter model bundles groceries, pharmacy, and general merchandise, matching busy families’ demand for one-stop shopping and reducing customer bargaining power by creating a convenience premium few niche retailers can offer.

Still, consumers expect high service across departments; Meijer reported 2024 same-store sales growth of about 2.5% and pharmacy volumes up ~3%, so service lapses would quickly erode that convenience advantage.

- Convenience premium reduces price-only bargaining

- 2024 same-store sales +2.5%, pharmacy +3%

- High service levels required across categories

Influence of Online Reviews and Social Media

- 72% of shoppers use reviews

- 24-hour responses cut damage ~30%

- Viral hits can move same-store sales by low single digits

Price‑savvy shoppers force Meijer promotions, trimming margins 40–80 bps

Customers hold high bargaining power: easy switching (43% visit 3+ chains, 2024 Nielsen), price-sensitivity (72% value price transparency, 2025 IRI), and in-store price checks (36%, 2025 NielsenIQ) force Meijer into promotions that cut gross margins ~40–80 bps; mPerks (5M users, 2024) and supercenter convenience blunt but don't eliminate this pressure.

| Metric | Value |

|---|---|

| Multi-chain shoppers (2024) | 43% |

| Price transparency importance (2025) | 72% |

| In-store price checks (2025) | 36% |

| mPerks users (2024) | 5M |

| Margin compression | 40–80 bps |

What You See Is What You Get

Meijer Porter's Five Forces Analysis

This preview shows the exact Meijer Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups—fully formatted and ready for use.