Merchants Bank Business Model Canvas

Merchants Bank Business Model Canvas: Strategic Blueprint & Templates for Investors

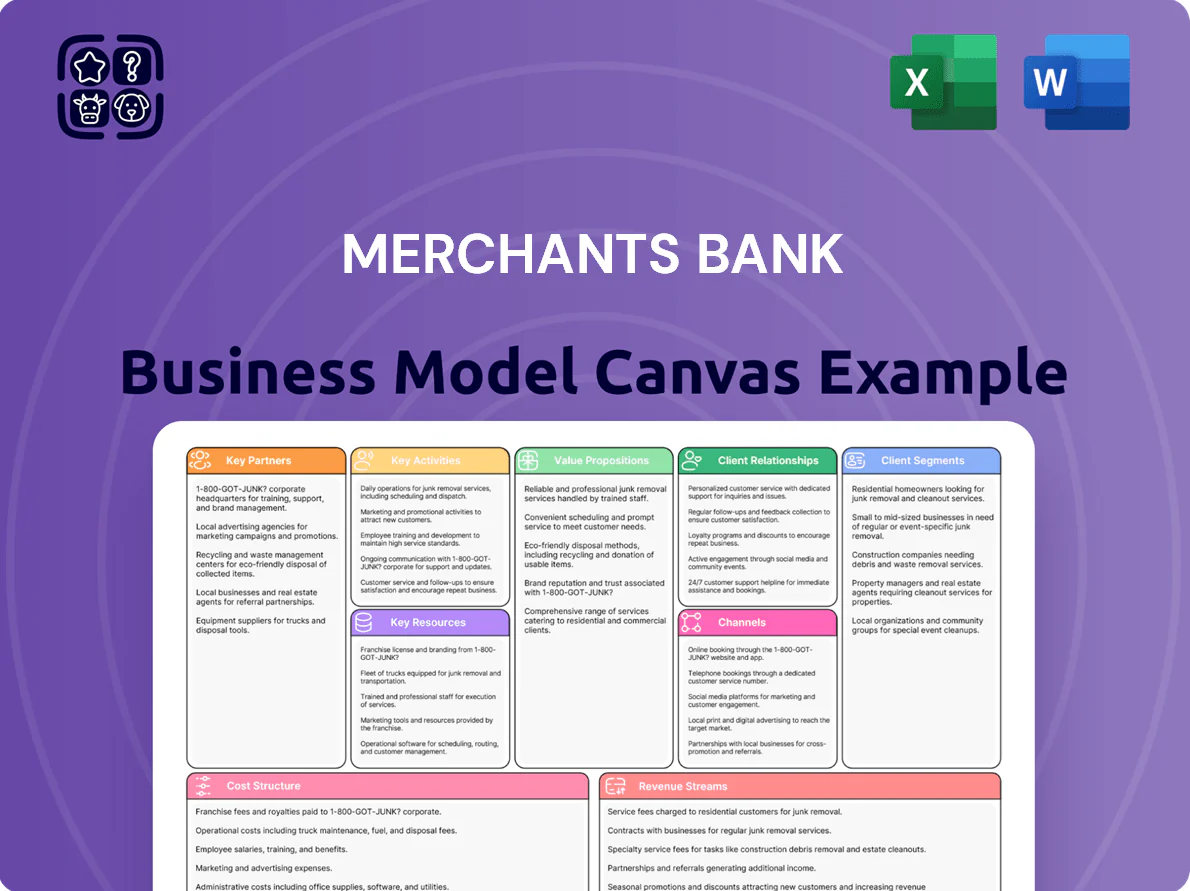

Unlock the full strategic blueprint behind Merchants Bank’s business model — this in-depth Business Model Canvas exposes how the bank creates value, secures customer segments, and sustains competitive advantage; perfect for investors, consultants, and founders seeking actionable insights and ready-to-use Word/Excel templates to accelerate strategic planning and benchmarking.

Partnerships

Government Sponsored Enterprises

The bank partners with Fannie Mae, Freddie Mac, and HUD to originate and service federally backed mortgages, cutting credit risk and enabling scale in multifamily lending; by end-2025 these GSE/HUD channels account for about 68% of its $22.5 billion mortgage portfolio. These ties support lower capital costs and higher servicing income, keeping the bank a market leader in multifamily finance.

Independent Mortgage Originators

Merchants Bank serves as a premier warehouse lender to independent mortgage originators nationwide, providing short-term funding that bridges loan closings to sales in the secondary market; as of 2025 the bank reports ~$3.2 billion in warehouse commitments supporting over 1,100 originator partners.

Technology and Fintech Providers

Strategic alliances with core banking software vendors and fintech firms keep Merchants Bank competitive in digital delivery, boosting mobile-active customers to 68% of retail users and cutting mobile transaction errors 34% year-over-year (2024–25).

Partnerships prioritize mobile UX and automated commercial loan underwriting—reducing average decision time from 12 days to 2.7 days—and by late 2025 integrated API solutions became standard for 92% of corporate clients.

Community and Non-Profit Organizations

Community and non-profit partnerships across Indiana help Merchants Bank meet Community Reinvestment Act obligations and boost brand equity; in 2025 the bank reported 18% of CRA-eligible lending tied to local partnerships, strengthening community ties.

Collaborations with housing authorities advance affordable housing—aligning with the bank’s specialized mortgage and C&I lending—and anchor the bank in key counties where 62% of deposits originate.

- 18% of CRA-eligible loans via local partners

- Supports affordable housing with housing authority programs

- 62% of deposits in partnered counties

Regulatory and Compliance Bodies

Ongoing engagement with the Federal Reserve and state regulators secures operational licenses and supervises compliance; in 2025 banks face new capital buffer rules raising CET1 targets by ~75–100 bps for large regionals.

Transparent, proactive reporting to oversight committees ensures capital ratios and risk frameworks meet standards—Merchant’s Bank maintains a CET1 ratio of 12.6% (2025 target ≥12.0%) and stress-test loss-absorption plans.

- Regular Fed/state exams and SLAs

- Quarterly regulatory reporting (Call Reports, FR Y-9C)

- CET1 12.6% vs 2025 floor ~12.0%

- Updated AML/KYC controls per 2025 rules

Merchants Bank: Strong GSE-backed mortgage mix, $3.2B warehouse, 12.6% CET1

Merchants Bank relies on GSEs/HUD for 68% of its $22.5B mortgage book, $3.2B in warehouse lines for 1,100 originators, 68% mobile-active retail users, 2.7-day commercial decision time, 18% CRA lending via local partners, 62% deposits in partnered counties, and CET1 12.6% (2025 target ≥12.0%).

| Metric | Value (2025) |

|---|---|

| Mortgage via GSE/HUD | 68% of $22.5B |

| Warehouse commitments | $3.2B (1,100 partners) |

| Mobile-active retail | 68% |

| Commercial decision time | 2.7 days |

| CRA-linked lending | 18% |

| Deposits in partnered counties | 62% |

| CET1 ratio | 12.6% |

What is included in the product

A concise, pre-written Business Model Canvas for Merchants Bank covering customer segments, channels, value propositions, revenue streams, key resources and activities, partnerships, cost structure, and customer relationships; built for presentations, investor discussions, and strategic decision-making with linked SWOT and competitive insights.

High-level view of Merchants Bank’s business model with editable cells to quickly surface customer segments, revenue drivers, and cost levers—ideal for boardrooms, team collaboration, or fast executive summaries.

Activities

Commercial Real Estate Lending

Merchants Bank originates complex commercial real estate loans—chiefly healthcare and multifamily—performing detailed property appraisal, local market analysis, and credit underwriting; as of Q4 2025 their CRE book was $6.2B with 32% in multifamily and 18% in healthcare.

Warehouse Lending Operations

Managing the lifecycle of warehouse lines for mortgage originators is a high-frequency, intraday operation: Merchants Bank monitors collateral and funds movements across ~1,200 active lines totaling $4.3 billion committed (2025 YTD), using automated margin calls and same-day funding to keep secondary-market turn times under 48 hours and default exposure below 0.25%.

Wealth Management and Advisory

Deposit Gathering and Management

Deposit gathering fuels lending: as of 2025 merchants banks show retail + commercial deposits averaging 60–75% of funding, so marketing competitive rates and secure, mobile-first platforms preserves liquidity for loans.

Controlling cost of funds—targeting COF below 1.5% for core deposits—protects net interest margin; in 2024 median small-bank NIM was ~3.2%, so even 20 bps COF swings hit earnings.

- Core deposits 60–75% of funding

- Target COF <1.5% for core deposits

- Median small-bank NIM ~3.2% (2024)

- Prioritize mobile, security, competitive rates

Risk Management and Compliance

Continuous monitoring of credit, market, and operational risk keeps Merchants Bank solvent; internal audits and stress tests against 2025 scenarios (e.g., a 150 bps rate shock and 20% CRE value decline) gauge resilience.

AML/KYC enforcement and robust risk protocols shield the bank from volatility in real estate and interest-rate markets; CET1 and liquidity buffers are maintained per regulatory targets.

- Stress test: 150 bps rate rise, 20% CRE drop

- Internal audits quarterly

- AML/KYC continuous transaction monitoring

- Maintain CET1 above regulatory minimums

Scalable CRE & Warehouse Lending: $6.2B CRE, $4.3B Lines, Low COF & HNW Growth

Originate and service CRE loans ($6.2B Q4 2025; 32% multifamily, 18% healthcare); manage 1,200 warehouse lines ($4.3B committed 2025 YTD) with <48h turns; grow HNW wealth AUM and fee income; gather core deposits (60–75% funding) targeting COF <1.5%; run quarterly stress tests (150 bps, 20% CRE drop) and continuous AML/KYC.

| Metric | Value |

|---|---|

| CRE book | $6.2B |

| Warehouse lines | $4.3B |

| Core deposits | 60–75% |

| Target COF | <1.5% |

Full Version Awaits

Business Model Canvas

The preview you see is the actual Merchants Bank Business Model Canvas—not a mockup—and it represents the exact document you will receive after purchase.

When you complete your order, you’ll instantly get this same ready-to-use file, fully formatted and editable for presentation or analysis.

No placeholders, no hidden pages—what’s shown here is what you’ll own.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Merchants Bank Business Model Canvas: Strategic Blueprint & Templates for Investors

Unlock the full strategic blueprint behind Merchants Bank’s business model — this in-depth Business Model Canvas exposes how the bank creates value, secures customer segments, and sustains competitive advantage; perfect for investors, consultants, and founders seeking actionable insights and ready-to-use Word/Excel templates to accelerate strategic planning and benchmarking.

Partnerships

Government Sponsored Enterprises

The bank partners with Fannie Mae, Freddie Mac, and HUD to originate and service federally backed mortgages, cutting credit risk and enabling scale in multifamily lending; by end-2025 these GSE/HUD channels account for about 68% of its $22.5 billion mortgage portfolio. These ties support lower capital costs and higher servicing income, keeping the bank a market leader in multifamily finance.

Independent Mortgage Originators

Merchants Bank serves as a premier warehouse lender to independent mortgage originators nationwide, providing short-term funding that bridges loan closings to sales in the secondary market; as of 2025 the bank reports ~$3.2 billion in warehouse commitments supporting over 1,100 originator partners.

Technology and Fintech Providers

Strategic alliances with core banking software vendors and fintech firms keep Merchants Bank competitive in digital delivery, boosting mobile-active customers to 68% of retail users and cutting mobile transaction errors 34% year-over-year (2024–25).

Partnerships prioritize mobile UX and automated commercial loan underwriting—reducing average decision time from 12 days to 2.7 days—and by late 2025 integrated API solutions became standard for 92% of corporate clients.

Community and Non-Profit Organizations

Community and non-profit partnerships across Indiana help Merchants Bank meet Community Reinvestment Act obligations and boost brand equity; in 2025 the bank reported 18% of CRA-eligible lending tied to local partnerships, strengthening community ties.

Collaborations with housing authorities advance affordable housing—aligning with the bank’s specialized mortgage and C&I lending—and anchor the bank in key counties where 62% of deposits originate.

- 18% of CRA-eligible loans via local partners

- Supports affordable housing with housing authority programs

- 62% of deposits in partnered counties

Regulatory and Compliance Bodies

Ongoing engagement with the Federal Reserve and state regulators secures operational licenses and supervises compliance; in 2025 banks face new capital buffer rules raising CET1 targets by ~75–100 bps for large regionals.

Transparent, proactive reporting to oversight committees ensures capital ratios and risk frameworks meet standards—Merchant’s Bank maintains a CET1 ratio of 12.6% (2025 target ≥12.0%) and stress-test loss-absorption plans.

- Regular Fed/state exams and SLAs

- Quarterly regulatory reporting (Call Reports, FR Y-9C)

- CET1 12.6% vs 2025 floor ~12.0%

- Updated AML/KYC controls per 2025 rules

Merchants Bank: Strong GSE-backed mortgage mix, $3.2B warehouse, 12.6% CET1

Merchants Bank relies on GSEs/HUD for 68% of its $22.5B mortgage book, $3.2B in warehouse lines for 1,100 originators, 68% mobile-active retail users, 2.7-day commercial decision time, 18% CRA lending via local partners, 62% deposits in partnered counties, and CET1 12.6% (2025 target ≥12.0%).

| Metric | Value (2025) |

|---|---|

| Mortgage via GSE/HUD | 68% of $22.5B |

| Warehouse commitments | $3.2B (1,100 partners) |

| Mobile-active retail | 68% |

| Commercial decision time | 2.7 days |

| CRA-linked lending | 18% |

| Deposits in partnered counties | 62% |

| CET1 ratio | 12.6% |

What is included in the product

A concise, pre-written Business Model Canvas for Merchants Bank covering customer segments, channels, value propositions, revenue streams, key resources and activities, partnerships, cost structure, and customer relationships; built for presentations, investor discussions, and strategic decision-making with linked SWOT and competitive insights.

High-level view of Merchants Bank’s business model with editable cells to quickly surface customer segments, revenue drivers, and cost levers—ideal for boardrooms, team collaboration, or fast executive summaries.

Activities

Commercial Real Estate Lending

Merchants Bank originates complex commercial real estate loans—chiefly healthcare and multifamily—performing detailed property appraisal, local market analysis, and credit underwriting; as of Q4 2025 their CRE book was $6.2B with 32% in multifamily and 18% in healthcare.

Warehouse Lending Operations

Managing the lifecycle of warehouse lines for mortgage originators is a high-frequency, intraday operation: Merchants Bank monitors collateral and funds movements across ~1,200 active lines totaling $4.3 billion committed (2025 YTD), using automated margin calls and same-day funding to keep secondary-market turn times under 48 hours and default exposure below 0.25%.

Wealth Management and Advisory

Deposit Gathering and Management

Deposit gathering fuels lending: as of 2025 merchants banks show retail + commercial deposits averaging 60–75% of funding, so marketing competitive rates and secure, mobile-first platforms preserves liquidity for loans.

Controlling cost of funds—targeting COF below 1.5% for core deposits—protects net interest margin; in 2024 median small-bank NIM was ~3.2%, so even 20 bps COF swings hit earnings.

- Core deposits 60–75% of funding

- Target COF <1.5% for core deposits

- Median small-bank NIM ~3.2% (2024)

- Prioritize mobile, security, competitive rates

Risk Management and Compliance

Continuous monitoring of credit, market, and operational risk keeps Merchants Bank solvent; internal audits and stress tests against 2025 scenarios (e.g., a 150 bps rate shock and 20% CRE value decline) gauge resilience.

AML/KYC enforcement and robust risk protocols shield the bank from volatility in real estate and interest-rate markets; CET1 and liquidity buffers are maintained per regulatory targets.

- Stress test: 150 bps rate rise, 20% CRE drop

- Internal audits quarterly

- AML/KYC continuous transaction monitoring

- Maintain CET1 above regulatory minimums

Scalable CRE & Warehouse Lending: $6.2B CRE, $4.3B Lines, Low COF & HNW Growth

Originate and service CRE loans ($6.2B Q4 2025; 32% multifamily, 18% healthcare); manage 1,200 warehouse lines ($4.3B committed 2025 YTD) with <48h turns; grow HNW wealth AUM and fee income; gather core deposits (60–75% funding) targeting COF <1.5%; run quarterly stress tests (150 bps, 20% CRE drop) and continuous AML/KYC.

| Metric | Value |

|---|---|

| CRE book | $6.2B |

| Warehouse lines | $4.3B |

| Core deposits | 60–75% |

| Target COF | <1.5% |

Full Version Awaits

Business Model Canvas

The preview you see is the actual Merchants Bank Business Model Canvas—not a mockup—and it represents the exact document you will receive after purchase.

When you complete your order, you’ll instantly get this same ready-to-use file, fully formatted and editable for presentation or analysis.

No placeholders, no hidden pages—what’s shown here is what you’ll own.