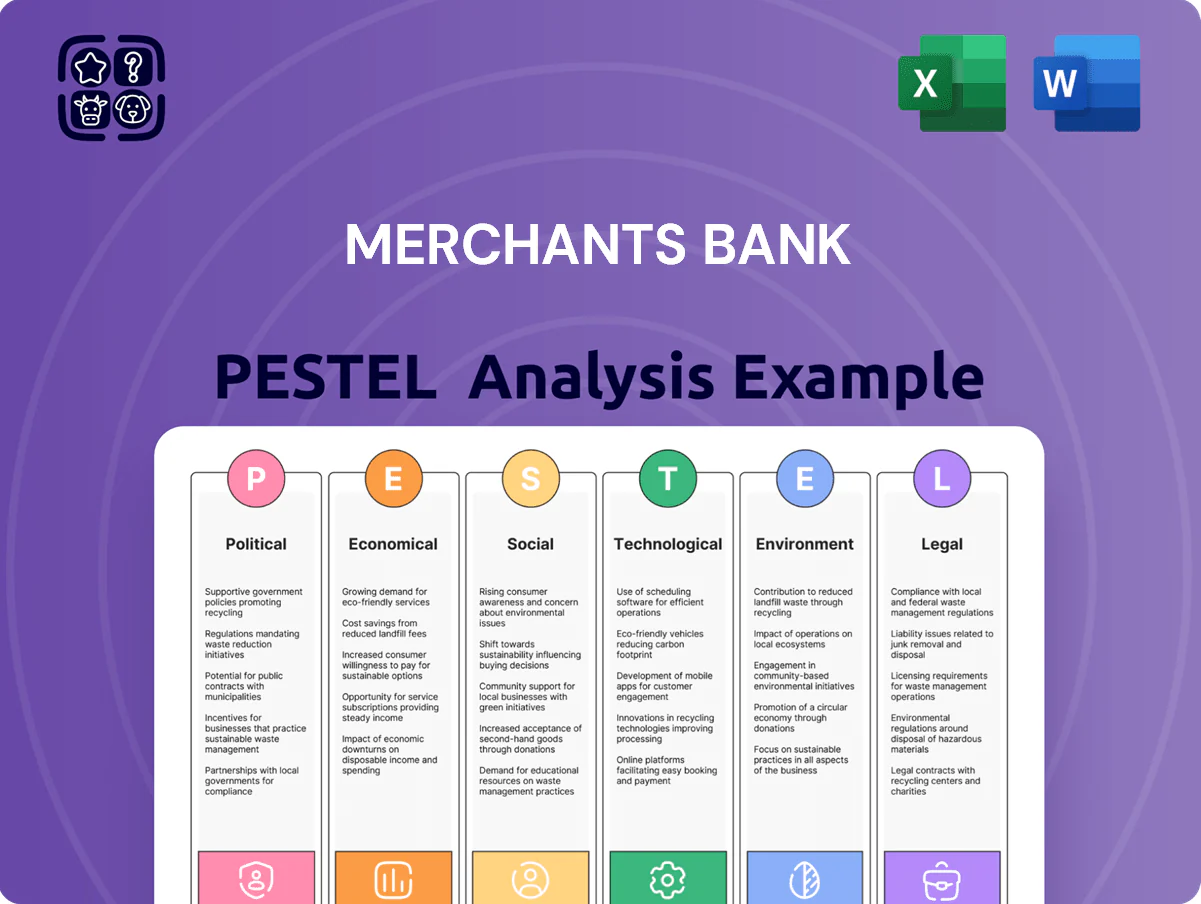

Merchants Bank PESTLE Analysis

Your Competitive Advantage Starts with This Report

Discover how political shifts, economic cycles, and technological disruption are reshaping Merchants Bank’s strategic landscape—our concise PESTLE snapshot highlights the critical external forces you need to watch. Purchase the full PESTLE analysis to unlock in-depth risk assessments, regulatory impacts, and actionable opportunities tailored for investors and strategists. Get the complete, ready-to-use report now and make smarter decisions faster.

Political factors

Federal Housing Policy Evolution

As of late 2025, federal initiatives boosting affordable housing—including a $65 billion low-income housing tax credit expansion and $20 billion in targeted HUD grants—have opened lending opportunities for Merchants Bank’s commercial real estate division, particularly in multi-family projects where demand rose 8% year-over-year.

Post-Election Regulatory Landscape

The post-election regulatory shift after late 2024 has driven 2025 legislation increasing transparency and raising capital buffer expectations for mid-sized banks; regulators now target a 2.0–3.0 percentage-point higher CET1 buffer for lenders with >25% real estate exposure.

Merchants Bank, with 28% CRE concentration and $3.4bn loans, must intensify policy advocacy to mitigate disproportionate impacts on lending capacity and capital ratios.

Local Government Infrastructure Investment

Indiana’s stable state politics and FY2025 $1.6B infrastructure plan support regional growth, benefiting banks like Merchants by expanding commercial lending opportunities.

Local government grants and over 200 active tax increment financing districts in Indiana drive developer demand for construction loans, deposits, and treasury services that Merchants offers.

Keeping close ties with county economic development offices and attending municipal bond financings helps Merchants anticipate new hubs—15 major projects awarded in 2024 across the state.

Geopolitical Impact on Capital Markets

Global political tensions, including 2024–25 Middle East and Ukraine conflicts, have pushed US 10-year treasury yield volatility to a realized annualized 18% in 2025, raising banks' cost of funds and dampening demand for mortgage-backed securities.

Merchants Bank, though domestic, faces margin pressure as sudden treasury moves altered 30-year mortgage spreads by ~40bps in Q4 2024, affecting loan pricing and hedging costs.

Strategic plans must model external shocks to protect net interest margin and secondary-market liquidity, using stress tests reflecting 50–100bp treasury shocks observed in 2024.

- 10y yield realized vol ~18% (2025)

- 30y mortgage spreads widened ~40bps (Q4 2024)

- Stress scenarios: 50–100bps treasury moves

Tax Policy and Real Estate Incentives

Changes in federal corporate tax rates and the 2023-2025 IRS guidance on bonus depreciation shifts affect Merchants Bank strategic planning, as 21% corporate tax norms and potential capital gains rate adjustments influence lending demand in CRE sectors.

Modifications to depreciation schedules or capital gains treatment can alter client ROI calculations—90% of the bank’s CRE portfolio decisions hinge on tax-affected cash flow projections.

The bank must scale advisory services, leveraging tax specialists to optimize client structures and preserve its own effective tax rate, aiming to limit tax-driven margin erosion.

- Federal corporate tax baseline ~21%

- Bonus depreciation changes impact CRE ROI

- ~90% of CRE lending sensitive to tax shifts

- Need for expanded tax advisory capabilities

Merchants Bank Faces CRE Pressure, Policy Shifts Demand Stronger Advocacy & Tax Planning

Federal housing incentives and heightened post-2024 bank capital rules pressure Merchants Bank’s CRE-heavy balance sheet, while Indiana infrastructure and TIF activity boost local lending; geopolitical-driven treasury volatility (10y vol ~18%, 30y spread +40bps) and tax policy shifts (corporate rate ~21%, bonus depreciation changes) necessitate stronger advocacy, stress-testing, and tax advisory to protect margins.

| Metric | Value |

|---|---|

| CRE concentration | 28% |

| 10y vol (2025) | ~18% |

| 30y spread change | +40bps (Q4 2024) |

| Corporate tax baseline | ~21% |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely impact Merchants Bank, combining data-driven trends and region-specific regulations to identify strategic threats and opportunities for executives, investors, and consultants.

A concise, visually segmented PESTLE summary for Merchants Bank that streamlines external risk assessment and market positioning, ready to drop into presentations or share across teams for faster, aligned strategy discussions.

Economic factors

Interest Rate Stabilization and Strategy

By end-2025, central bank rates stabilized around 4.25%–4.50%, giving Merchants Bank clearer pricing for long-term loans and deposits and reducing hedging costs by an estimated 15% versus 2023–24 volatility.

This predictability enables refined mortgage origination—projected 8% YoY growth in fixed-rate originations—as the bank reallocates from short-term repricing products.

Still, a prolonged high-rate environment risks tipping GDP growth toward 0.5%–1.0% in stress scenarios, requiring conservative credit buffers and tighter underwriting.

Multi-family Real Estate Market Health

The multi-family housing sector underpins Merchants Bank’s asset growth; U.S. apartment vacancy in Q4 2025 averaged 5.6% while Midwest metros like Cleveland and Columbus saw vacancies of 6.2% and 5.9%, signaling localized oversupply that could weigh on occupancy and loan performance.

Inflationary Pressures on Operational Costs

Persistent inflation, with US core PCE at 3.8% in 2024 and CPI averaging 3.4%, raised Merchants Bank non-interest costs—notably a 6–8% rise in labor and 10%+ increases in tech procurement—pressuring margins.

Regional Economic Diversification in Indiana

Indiana's shift toward tech and advanced manufacturing—with manufacturing contributing about 18% of state GDP and tech employment growing roughly 12% from 2019–2024—expands Merchants Bank's pool of commercial clients beyond traditional real estate borrowers.

As regional firms scale, the bank can grow wealth management and business banking revenues; diversifying client sectors reduces concentration risk and strengthens capital and liquidity resilience.

- Manufacturing ~18% of GDP

- Tech employment +12% (2019–2024)

- Lower industry concentration risk

- Opportunity to increase non-RE loan and fee income

Mortgage Market Recovery Trends

The U.S. residential mortgage market shows gradual recovery: origination volume rose 12% year-over-year in 2024 as rates eased from 2023 peaks, though affordability remains strained with median home prices still ~8% above pre-pandemic levels.

Merchants Bank’s mortgage division should target first-time buyers and refinancers with tailored low-down-payment and rate-buydown products while sustaining sub-30-day processing and pricing within 25–50 bps of market to win share.

- Origination +12% YoY (2024)

- Median home price +8% vs 2019

- Processing target: <30 days

- Pricing gap: 25–50 bps

Stable 2025 rates cut hedging costs, boost originations; inflation squeezes margins

Stable 2025 rates (4.25–4.50%) cut hedging costs ~15% vs 2023–24; fixed-rate mortgage originations projected +8% YoY; core PCE 3.8% (2024) and CPI 3.4% raised labor/tech costs 6–10% squeezing margins; U.S. origination +12% YoY (2024); Indiana manufacturing ~18% GDP, tech jobs +12% (2019–24) diversifies loan mix and fee income.

| Metric | Value |

|---|---|

| Policy rate (2025) | 4.25–4.50% |

| Core PCE (2024) | 3.8% |

| Mortgage originations (2024) | +12% YoY |

| Indiana manufacturing | ~18% GDP |

Same Document Delivered

Merchants Bank PESTLE Analysis

The preview shown here is the exact Merchants Bank PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Competitive Advantage Starts with This Report

Discover how political shifts, economic cycles, and technological disruption are reshaping Merchants Bank’s strategic landscape—our concise PESTLE snapshot highlights the critical external forces you need to watch. Purchase the full PESTLE analysis to unlock in-depth risk assessments, regulatory impacts, and actionable opportunities tailored for investors and strategists. Get the complete, ready-to-use report now and make smarter decisions faster.

Political factors

Federal Housing Policy Evolution

As of late 2025, federal initiatives boosting affordable housing—including a $65 billion low-income housing tax credit expansion and $20 billion in targeted HUD grants—have opened lending opportunities for Merchants Bank’s commercial real estate division, particularly in multi-family projects where demand rose 8% year-over-year.

Post-Election Regulatory Landscape

The post-election regulatory shift after late 2024 has driven 2025 legislation increasing transparency and raising capital buffer expectations for mid-sized banks; regulators now target a 2.0–3.0 percentage-point higher CET1 buffer for lenders with >25% real estate exposure.

Merchants Bank, with 28% CRE concentration and $3.4bn loans, must intensify policy advocacy to mitigate disproportionate impacts on lending capacity and capital ratios.

Local Government Infrastructure Investment

Indiana’s stable state politics and FY2025 $1.6B infrastructure plan support regional growth, benefiting banks like Merchants by expanding commercial lending opportunities.

Local government grants and over 200 active tax increment financing districts in Indiana drive developer demand for construction loans, deposits, and treasury services that Merchants offers.

Keeping close ties with county economic development offices and attending municipal bond financings helps Merchants anticipate new hubs—15 major projects awarded in 2024 across the state.

Geopolitical Impact on Capital Markets

Global political tensions, including 2024–25 Middle East and Ukraine conflicts, have pushed US 10-year treasury yield volatility to a realized annualized 18% in 2025, raising banks' cost of funds and dampening demand for mortgage-backed securities.

Merchants Bank, though domestic, faces margin pressure as sudden treasury moves altered 30-year mortgage spreads by ~40bps in Q4 2024, affecting loan pricing and hedging costs.

Strategic plans must model external shocks to protect net interest margin and secondary-market liquidity, using stress tests reflecting 50–100bp treasury shocks observed in 2024.

- 10y yield realized vol ~18% (2025)

- 30y mortgage spreads widened ~40bps (Q4 2024)

- Stress scenarios: 50–100bps treasury moves

Tax Policy and Real Estate Incentives

Changes in federal corporate tax rates and the 2023-2025 IRS guidance on bonus depreciation shifts affect Merchants Bank strategic planning, as 21% corporate tax norms and potential capital gains rate adjustments influence lending demand in CRE sectors.

Modifications to depreciation schedules or capital gains treatment can alter client ROI calculations—90% of the bank’s CRE portfolio decisions hinge on tax-affected cash flow projections.

The bank must scale advisory services, leveraging tax specialists to optimize client structures and preserve its own effective tax rate, aiming to limit tax-driven margin erosion.

- Federal corporate tax baseline ~21%

- Bonus depreciation changes impact CRE ROI

- ~90% of CRE lending sensitive to tax shifts

- Need for expanded tax advisory capabilities

Merchants Bank Faces CRE Pressure, Policy Shifts Demand Stronger Advocacy & Tax Planning

Federal housing incentives and heightened post-2024 bank capital rules pressure Merchants Bank’s CRE-heavy balance sheet, while Indiana infrastructure and TIF activity boost local lending; geopolitical-driven treasury volatility (10y vol ~18%, 30y spread +40bps) and tax policy shifts (corporate rate ~21%, bonus depreciation changes) necessitate stronger advocacy, stress-testing, and tax advisory to protect margins.

| Metric | Value |

|---|---|

| CRE concentration | 28% |

| 10y vol (2025) | ~18% |

| 30y spread change | +40bps (Q4 2024) |

| Corporate tax baseline | ~21% |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely impact Merchants Bank, combining data-driven trends and region-specific regulations to identify strategic threats and opportunities for executives, investors, and consultants.

A concise, visually segmented PESTLE summary for Merchants Bank that streamlines external risk assessment and market positioning, ready to drop into presentations or share across teams for faster, aligned strategy discussions.

Economic factors

Interest Rate Stabilization and Strategy

By end-2025, central bank rates stabilized around 4.25%–4.50%, giving Merchants Bank clearer pricing for long-term loans and deposits and reducing hedging costs by an estimated 15% versus 2023–24 volatility.

This predictability enables refined mortgage origination—projected 8% YoY growth in fixed-rate originations—as the bank reallocates from short-term repricing products.

Still, a prolonged high-rate environment risks tipping GDP growth toward 0.5%–1.0% in stress scenarios, requiring conservative credit buffers and tighter underwriting.

Multi-family Real Estate Market Health

The multi-family housing sector underpins Merchants Bank’s asset growth; U.S. apartment vacancy in Q4 2025 averaged 5.6% while Midwest metros like Cleveland and Columbus saw vacancies of 6.2% and 5.9%, signaling localized oversupply that could weigh on occupancy and loan performance.

Inflationary Pressures on Operational Costs

Persistent inflation, with US core PCE at 3.8% in 2024 and CPI averaging 3.4%, raised Merchants Bank non-interest costs—notably a 6–8% rise in labor and 10%+ increases in tech procurement—pressuring margins.

Regional Economic Diversification in Indiana

Indiana's shift toward tech and advanced manufacturing—with manufacturing contributing about 18% of state GDP and tech employment growing roughly 12% from 2019–2024—expands Merchants Bank's pool of commercial clients beyond traditional real estate borrowers.

As regional firms scale, the bank can grow wealth management and business banking revenues; diversifying client sectors reduces concentration risk and strengthens capital and liquidity resilience.

- Manufacturing ~18% of GDP

- Tech employment +12% (2019–2024)

- Lower industry concentration risk

- Opportunity to increase non-RE loan and fee income

Mortgage Market Recovery Trends

The U.S. residential mortgage market shows gradual recovery: origination volume rose 12% year-over-year in 2024 as rates eased from 2023 peaks, though affordability remains strained with median home prices still ~8% above pre-pandemic levels.

Merchants Bank’s mortgage division should target first-time buyers and refinancers with tailored low-down-payment and rate-buydown products while sustaining sub-30-day processing and pricing within 25–50 bps of market to win share.

- Origination +12% YoY (2024)

- Median home price +8% vs 2019

- Processing target: <30 days

- Pricing gap: 25–50 bps

Stable 2025 rates cut hedging costs, boost originations; inflation squeezes margins

Stable 2025 rates (4.25–4.50%) cut hedging costs ~15% vs 2023–24; fixed-rate mortgage originations projected +8% YoY; core PCE 3.8% (2024) and CPI 3.4% raised labor/tech costs 6–10% squeezing margins; U.S. origination +12% YoY (2024); Indiana manufacturing ~18% GDP, tech jobs +12% (2019–24) diversifies loan mix and fee income.

| Metric | Value |

|---|---|

| Policy rate (2025) | 4.25–4.50% |

| Core PCE (2024) | 3.8% |

| Mortgage originations (2024) | +12% YoY |

| Indiana manufacturing | ~18% GDP |

Same Document Delivered

Merchants Bank PESTLE Analysis

The preview shown here is the exact Merchants Bank PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.