Merit Medical PESTLE Analysis

Your Competitive Advantage Starts with This Report

Discover how political, economic, social, technological, legal, and environmental forces are shaping Merit Medical's strategic outlook in our concise PESTLE snapshot—ideal for investors and strategists who need quick, actionable context. Purchase the full PESTLE analysis to unlock detailed risk assessments, trend forecasts, and practical recommendations you can use immediately to inform decisions and outmaneuver competitors.

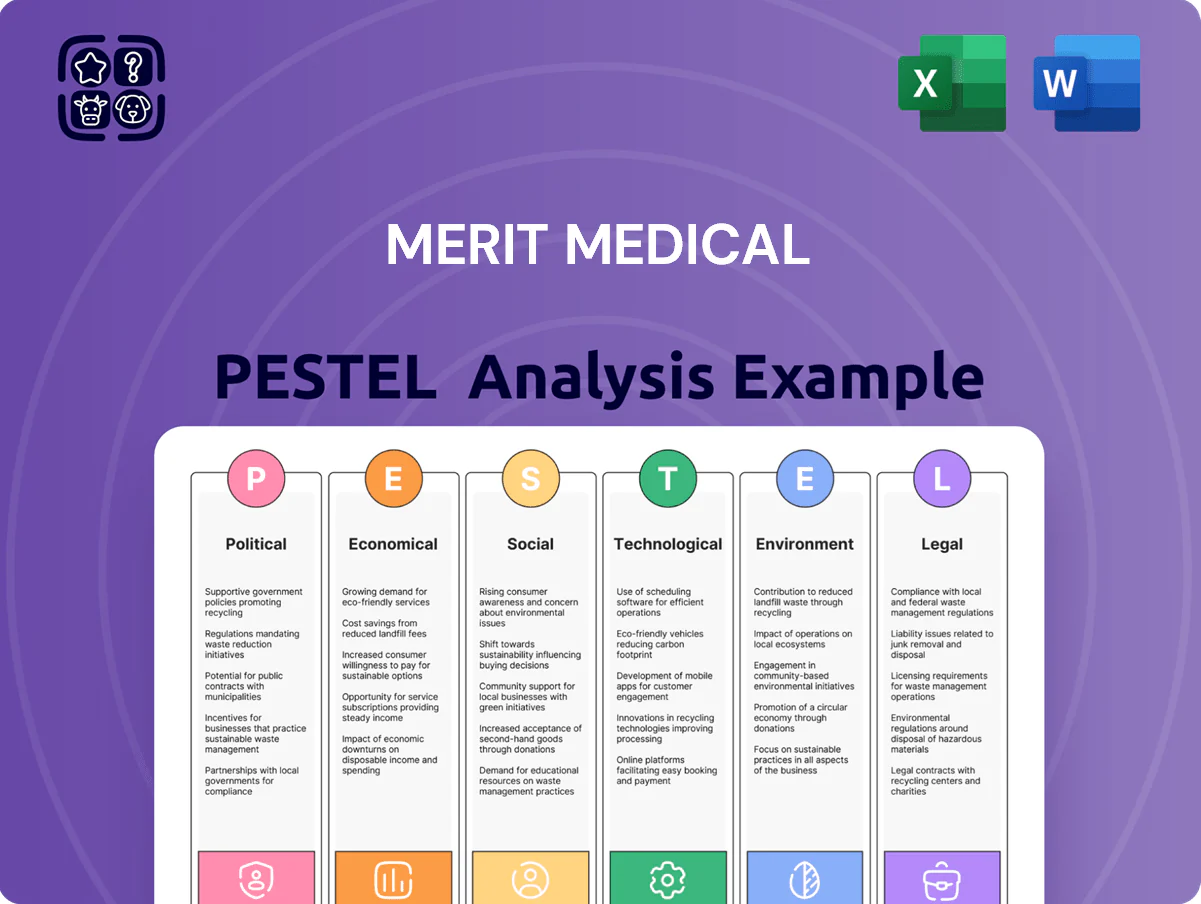

Political factors

Geopolitical Trade Relations

Ongoing US-China trade tensions have raised tariff uncertainty that affects medical device supply chains; tariffs and export controls contributed to a 6–12% increase in component costs for some manufacturers in 2023–2024, pressuring Merit Medical’s margins.

Shifting tariff structures and regional agreements (USMCA, CPTPP accession talks) alter input and finished-goods costs, with ocean freight volatility—up 40% in 2021–2022 and normalizing but still elevated—adding to expense variability.

Strategic diversification of manufacturing—Merit’s 2024 investments expanding capacity in Ireland and Mexico—reduces exposure to sudden policy shifts in major markets and helps stabilize lead times and cost predictability.

Healthcare Reimbursement Policies

Government-led shifts in reimbursement, notably CMS's 2024 Inpatient Prospective Payment updates and expansion of value-based programs covering over 35% of Medicare payments, directly reduce hospital purchasing power and prioritize cost-effective disposables. Political pressure to cut healthcare spending has driven value-based pricing mandates that compress margins for single-use devices, where Merit reported 2024 disposable product revenue of roughly $1.1 billion. Merit must align product value propositions with legislative priorities on affordability and procedural efficiency to protect uptake and margins.

Global Regulatory Harmonization

Global regulatory harmonization can lower compliance costs for Merit Medical, which reported $1.56B revenue in FY2024, by streamlining approvals across markets but may also impose EU MDR-like requirements that raise R&D spend; FDA collaboration with EMA and ICH shortens time-to-market—recent joint guidances cut review times by ~15% in pilot programs—while political instability in emerging markets (e.g., 2024 GDP growth volatility: Latin America 3.1%, Sub-Saharan Africa 3.5%) influences expansion risk and capital allocation.

Government Healthcare Spending

Government healthcare budgets and fiscal policies shape public funding for infrastructure and elective procedures; global public health spending reached an estimated $9.3 trillion in 2024, with OECD countries averaging 8.6% of GDP.

In socialized systems, 2024 austerity pushed procurement delays and preference for lower-cost domestic suppliers, reducing import med-tech spend by ~4–6% in some EU markets.

Merit Medical’s demand depends on steady public investment in cardiology and oncology—markets where public hospitals accounted for roughly 60% of device purchases in 2024.

- Public health spend $9.3T (2024)

- OECD avg 8.6% GDP

- EU med-tech import spend down 4–6% in austerity

- Public hospitals ~60% of cardiology/oncology device buys (2024)

Taxation and Corporate Policy

Changes in US federal corporate tax rates and OECD international tax reforms (e.g., 15% global minimum tax) can materially affect Merit Medical’s FY2025 net income and free cash flow, altering effective tax rate assumptions used in valuations; Merit reported $17.2M tax expense in FY2024, highlighting sensitivity to rate shifts.

Political moves to impose excise taxes on medical device makers could raise COGS and SG&A, squeezing margins—device tax proposals historically targeted up to 2.3% of sales, which on Merit’s $1.0B revenue (TTM 2024) would imply ~$23M incremental cost.

Legislative changes to R&D tax credits influence Merit’s R&D capitalization and cash tax outflows; expansion of credits (e.g., increase from 14% to proposed 20% rates in some bills) could materially improve after-tax cash available for product development.

- OECD 15% global minimum tax impacts effective tax rate planning

- 2.3% device excise tax on $1.0B revenue ≈ $23M annual cost

- FY2024 tax expense $17.2M — indicates tax sensitivity

- Stronger R&D credits could reduce cash tax and fund innovation

Trade, tariffs and taxes squeeze margins—$1.56B revenue, $1.1B disposables in 2024

Trade tensions, tariffs and freight volatility raised component costs ~6–12% in 2023–24; Merit’s 2024 Ireland/Mexico capacity reduces policy exposure. CMS payment shifts and value-based mandates (35%+ Medicare value payments) compress margins on disposables—2024 disposable revenue ≈ $1.1B. OECD 15% minimum tax and potential 2.3% device excise pose tax/COGS risks; FY2024 revenue $1.56B, tax expense $17.2M.

| Metric | 2024 |

|---|---|

| Total revenue | $1.56B |

| Disposable revenue | $1.1B |

| Tax expense | $17.2M |

| Tariff impact | 6–12% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Merit Medical across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends, actionable insights for executives and investors, and forward-looking scenario inputs—formatted for easy inclusion in plans, decks, or reports.

Condenses Merit Medical's PESTLE into a concise, shareable summary that surfaces key external risks and opportunities for rapid decision-making in meetings or presentations.

Economic factors

Inflationary Pressure on Costs

Rising raw material, energy and labor costs compressed Merit Medicals gross margins for disposables; commodity and resin prices rose ~18% in 2024 and US industrial energy CPI rose 9.6% year-over-year, squeezing margins on high-volume items.

Passing costs to hospitals is constrained as US hospital operating margins averaged 2.8% in 2024, forcing Merit to absorb increases or seek price concessions.

Economic volatility in 2024–2025 makes disciplined cost management essential: Merit reported 6.5% productivity improvements in 2024 and prioritized automation and sourcing to protect profitability.

Currency Exchange Fluctuations

As a global medical device maker, Merit Medical faces notable currency risk: in 2024 foreign exchange movements trimmed international revenue by an estimated 2.1% after translation, with EUR/USD volatility ±6% and CNY/USD swings up to ±8% year-over-year affecting reported sales.

Large moves in the euro, yuan or yen can compress local margins and force price adjustments versus competitors; in 2024 Merit cited FX as a key driver of a mid-single-digit impact on operating income.

Merit mitigates exposure through forward hedges covering a portion of forecasted flows and by regionalizing production—localized manufacturing in Europe and APAC reduced translation sensitivity and import cost pressure in 2024.

Interest Rate Environment

The current higher interest rate environment—US Fed funds at 5.25–5.50% as of Dec 2024—raises Merit Medical’s cost of debt, increasing financing costs for acquisitions and capex and potentially constraining M&A; Moody’s Baa corporate yields ~5.1% in 2024 versus ~3% in 2021, making large leveraged deals more expensive. A stabilizing rate path would improve predictability for long‑term investments in manufacturing capacity.

Global Economic Growth Trends

The demand for diagnostic and therapeutic procedures tracks with economic health; global GDP growth slowed to about 3.0% in 2023 and IMF projects 3.0–3.2% for 2024–25, which can constrain elective procedure volumes and device purchases.

Medical devices show relative resilience, but a sharp downturn (eg 2008–09) historically cut elective procedures by double digits; Merit’s sales growth hinges on recovery pace and rising middle-class healthcare spending in EMs where middle-class population is projected to add ~1.0 billion people by 2030.

Merit’s exposure to emerging markets makes expansion dependent on GDP per capita gains and healthcare spend growth, with global health expenditure reaching ~10% of GDP in high-income countries vs 5% in low-income markets, affecting procedure mix and ASPs.

- IMF global GDP ~3.0% (2024–25 forecast)

- Middle-class +~1.0B by 2030 (Emerging Markets)

- Health spend: ~10% GDP (high-income) vs ~5% (low-income)

Labor Market Dynamics

- Manufacturing vacancies ~642,000 (2024)

- Industry capex +8% (2024)

- Biomedical engineering grads +3% (2023)

- Higher wage competition increases COGS and delays time-to-market

Rising input & energy costs squeeze margins amid weak demand, FX drag, and higher rates

Rising input costs and energy (resin +18% in 2024; US industrial energy CPI +9.6%) compressed margins while hospital margins (2.8% in 2024) limit price pass-through; FX trimmed international revenue ~2.1% in 2024; Fed funds 5.25–5.50% (Dec 2024) raised cost of debt; IMF GDP ~3.0% (2024–25) moderates procedure demand; manufacturing vacancies ~642,000 (2024).

| Metric | 2024/25 |

|---|---|

| Resin/commodity change | +18% |

| US industrial energy CPI | +9.6% YoY |

| Hospital operating margin | 2.8% |

| FX revenue impact | -2.1% |

| Fed funds | 5.25–5.50% |

| IMF global GDP | ~3.0% |

| US manufacturing vacancies | ~642,000 |

Full Version Awaits

Merit Medical PESTLE Analysis

The preview shown here is the exact Merit Medical PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic or investment decisions.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Competitive Advantage Starts with This Report

Discover how political, economic, social, technological, legal, and environmental forces are shaping Merit Medical's strategic outlook in our concise PESTLE snapshot—ideal for investors and strategists who need quick, actionable context. Purchase the full PESTLE analysis to unlock detailed risk assessments, trend forecasts, and practical recommendations you can use immediately to inform decisions and outmaneuver competitors.

Political factors

Geopolitical Trade Relations

Ongoing US-China trade tensions have raised tariff uncertainty that affects medical device supply chains; tariffs and export controls contributed to a 6–12% increase in component costs for some manufacturers in 2023–2024, pressuring Merit Medical’s margins.

Shifting tariff structures and regional agreements (USMCA, CPTPP accession talks) alter input and finished-goods costs, with ocean freight volatility—up 40% in 2021–2022 and normalizing but still elevated—adding to expense variability.

Strategic diversification of manufacturing—Merit’s 2024 investments expanding capacity in Ireland and Mexico—reduces exposure to sudden policy shifts in major markets and helps stabilize lead times and cost predictability.

Healthcare Reimbursement Policies

Government-led shifts in reimbursement, notably CMS's 2024 Inpatient Prospective Payment updates and expansion of value-based programs covering over 35% of Medicare payments, directly reduce hospital purchasing power and prioritize cost-effective disposables. Political pressure to cut healthcare spending has driven value-based pricing mandates that compress margins for single-use devices, where Merit reported 2024 disposable product revenue of roughly $1.1 billion. Merit must align product value propositions with legislative priorities on affordability and procedural efficiency to protect uptake and margins.

Global Regulatory Harmonization

Global regulatory harmonization can lower compliance costs for Merit Medical, which reported $1.56B revenue in FY2024, by streamlining approvals across markets but may also impose EU MDR-like requirements that raise R&D spend; FDA collaboration with EMA and ICH shortens time-to-market—recent joint guidances cut review times by ~15% in pilot programs—while political instability in emerging markets (e.g., 2024 GDP growth volatility: Latin America 3.1%, Sub-Saharan Africa 3.5%) influences expansion risk and capital allocation.

Government Healthcare Spending

Government healthcare budgets and fiscal policies shape public funding for infrastructure and elective procedures; global public health spending reached an estimated $9.3 trillion in 2024, with OECD countries averaging 8.6% of GDP.

In socialized systems, 2024 austerity pushed procurement delays and preference for lower-cost domestic suppliers, reducing import med-tech spend by ~4–6% in some EU markets.

Merit Medical’s demand depends on steady public investment in cardiology and oncology—markets where public hospitals accounted for roughly 60% of device purchases in 2024.

- Public health spend $9.3T (2024)

- OECD avg 8.6% GDP

- EU med-tech import spend down 4–6% in austerity

- Public hospitals ~60% of cardiology/oncology device buys (2024)

Taxation and Corporate Policy

Changes in US federal corporate tax rates and OECD international tax reforms (e.g., 15% global minimum tax) can materially affect Merit Medical’s FY2025 net income and free cash flow, altering effective tax rate assumptions used in valuations; Merit reported $17.2M tax expense in FY2024, highlighting sensitivity to rate shifts.

Political moves to impose excise taxes on medical device makers could raise COGS and SG&A, squeezing margins—device tax proposals historically targeted up to 2.3% of sales, which on Merit’s $1.0B revenue (TTM 2024) would imply ~$23M incremental cost.

Legislative changes to R&D tax credits influence Merit’s R&D capitalization and cash tax outflows; expansion of credits (e.g., increase from 14% to proposed 20% rates in some bills) could materially improve after-tax cash available for product development.

- OECD 15% global minimum tax impacts effective tax rate planning

- 2.3% device excise tax on $1.0B revenue ≈ $23M annual cost

- FY2024 tax expense $17.2M — indicates tax sensitivity

- Stronger R&D credits could reduce cash tax and fund innovation

Trade, tariffs and taxes squeeze margins—$1.56B revenue, $1.1B disposables in 2024

Trade tensions, tariffs and freight volatility raised component costs ~6–12% in 2023–24; Merit’s 2024 Ireland/Mexico capacity reduces policy exposure. CMS payment shifts and value-based mandates (35%+ Medicare value payments) compress margins on disposables—2024 disposable revenue ≈ $1.1B. OECD 15% minimum tax and potential 2.3% device excise pose tax/COGS risks; FY2024 revenue $1.56B, tax expense $17.2M.

| Metric | 2024 |

|---|---|

| Total revenue | $1.56B |

| Disposable revenue | $1.1B |

| Tax expense | $17.2M |

| Tariff impact | 6–12% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Merit Medical across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends, actionable insights for executives and investors, and forward-looking scenario inputs—formatted for easy inclusion in plans, decks, or reports.

Condenses Merit Medical's PESTLE into a concise, shareable summary that surfaces key external risks and opportunities for rapid decision-making in meetings or presentations.

Economic factors

Inflationary Pressure on Costs

Rising raw material, energy and labor costs compressed Merit Medicals gross margins for disposables; commodity and resin prices rose ~18% in 2024 and US industrial energy CPI rose 9.6% year-over-year, squeezing margins on high-volume items.

Passing costs to hospitals is constrained as US hospital operating margins averaged 2.8% in 2024, forcing Merit to absorb increases or seek price concessions.

Economic volatility in 2024–2025 makes disciplined cost management essential: Merit reported 6.5% productivity improvements in 2024 and prioritized automation and sourcing to protect profitability.

Currency Exchange Fluctuations

As a global medical device maker, Merit Medical faces notable currency risk: in 2024 foreign exchange movements trimmed international revenue by an estimated 2.1% after translation, with EUR/USD volatility ±6% and CNY/USD swings up to ±8% year-over-year affecting reported sales.

Large moves in the euro, yuan or yen can compress local margins and force price adjustments versus competitors; in 2024 Merit cited FX as a key driver of a mid-single-digit impact on operating income.

Merit mitigates exposure through forward hedges covering a portion of forecasted flows and by regionalizing production—localized manufacturing in Europe and APAC reduced translation sensitivity and import cost pressure in 2024.

Interest Rate Environment

The current higher interest rate environment—US Fed funds at 5.25–5.50% as of Dec 2024—raises Merit Medical’s cost of debt, increasing financing costs for acquisitions and capex and potentially constraining M&A; Moody’s Baa corporate yields ~5.1% in 2024 versus ~3% in 2021, making large leveraged deals more expensive. A stabilizing rate path would improve predictability for long‑term investments in manufacturing capacity.

Global Economic Growth Trends

The demand for diagnostic and therapeutic procedures tracks with economic health; global GDP growth slowed to about 3.0% in 2023 and IMF projects 3.0–3.2% for 2024–25, which can constrain elective procedure volumes and device purchases.

Medical devices show relative resilience, but a sharp downturn (eg 2008–09) historically cut elective procedures by double digits; Merit’s sales growth hinges on recovery pace and rising middle-class healthcare spending in EMs where middle-class population is projected to add ~1.0 billion people by 2030.

Merit’s exposure to emerging markets makes expansion dependent on GDP per capita gains and healthcare spend growth, with global health expenditure reaching ~10% of GDP in high-income countries vs 5% in low-income markets, affecting procedure mix and ASPs.

- IMF global GDP ~3.0% (2024–25 forecast)

- Middle-class +~1.0B by 2030 (Emerging Markets)

- Health spend: ~10% GDP (high-income) vs ~5% (low-income)

Labor Market Dynamics

- Manufacturing vacancies ~642,000 (2024)

- Industry capex +8% (2024)

- Biomedical engineering grads +3% (2023)

- Higher wage competition increases COGS and delays time-to-market

Rising input & energy costs squeeze margins amid weak demand, FX drag, and higher rates

Rising input costs and energy (resin +18% in 2024; US industrial energy CPI +9.6%) compressed margins while hospital margins (2.8% in 2024) limit price pass-through; FX trimmed international revenue ~2.1% in 2024; Fed funds 5.25–5.50% (Dec 2024) raised cost of debt; IMF GDP ~3.0% (2024–25) moderates procedure demand; manufacturing vacancies ~642,000 (2024).

| Metric | 2024/25 |

|---|---|

| Resin/commodity change | +18% |

| US industrial energy CPI | +9.6% YoY |

| Hospital operating margin | 2.8% |

| FX revenue impact | -2.1% |

| Fed funds | 5.25–5.50% |

| IMF global GDP | ~3.0% |

| US manufacturing vacancies | ~642,000 |

Full Version Awaits

Merit Medical PESTLE Analysis

The preview shown here is the exact Merit Medical PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic or investment decisions.