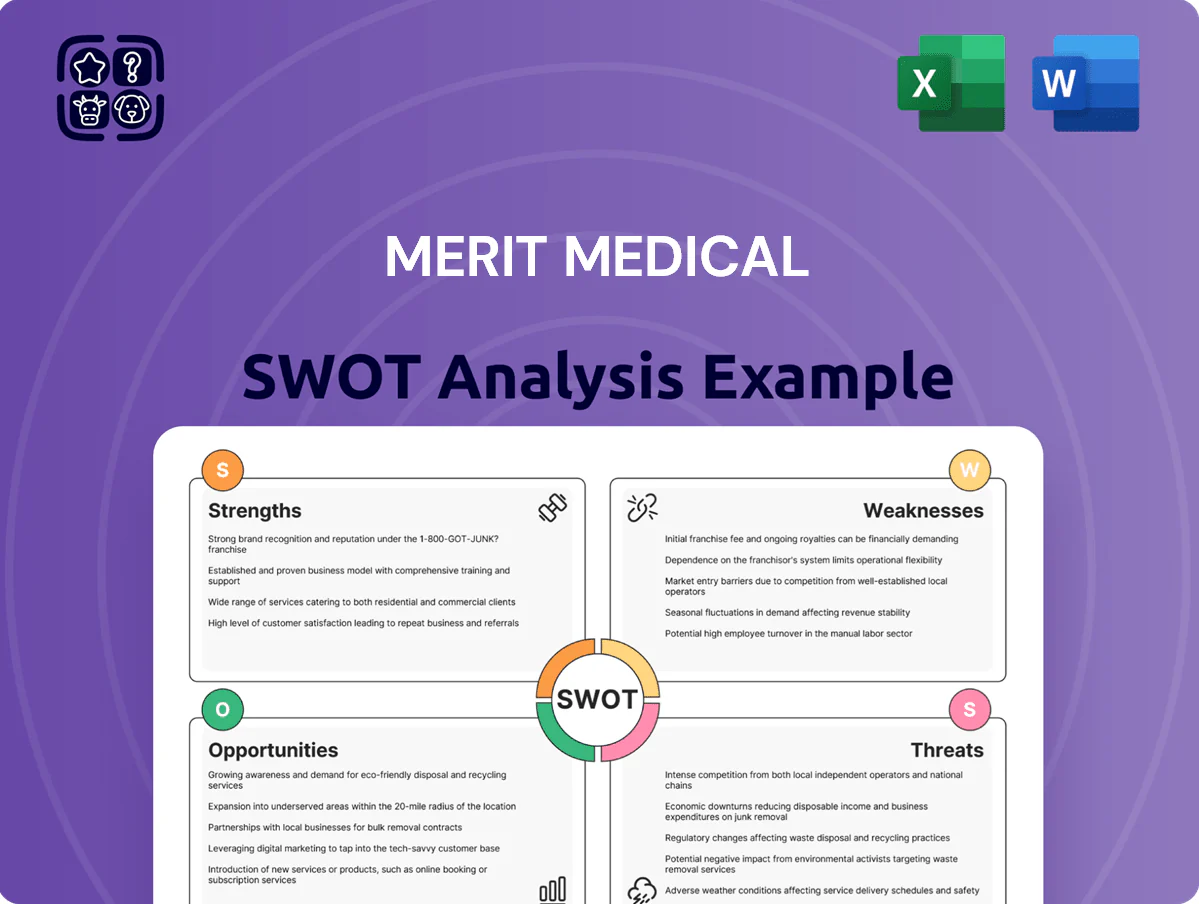

Merit Medical SWOT Analysis

Make Insightful Decisions Backed by Expert Research

Merit Medical’s SWOT highlights robust product diversification and a strong commercial footprint in minimally invasive therapies, tempered by supply-chain exposure and competitive pressure; our full SWOT unpacks these forces with financial context and strategic options—purchase the complete, editable report (Word + Excel) to turn insights into actionable plans for investing, advising, or competing.

Strengths

Broad Product Diversification

Merit Medical sells a wide range of disposable devices across cardiology, radiology, oncology and endoscopy, with product diversification supporting 2024 revenue of about $1.23 billion and a 2024 gross margin near 57% (company filings).

This spread reduces single-specialty downturn risk—cardiology or oncology drag would be cushioned by others—helping stabilize recurring sales and cash flow.

Offering a one-stop portfolio speeds procurement for hospitals; Merit served customers in 90+ countries by end-2024, strengthening channel stickiness and cross-sell opportunities.

Robust Global Sales Infrastructure

Merit Medical operates a global distribution network spanning 100+ countries, enabling rapid scaling of new devices and contributing to roughly 60% of 2024 revenue from international markets (Merit 2024 Form 10-K).

Strong local teams in China and EMEA capture rising procedure volumes—EMEA sales grew ~12% YoY in FY 2024—giving Merit an edge over smaller regional competitors.

Innovation-Driven R&D Culture

Merit Medical’s sustained R&D spending—170–180 million USD annually in 2023–2024, roughly 6–7% of revenue—has produced hundreds of patents and proprietary platforms, keeping it competitive in interventional medicine.

Its clinician-driven design loop yields devices that cut procedure times and complications; internal studies report single-digit percentage gains in procedure efficiency and measurable outcome improvements.

Vertical Integration Efficiencies

Merit Medical’s vertical integration gives tight control over costs and quality, reducing supplier dependency and speeding response to demand shifts; in 2024 the company reported gross margin around 52%, reflecting higher value capture across manufacturing and assembly.

This structure cut lead times by weeks during 2023 supply disruptions and helped sustain adjusted operating margin near 18% in FY2024, supporting faster commercialization of new devices.

- ~52% gross margin (2024)

- ~18% adjusted operating margin (FY2024)

- Reduced supplier reliance; shorter lead times vs market

Strong Clinical Relationships

Merit Medical has cultivated long-term ties with interventional physicians and clinical staff via training and education, driving repeat purchases and implanting products in protocols; this contributed to device revenue stability—Merit reported $466.6 million in device sales for FY2024, up 7% year-over-year.

These programs boost brand loyalty and product stickiness within hospital systems, raising switching costs and shortening adoption cycles for new Merit launches; Nielsen data show clinician recommendation accounts for ~62% of hospital device purchases in vascular niches.

Deep clinical trust creates a high barrier to entry for competitors in specialized segments, protecting margins and market share in core lines like vascular access and oncology devices, where Merit held an estimated 8–10% global share in 2024.

- 466.6M device sales FY2024

- +7% device revenue YoY

- ~62% clinician-driven purchases

- 8–10% global share in core lines

Merit Medical: $1.23B 2024, strong margins, 60% intl, $466.6M devices, robust cash flow

Merit Medical’s diversified disposable portfolio and vertical integration supported ~ $1.23B revenue in 2024 with ~52–57% gross margin and ~18% adjusted operating margin, ~60% international sales, $466.6M device revenue (+7% YoY), R&D $170–180M (6–7% of revenue), and 8–10% share in core lines—driving stable cash flow, shorter lead times, and strong clinician-driven adoption.

| Metric | 2024 |

|---|---|

| Revenue | $1.23B |

| Gross margin | 52–57% |

| Adj. operating margin | ~18% |

| Intl sales | ~60% |

| Device sales | $466.6M (+7%) |

| R&D | $170–180M (6–7%) |

| Core share | 8–10% |

What is included in the product

Provides a concise SWOT overview of Merit Medical, highlighting its core strengths, operational weaknesses, growth opportunities, and external threats shaping competitive positioning and strategic priorities.

Provides a concise Merit Medical SWOT snapshot for rapid strategic alignment and clear communication across teams.

Weaknesses

Elevated Debt-to-Equity Ratio

Merit Medical’s aggressive acquisitions have pushed reported long-term debt to about $1.25 billion as of FY2024, raising the debt-to-equity ratio above 1.1 and concentrating risk on the balance sheet.

Sustaining this leverage needs strong operating cash flow—Merit generated $190 million of operating cash in 2024—so a sharp revenue drop could quickly constrain liquidity and capital allocation.

With U.S. benchmark rates up ~300 basis points since 2021, interest expense rose, subtracting roughly $25–35 million from 2024 net income and compressing margins.

Acquisition Integration Complexity

Integrating Merit Medical’s (market cap ~$2.9B as of Dec 2025) acquisitions—17 deals since 2019—creates ongoing operational and cultural strain on management; failed integrations risk inefficiencies, loss of key talent, and missed revenue targets (Q3 2025 organic growth 1.8%).

Vulnerability to Supply Chain Disruptions

Merit Medical is exposed to raw material price swings—medical-grade plastics and stainless steel—where input costs rose ~18% in 2021–2022 and supply shocks in 2021 cut production days by an estimated 12%; such disruptions can raise manufacturing costs and compress 2024 gross margin (reported 34.5% in FY2024) if Merit cannot pass higher prices to price-sensitive hospitals and IDNs.

Concentration in Single-Use Plastics

Merit Medical’s product mix is heavily weighted to single-use plastic devices; about 70% of 2024 revenue came from disposable procedural products, raising environmental scrutiny as hospitals push for greener procurement.

Reliance on disposables risks procurement exclusions and reputational harm; switching to sustainable polymers needs large capex and can trigger months-to-years of regulatory re-approval, affecting near-term margins.

- ~70% 2024 revenue from disposables

- Hospitals targeting 30–50% procurement sustainability by 2027

- Material & regulatory shift may reduce margins for 12–36 months

Geographic Currency Sensitivity

- FY2024: FX reduced revenue growth by ~3.2 ppt

- FY2024: $12.4M FX hit to operating income

- Hedging limits sudden devaluation exposure

High leverage, disposable-reliant: integration, FX and rate pressures threaten growth

High leverage: $1.25B debt (FY2024) pushes D/E >1.1; operating cash $190M in 2024. Integration risk: 17 deals since 2019; Q3 2025 organic growth 1.8%. Product risk: ~70% 2024 revenue from disposables; hospitals target 30–50% sustainable procurement by 2027. FX and rates: FX cut rev growth ~3.2 ppt and $12.4M hit in 2024; rates raised interest expense ~ $25–35M in 2024.

| Metric | Value |

|---|---|

| Long-term debt (FY2024) | $1.25B |

| Debt/equity | >1.1 |

| Operating cash (2024) | $190M |

| Disposable revenue (2024) | ~70% |

| FX impact (2024) | -3.2 ppt rev growth; -$12.4M OI |

| Interest expense impact (2024) | ~$25–35M |

Preview the Actual Deliverable

Merit Medical SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get; once purchased, the complete, editable version is unlocked. You’re viewing a live preview of the actual file and the full, detailed report becomes available immediately after checkout.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Insightful Decisions Backed by Expert Research

Merit Medical’s SWOT highlights robust product diversification and a strong commercial footprint in minimally invasive therapies, tempered by supply-chain exposure and competitive pressure; our full SWOT unpacks these forces with financial context and strategic options—purchase the complete, editable report (Word + Excel) to turn insights into actionable plans for investing, advising, or competing.

Strengths

Broad Product Diversification

Merit Medical sells a wide range of disposable devices across cardiology, radiology, oncology and endoscopy, with product diversification supporting 2024 revenue of about $1.23 billion and a 2024 gross margin near 57% (company filings).

This spread reduces single-specialty downturn risk—cardiology or oncology drag would be cushioned by others—helping stabilize recurring sales and cash flow.

Offering a one-stop portfolio speeds procurement for hospitals; Merit served customers in 90+ countries by end-2024, strengthening channel stickiness and cross-sell opportunities.

Robust Global Sales Infrastructure

Merit Medical operates a global distribution network spanning 100+ countries, enabling rapid scaling of new devices and contributing to roughly 60% of 2024 revenue from international markets (Merit 2024 Form 10-K).

Strong local teams in China and EMEA capture rising procedure volumes—EMEA sales grew ~12% YoY in FY 2024—giving Merit an edge over smaller regional competitors.

Innovation-Driven R&D Culture

Merit Medical’s sustained R&D spending—170–180 million USD annually in 2023–2024, roughly 6–7% of revenue—has produced hundreds of patents and proprietary platforms, keeping it competitive in interventional medicine.

Its clinician-driven design loop yields devices that cut procedure times and complications; internal studies report single-digit percentage gains in procedure efficiency and measurable outcome improvements.

Vertical Integration Efficiencies

Merit Medical’s vertical integration gives tight control over costs and quality, reducing supplier dependency and speeding response to demand shifts; in 2024 the company reported gross margin around 52%, reflecting higher value capture across manufacturing and assembly.

This structure cut lead times by weeks during 2023 supply disruptions and helped sustain adjusted operating margin near 18% in FY2024, supporting faster commercialization of new devices.

- ~52% gross margin (2024)

- ~18% adjusted operating margin (FY2024)

- Reduced supplier reliance; shorter lead times vs market

Strong Clinical Relationships

Merit Medical has cultivated long-term ties with interventional physicians and clinical staff via training and education, driving repeat purchases and implanting products in protocols; this contributed to device revenue stability—Merit reported $466.6 million in device sales for FY2024, up 7% year-over-year.

These programs boost brand loyalty and product stickiness within hospital systems, raising switching costs and shortening adoption cycles for new Merit launches; Nielsen data show clinician recommendation accounts for ~62% of hospital device purchases in vascular niches.

Deep clinical trust creates a high barrier to entry for competitors in specialized segments, protecting margins and market share in core lines like vascular access and oncology devices, where Merit held an estimated 8–10% global share in 2024.

- 466.6M device sales FY2024

- +7% device revenue YoY

- ~62% clinician-driven purchases

- 8–10% global share in core lines

Merit Medical: $1.23B 2024, strong margins, 60% intl, $466.6M devices, robust cash flow

Merit Medical’s diversified disposable portfolio and vertical integration supported ~ $1.23B revenue in 2024 with ~52–57% gross margin and ~18% adjusted operating margin, ~60% international sales, $466.6M device revenue (+7% YoY), R&D $170–180M (6–7% of revenue), and 8–10% share in core lines—driving stable cash flow, shorter lead times, and strong clinician-driven adoption.

| Metric | 2024 |

|---|---|

| Revenue | $1.23B |

| Gross margin | 52–57% |

| Adj. operating margin | ~18% |

| Intl sales | ~60% |

| Device sales | $466.6M (+7%) |

| R&D | $170–180M (6–7%) |

| Core share | 8–10% |

What is included in the product

Provides a concise SWOT overview of Merit Medical, highlighting its core strengths, operational weaknesses, growth opportunities, and external threats shaping competitive positioning and strategic priorities.

Provides a concise Merit Medical SWOT snapshot for rapid strategic alignment and clear communication across teams.

Weaknesses

Elevated Debt-to-Equity Ratio

Merit Medical’s aggressive acquisitions have pushed reported long-term debt to about $1.25 billion as of FY2024, raising the debt-to-equity ratio above 1.1 and concentrating risk on the balance sheet.

Sustaining this leverage needs strong operating cash flow—Merit generated $190 million of operating cash in 2024—so a sharp revenue drop could quickly constrain liquidity and capital allocation.

With U.S. benchmark rates up ~300 basis points since 2021, interest expense rose, subtracting roughly $25–35 million from 2024 net income and compressing margins.

Acquisition Integration Complexity

Integrating Merit Medical’s (market cap ~$2.9B as of Dec 2025) acquisitions—17 deals since 2019—creates ongoing operational and cultural strain on management; failed integrations risk inefficiencies, loss of key talent, and missed revenue targets (Q3 2025 organic growth 1.8%).

Vulnerability to Supply Chain Disruptions

Merit Medical is exposed to raw material price swings—medical-grade plastics and stainless steel—where input costs rose ~18% in 2021–2022 and supply shocks in 2021 cut production days by an estimated 12%; such disruptions can raise manufacturing costs and compress 2024 gross margin (reported 34.5% in FY2024) if Merit cannot pass higher prices to price-sensitive hospitals and IDNs.

Concentration in Single-Use Plastics

Merit Medical’s product mix is heavily weighted to single-use plastic devices; about 70% of 2024 revenue came from disposable procedural products, raising environmental scrutiny as hospitals push for greener procurement.

Reliance on disposables risks procurement exclusions and reputational harm; switching to sustainable polymers needs large capex and can trigger months-to-years of regulatory re-approval, affecting near-term margins.

- ~70% 2024 revenue from disposables

- Hospitals targeting 30–50% procurement sustainability by 2027

- Material & regulatory shift may reduce margins for 12–36 months

Geographic Currency Sensitivity

- FY2024: FX reduced revenue growth by ~3.2 ppt

- FY2024: $12.4M FX hit to operating income

- Hedging limits sudden devaluation exposure

High leverage, disposable-reliant: integration, FX and rate pressures threaten growth

High leverage: $1.25B debt (FY2024) pushes D/E >1.1; operating cash $190M in 2024. Integration risk: 17 deals since 2019; Q3 2025 organic growth 1.8%. Product risk: ~70% 2024 revenue from disposables; hospitals target 30–50% sustainable procurement by 2027. FX and rates: FX cut rev growth ~3.2 ppt and $12.4M hit in 2024; rates raised interest expense ~ $25–35M in 2024.

| Metric | Value |

|---|---|

| Long-term debt (FY2024) | $1.25B |

| Debt/equity | >1.1 |

| Operating cash (2024) | $190M |

| Disposable revenue (2024) | ~70% |

| FX impact (2024) | -3.2 ppt rev growth; -$12.4M OI |

| Interest expense impact (2024) | ~$25–35M |

Preview the Actual Deliverable

Merit Medical SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get; once purchased, the complete, editable version is unlocked. You’re viewing a live preview of the actual file and the full, detailed report becomes available immediately after checkout.