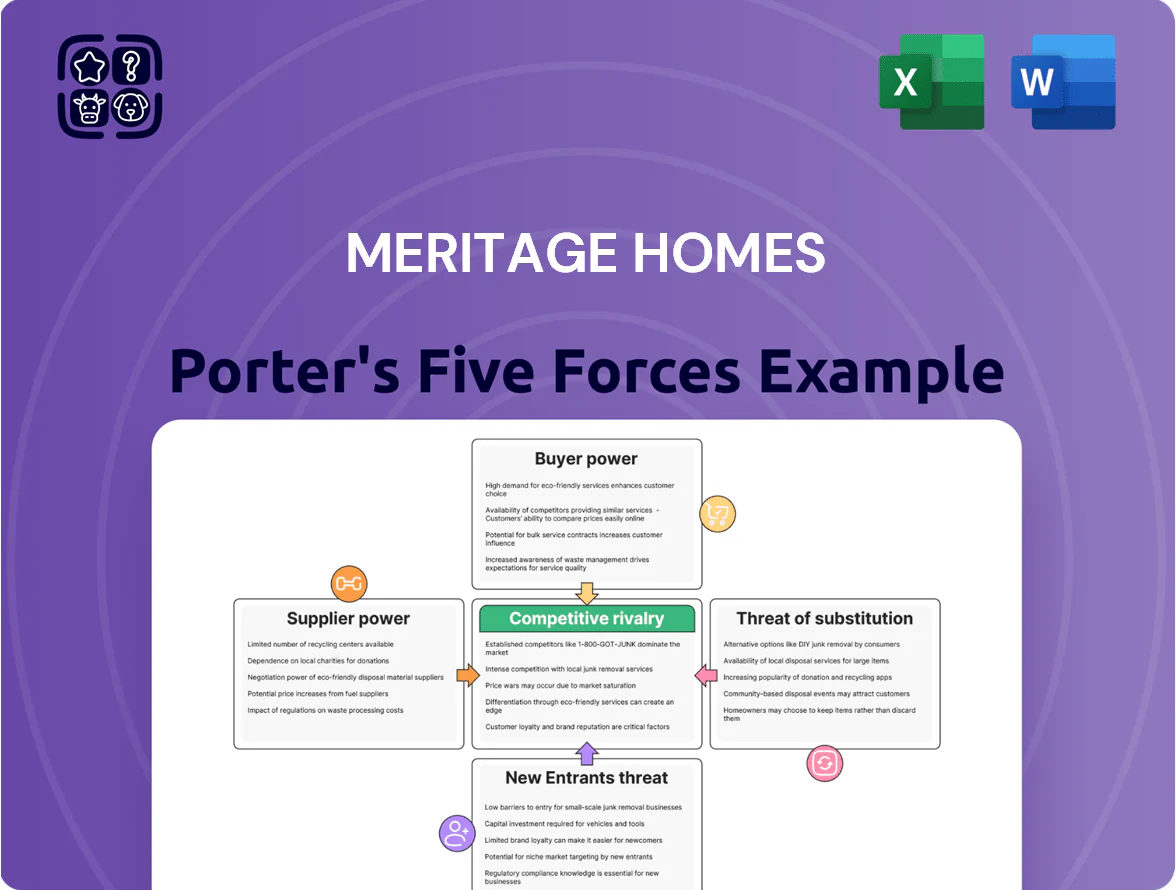

Meritage Homes Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

Meritage Homes faces moderate buyer power, supplier constraints on materials, and significant rivalry amid regional builders, while scale and tech adoption mitigate some threats from new entrants and substitutes.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Meritage Homes’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of building material manufacturers

The market for lumber, gypsum and steel is concentrated among a few large producers, giving suppliers pricing power that kept U.S. softwood lumber futures volatile in 2024–25 (peaks near $700/MBF in 2024). By end-2025 Meritage Homes remains exposed to supplier-driven cost swings despite national buying scale that secured roughly 3–5% volume discounts on commodity buys in 2024.

Shortage of skilled trade labor

The US homebuilding sector faces a persistent shortfall of skilled trades—estimated by the National Association of Home Builders at a 2024 deficit of ~200,000 workers—pressuring Meritage Homes to compete for electricians, plumbers and carpenters with national peers.

Competition raises subcontractor rates; NAHB data show wage inflation for trades at ~6–8% in 2023–24, increasing build costs and risking schedule slippage in high-growth Sun Belt markets.

That scarcity gives subcontractors leverage to demand stricter terms, higher advance payments, and looser timelines, which can compress Meritage’s margins and extend cycle times on large communities.

Limited availability of developed land

Land developers and municipalities control most shovel-ready lots in Meritage Homes’ target Sunbelt and West metros, shrinking available inventory; from 2023–2024, US single-family lot starts fell ~8% while lot prices in Phoenix and Austin rose 12–18%, letting sellers push premiums that compress Meritage’s 2024 gross margin (reported 18.5%) and force higher land spend per lot, tightening its multi-year pipeline visibility.

Impact of global supply chain logistics

Suppliers of specialized appliances and HVAC face global logistics limits and tariffs; in 2024 U.S. appliance import costs rose ~8% year-over-year, raising manufacturer pricing power that can be passed to Meritage Homes.

Meritage’s LiVE.NOW. just-in-time model increases sensitivity: a 2023 Port of Los Angeles congestion spike added ~5–7 day delays, elevating project hold costs and risk of subcontractor claims.

- Appliance/HVAC imports +8% (2024)

- Ports delays added 5–7 days (2023)

- Tariff exposure increases supplier pass-through

- JIT model amplifies disruption impact

Vertical integration of competitors

As rivals like D.R. Horton and Lennar expanded vertical integration—D.R. Horton reported 2024 supplier-controlled lumber yards and Lennar increased owned component operations—independent suppliers' bargaining power rises, squeezing Meritage Homes (NYSE: MTH) as a smaller buyer.

With fewer independent suppliers and concentrated buyers, Meritage faces stiffer price and delivery terms; maintaining diverse supplier relationships reduces risk of being sidelined by competitors with internal supply chains.

- 2024: D.R. Horton and Lennar increased in-house sourcing, shrinking independent supplier pool

- Supply concentration raises input-cost volatility and negotiation rigidity

- Action: diversify suppliers, secure multi-year contracts, consider selective vertical moves

Supplier squeeze, wage inflation and material spikes compress Meritage margins

Supplier power is high: concentrated lumber/gypsum/steel producers and rising vertical integration by D.R. Horton and Lennar pushed input cost volatility (softwood peaks ~700/MBF in 2024) and narrowed supplier options, while skilled-trades shortages (~200,000 deficit in 2024) and 6–8% trade wage inflation raised subcontractor leverage, compressing Meritage’s margins (2024 gross margin 18.5%) and increasing schedule risk.

| Metric | Value |

|---|---|

| Softwood peak (2024) | $700/MBF |

| Trades deficit (2024) | ~200,000 workers |

| Trade wage inflation | 6–8% (2023–24) |

| Appliance import cost rise (2024) | +8% |

| Meritage gross margin (2024) | 18.5% |

What is included in the product

Tailored exclusively for Meritage Homes, this Porter's Five Forces overview uncovers key competitive drivers, buyer and supplier power, entry barriers, substitutes, and emerging threats that shape its pricing, margins, and strategic resilience.

A concise Porter's Five Forces one-sheet for Meritage Homes—quickly spot competitive pressures from suppliers, buyers, new entrants, substitutes, and rivalry to streamline strategic decisions.

Customers Bargaining Power

Sensitivity to mortgage interest rates

By end-2025, Meritage Homes primary buyers—first-time and move-up—are highly sensitive to monthly payments; a 1 percentage-point rise in mortgage rates raised median payment by about 12% in 2024, cutting affordability for buyers earning median US household income ($74,580 in 2023).

When rates stay elevated (30-year fixed averaged ~6.8% in 2025 YTD), buyers secure bargaining power to demand price cuts or rate buy-downs; Meritage reported offering lender credits and buy-downs on 18–25% of closings in 2024 to preserve sales.

Meritage often absorbs concession costs—reducing gross margin per home by several thousand dollars (typical buy-downs cost $6k–$20k)—to help buyers qualify and close, increasing sensitivity of profit to rate moves.

Availability of existing home inventory

The bargaining power of buyers rises as resale inventory climbs; U.S. existing-home listings averaged 1.05 million in 2024 (NAR), giving buyers more alternatives to Meritage new builds and pressuring pricing, incentives, and upgrade offers. Conversely, mortgage rate lock-in—about 65% of homeowners holding sub-4% loans in 2024—keeps many homes off market, reducing substitute supply and slightly weakening buyer leverage versus new construction.

Information transparency and digital tools

Modern homebuyers use online platforms like Zillow, Redfin and builder portals to access comparable sales, construction specs and neighborhood amenities, increasing transparency; in 2024, 72% of buyers used online listings as a primary search tool. This lets customers compare Meritage Homes directly with Lennar and D.R. Horton in real time, pressuring list-price premiums—average incentive packages rose to $15,800 in 2024 across top builders. High market awareness strengthens buyers’ leverage to negotiate upgrades and closing-cost assistance, raising bargaining power.

Incentive expectations in a competitive market

Buyers in the 2025 US housing market expect builder incentives—design-center credits, appliances, and up to 2-3% in covered closing costs—so perks are treated as standard negotiation starters.

Meritage Homes must balance offering those incentives with a 2025 gross margin target near 18–20% to keep sales velocity without margin erosion; a $10k–$30k incentive can cut per-home margin materially.

- 2025 norm: 2–3% closing-costs

- Common credits: $10k–$30k design/appliance

- Meritage margin target: ~18–20%

- Trade-off: faster sales vs. lower per-home profit

Switching costs and alternative housing types

Switching costs are low in the shopping phase: buyers can pivot to competitors, townhomes, or high-end rentals if single-family pricing feels high, and Zillow data (2025) shows U.S. monthly rent rose 6% YoY while median new-home list prices rose 4% YoY, making rentals relatively more attractive.

Low switching raises buyer power, so Meritage must stay price-competitive and push its energy-efficient branding—its solar-ready and Zero Energy Ready Home claims can cut homeowner energy bills by ~30% annually per DOE estimates.

- Low initial switching cost

- Rent vs buy gap widened (rent +6% YoY, 2025)

- New-home list prices +4% YoY (2025)

- Energy-efficiency claim ≈30% bill reduction (DOE)

Buyers Dictate 2025: High Rates + Listings Force Price Cuts, Buy‑downs and $10–30k Incentives

Buyers hold strong leverage in 2025: high mortgage rates (30y ~6.8% YTD) and ample resale listings (1.05M in 2024) drive demands for price cuts, buy-downs (18–25% of Meritage 2024 closings) and $10k–$30k incentives, squeezing Meritage margins (target ~18–20%).

| Metric | Value |

|---|---|

| 30y rate | ~6.8% (2025 YTD) |

| Existing listings | 1.05M (2024) |

| Buy-downs | 18–25% closings (2024) |

| Incentives | $10k–$30k |

Preview the Actual Deliverable

Meritage Homes Porter's Five Forces Analysis

This preview shows the exact Meritage Homes Porter’s Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders.

It’s the full, professionally written assessment of competitive rivalry, supplier and buyer power, threat of entrants, and substitution—formatted and ready for download the moment you buy.

You're viewing the final deliverable; completing payment grants instant access to this identical document for immediate use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

Meritage Homes faces moderate buyer power, supplier constraints on materials, and significant rivalry amid regional builders, while scale and tech adoption mitigate some threats from new entrants and substitutes.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Meritage Homes’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of building material manufacturers

The market for lumber, gypsum and steel is concentrated among a few large producers, giving suppliers pricing power that kept U.S. softwood lumber futures volatile in 2024–25 (peaks near $700/MBF in 2024). By end-2025 Meritage Homes remains exposed to supplier-driven cost swings despite national buying scale that secured roughly 3–5% volume discounts on commodity buys in 2024.

Shortage of skilled trade labor

The US homebuilding sector faces a persistent shortfall of skilled trades—estimated by the National Association of Home Builders at a 2024 deficit of ~200,000 workers—pressuring Meritage Homes to compete for electricians, plumbers and carpenters with national peers.

Competition raises subcontractor rates; NAHB data show wage inflation for trades at ~6–8% in 2023–24, increasing build costs and risking schedule slippage in high-growth Sun Belt markets.

That scarcity gives subcontractors leverage to demand stricter terms, higher advance payments, and looser timelines, which can compress Meritage’s margins and extend cycle times on large communities.

Limited availability of developed land

Land developers and municipalities control most shovel-ready lots in Meritage Homes’ target Sunbelt and West metros, shrinking available inventory; from 2023–2024, US single-family lot starts fell ~8% while lot prices in Phoenix and Austin rose 12–18%, letting sellers push premiums that compress Meritage’s 2024 gross margin (reported 18.5%) and force higher land spend per lot, tightening its multi-year pipeline visibility.

Impact of global supply chain logistics

Suppliers of specialized appliances and HVAC face global logistics limits and tariffs; in 2024 U.S. appliance import costs rose ~8% year-over-year, raising manufacturer pricing power that can be passed to Meritage Homes.

Meritage’s LiVE.NOW. just-in-time model increases sensitivity: a 2023 Port of Los Angeles congestion spike added ~5–7 day delays, elevating project hold costs and risk of subcontractor claims.

- Appliance/HVAC imports +8% (2024)

- Ports delays added 5–7 days (2023)

- Tariff exposure increases supplier pass-through

- JIT model amplifies disruption impact

Vertical integration of competitors

As rivals like D.R. Horton and Lennar expanded vertical integration—D.R. Horton reported 2024 supplier-controlled lumber yards and Lennar increased owned component operations—independent suppliers' bargaining power rises, squeezing Meritage Homes (NYSE: MTH) as a smaller buyer.

With fewer independent suppliers and concentrated buyers, Meritage faces stiffer price and delivery terms; maintaining diverse supplier relationships reduces risk of being sidelined by competitors with internal supply chains.

- 2024: D.R. Horton and Lennar increased in-house sourcing, shrinking independent supplier pool

- Supply concentration raises input-cost volatility and negotiation rigidity

- Action: diversify suppliers, secure multi-year contracts, consider selective vertical moves

Supplier squeeze, wage inflation and material spikes compress Meritage margins

Supplier power is high: concentrated lumber/gypsum/steel producers and rising vertical integration by D.R. Horton and Lennar pushed input cost volatility (softwood peaks ~700/MBF in 2024) and narrowed supplier options, while skilled-trades shortages (~200,000 deficit in 2024) and 6–8% trade wage inflation raised subcontractor leverage, compressing Meritage’s margins (2024 gross margin 18.5%) and increasing schedule risk.

| Metric | Value |

|---|---|

| Softwood peak (2024) | $700/MBF |

| Trades deficit (2024) | ~200,000 workers |

| Trade wage inflation | 6–8% (2023–24) |

| Appliance import cost rise (2024) | +8% |

| Meritage gross margin (2024) | 18.5% |

What is included in the product

Tailored exclusively for Meritage Homes, this Porter's Five Forces overview uncovers key competitive drivers, buyer and supplier power, entry barriers, substitutes, and emerging threats that shape its pricing, margins, and strategic resilience.

A concise Porter's Five Forces one-sheet for Meritage Homes—quickly spot competitive pressures from suppliers, buyers, new entrants, substitutes, and rivalry to streamline strategic decisions.

Customers Bargaining Power

Sensitivity to mortgage interest rates

By end-2025, Meritage Homes primary buyers—first-time and move-up—are highly sensitive to monthly payments; a 1 percentage-point rise in mortgage rates raised median payment by about 12% in 2024, cutting affordability for buyers earning median US household income ($74,580 in 2023).

When rates stay elevated (30-year fixed averaged ~6.8% in 2025 YTD), buyers secure bargaining power to demand price cuts or rate buy-downs; Meritage reported offering lender credits and buy-downs on 18–25% of closings in 2024 to preserve sales.

Meritage often absorbs concession costs—reducing gross margin per home by several thousand dollars (typical buy-downs cost $6k–$20k)—to help buyers qualify and close, increasing sensitivity of profit to rate moves.

Availability of existing home inventory

The bargaining power of buyers rises as resale inventory climbs; U.S. existing-home listings averaged 1.05 million in 2024 (NAR), giving buyers more alternatives to Meritage new builds and pressuring pricing, incentives, and upgrade offers. Conversely, mortgage rate lock-in—about 65% of homeowners holding sub-4% loans in 2024—keeps many homes off market, reducing substitute supply and slightly weakening buyer leverage versus new construction.

Information transparency and digital tools

Modern homebuyers use online platforms like Zillow, Redfin and builder portals to access comparable sales, construction specs and neighborhood amenities, increasing transparency; in 2024, 72% of buyers used online listings as a primary search tool. This lets customers compare Meritage Homes directly with Lennar and D.R. Horton in real time, pressuring list-price premiums—average incentive packages rose to $15,800 in 2024 across top builders. High market awareness strengthens buyers’ leverage to negotiate upgrades and closing-cost assistance, raising bargaining power.

Incentive expectations in a competitive market

Buyers in the 2025 US housing market expect builder incentives—design-center credits, appliances, and up to 2-3% in covered closing costs—so perks are treated as standard negotiation starters.

Meritage Homes must balance offering those incentives with a 2025 gross margin target near 18–20% to keep sales velocity without margin erosion; a $10k–$30k incentive can cut per-home margin materially.

- 2025 norm: 2–3% closing-costs

- Common credits: $10k–$30k design/appliance

- Meritage margin target: ~18–20%

- Trade-off: faster sales vs. lower per-home profit

Switching costs and alternative housing types

Switching costs are low in the shopping phase: buyers can pivot to competitors, townhomes, or high-end rentals if single-family pricing feels high, and Zillow data (2025) shows U.S. monthly rent rose 6% YoY while median new-home list prices rose 4% YoY, making rentals relatively more attractive.

Low switching raises buyer power, so Meritage must stay price-competitive and push its energy-efficient branding—its solar-ready and Zero Energy Ready Home claims can cut homeowner energy bills by ~30% annually per DOE estimates.

- Low initial switching cost

- Rent vs buy gap widened (rent +6% YoY, 2025)

- New-home list prices +4% YoY (2025)

- Energy-efficiency claim ≈30% bill reduction (DOE)

Buyers Dictate 2025: High Rates + Listings Force Price Cuts, Buy‑downs and $10–30k Incentives

Buyers hold strong leverage in 2025: high mortgage rates (30y ~6.8% YTD) and ample resale listings (1.05M in 2024) drive demands for price cuts, buy-downs (18–25% of Meritage 2024 closings) and $10k–$30k incentives, squeezing Meritage margins (target ~18–20%).

| Metric | Value |

|---|---|

| 30y rate | ~6.8% (2025 YTD) |

| Existing listings | 1.05M (2024) |

| Buy-downs | 18–25% closings (2024) |

| Incentives | $10k–$30k |

Preview the Actual Deliverable

Meritage Homes Porter's Five Forces Analysis

This preview shows the exact Meritage Homes Porter’s Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders.

It’s the full, professionally written assessment of competitive rivalry, supplier and buyer power, threat of entrants, and substitution—formatted and ready for download the moment you buy.

You're viewing the final deliverable; completing payment grants instant access to this identical document for immediate use.