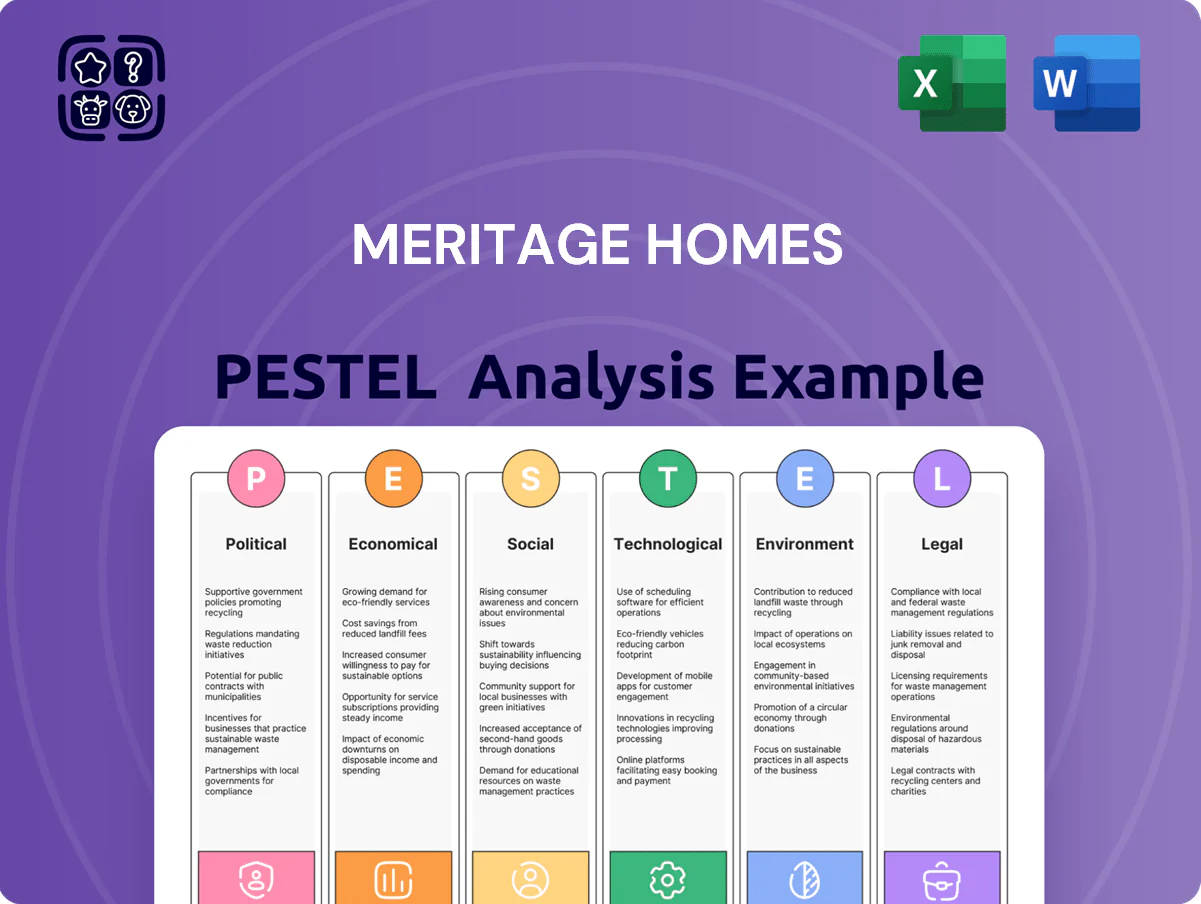

Meritage Homes PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Unlock how political, economic, social, technological, legal, and environmental forces are reshaping Meritage Homes’ growth and risk profile—our PESTLE pinpoints supply-chain pressures, regulatory exposures, and sustainability drivers you need to know; buy the full analysis for the complete, actionable briefing and ready-to-use charts.

Political factors

Federal housing policy and tax incentives

Zoning and land use regulations

Local and state political climates shape Meritage Homes ability to acquire developable parcels; in 2024 Meritage opened 5,300 homes and cited lot constraints as a key limiter to starts, reflecting regulatory impact on supply.

Rising NIMBY opposition and anti-sprawl measures have prompted tighter zoning in key Sun Belt markets, adding estimated $15,000–$40,000 per home in entitlement and mitigation costs in recent projects.

Delays from rezoning can push construction timelines by 6–18 months, so proactive engagement with local councils and targeted community outreach is essential to preserve Meritage’s steady community opening pipeline.

Trade policies and material tariffs

Tariffs on imported building materials—like Canadian softwood lumber tariffs reinstated intermittently and US steel/aluminum duties averaging 10–25% since 2018—increase Meritage Homes’ COGS and drove a 2023 industry-wide lumber cost spike where lumber futures rose ~40%, squeezing margins. Political shifts or new trade barriers can cause rapid cost volatility, forcing frequent pricing and option-package adjustments. Robust strategic procurement, diversified sourcing and political risk assessment are essential to protect FY2024–2025 margins.

Government-sponsored enterprise reform

The political direction of Fannie Mae and Freddie Mac shapes mortgage credit availability and cost for Meritage Homes’ primary customers; in 2025 these agencies backstopped roughly 40% of single-family mortgages, so policy shifts can materially affect demand.

Legislative moves toward privatization or stricter capital/lending standards could tighten credit, raising borrowing costs and reducing approvals for first-time buyers who made up about 35% of Meritage purchasers in 2024.

Meritage’s mortgage operations must stay agile—adjusting seller-assisted programs and down-payment options—to offset potential declines in buyer financing amid evolving federal rules and higher mortgage rates.

- ~40% of single-family mortgages tied to GSEs (2025)

- 35% of Meritage buyers were first-time purchasers (2024)

- Need for flexible internal mortgage programs to mitigate tighter credit

Infrastructure investment and development

Federal and state infrastructure funding—$153 billion allocated in FY2025 under IIJA-related programs and continued CHIPS/INFRA grants—directly affects the viability of suburban projects where Meritage Homes operates, improving roads, water and power required for new communities.

Political prioritization of projects raises land values and accessibility; metro-edge lots near planned highway expansions have seen parcel premiums of 8–12% in 2024.

Conversely, municipalities that reduced capital budgets in 2024 saw permit backlogs increase 15–25%, stalling community build-out and constraining Meritage’s expansion timing.

- FY2025 federal infrastructure allocations $153B impact utilities/highways

- Land premiums near planned projects +8–12% (2024 data)

- Permit backlogs +15–25% where funding dropped (2024)

Policy, tariffs & zoning reshape housing: first‑time buyers up, costs and lot premiums rise

| Metric | Value |

|---|---|

| First-time buyers (2024) | 34–35% |

| GSE share (2025) | ~40% |

| IIJA funds (FY2025) | $153B |

| Lumber futures spike (2023) | +40% |

What is included in the product

Explores how macro-environmental forces uniquely impact Meritage Homes across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven trends and region-specific examples to identify risks and opportunities for executives, investors, and strategists.

Provides a concise, visually segmented PESTLE summary of Meritage Homes that’s easily dropped into presentations or shared across teams to streamline external risk discussions and strategic planning.

Economic factors

Interest rate environment and mortgage costs

Fluctuations in the federal funds rate drive mortgage yields; as of Jan 2026 the 30-year fixed mortgage averaged about 6.8%, up from ~3% in 2021, cutting affordability and suppressing Meritage Homes’ cancellations and new orders in 2022–25.

Higher rates raise Meritage’s cost of capital and pressure profit margins on spec inventory; the company must manage spec homes given tighter buyer borrowing power and observed single-family starts fell ~15% YoY in 2023–24.

Inflationary pressures on construction costs

Economic inflation raises costs for materials, labor, and energy—input costs for Meritage—where US construction material prices rose 6.3% year-over-year in 2024 and producer prices for residential construction were up 5.8% through 2024.

Persistent 2025 inflation could force Meritage to raise home prices, threatening affordability for entry-level buyers given existing median new-home price of about $441,700 in 2024.

Meritage’s supply-chain management and efficiency gains—it reported gross margin of 21.5% in FY2024—will be critical to preserve competitiveness amid higher input inflation.

Labor market conditions and wage growth

Tight U.S. construction labor pushed average hourly wages for construction workers up 5.6% year-over-year in 2024, raising Meritage Homes’ skilled-trade payroll and contributing to supply-side delays in 2024–2025; concurrently, median household income rose ~4.8% in 2024, expanding the buyer pool but increasing overhead. Meritage’s lean floor plans and standardized processes aim to offset labor shortages and a reported 3–5% rise in build costs per home in 2024.

Consumer confidence and wealth effects

Consumer confidence drives Meritage Homes demand; US consumer confidence index was 104.7 in Jan 2026 and the S&P 500 rose ~18% in 2024, supporting higher buyer activity and up to 10–15% better conversion in strong periods.

Rising unemployment (4.0% Dec 2025) or recession fears increase cancellations and shift buyers toward entry-level communities; during 2020–2023 downturns cancellations spiked and entry-level sales share rose ~6–8%.

- Higher confidence/S&P gains → increased traffic, ~10–15% higher conversion

- Unemployment up → more cancellations, demand shifts to lower-priced homes

- CCI 104.7 (Jan 2026); unemployment 4.0% (Dec 2025)

Housing inventory levels and competition

The limited supply of existing homes versus new construction strengthens Meritage Homes’ pricing power and can shift market share to builders; U.S. resale inventory hit about 2.1 months supply in late 2023-early 2024, enhancing demand for new builds.

Low resale inventory and rate-lock effects—roughly 20–25% of homeowners estimated to be rate-locked with sub-4% mortgages in 2024—support Meritage’s spec-home, quick-turn strategy, improving turnover and margins.

Higher rates, rising costs squeeze builders as tight resale supply sustains spec demand

Higher rates (30-yr ~6.8% Jan 2026) cut affordability and orders; construction input inflation (+6.3% materials 2024) and wage rises (+5.6% 2024) squeeze margins despite gross margin 21.5% FY2024; resale inventory tight (~2.1 months) and ~20–25% rate-locked homeowners support spec-sales; unemployment 4.0% Dec 2025 and CCI 104.7 Jan 2026 drive demand volatility.

| Metric | Value |

|---|---|

| 30-yr mortgage | 6.8% (Jan 2026) |

| Materials inflation | +6.3% (2024) |

| Wage growth | +5.6% (2024) |

| Gross margin | 21.5% (FY2024) |

| Resale supply | 2.1 months |

| Unemployment | 4.0% (Dec 2025) |

| CCI | 104.7 (Jan 2026) |

Full Version Awaits

Meritage Homes PESTLE Analysis

The preview shown here is the exact Meritage Homes PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning or investment decisions.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Unlock how political, economic, social, technological, legal, and environmental forces are reshaping Meritage Homes’ growth and risk profile—our PESTLE pinpoints supply-chain pressures, regulatory exposures, and sustainability drivers you need to know; buy the full analysis for the complete, actionable briefing and ready-to-use charts.

Political factors

Federal housing policy and tax incentives

Zoning and land use regulations

Local and state political climates shape Meritage Homes ability to acquire developable parcels; in 2024 Meritage opened 5,300 homes and cited lot constraints as a key limiter to starts, reflecting regulatory impact on supply.

Rising NIMBY opposition and anti-sprawl measures have prompted tighter zoning in key Sun Belt markets, adding estimated $15,000–$40,000 per home in entitlement and mitigation costs in recent projects.

Delays from rezoning can push construction timelines by 6–18 months, so proactive engagement with local councils and targeted community outreach is essential to preserve Meritage’s steady community opening pipeline.

Trade policies and material tariffs

Tariffs on imported building materials—like Canadian softwood lumber tariffs reinstated intermittently and US steel/aluminum duties averaging 10–25% since 2018—increase Meritage Homes’ COGS and drove a 2023 industry-wide lumber cost spike where lumber futures rose ~40%, squeezing margins. Political shifts or new trade barriers can cause rapid cost volatility, forcing frequent pricing and option-package adjustments. Robust strategic procurement, diversified sourcing and political risk assessment are essential to protect FY2024–2025 margins.

Government-sponsored enterprise reform

The political direction of Fannie Mae and Freddie Mac shapes mortgage credit availability and cost for Meritage Homes’ primary customers; in 2025 these agencies backstopped roughly 40% of single-family mortgages, so policy shifts can materially affect demand.

Legislative moves toward privatization or stricter capital/lending standards could tighten credit, raising borrowing costs and reducing approvals for first-time buyers who made up about 35% of Meritage purchasers in 2024.

Meritage’s mortgage operations must stay agile—adjusting seller-assisted programs and down-payment options—to offset potential declines in buyer financing amid evolving federal rules and higher mortgage rates.

- ~40% of single-family mortgages tied to GSEs (2025)

- 35% of Meritage buyers were first-time purchasers (2024)

- Need for flexible internal mortgage programs to mitigate tighter credit

Infrastructure investment and development

Federal and state infrastructure funding—$153 billion allocated in FY2025 under IIJA-related programs and continued CHIPS/INFRA grants—directly affects the viability of suburban projects where Meritage Homes operates, improving roads, water and power required for new communities.

Political prioritization of projects raises land values and accessibility; metro-edge lots near planned highway expansions have seen parcel premiums of 8–12% in 2024.

Conversely, municipalities that reduced capital budgets in 2024 saw permit backlogs increase 15–25%, stalling community build-out and constraining Meritage’s expansion timing.

- FY2025 federal infrastructure allocations $153B impact utilities/highways

- Land premiums near planned projects +8–12% (2024 data)

- Permit backlogs +15–25% where funding dropped (2024)

Policy, tariffs & zoning reshape housing: first‑time buyers up, costs and lot premiums rise

| Metric | Value |

|---|---|

| First-time buyers (2024) | 34–35% |

| GSE share (2025) | ~40% |

| IIJA funds (FY2025) | $153B |

| Lumber futures spike (2023) | +40% |

What is included in the product

Explores how macro-environmental forces uniquely impact Meritage Homes across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven trends and region-specific examples to identify risks and opportunities for executives, investors, and strategists.

Provides a concise, visually segmented PESTLE summary of Meritage Homes that’s easily dropped into presentations or shared across teams to streamline external risk discussions and strategic planning.

Economic factors

Interest rate environment and mortgage costs

Fluctuations in the federal funds rate drive mortgage yields; as of Jan 2026 the 30-year fixed mortgage averaged about 6.8%, up from ~3% in 2021, cutting affordability and suppressing Meritage Homes’ cancellations and new orders in 2022–25.

Higher rates raise Meritage’s cost of capital and pressure profit margins on spec inventory; the company must manage spec homes given tighter buyer borrowing power and observed single-family starts fell ~15% YoY in 2023–24.

Inflationary pressures on construction costs

Economic inflation raises costs for materials, labor, and energy—input costs for Meritage—where US construction material prices rose 6.3% year-over-year in 2024 and producer prices for residential construction were up 5.8% through 2024.

Persistent 2025 inflation could force Meritage to raise home prices, threatening affordability for entry-level buyers given existing median new-home price of about $441,700 in 2024.

Meritage’s supply-chain management and efficiency gains—it reported gross margin of 21.5% in FY2024—will be critical to preserve competitiveness amid higher input inflation.

Labor market conditions and wage growth

Tight U.S. construction labor pushed average hourly wages for construction workers up 5.6% year-over-year in 2024, raising Meritage Homes’ skilled-trade payroll and contributing to supply-side delays in 2024–2025; concurrently, median household income rose ~4.8% in 2024, expanding the buyer pool but increasing overhead. Meritage’s lean floor plans and standardized processes aim to offset labor shortages and a reported 3–5% rise in build costs per home in 2024.

Consumer confidence and wealth effects

Consumer confidence drives Meritage Homes demand; US consumer confidence index was 104.7 in Jan 2026 and the S&P 500 rose ~18% in 2024, supporting higher buyer activity and up to 10–15% better conversion in strong periods.

Rising unemployment (4.0% Dec 2025) or recession fears increase cancellations and shift buyers toward entry-level communities; during 2020–2023 downturns cancellations spiked and entry-level sales share rose ~6–8%.

- Higher confidence/S&P gains → increased traffic, ~10–15% higher conversion

- Unemployment up → more cancellations, demand shifts to lower-priced homes

- CCI 104.7 (Jan 2026); unemployment 4.0% (Dec 2025)

Housing inventory levels and competition

The limited supply of existing homes versus new construction strengthens Meritage Homes’ pricing power and can shift market share to builders; U.S. resale inventory hit about 2.1 months supply in late 2023-early 2024, enhancing demand for new builds.

Low resale inventory and rate-lock effects—roughly 20–25% of homeowners estimated to be rate-locked with sub-4% mortgages in 2024—support Meritage’s spec-home, quick-turn strategy, improving turnover and margins.

Higher rates, rising costs squeeze builders as tight resale supply sustains spec demand

Higher rates (30-yr ~6.8% Jan 2026) cut affordability and orders; construction input inflation (+6.3% materials 2024) and wage rises (+5.6% 2024) squeeze margins despite gross margin 21.5% FY2024; resale inventory tight (~2.1 months) and ~20–25% rate-locked homeowners support spec-sales; unemployment 4.0% Dec 2025 and CCI 104.7 Jan 2026 drive demand volatility.

| Metric | Value |

|---|---|

| 30-yr mortgage | 6.8% (Jan 2026) |

| Materials inflation | +6.3% (2024) |

| Wage growth | +5.6% (2024) |

| Gross margin | 21.5% (FY2024) |

| Resale supply | 2.1 months |

| Unemployment | 4.0% (Dec 2025) |

| CCI | 104.7 (Jan 2026) |

Full Version Awaits

Meritage Homes PESTLE Analysis

The preview shown here is the exact Meritage Homes PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning or investment decisions.