MGIC Boston Consulting Group Matrix

See the Bigger Picture

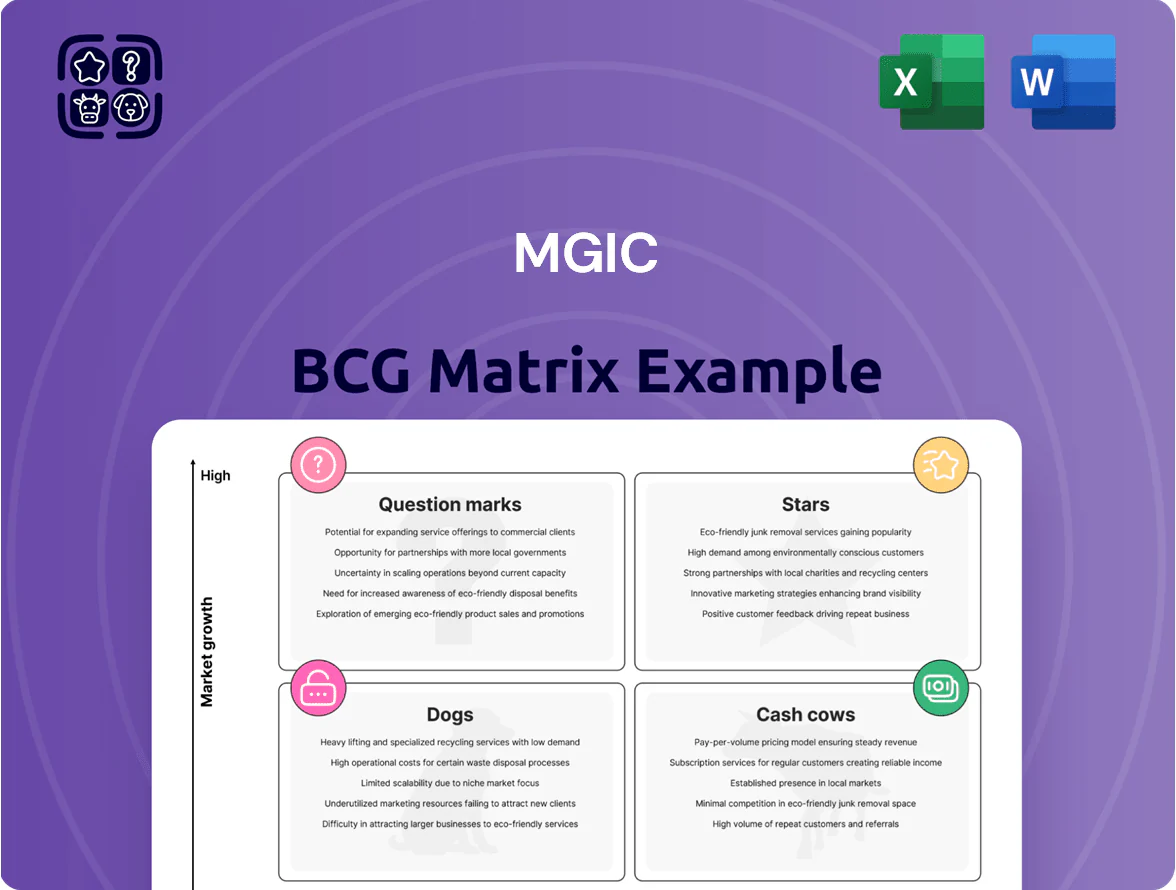

Explore MGIC’s BCG Matrix to see which business lines are driving growth and which may be draining resources—this snapshot highlights likely Stars, Cash Cows, Dogs, and Question Marks based on market share and growth trends. The full BCG Matrix delivers quadrant-by-quadrant placement, data-backed recommendations, and strategic actions tailored to MGIC’s evolving mortgage insurance landscape. Purchase the complete report for a ready-to-use Word analysis and Excel summary to inform investment, resource allocation, and competitive strategy.

Stars

New Insurance Written (NIW)

As of late 2025, MGIC’s New Insurance Written (NIW) is a Star in the BCG matrix, with $17.1 billion written in Q4 2025, reflecting a leading market share in the active purchase segment.

NIW captures the wave of first-time homebuyers needing mortgage insurance for low‑down‑payment loans, supporting MGIC’s top position among lenders.

The unit consumes capital to support this new volume—reserve and capital usage rose in 2025—but its growth and market leadership keep MGIC a top-tier choice for lending partners.

Advanced Risk Analytics and MiQ

MGIC’s proprietary MiQ pricing engine uses AI and data analytics to deliver granular, adaptive pricing; in 2025 MiQ helped underwrite ~30% of new policies, improving risk-adjusted margins by an estimated 120 basis points versus cohort pricing.

MiQ is a Star in the BCG matrix because it captures higher-quality loans and supports growth in the fintech-integrated mortgage market, where originations rose ~18% year-over-year in 2024.

Ongoing investment is critical: MGIC’s 2024 tech spend climbed to $95M to counter rival automated valuation and pricing models and protect this competitive advantage.

Lender-Paid Mortgage Insurance (LPMI)

Lender-Paid Mortgage Insurance (LPMI) is a high-growth MGIC product segment; industry LPMI originations rose ~18% in 2024 to $45B, and MGIC is expanding to offer flexible alternatives to borrower-paid MI that appeal to lenders who bake insurance into rates.

Targeting this niche can lift MGIC’s lender-market share—MGIC held ~24% private MI market share in 2024—and win accounts that favor rate-based pricing, but conversion needs heavy promotion and broker relationships.

To turn rapid growth into dominance, MGIC must invest in placement incentives, co-marketing, and tech integration; expect marketing and distribution spend to rise by mid-teens percent in FY2025 to capture scale.

Digital Integration and API Services

MGIC’s deep API and LOS integrations with top originators (including Ellie Mae/ICE and Blend) act as a Star by capturing high placement at point-of-sale; MGIC reported a 22% rise in digital-delivered endorsements in 2024, lifting placement with tech-enabled lenders.

These integrations meet market demand for real-time decisioning and seamless workflows—digital mortgage volume hit 48% of originations in 2024, so MGIC’s platform investments keep it the primary choice for modern lenders.

- 22% rise in digital endorsements (2024)

- 48% of originations via digital channels (2024)

- Close ties to Ellie Mae/ICE and Blend LOS

Emerging Geographic Markets

MGIC is targeting high-growth regions where U.S. Sun Belt metros saw population gains of 1.1–1.8% in 2024 versus national 0.4%, and housing permits rose 12% year-over-year; MGIC aims to capture new mortgages ahead of rivals by deploying localized underwriting and distribution.

The push requires higher marketing and acquisition spend—MGIC increased field marketing by ~22% in 2024—yet positions the firm to lead in hubs forecasted to account for ≥30% of net new single-family mortgage originations through 2027.

- Target: Sun Belt metros with 1%+ population growth

- CapEx/marketing: +22% in 2024

- Goal: capture ≥30% of new single-family originations by 2027

MGIC Soars: $17.1B NIW, MiQ ~30% Market Share, 120bps Margin Boost

MGIC’s NIW and MiQ are Stars: NIW hit $17.1B in Q4 2025; MiQ underwrote ~30% of new policies in 2025, adding ~120 bps to margins. Digital integrations raised endorsements 22% in 2024; digital mortgage share was 48%. MGIC held ~24% private MI share in 2024 and targets Sun Belt growth to capture ≥30% of new originations by 2027.

| Metric | 2024–2025 |

|---|---|

| NIW Q4 2025 | $17.1B |

| MiQ share 2025 | ~30% |

| Margin lift | ~120 bps |

| Digital endorsements | +22% (2024) |

| Private MI share | ~24% (2024) |

What is included in the product

Comprehensive BCG Matrix analysis of MGIC’s units with strategic guidance—identify Stars, Cash Cows, Question Marks, Dogs and recommended actions.

One-page MGIC BCG Matrix placing each unit in a quadrant for clear strategic prioritization

Cash Cows

Primary Insurance in Force (IIF)

Surpassing $303 billion IIF by year-end 2025, MGIC’s primary Insurance in Force is the ultimate Cash Cow, producing steady premium income and underwriting margin that funded $420 million in dividends and $300 million in buybacks in 2025.

The mature portfolio needs minimal new capital to maintain, converting low maintenance expense into free cash flow; persistence runs ~85%, keeping lifetime profits high and loss ratios stable around 12% in 2025.

Investment Portfolio Yield

With a book yield of 4% and quarterly investment income of $62 million, MGIC’s $5.7 billion portfolio functions as a reliable Cash Cow in the BCG matrix.

Disciplined fixed-income management taps the higher-for-longer 2025 rate backdrop, translating to steady, non-cyclical income that buffered MGIC through 2025 credit spread volatility.

This predictable cash flow covers administrative costs and preserves capital flexibility, supporting reserve builds and strategic optionality such as repurchases or bolt-on investments.

Established Lender Relationships

MGIC’s decades-long ties with over 1,000 national and regional lenders generate steady book flow, representing a high-market-share cash cow that accounted for roughly 60% of 2024 premium volume ($1.2B of $2.0B total), minimizing need for heavy promotion.

This mature network sustains MGIC’s market-leading position with low customer acquisition costs—loss-adjusted expense ratios held near 12% in 2024—so revenue scales with underwriting rather than marketing spend.

Legacy Underwriting Operations

MGIC’s mature underwriting operations act as a Cash Cow by cutting admin costs and boosting margins—2024 combined ratio improved to ~62%, lifting underwriting income to $1.1B and free cash flow used for tech R&D.

Decades of refined workflows process ~2.3M applications yearly with claims-cycle time down 18% since 2019, sustaining ~30% operating margin on legacy products.

- High-volume: ~2.3M applications/year

- Efficiency: combined ratio ~62% (2024)

- Profit: $1.1B underwriting income (2024)

- Margin: ~30% operating margin on legacy

- Reinvestment: free cash flow funds tech R&D

Reinsurance Program Benefits

MGIC’s quota share and excess-of-loss reinsurance, including a planned 40% quota share on 2027 new insurance written (NIW), acts as a Cash Cow by cutting required capital and boosting free cash for dividends and buybacks; in 2024 MGIC ceded about 35% of NIW, trimming statutory RBC needs by an estimated 20% and lifting return on equity.

These transfers shift loss volatility to reinsurers, lower MGIC’s capital buffers, and raise core underwriting margins; reinsuring 40% of 2027 NIW could free roughly $200–300 million in regulatory capital assuming 2024 NIW run-rate and typical loss development.

- 40% quota share on 2027 NIW

- ~35% ceded in 2024; ~20% RBC reduction

- $200–300M estimated capital freed

- Higher ROE via lower capital load

MGIC’s $303B IIF: Cash‑cow premiums fuel $720M capital returns, 12% loss ratio, 4% yield

MGIC’s primary Insurance-in-Force (>$303B by YE 2025) is the Cash Cow: steady premiums funded $420M dividends and $300M buybacks in 2025, with ~85% persistence, 12% loss ratio, $5.7B investable portfolio (4% book yield) and $62M quarterly investment income, freeing capital via ~35% reinsurance cessions and ~20% RBC relief.

| Metric | 2024/2025 |

|---|---|

| IIF | >$303B (YE 2025) |

| Dividends / Buybacks | $420M / $300M (2025) |

| Persistence | ~85% |

| Loss ratio | ~12% (2025) |

| Investable portfolio | $5.7B (4% yield) |

| Quarterly invest. income | $62M |

| NIW cession | ~35% (2024); 40% planned 2027 |

| RBC relief | ~20% |

Full Transparency, Always

MGIC BCG Matrix

The preview you're viewing is the exact MGIC BCG Matrix report you'll receive after purchase—no watermarks, no placeholders, just the fully formatted, analysis-ready document crafted for strategic use. This file matches the downloadable version precisely and is optimized for editing, printing, or presenting to clients and stakeholders. Once purchased, the final BCG Matrix is delivered immediately to your inbox with professional design and market-backed insights for direct use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

See the Bigger Picture

Explore MGIC’s BCG Matrix to see which business lines are driving growth and which may be draining resources—this snapshot highlights likely Stars, Cash Cows, Dogs, and Question Marks based on market share and growth trends. The full BCG Matrix delivers quadrant-by-quadrant placement, data-backed recommendations, and strategic actions tailored to MGIC’s evolving mortgage insurance landscape. Purchase the complete report for a ready-to-use Word analysis and Excel summary to inform investment, resource allocation, and competitive strategy.

Stars

New Insurance Written (NIW)

As of late 2025, MGIC’s New Insurance Written (NIW) is a Star in the BCG matrix, with $17.1 billion written in Q4 2025, reflecting a leading market share in the active purchase segment.

NIW captures the wave of first-time homebuyers needing mortgage insurance for low‑down‑payment loans, supporting MGIC’s top position among lenders.

The unit consumes capital to support this new volume—reserve and capital usage rose in 2025—but its growth and market leadership keep MGIC a top-tier choice for lending partners.

Advanced Risk Analytics and MiQ

MGIC’s proprietary MiQ pricing engine uses AI and data analytics to deliver granular, adaptive pricing; in 2025 MiQ helped underwrite ~30% of new policies, improving risk-adjusted margins by an estimated 120 basis points versus cohort pricing.

MiQ is a Star in the BCG matrix because it captures higher-quality loans and supports growth in the fintech-integrated mortgage market, where originations rose ~18% year-over-year in 2024.

Ongoing investment is critical: MGIC’s 2024 tech spend climbed to $95M to counter rival automated valuation and pricing models and protect this competitive advantage.

Lender-Paid Mortgage Insurance (LPMI)

Lender-Paid Mortgage Insurance (LPMI) is a high-growth MGIC product segment; industry LPMI originations rose ~18% in 2024 to $45B, and MGIC is expanding to offer flexible alternatives to borrower-paid MI that appeal to lenders who bake insurance into rates.

Targeting this niche can lift MGIC’s lender-market share—MGIC held ~24% private MI market share in 2024—and win accounts that favor rate-based pricing, but conversion needs heavy promotion and broker relationships.

To turn rapid growth into dominance, MGIC must invest in placement incentives, co-marketing, and tech integration; expect marketing and distribution spend to rise by mid-teens percent in FY2025 to capture scale.

Digital Integration and API Services

MGIC’s deep API and LOS integrations with top originators (including Ellie Mae/ICE and Blend) act as a Star by capturing high placement at point-of-sale; MGIC reported a 22% rise in digital-delivered endorsements in 2024, lifting placement with tech-enabled lenders.

These integrations meet market demand for real-time decisioning and seamless workflows—digital mortgage volume hit 48% of originations in 2024, so MGIC’s platform investments keep it the primary choice for modern lenders.

- 22% rise in digital endorsements (2024)

- 48% of originations via digital channels (2024)

- Close ties to Ellie Mae/ICE and Blend LOS

Emerging Geographic Markets

MGIC is targeting high-growth regions where U.S. Sun Belt metros saw population gains of 1.1–1.8% in 2024 versus national 0.4%, and housing permits rose 12% year-over-year; MGIC aims to capture new mortgages ahead of rivals by deploying localized underwriting and distribution.

The push requires higher marketing and acquisition spend—MGIC increased field marketing by ~22% in 2024—yet positions the firm to lead in hubs forecasted to account for ≥30% of net new single-family mortgage originations through 2027.

- Target: Sun Belt metros with 1%+ population growth

- CapEx/marketing: +22% in 2024

- Goal: capture ≥30% of new single-family originations by 2027

MGIC Soars: $17.1B NIW, MiQ ~30% Market Share, 120bps Margin Boost

MGIC’s NIW and MiQ are Stars: NIW hit $17.1B in Q4 2025; MiQ underwrote ~30% of new policies in 2025, adding ~120 bps to margins. Digital integrations raised endorsements 22% in 2024; digital mortgage share was 48%. MGIC held ~24% private MI share in 2024 and targets Sun Belt growth to capture ≥30% of new originations by 2027.

| Metric | 2024–2025 |

|---|---|

| NIW Q4 2025 | $17.1B |

| MiQ share 2025 | ~30% |

| Margin lift | ~120 bps |

| Digital endorsements | +22% (2024) |

| Private MI share | ~24% (2024) |

What is included in the product

Comprehensive BCG Matrix analysis of MGIC’s units with strategic guidance—identify Stars, Cash Cows, Question Marks, Dogs and recommended actions.

One-page MGIC BCG Matrix placing each unit in a quadrant for clear strategic prioritization

Cash Cows

Primary Insurance in Force (IIF)

Surpassing $303 billion IIF by year-end 2025, MGIC’s primary Insurance in Force is the ultimate Cash Cow, producing steady premium income and underwriting margin that funded $420 million in dividends and $300 million in buybacks in 2025.

The mature portfolio needs minimal new capital to maintain, converting low maintenance expense into free cash flow; persistence runs ~85%, keeping lifetime profits high and loss ratios stable around 12% in 2025.

Investment Portfolio Yield

With a book yield of 4% and quarterly investment income of $62 million, MGIC’s $5.7 billion portfolio functions as a reliable Cash Cow in the BCG matrix.

Disciplined fixed-income management taps the higher-for-longer 2025 rate backdrop, translating to steady, non-cyclical income that buffered MGIC through 2025 credit spread volatility.

This predictable cash flow covers administrative costs and preserves capital flexibility, supporting reserve builds and strategic optionality such as repurchases or bolt-on investments.

Established Lender Relationships

MGIC’s decades-long ties with over 1,000 national and regional lenders generate steady book flow, representing a high-market-share cash cow that accounted for roughly 60% of 2024 premium volume ($1.2B of $2.0B total), minimizing need for heavy promotion.

This mature network sustains MGIC’s market-leading position with low customer acquisition costs—loss-adjusted expense ratios held near 12% in 2024—so revenue scales with underwriting rather than marketing spend.

Legacy Underwriting Operations

MGIC’s mature underwriting operations act as a Cash Cow by cutting admin costs and boosting margins—2024 combined ratio improved to ~62%, lifting underwriting income to $1.1B and free cash flow used for tech R&D.

Decades of refined workflows process ~2.3M applications yearly with claims-cycle time down 18% since 2019, sustaining ~30% operating margin on legacy products.

- High-volume: ~2.3M applications/year

- Efficiency: combined ratio ~62% (2024)

- Profit: $1.1B underwriting income (2024)

- Margin: ~30% operating margin on legacy

- Reinvestment: free cash flow funds tech R&D

Reinsurance Program Benefits

MGIC’s quota share and excess-of-loss reinsurance, including a planned 40% quota share on 2027 new insurance written (NIW), acts as a Cash Cow by cutting required capital and boosting free cash for dividends and buybacks; in 2024 MGIC ceded about 35% of NIW, trimming statutory RBC needs by an estimated 20% and lifting return on equity.

These transfers shift loss volatility to reinsurers, lower MGIC’s capital buffers, and raise core underwriting margins; reinsuring 40% of 2027 NIW could free roughly $200–300 million in regulatory capital assuming 2024 NIW run-rate and typical loss development.

- 40% quota share on 2027 NIW

- ~35% ceded in 2024; ~20% RBC reduction

- $200–300M estimated capital freed

- Higher ROE via lower capital load

MGIC’s $303B IIF: Cash‑cow premiums fuel $720M capital returns, 12% loss ratio, 4% yield

MGIC’s primary Insurance-in-Force (>$303B by YE 2025) is the Cash Cow: steady premiums funded $420M dividends and $300M buybacks in 2025, with ~85% persistence, 12% loss ratio, $5.7B investable portfolio (4% book yield) and $62M quarterly investment income, freeing capital via ~35% reinsurance cessions and ~20% RBC relief.

| Metric | 2024/2025 |

|---|---|

| IIF | >$303B (YE 2025) |

| Dividends / Buybacks | $420M / $300M (2025) |

| Persistence | ~85% |

| Loss ratio | ~12% (2025) |

| Investable portfolio | $5.7B (4% yield) |

| Quarterly invest. income | $62M |

| NIW cession | ~35% (2024); 40% planned 2027 |

| RBC relief | ~20% |

Full Transparency, Always

MGIC BCG Matrix

The preview you're viewing is the exact MGIC BCG Matrix report you'll receive after purchase—no watermarks, no placeholders, just the fully formatted, analysis-ready document crafted for strategic use. This file matches the downloadable version precisely and is optimized for editing, printing, or presenting to clients and stakeholders. Once purchased, the final BCG Matrix is delivered immediately to your inbox with professional design and market-backed insights for direct use.