MGP Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

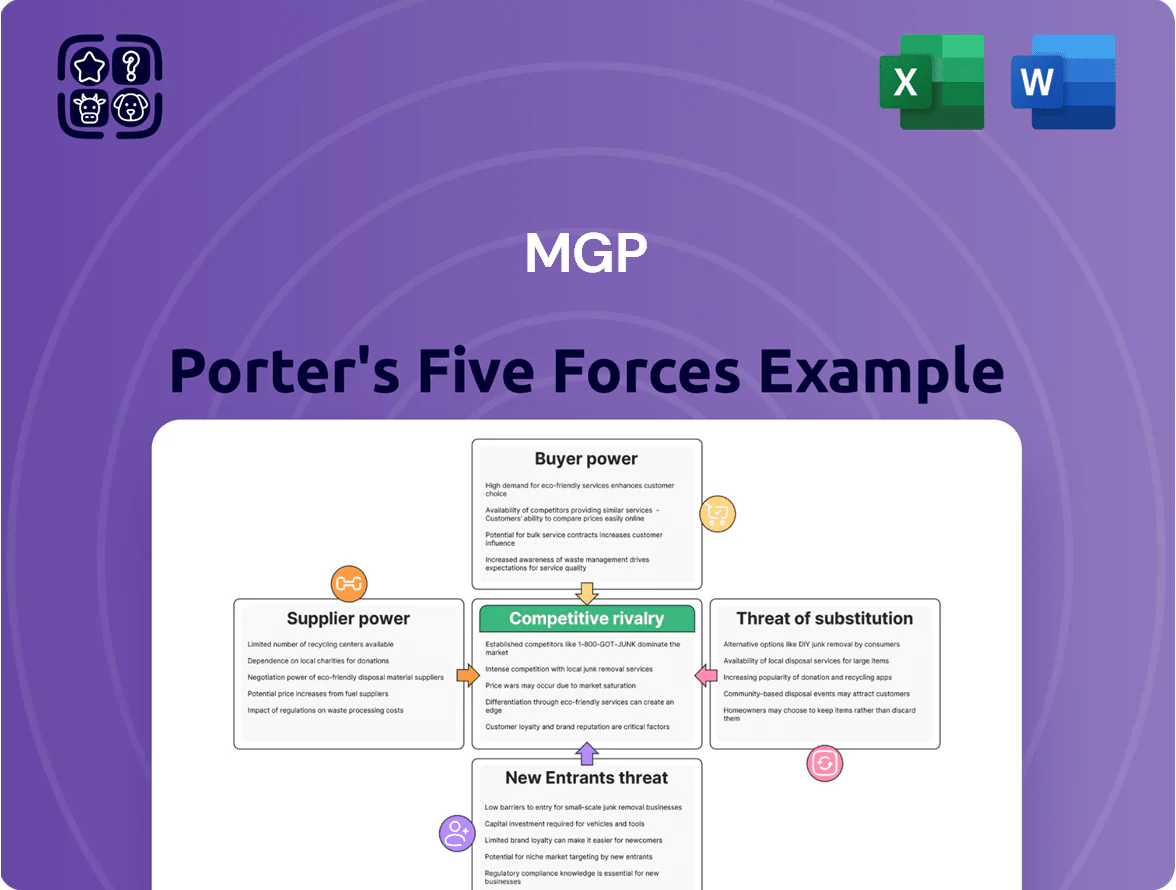

MGP faces moderate buyer power and supplier concentration, while competitive rivalry and regulatory pressures shape margin dynamics; potential new entrants and substitutes create selective risk across segments.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore MGP’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Volatility in Agricultural Raw Materials

Primary inputs corn, wheat, rye face volatile prices; CBOT corn rose 24% in 2023–2024 and droughts cut US corn yields by ~8% in 2024, raising costs for MGP’s Distilling and Ingredient Solutions segments.

MGP hedges via futures and forward contracts but remains exposed: large ag cooperatives and traders control high-quality non-GMO grain flows, giving suppliers pricing power that can lift COGS materially.

Scarcity of High-Quality Oak Barrels

The production of premium bourbon and rye needs new charred white oak barrels made by few specialized cooperages; roughly 70% of US bourbon barrels come from about 15 large cooperages as of 2025, concentrating supply and raising supplier power.

Global demand for aged spirits stayed strong in 2024–25—US whiskey exports rose ~12% in 2024—so cooperages gain leverage, since white oak growth cycles are 25–50 years, limiting near-term capacity expansion.

MGP secures barrels via multi-year contracts and capacity reservations; rising input costs pushed barrel prices up ~8–15% in 2023–25, forcing MGP to accept higher per-unit costs to ensure supply.

Energy and Utility Cost Fluctuations

Distillation and ingredient processing at MGP are energy-heavy, using large volumes of natural gas and electricity for boilers and dryers; U.S. industrial natural gas prices averaged about 3.60 USD/MMBtu in 2024, so energy suppliers exert strong leverage.

Few short-term alternatives exist for industrial-scale power, so regional gas price spikes or new carbon pricing (e.g., state-level $20–50/ton CO2 proposals) can raise COGS quickly and squeeze margins.

Specialized Enzyme and Yeast Providers

The fermentation stage needs specific yeast strains and proprietary enzymes; while they are under 5% of COGS for distillers like MGP Ingredients (MGP) in 2024, changing suppliers risks altering flavor and yield, so MGP rarely swaps vendors.

That technical lock-in gives biotech suppliers moderate leverage: they can press for tighter contracts and price premia, but MGP’s scale (2024 net sales $1.1B) and long-term sourcing reduce extreme supplier power.

- Yeast/enzymes <5% of COGS

- MGP 2024 sales $1.1B

- Technical switching risk: product profile change

- Supplier leverage: moderate, not dominant

Logistics and Freight Dependency

MGP depends on rail and trucking from Kansas and Indiana to move bulk spirits; in 2024 US rail freight rates rose ~6% while trucking spot rates were up ~12%, giving carriers pricing power.

Transport consolidation—Top 4 US railroads control ~80% of volume and large carriers handle most long-haul trucking—lets providers set schedules and fuel surcharges, which averaged 8–10% in 2024.

Network disruptions can cause inventory pileups, pushing storage costs up; a week-long delay could add tens of thousands in holding costs for bulk ethanol and aged spirits.

- Rail/truck rate increases: rail +6% (2024), trucking spot +12% (2024)

- Top 4 railroads ≈80% market share

- Fuel surcharges averaged 8–10% (2024)

- Week delays can add tens of thousands in storage for bulk spirit inventory

Supply squeeze: volatile corn, concentrated cooperages & rising energy/transport costs

Suppliers exert moderate-to-strong power: volatile grains (CBOT corn +24% 2023–24; US corn yields −8% 2024) and concentrated cooperages (≈70% barrels from ~15 cooperages, 2025) raise COGS; energy (US industrial gas ≈3.60 USD/MMBtu 2024) and transport (rail +6% 2024; trucking spot +12% 2024; top4 rail ≈80%) add leverage; yeast/enzyme costs <5% of COGS, limiting extreme supplier power.

| Input | Key stat |

|---|---|

| Corn price move | CBOT +24% (2023–24) |

| US corn yield | −8% (2024) |

| Barrel supply | ≈70% from ~15 cooperages (2025) |

| Natural gas | ≈3.60 USD/MMBtu (2024) |

| Rail/truck | Rail +6%, Truck +12% (2024); top4 rail ≈80% |

| Yeast/enzymes | <5% of COGS (2024) |

What is included in the product

Tailored for MGP, this Porter's Five Forces overview uncovers competitive drivers, supplier/buyer power, substitution risks, and entry barriers to assess pricing leverage and strategic vulnerabilities.

A concise Porter’s Five Forces snapshot tailored for MGP—quickly reveals competitive pressures, supplier/buyer dynamics, and threat levels to guide decisive strategy and investment choices.

Customers Bargaining Power

Consolidation of Wholesale Distributors

Dependence of Craft Distillers on Bulk Supply

A large share of MGP Ingredients revenue—about 40% in 2024—came from bulk sales to craft distillers that lack production capacity, creating customer dependence but also risk. As craft brands scale, they can build in-house facilities or switch to other contract distillers, raising customer bargaining power. To retain accounts MGP must compete on quality, consistency, and technical support, and invested $150m+ in capacity and R&D through 2024 to lower churn.

Price Sensitivity of Food Manufacturers

Large-scale food processors in Ingredient Solutions buy specialty wheat proteins and starches and are highly price-sensitive; ingredient costs typically account for 20–35% of COGS in processed foods, so a 5–10% price gap pushes reformulation to soy or pea proteins.

Because substitutes exist and switching costs are low, MGP’s pricing power is limited; in 2024 Ingredient Solutions gross margin was ~28%, so MGP must sell functional benefits—texture, yield, clean-label—to sustain any 10–15% premium.

Influence of National Retail Chains

Shifting Consumer Brand Loyalty

End consumers are more experimental, shifting between brands and categories by trend and perceived authenticity, so MGP’s branded spirits must spend more on marketing to keep pull as switching costs between bourbon or gin bottles remain low.

Power sits with rapidly changing consumer tastes—new flavor profiles and a rise in non-alcoholic alternatives cut into sales; MGP reported branded net sales growth of 18% in FY2024 but higher A&P spend as a share of sales, rising to ~12%.

- Consumers: low switching cost, trend-driven

- MGP response: higher marketing spend (~12% of branded sales in 2024)

- Risk: rapid taste shifts to flavors/non-alc

- Impact: volatility in branded revenue despite 18% FY2024 growth

MGP under distributor pressure: heavy contract/bulk mix forces $150M+ investments

| Metric | 2024 |

|---|---|

| Distributor share | 40–50% |

| Southern Glazer’s rev | $10.7B |

| MGP contract/private-label | ~41% |

| Bulk sales share | ~40% |

| Ingredient margin | ~28% |

| Branded growth | +18% |

| A&P share | ~12% |

| Capacity/R&D spend | $150M+ |

Full Version Awaits

MGP Porter's Five Forces Analysis

This preview shows the exact MGP Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders, no mockups, fully formatted and ready for use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

MGP faces moderate buyer power and supplier concentration, while competitive rivalry and regulatory pressures shape margin dynamics; potential new entrants and substitutes create selective risk across segments.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore MGP’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Volatility in Agricultural Raw Materials

Primary inputs corn, wheat, rye face volatile prices; CBOT corn rose 24% in 2023–2024 and droughts cut US corn yields by ~8% in 2024, raising costs for MGP’s Distilling and Ingredient Solutions segments.

MGP hedges via futures and forward contracts but remains exposed: large ag cooperatives and traders control high-quality non-GMO grain flows, giving suppliers pricing power that can lift COGS materially.

Scarcity of High-Quality Oak Barrels

The production of premium bourbon and rye needs new charred white oak barrels made by few specialized cooperages; roughly 70% of US bourbon barrels come from about 15 large cooperages as of 2025, concentrating supply and raising supplier power.

Global demand for aged spirits stayed strong in 2024–25—US whiskey exports rose ~12% in 2024—so cooperages gain leverage, since white oak growth cycles are 25–50 years, limiting near-term capacity expansion.

MGP secures barrels via multi-year contracts and capacity reservations; rising input costs pushed barrel prices up ~8–15% in 2023–25, forcing MGP to accept higher per-unit costs to ensure supply.

Energy and Utility Cost Fluctuations

Distillation and ingredient processing at MGP are energy-heavy, using large volumes of natural gas and electricity for boilers and dryers; U.S. industrial natural gas prices averaged about 3.60 USD/MMBtu in 2024, so energy suppliers exert strong leverage.

Few short-term alternatives exist for industrial-scale power, so regional gas price spikes or new carbon pricing (e.g., state-level $20–50/ton CO2 proposals) can raise COGS quickly and squeeze margins.

Specialized Enzyme and Yeast Providers

The fermentation stage needs specific yeast strains and proprietary enzymes; while they are under 5% of COGS for distillers like MGP Ingredients (MGP) in 2024, changing suppliers risks altering flavor and yield, so MGP rarely swaps vendors.

That technical lock-in gives biotech suppliers moderate leverage: they can press for tighter contracts and price premia, but MGP’s scale (2024 net sales $1.1B) and long-term sourcing reduce extreme supplier power.

- Yeast/enzymes <5% of COGS

- MGP 2024 sales $1.1B

- Technical switching risk: product profile change

- Supplier leverage: moderate, not dominant

Logistics and Freight Dependency

MGP depends on rail and trucking from Kansas and Indiana to move bulk spirits; in 2024 US rail freight rates rose ~6% while trucking spot rates were up ~12%, giving carriers pricing power.

Transport consolidation—Top 4 US railroads control ~80% of volume and large carriers handle most long-haul trucking—lets providers set schedules and fuel surcharges, which averaged 8–10% in 2024.

Network disruptions can cause inventory pileups, pushing storage costs up; a week-long delay could add tens of thousands in holding costs for bulk ethanol and aged spirits.

- Rail/truck rate increases: rail +6% (2024), trucking spot +12% (2024)

- Top 4 railroads ≈80% market share

- Fuel surcharges averaged 8–10% (2024)

- Week delays can add tens of thousands in storage for bulk spirit inventory

Supply squeeze: volatile corn, concentrated cooperages & rising energy/transport costs

Suppliers exert moderate-to-strong power: volatile grains (CBOT corn +24% 2023–24; US corn yields −8% 2024) and concentrated cooperages (≈70% barrels from ~15 cooperages, 2025) raise COGS; energy (US industrial gas ≈3.60 USD/MMBtu 2024) and transport (rail +6% 2024; trucking spot +12% 2024; top4 rail ≈80%) add leverage; yeast/enzyme costs <5% of COGS, limiting extreme supplier power.

| Input | Key stat |

|---|---|

| Corn price move | CBOT +24% (2023–24) |

| US corn yield | −8% (2024) |

| Barrel supply | ≈70% from ~15 cooperages (2025) |

| Natural gas | ≈3.60 USD/MMBtu (2024) |

| Rail/truck | Rail +6%, Truck +12% (2024); top4 rail ≈80% |

| Yeast/enzymes | <5% of COGS (2024) |

What is included in the product

Tailored for MGP, this Porter's Five Forces overview uncovers competitive drivers, supplier/buyer power, substitution risks, and entry barriers to assess pricing leverage and strategic vulnerabilities.

A concise Porter’s Five Forces snapshot tailored for MGP—quickly reveals competitive pressures, supplier/buyer dynamics, and threat levels to guide decisive strategy and investment choices.

Customers Bargaining Power

Consolidation of Wholesale Distributors

Dependence of Craft Distillers on Bulk Supply

A large share of MGP Ingredients revenue—about 40% in 2024—came from bulk sales to craft distillers that lack production capacity, creating customer dependence but also risk. As craft brands scale, they can build in-house facilities or switch to other contract distillers, raising customer bargaining power. To retain accounts MGP must compete on quality, consistency, and technical support, and invested $150m+ in capacity and R&D through 2024 to lower churn.

Price Sensitivity of Food Manufacturers

Large-scale food processors in Ingredient Solutions buy specialty wheat proteins and starches and are highly price-sensitive; ingredient costs typically account for 20–35% of COGS in processed foods, so a 5–10% price gap pushes reformulation to soy or pea proteins.

Because substitutes exist and switching costs are low, MGP’s pricing power is limited; in 2024 Ingredient Solutions gross margin was ~28%, so MGP must sell functional benefits—texture, yield, clean-label—to sustain any 10–15% premium.

Influence of National Retail Chains

Shifting Consumer Brand Loyalty

End consumers are more experimental, shifting between brands and categories by trend and perceived authenticity, so MGP’s branded spirits must spend more on marketing to keep pull as switching costs between bourbon or gin bottles remain low.

Power sits with rapidly changing consumer tastes—new flavor profiles and a rise in non-alcoholic alternatives cut into sales; MGP reported branded net sales growth of 18% in FY2024 but higher A&P spend as a share of sales, rising to ~12%.

- Consumers: low switching cost, trend-driven

- MGP response: higher marketing spend (~12% of branded sales in 2024)

- Risk: rapid taste shifts to flavors/non-alc

- Impact: volatility in branded revenue despite 18% FY2024 growth

MGP under distributor pressure: heavy contract/bulk mix forces $150M+ investments

| Metric | 2024 |

|---|---|

| Distributor share | 40–50% |

| Southern Glazer’s rev | $10.7B |

| MGP contract/private-label | ~41% |

| Bulk sales share | ~40% |

| Ingredient margin | ~28% |

| Branded growth | +18% |

| A&P share | ~12% |

| Capacity/R&D spend | $150M+ |

Full Version Awaits

MGP Porter's Five Forces Analysis

This preview shows the exact MGP Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders, no mockups, fully formatted and ready for use.