Micro-Tech Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

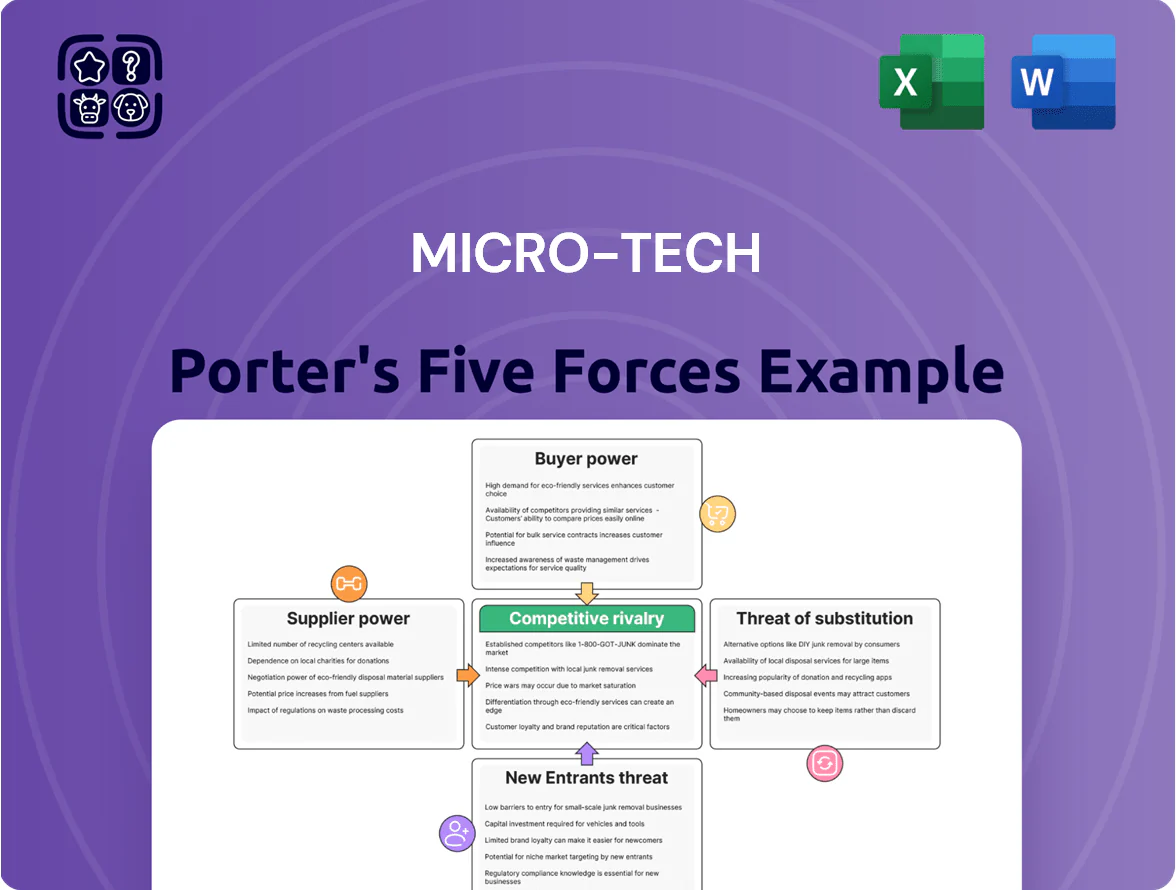

Micro-Tech faces moderate supplier power, aggressive peer rivalry, and a rising threat from substitutes driven by rapid tech shifts, while customer bargaining and entry barriers vary across product lines.

This brief snapshot only scratches the surface; unlock the full Porter's Five Forces Analysis to explore Micro-Tech’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Raw Material Dependency

Nanjing Micro-Tech depends on certified medical-grade stainless steel, nitinol, and specialty polymers for endoscopic tools; global-certified suppliers number under 30 for nitinol and ~120 for medical-grade stainless steel as of 2025, concentrating supply.

Basic feeds are commoditized, yet ISO 13485 and FDA 510(k) requirements cut qualified vendors, raising switching costs and single-source risk for ~15–20% of SKUs.

Supplier concentration gives a moderate bargaining power: price pressure limited, but supply disruption could delay >3 months of production and affect ~12% of FY2024 revenue.

Technological Integration of Components

As Micro-Tech shifts to advanced visualization and robotic-assisted devices, reliance on high-tech sensors and ASICs rises, and roughly 60–70% of these parts come from a handful of suppliers, boosting supplier leverage on price and 12–24 week lead times.

Digital integration in gastroenterology makes tech partnerships strategic: 2024 device OEMs reported 18% higher COGS when single-sourcing critical electronics, so supplier terms directly affect margins and product timelines.

High Switching Costs for Certified Inputs

Switching certified suppliers in medical devices forces re-validation and often new filings with regulators like FDA or NMPA, which can cost $0.5–$5M and take 6–18 months per component; these administrative and technical burdens make Nanjing Micro-Tech unlikely to switch frequently to chase small price cuts.

As a result, incumbent suppliers keep steady bargaining power—Micro-Tech reported 62% of critical components single- or dual-sourced in 2024, so supplier-led price and delivery leverage remains high.

Supplier Concentration in High-End Alloys

The nitinol (shape-memory alloy) market is concentrated: top 3 global suppliers held ~65% of medical-grade nitinol supply in 2024, giving them pricing and lead-time power over Nanjing Micro-Tech’s stent and biopsy-forceps production.

Nanjing Micro-Tech pursues domestic substitutes—local mills grew medical-grade output ~28% in 2023—but global grades still outperform on fatigue life and regulatory track records, so suppliers can dictate specs and premium pricing.

- Top 3 suppliers ~65% market share (2024)

- Local supply +28% output (2023)

- Global grades lead on fatigue life, regulatory approvals

- Supplier terms affect pricing, lead times, product specs

Impact of Global Supply Chain Volatility

By end-2025, regional trade shifts cut availability of specialized medical components by an estimated 12% in China-imported volumes, letting suppliers in stable regions charge 8–15% premiums for guaranteed lead times.

Nanjing Micro-Tech must weigh cost versus resilience, targeting a 30–40% multi-sourced supply mix and keeping strategic inventory equal to 60 days of sales to blunt supplier leverage.

- 12% drop in China-imported component volumes

- 8–15% supplier premium in aligned regions

- 30–40% target multi-sourced mix

- 60 days strategic inventory

High supplier power: 65% nitinol concentration puts 12% revenue at risk, targets 30–40% multi-sourcing

Supplier power is high: top-3 nitinol suppliers held ~65% (2024), 62% of Micro-Tech critical parts were single/dual-sourced (2024), and supplier-led delays can cut >3 months production impacting ~12% of FY2024 revenue; switching costs (validation, filings) range $0.5–5M and 6–18 months, so Micro-Tech targets 30–40% multi-sourcing and 60 days inventory.

| Metric | Value |

|---|---|

| Top-3 nitinol share (2024) | 65% |

| Critical single/dual-sourced | 62% |

| Revenue at risk (delay) | 12% |

| Switch cost/time | $0.5–5M / 6–18m |

| Target multi-sourcing | 30–40% |

| Strategic inventory | 60 days |

What is included in the product

Concise Porter's Five Forces for Micro-Tech: evaluates competitive rivalry, supplier and buyer power, threat of new entrants and substitutes, and highlights disruptive risks and protective dynamics to inform strategy and valuation.

A concise, one-sheet Porter's Five Forces snapshot for Micro-Tech that highlights competitive pressures and strategic levers—ideal for quick boardroom decisions.

Customers Bargaining Power

Concentrated Hospital Purchasing Groups

Government-Led Centralized Procurement

In China, volume-based procurement (VBP) now covers medical consumables worth over CNY 120 billion (2024 MOF data), shifting bargaining power to state health authorities and forcing price-driven competition.

VBP tendering has cut some suppliers’ ASPs by 30–60%, so Nanjing Micro-Tech must bid aggressively in tenders to retain hospital shelf space while defending margins.

Low Switching Costs for Consumables

High Clinical Demand for Innovation

Surgeons prioritize innovative features that boost outcomes and speed; price matters less for devices that reduce complications or OR time. When Nanjing Micro-Tech offers patented tools for complex endovascular or cardiac procedures, customer bargaining falls because substitutes are scarce. The firm’s R&D — >10% of revenue in 2024 — creates must-have devices that offset price pressure on commodity lines.

- Patented solutions reduce alternatives

- Surgeon demand raises willingness to pay

- R&D >10% of revenue (2024)

- MUST-HAVE tools lower customer power

Information Transparency and Benchmarking

Modern procurement teams use analytics to benchmark device price and outcomes, comparing Nanjing Micro-Tech to Boston Scientific and Olympus; in 2024 hospital group tenders showed 18–25% price pressure when outcomes were equivalent.

Real-time dashboards and registries (e.g., national device registries) force transparent comparisons, so Micro-Tech can’t sustain premium pricing without documented clinical benefit.

- Procurement analytics drive 18–25% price compression

- Real-time benchmarking vs Boston Scientific, Olympus

- Premium margins require documented outcome delta

GPOs & VBP squeeze Nanjing Micro‑Tech margins despite high‑R&D, patented devices

Large hospital groups/GPOs drive 35–45% of Nanjing Micro‑Tech revenue, forcing double‑digit discounts and 60–120 day terms that cut gross margin ~3–6 ppt; VBP (CNY 120bn+ in 2024) and procurement analytics compressed ASPs 18–25% in equivalent‑outcome tenders; patented, high‑R&D (>10% rev) devices reduce buyer power for complex procedures.

| Metric | Value (2024) |

|---|---|

| Revenue from hospital groups/GPOs | 35–45% |

| VBP market size | CNY 120+ bn |

| ASP compression in tenders | 18–25% |

| Gross margin hit from terms | 3–6 ppt |

| R&D spend | >10% of revenue |

What You See Is What You Get

Micro-Tech Porter's Five Forces Analysis

This preview shows the exact Micro-Tech Porter's Five Forces analysis you'll receive immediately after purchase—fully formatted, professional, and ready for use with no placeholders or mockups.

The document displayed here is the same complete file available for instant download once you buy, containing the full competitive assessment and actionable insights.

No samples or excerpts — what you see is the final deliverable, ready to support decision-making the moment payment is completed.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

Micro-Tech faces moderate supplier power, aggressive peer rivalry, and a rising threat from substitutes driven by rapid tech shifts, while customer bargaining and entry barriers vary across product lines.

This brief snapshot only scratches the surface; unlock the full Porter's Five Forces Analysis to explore Micro-Tech’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Raw Material Dependency

Nanjing Micro-Tech depends on certified medical-grade stainless steel, nitinol, and specialty polymers for endoscopic tools; global-certified suppliers number under 30 for nitinol and ~120 for medical-grade stainless steel as of 2025, concentrating supply.

Basic feeds are commoditized, yet ISO 13485 and FDA 510(k) requirements cut qualified vendors, raising switching costs and single-source risk for ~15–20% of SKUs.

Supplier concentration gives a moderate bargaining power: price pressure limited, but supply disruption could delay >3 months of production and affect ~12% of FY2024 revenue.

Technological Integration of Components

As Micro-Tech shifts to advanced visualization and robotic-assisted devices, reliance on high-tech sensors and ASICs rises, and roughly 60–70% of these parts come from a handful of suppliers, boosting supplier leverage on price and 12–24 week lead times.

Digital integration in gastroenterology makes tech partnerships strategic: 2024 device OEMs reported 18% higher COGS when single-sourcing critical electronics, so supplier terms directly affect margins and product timelines.

High Switching Costs for Certified Inputs

Switching certified suppliers in medical devices forces re-validation and often new filings with regulators like FDA or NMPA, which can cost $0.5–$5M and take 6–18 months per component; these administrative and technical burdens make Nanjing Micro-Tech unlikely to switch frequently to chase small price cuts.

As a result, incumbent suppliers keep steady bargaining power—Micro-Tech reported 62% of critical components single- or dual-sourced in 2024, so supplier-led price and delivery leverage remains high.

Supplier Concentration in High-End Alloys

The nitinol (shape-memory alloy) market is concentrated: top 3 global suppliers held ~65% of medical-grade nitinol supply in 2024, giving them pricing and lead-time power over Nanjing Micro-Tech’s stent and biopsy-forceps production.

Nanjing Micro-Tech pursues domestic substitutes—local mills grew medical-grade output ~28% in 2023—but global grades still outperform on fatigue life and regulatory track records, so suppliers can dictate specs and premium pricing.

- Top 3 suppliers ~65% market share (2024)

- Local supply +28% output (2023)

- Global grades lead on fatigue life, regulatory approvals

- Supplier terms affect pricing, lead times, product specs

Impact of Global Supply Chain Volatility

By end-2025, regional trade shifts cut availability of specialized medical components by an estimated 12% in China-imported volumes, letting suppliers in stable regions charge 8–15% premiums for guaranteed lead times.

Nanjing Micro-Tech must weigh cost versus resilience, targeting a 30–40% multi-sourced supply mix and keeping strategic inventory equal to 60 days of sales to blunt supplier leverage.

- 12% drop in China-imported component volumes

- 8–15% supplier premium in aligned regions

- 30–40% target multi-sourced mix

- 60 days strategic inventory

High supplier power: 65% nitinol concentration puts 12% revenue at risk, targets 30–40% multi-sourcing

Supplier power is high: top-3 nitinol suppliers held ~65% (2024), 62% of Micro-Tech critical parts were single/dual-sourced (2024), and supplier-led delays can cut >3 months production impacting ~12% of FY2024 revenue; switching costs (validation, filings) range $0.5–5M and 6–18 months, so Micro-Tech targets 30–40% multi-sourcing and 60 days inventory.

| Metric | Value |

|---|---|

| Top-3 nitinol share (2024) | 65% |

| Critical single/dual-sourced | 62% |

| Revenue at risk (delay) | 12% |

| Switch cost/time | $0.5–5M / 6–18m |

| Target multi-sourcing | 30–40% |

| Strategic inventory | 60 days |

What is included in the product

Concise Porter's Five Forces for Micro-Tech: evaluates competitive rivalry, supplier and buyer power, threat of new entrants and substitutes, and highlights disruptive risks and protective dynamics to inform strategy and valuation.

A concise, one-sheet Porter's Five Forces snapshot for Micro-Tech that highlights competitive pressures and strategic levers—ideal for quick boardroom decisions.

Customers Bargaining Power

Concentrated Hospital Purchasing Groups

Government-Led Centralized Procurement

In China, volume-based procurement (VBP) now covers medical consumables worth over CNY 120 billion (2024 MOF data), shifting bargaining power to state health authorities and forcing price-driven competition.

VBP tendering has cut some suppliers’ ASPs by 30–60%, so Nanjing Micro-Tech must bid aggressively in tenders to retain hospital shelf space while defending margins.

Low Switching Costs for Consumables

High Clinical Demand for Innovation

Surgeons prioritize innovative features that boost outcomes and speed; price matters less for devices that reduce complications or OR time. When Nanjing Micro-Tech offers patented tools for complex endovascular or cardiac procedures, customer bargaining falls because substitutes are scarce. The firm’s R&D — >10% of revenue in 2024 — creates must-have devices that offset price pressure on commodity lines.

- Patented solutions reduce alternatives

- Surgeon demand raises willingness to pay

- R&D >10% of revenue (2024)

- MUST-HAVE tools lower customer power

Information Transparency and Benchmarking

Modern procurement teams use analytics to benchmark device price and outcomes, comparing Nanjing Micro-Tech to Boston Scientific and Olympus; in 2024 hospital group tenders showed 18–25% price pressure when outcomes were equivalent.

Real-time dashboards and registries (e.g., national device registries) force transparent comparisons, so Micro-Tech can’t sustain premium pricing without documented clinical benefit.

- Procurement analytics drive 18–25% price compression

- Real-time benchmarking vs Boston Scientific, Olympus

- Premium margins require documented outcome delta

GPOs & VBP squeeze Nanjing Micro‑Tech margins despite high‑R&D, patented devices

Large hospital groups/GPOs drive 35–45% of Nanjing Micro‑Tech revenue, forcing double‑digit discounts and 60–120 day terms that cut gross margin ~3–6 ppt; VBP (CNY 120bn+ in 2024) and procurement analytics compressed ASPs 18–25% in equivalent‑outcome tenders; patented, high‑R&D (>10% rev) devices reduce buyer power for complex procedures.

| Metric | Value (2024) |

|---|---|

| Revenue from hospital groups/GPOs | 35–45% |

| VBP market size | CNY 120+ bn |

| ASP compression in tenders | 18–25% |

| Gross margin hit from terms | 3–6 ppt |

| R&D spend | >10% of revenue |

What You See Is What You Get

Micro-Tech Porter's Five Forces Analysis

This preview shows the exact Micro-Tech Porter's Five Forces analysis you'll receive immediately after purchase—fully formatted, professional, and ready for use with no placeholders or mockups.

The document displayed here is the same complete file available for instant download once you buy, containing the full competitive assessment and actionable insights.

No samples or excerpts — what you see is the final deliverable, ready to support decision-making the moment payment is completed.